Resources

About Us

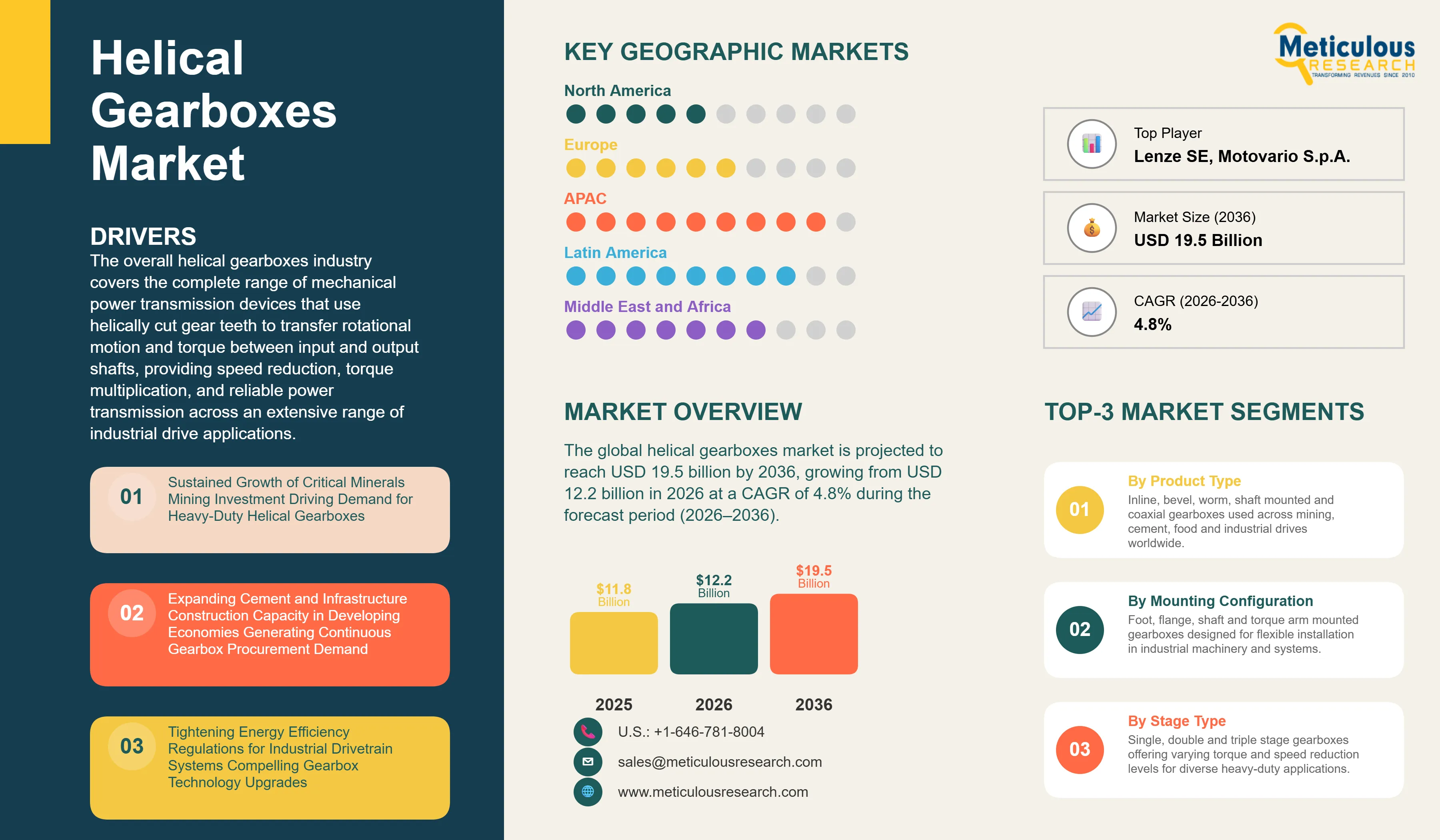

The global helical gearboxes market was valued at USD 11.8 billion in 2025. The market is projected to reach USD 19.5 billion by 2036, growing from USD 12.2 billion in 2026 at a CAGR of 4.8% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall helical gearboxes industry covers the complete range of mechanical power transmission devices that use helically cut gear teeth to transfer rotational motion and torque between input and output shafts, providing speed reduction, torque multiplication, and reliable power transmission across an extensive range of industrial drive applications. The market includes inline and parallel shaft helical gearboxes, bevel helical gearboxes, helical worm gearboxes, shaft mounted helical gearboxes, and coaxial helical inline gearboxes, deployed across end-use industries including mining and minerals processing, cement and construction materials, food and beverage processing, metals and steel, chemical and petrochemical processing, water and wastewater treatment, power generation, and packaging. These products are manufactured and marketed by leading global drivetrain equipment suppliers including FLENDER GmbH, SEW-Eurodrive GmbH & Co KG, Bonfiglioli Riduttori S.p.A., Getriebebau NORD GmbH & Co. KG, and Regal Rexnord Corporation, among others, across a broad spectrum of power ratings, gear ratios, and application-specific design configurations.

Helical gearboxes play a critical role in process and manufacturing industries, where dependable, efficient, and accurately controlled mechanical power transmission is vital for optimal plant operations. Their smooth and low-noise performance, achieved through the gradual meshing of helically cut gear teeth, along with high power density and the availability of specialized variants such as food-grade stainless steel models, explosion-proof units, and corrosion-resistant designs, has established them as the preferred gearbox solution for most new industrial drivetrain installations worldwide. Additionally, the ongoing replacement of traditional worm gearboxes and older spur gear systems with helical and hybrid helical configurations during modernization and retrofit projects continues to act as a key structural growth driver, expanding the installed base across a wide range of industrial applications.

The growth of the helical gearboxes market is primarily driven by sustained capital investment in mining and mineral processing infrastructure, the ongoing expansion of cement and construction materials production capacity in developing economies, and the accelerating buildout of food and beverage processing facilities across Asia Pacific, Africa, and the Middle East. In the mining sector, the global energy transition is intensifying demand for copper, lithium, cobalt, nickel, and other critical minerals, driving large-scale mine development and processing plant construction that requires significant quantities of high-torque helical gearboxes for grinding mill drives, conveyor systems, hoists, and mineral processing equipment. According to the International Energy Agency's Critical Minerals Market Review 2024, global investment in critical mineral supply chains reached a record level in 2023 and continued to grow through 2024, with mining and processing infrastructure representing the majority of committed capital expenditure. This investment directly translates into demand for large industrial gearboxes, particularly bevel helical and heavy-duty inline configurations capable of transmitting the torque levels required at the scale of modern mining and concentration operations.

In parallel, the global drive toward industrial energy efficiency is reshaping gearbox procurement decisions as operators seek to reduce drivetrain energy losses and comply with tightening efficiency standards governing electric motors and associated mechanical transmission equipment. The European Union's Ecodesign Regulation (EU) 2019/1781, which established mandatory IE3 and IE4 efficiency requirements for electric motors, has accelerated system-level drivetrain optimization reviews across European industrial operators, prompting simultaneous evaluation and upgrading of gearbox components to reduce overall drivetrain losses. China's revised motor efficiency standard GB 18613-2020, which mandated IE3-equivalent minimum efficiency for general-purpose motors effective July 2021, has had a comparable effect on industrial drivetrain upgrade investment across the Chinese manufacturing sector. These efficiency mandates are driving replacement cycles that create recurring demand for modern, low-loss helical gearbox designs incorporating precision-ground gear teeth and optimized internal geometries that minimize churning and friction-induced energy waste across the drivetrain.

Despite strong underlying growth fundamentals, the helical gearboxes market faces challenges related to the high cost and long lead times associated with large custom-engineered gearbox specifications for mining and cement applications, where individual units can require several months of manufacturing and assembly time. The complexity of maintaining adequate stocking and service infrastructure across geographically dispersed mining and industrial operations also adds to the total cost of ownership for operators managing distributed gearbox fleets. The presence of a large and fragmented aftermarket for refurbished and remanufactured gearboxes in price-sensitive emerging markets creates competitive pricing pressure for original equipment manufacturers, particularly in standard and medium-sized product categories where differentiation on technical specifications alone is limited.

The rapid expansion of critical minerals mining capacity across Sub-Saharan Africa, Latin America, and Southeast Asia is creating structurally new demand pools for heavy-duty helical gearboxes in regions where market penetration by global OEM suppliers has historically been constrained by distribution and service infrastructure gaps. The growing adoption of hygienic and food-grade helical gearbox designs in food and beverage processing applications in emerging markets is opening a premium, high-growth segment for manufacturers that invest in region-specific product approvals and local distribution capabilities. In addition, the increasing integration of condition monitoring sensors and digital connectivity into helical gearbox platforms is creating service-based revenue opportunities that extend the commercial relationship between gearbox manufacturers and industrial operators beyond the initial equipment sale, improving customer retention and providing predictable aftermarket revenue streams.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 19.5 Billion |

|

Market Size in 2026 |

USD 12.2 Billion |

|

Market Size in 2025 |

USD 11.8 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 4.8% |

|

Dominating Product Type |

Inline/Parallel Shaft Helical Gearboxes |

|

Fastest Growing Product Type |

Bevel Helical Gearboxes |

|

Dominating Mounting Configuration |

Foot Mounted |

|

Fastest Growing Mounting Configuration |

Flange Mounted |

|

Dominating Stage |

Double Stage |

|

Fastest Growing Stage |

Triple Stage and Above |

|

Dominating End-use Industry |

Mining & Minerals Processing |

|

Fastest Growing End-use Industry |

Food & Beverage Processing |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Global Energy Efficiency Mandates and Drivetrain Optimization Requirements Compelling Helical Gearbox Technology Upgrades

The tightening of electric motor and industrial drivetrain efficiency regulations across major manufacturing economies is establishing energy efficiency as a primary purchasing criterion for helical gearboxes in new installations and replacement cycles alike. The European Union's Ecodesign Regulation (EU) 2019/1781 set mandatory IE3 minimum efficiency requirements for motors above 0.75 kW and introduced IE4 Super Premium efficiency requirements for motors in the 75 kW to 200 kW range, effective from July 2023. This regulation directly affects the electric motor component of gearmotor assemblies and has prompted European industrial operators to undertake comprehensive drivetrain audits that invariably extend to the gearbox stage of the drivetrain, given that gearbox transmission losses can represent a meaningful share of total drivetrain energy consumption in older or poorly maintained designs. The resulting replacement procurement cycles are creating sustained demand for modern helical gearbox designs incorporating precision-ground gears, low-viscosity synthetic lubricants, and optimized housing geometries that minimize churning and friction losses compared to the aging equipment they replace.

China's implementation of GB 18613-2020 represents a comparable regulatory inflection point for the world's largest industrial market. The standard, which mandated IE3-equivalent minimum efficiency requirements for electric motors across a broad range of power ratings from July 2021, catalyzed a widespread replacement cycle across China's industrial sector as aging below-standard motor and gearbox combinations are progressively retired. Major manufacturers of industrial drivetrain equipment have responded to this transition by expanding their offerings of energy-efficient gearmotor systems integrating IE3 and IE4 motors with modern helical gearboxes, intensifying price competition in the mass-market segment while also generating a volume-growth tailwind for helical gearbox procurement. Similar efficiency regulatory initiatives are advancing in India under the Bureau of Energy Efficiency's STAR labeling program for electric motors and in Southeast Asian markets under national energy efficiency action plans aligned with the ASEAN Energy Cooperation Framework.

Beyond direct motor efficiency mandates, the European Commission's Ecodesign Working Plan has identified mechanical power transmissions including industrial gearboxes as a product group under active study for potential future ecodesign efficiency requirements. While no standalone gearbox-specific regulation has yet been finalized, the directional signal from the regulatory environment is clear: transmission efficiency will increasingly become a compliance requirement rather than merely a commercial differentiator. Leading manufacturers including FLENDER GmbH, SEW-Eurodrive GmbH & Co KG, and Getriebebau NORD GmbH & Co. KG are already positioning their product portfolios accordingly, investing in gear geometry optimization, surface finishing technology, and bearing specification upgrades that reduce gearbox no-load and load-dependent losses. This regulatory-driven transition is accelerating the displacement of older worm gear and conventional spur gear reducers across general industrial applications, structurally expanding the installed base replacement opportunity for modern helical gearbox technology over the forecast period.

Critical Minerals Mining Expansion and Global Infrastructure Investment Driving Sustained Demand for Heavy-Duty Helical Gearbox Systems

The global transition to renewable energy and electrified transportation is creating an unprecedented structural demand surge for critical minerals including copper, lithium, cobalt, and nickel, driving a multi-year wave of new mine development and processing plant investment that represents one of the most significant growth drivers for large industrial helical gearboxes in the current decade. According to the International Energy Agency's Critical Minerals Market Review 2024, approved capital commitments for new critical mineral mining and processing projects globally have reached levels not seen since the commodity supercycle of the early 2000s, with copper, lithium, and nickel projects accounting for the majority of announced investment. Each new large-scale copper concentrator, lithium processing facility, or nickel smelter requires multiple heavy-duty helical gearboxes including multi-megawatt grinding mill drives, large conveyor drive gearboxes, and kiln or rotary dryer drive units, with individual gearbox values in large grinding mill drive applications ranging from several hundred thousand to several million U.S. dollars depending on the application and power rating.

In parallel, large-scale infrastructure development programs in emerging and developing economies are sustaining demand for cement-grade helical gearboxes used in vertical roller mills, ball mills, and kiln drive applications. According to the United States Geological Survey Mineral Commodity Summaries 2025, global cement production remained at approximately 4.1 billion metric tons in 2024, with China accounting for approximately 55% of global output and India maintaining its position as the second-largest producer with continued capacity expansion underway across multiple states. India's National Infrastructure Pipeline, which encompasses road, rail, urban, and industrial infrastructure projects valued at over USD 1.4 trillion through 2030, is a directly relevant driver of cement production investment and the associated demand for large kiln and mill drive gearboxes that sustains procurement activity across both new capacity installations and plant modernization programs.

The mining capital expenditure cycle is also being driven by the geographic expansion of mining operations into frontier regions including Sub-Saharan Africa, Central Asia, and remote areas of Latin America, where new mining infrastructure requires procurement of complete drivetrain equipment packages. This regional expansion is increasing the total addressable market for heavy-duty helical gearboxes by bringing previously untapped project pipelines into active procurement cycles. Manufacturers such as FLENDER GmbH, David Brown Santasalo, and Elecon Engineering Company Limited have well-established capabilities in mining-grade helical gearbox engineering and are actively pursuing this expanding project pipeline. The growing scale of individual mining projects, which increasingly require single grinding mill gearboxes rated at 10 MW and above, is also increasing the average selling price per unit in the mining gearbox segment, positively influencing market revenue growth rates beyond what underlying unit volume growth would alone indicate.

Modular Gearmotor Integration and Smart Condition Monitoring Platforms Reshaping Helical Gearbox Ownership Economics

The evolution of helical gearboxes from standalone mechanical components toward integrated gearmotor systems with embedded digital monitoring capabilities represents the most significant structural change in the commercial model of the helical gearboxes market over the current decade. Leading manufacturers including SEW-Eurodrive GmbH & Co KG, Getriebebau NORD GmbH & Co. KG, and Lenze SE have developed highly modular gearmotor platforms that combine helical gearboxes with motors, frequency inverters, and decentralized control electronics into unified field-installable assemblies that reduce wiring complexity, installation time, and control panel space requirements compared to separately sourced drive components. SEW-Eurodrive's MOVI-C modular automation system and Nord Drivesystems' NORDAC decentralized drive technology exemplify this integration trend, enabling machine builders and system integrators to deploy complete drive units with standardized interfaces and programming environments that reduce total system cost and accelerate commissioning timelines for automated manufacturing equipment.

The incorporation of condition monitoring sensors and cloud-connected analytics into helical gearbox platforms is transforming how industrial operators manage gearbox maintenance across large equipment fleets. Traditionally, gearbox service intervals were defined by calendar-based schedules or fixed operating hour thresholds that often did not reflect actual gearbox condition, leading either to premature lubricant changes and unnecessary planned downtime or to undetected gear tooth fatigue and bearing wear that resulted in unexpected failures. Connected gearbox platforms from manufacturers including FLENDER GmbH, whose FLENDER Connect system provides real-time vibration monitoring, oil temperature tracking, and cloud-based analytics for installed gearbox fleets, and Sumitomo Drive Technologies are enabling condition-based maintenance strategies that extend service intervals, reduce lubricant consumption, and provide early warning of developing faults before they result in catastrophic failure and unplanned production stoppage.

The business case for connected helical gearbox platforms is particularly compelling in mining and cement applications, where unexpected gearbox failure on a grinding mill or kiln drive can halt production for days or weeks and result in significant revenue losses and contractual penalties. The integration of digital twin technology into gearbox performance management is further strengthening this value proposition, enabling operators to simulate the remaining service life of critical gearbox components under current operating conditions and optimize maintenance scheduling accordingly. As the cost of IoT hardware and cloud connectivity continues to decline, the economics of connected gearbox monitoring are becoming attractive not only for the largest industrial installations but also for medium-sized facilities across food processing, water treatment, and chemical manufacturing. This broadening of the addressable market for connected gearbox technology is accelerating the transition from transactional equipment procurement toward subscription-based performance management service models that improve customer retention and create predictable recurring revenue streams for manufacturers that invest in this capability.

By Product Type: In 2026, the Inline/Parallel Shaft Helical Gearboxes Segment to Dominate the Global Helical Gearboxes Market

Based on product type, the helical gearboxes industry is segmented into inline/parallel shaft helical gearboxes, bevel helical gearboxes, helical worm gearboxes, shaft mounted helical gearboxes, and coaxial helical inline gearboxes. In 2026, the inline/parallel shaft helical gearboxes segment is expected to account for the largest share of this market. The leading position of this segment is attributed to the universal applicability of inline and parallel shaft configurations across the broadest range of industrial drive applications including screw and belt conveyors, mixers and agitators, pumps, compressors, fans, and general material handling equipment, where alignment of the input and output shafts on parallel axes simplifies mechanical integration and provides the most direct and efficient power transmission path. Manufacturers including SEW-Eurodrive GmbH & Co KG (R-series and F-series), Bonfiglioli Riduttori S.p.A. (TR series), Getriebebau NORD GmbH & Co. KG (SK series), and Regal Rexnord Corporation (Dodge Quantis) maintain deep and well-established product portfolios in this category covering power ratings from fractional kilowatt to several thousand kilowatt, supporting both standard catalog procurement and engineered-to-order specifications across a wide range of industrial applications.

However, the bevel helical gearboxes segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the expanding procurement of right-angle drive gearboxes in mining and minerals processing, cement manufacturing, and bulk material handling applications where spatial constraints require input and output shafts to be oriented at 90 degrees and where the torque density of bevel helical designs exceeds that of equivalent helical worm configurations at higher power ratings. The growth of large-scale mineral processing projects requiring multi-megawatt kiln and mill drives, the expansion of aggregate and crushed stone production for infrastructure construction across Asia Pacific and the Middle East, and the increasing adoption of bevel helical gearboxes in water and wastewater treatment applications for mixer and aerator drives are all contributing to the strong growth trajectory of this segment. Manufacturers such as FLENDER GmbH (B-series), SEW-Eurodrive GmbH & Co KG (K-series), Bonfiglioli Riduttori S.p.A. (C series), and David Brown Santasalo are actively expanding their bevel helical portfolios with new ratio and power rating options to capture this growing demand.

By Mounting Configuration: In 2026, the Foot-Mounted Segment to Hold the Largest Share

Based on mounting configuration, the helical gearboxes industry is segmented into foot mounted, flange mounted, shaft mounted (hollow bore), and torque arm mounted. In 2026, the foot-mounted segment is expected to account for the largest share of this market. This dominance is driven by the status of foot mounting as the standard baseline installation configuration for helical gearboxes across the full range of general industrial applications, from light-duty conveyor drives to large mining equipment drives, offering the broadest compatibility with existing machinery foundations and structural supports and the most straightforward mechanical installation and alignment procedure. The extensive installed base of foot-mounted helical gearboxes across cement, mining, chemical processing, and metals manufacturing sectors generates significant replacement procurement activity that sustains this segment's volume dominance.

However, the flange-mounted segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the growing adoption of gearmotor assemblies in which helical gearboxes are directly mated to IEC-frame electric motors via standard bell housings, eliminating the need for separate shaft alignment and coupling installation while reducing the overall assembly footprint. The expansion of automated manufacturing, food and beverage processing lines, and packaging equipment in emerging markets is particularly supporting this growth, as these application segments strongly favor compact and easy-to-install gearmotor assemblies over separately sourced gearbox and motor procurement. The transition to modular machine design architectures in the packaging, material handling, and logistics automation sectors further amplifies demand for flange-mounted gearbox units that integrate cleanly into standardized machine module designs.

By Stage: In 2026, the Double-Stage Segment to Account for the Largest Share

Based on stage, the helical gearboxes industry is segmented into single stage, double stage, and triple stage and above. In 2026, the double-stage segment is expected to account for the largest share of this market. The dominance of this segment reflects the concentration of helical gearbox demand in applications requiring moderate speed reduction ratios in the range of approximately 10:1 to 50:1, which represent the most common drivetrain reduction requirements across conveyors, mixers, pumps, fans, and general process machinery in food processing, chemicals, water treatment, and light to medium manufacturing. Double-stage helical configurations achieve these reduction ratios within a compact and cost-effective package, providing the best balance of transmission efficiency, mechanical reliability, and product cost for the broadest range of standard industrial procurement requirements.

However, the triple-stage and above segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the increasing share of helical gearbox demand coming from heavy industrial and mining applications where reduction ratios exceeding 100:1 are required in a single gearbox unit to drive large grinding mills, rotary kilns, heavy-duty conveyors, and slurry pumps from standard-speed electric motors. The replacement of older multistage gearbox trains, consisting of separate primary and secondary reduction units connected by intermediate shafting, with modern high-stage-count gearboxes offering equivalent reduction in a single housing is a growing trend in cement plant and mining drive system upgrades that directly increases demand for three-stage and four-stage helical and bevel helical gearboxes.

By End-use Industry: In 2026, the Mining & Minerals Processing Segment to Hold the Largest Share

Based on end-use industry, the helical gearboxes industry is segmented into mining and minerals processing, cement and construction materials, food and beverage processing, metals and steel, chemical and petrochemical processing, water and wastewater treatment, power generation, packaging, and other end-use industries. In 2026, the mining and minerals processing segment is expected to account for the largest share of this market, reflecting the sector's position as both the highest-value and highest-volume consumer of helical gearboxes globally. Mining operations deploy helical gearboxes across a wide range of critical equipment including grinding mill drives, conveyor systems extending several kilometers in length, hoist and winder drives, thickener drives, and process plant agitators and mixers, with individual unit values in large grinding mill drive applications ranging from several hundred thousand to several million U.S. dollars. The sustained growth of critical mineral mining investment driven by the global energy transition and the expansion of copper, lithium, cobalt, and nickel production capacity is extending and strengthening the demand base for large and heavy-duty helical gearboxes in this segment. According to the U.S. Geological Survey Mineral Commodity Summaries 2025, global mine production of copper reached approximately 22 million metric tons in 2024, reflecting the ongoing expansion of new mine and concentrator projects that carry significant associated gearbox procurement requirements across grinding, conveying, and flotation processing circuits.

However, the food and beverage processing segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the combination of rapid expansion in food and beverage manufacturing capacity across Asia Pacific, Africa, and the Middle East, and the growing regulatory and commercial pressure on food processors globally to transition to hygienic, wash-down-rated, and allergen-safe gearbox designs that meet international food safety standards. The U.S. Food and Drug Administration's Food Safety Modernization Act and the European Union's Food Hygiene Regulation (EC) 852/2004, together with certification standards including EHEDG and 3-A Sanitary Standards, mandate design practices for food processing equipment including gearboxes that require smooth external surfaces without contamination-trapping crevices and food-grade lubrication. These requirements eliminate the use of conventional industrial gearboxes in direct food contact zones and create a distinct, premium-priced procurement category for hygienic helical gearboxes. Manufacturers including SEW-Eurodrive GmbH & Co KG (Stainless Steel Hygienic series), Getriebebau NORD GmbH & Co. KG (UNICASE Stainless Steel series), and Bonfiglioli Riduttori S.p.A. maintain dedicated food-grade product lines that command significant price premiums over standard industrial equivalents, enhancing the revenue growth contribution of this segment beyond what unit volume growth alone would suggest.

Based on geography, the overall helical gearboxes market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, Asia Pacific is expected to account for the largest share of this market. The dominance of the region is driven by the concentration of the world's largest heavy industrial sectors, including steel, cement, mining, and chemicals manufacturing, across China, India, Japan, South Korea, and Southeast Asia, which collectively represent the world's highest concentration of helical gearbox-intensive industries. China alone accounts for approximately 55% of global cement production and produces over 1 billion metric tons of crude steel annually according to the World Steel Association, sustaining massive and continuous procurement of industrial gearboxes across both new capacity installation and replacement cycles. India's rapidly expanding manufacturing sector, underpinned by the Government of India's Production Linked Incentive schemes across sectors including steel, food processing, chemicals, and pharmaceuticals, is generating an expanding and increasingly sophisticated demand base for industrial helical gearboxes across a growing range of power ratings and application types. South Korea and Japan contribute high-value demand from precision manufacturing, shipbuilding, and advanced materials sectors that require application-specific helical gearbox configurations with close engineering specifications and established OEM supply relationships.

The Middle East and Africa helical gearboxes market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by a combination of large-scale industrial investment programs in the Gulf Cooperation Council countries and the accelerating development of mining infrastructure across Sub-Saharan Africa. Saudi Arabia's Vision 2030 program and its associated National Industrial Development and Logistics Program are driving the construction of new industrial manufacturing capacity in sectors including chemicals, metals fabrication, building materials, and food processing, each of which requires industrial helical gearboxes as a standard drivetrain component. The UAE's industrial strategy and Oman's and Bahrain's economic diversification programs are creating further greenfield industrial procurement demand across the GCC region. In Sub-Saharan Africa, the development of copper mines in the Democratic Republic of Congo and Zambia, cobalt processing capacity in the DRC, and manganese and iron ore mining in West and Southern Africa is generating substantial demand for mining-grade helical gearboxes from international OEM suppliers that are actively establishing regional service and distribution capabilities to support this growing project pipeline.

Europe is a large and well-established market for helical gearboxes, supported by a strong industrial manufacturing base and a well-developed aftermarket services infrastructure. Germany remains the largest single-country market within Europe, driven by the strength of its machine tool, automotive manufacturing equipment, and chemical engineering industries, all of which are intensive consumers of precision helical gearboxes. The European market benefits from the presence of several globally leading helical gearbox manufacturers including FLENDER GmbH, SEW-Eurodrive GmbH & Co KG, Getriebebau NORD GmbH & Co. KG, Lenze SE, and Bonfiglioli Riduttori S.p.A. (Italy), which maintain strong positions in their home region and generate significant export revenues from global industrial projects. The EU's energy efficiency regulations and the ongoing modernization of aging industrial drivetrain infrastructure across established European manufacturing sectors are sustaining steady replacement procurement demand that partially offsets the impact of slower overall industrial volume growth compared to Asia Pacific.

The global helical gearboxes market is moderately consolidated at the level of complete system supply, with competition driven primarily by transmission efficiency, torque density, application-specific engineering capability, the breadth and modularity of standard product portfolios, and the strength and geographic reach of aftermarket service and spare parts supply networks. Key differentiators include the availability of application-specific product variants including hygienic, explosion-proof, and corrosion-resistant designs, the level of technical application engineering expertise maintained across end-use industries, the integration of condition monitoring and digital connectivity capabilities into product platforms, and the scale of regional distribution, service center, and spare parts stocking infrastructure that industrial operators increasingly require when selecting a long-term drivetrain equipment partner.

Large full-portfolio drivetrain suppliers such as SEW-Eurodrive GmbH & Co KG, FLENDER GmbH, and Bonfiglioli Riduttori S.p.A. compete through comprehensive product portfolios covering all major helical gearbox configurations across a broad power rating range, deep application engineering expertise maintained across multiple industrial sectors, and extensive global distribution and service center networks that support installed base maintenance and provide rapid response to unplanned downtime events. Getriebebau NORD GmbH & Co. KG and Lenze SE compete through highly modular and integrated gearmotor and drive system platforms that are particularly well suited for automated manufacturing and logistics applications, while Regal Rexnord Corporation leverages its extensive North American distribution network and the strong brand recognition of the Dodge product line across general industrial and mining applications. Sumitomo Drive Technologies competes through proprietary gear geometry technology and a strong position in precision and high-load gearbox applications, while WEG S.A. leverages its acquisition of the Rossi brand to compete across the European and Latin American industrial gearbox markets with an expanded product portfolio spanning helical, bevel helical, and helical worm configurations. Regional specialists including Elecon Engineering Company Limited maintain strong competitive positions across mining, cement, and metals sectors in South Asia and select export markets, while David Brown Santasalo competes effectively in large-scale mining and industrial gearbox applications across Africa, Australia, and Latin America.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global helical gearboxes market include FLENDER GmbH (Germany), SEW-Eurodrive GmbH & Co KG (Germany), Bonfiglioli Riduttori S.p.A. (Italy), Getriebebau NORD GmbH & Co. KG (Germany), Regal Rexnord Corporation (U.S.), Sumitomo Drive Technologies — Sumitomo Heavy Industries, Ltd. (Japan), Dana Incorporated (U.S.), Elecon Engineering Company Limited (India), Lenze SE (Germany), WEG S.A. (Brazil), Motovario S.p.A. (Italy), David Brown Santasalo (U.K.), and Varvel S.r.l. (Italy), among others.

The global helical gearboxes market is expected to reach USD 19.5 billion by 2036 from an estimated USD 12.2 billion in 2026, at a CAGR of 4.8% during the forecast period 2026–2036.

In 2026, the inline/parallel shaft helical gearboxes segment is expected to hold the largest share of this market, driven by its broad applicability across conveying, mixing, pumping, and general material handling applications across virtually all industrial sectors.

The bevel helical gearboxes segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing demand for right-angle drive configurations in mining, cement production, and bulk material handling applications where torque density and compact installation geometry are critical requirements.

In 2026, the foot-mounted segment is expected to hold the largest share of this market, reflecting the status of foot mounting as the standard baseline installation configuration for helical gearboxes across the full range of general industrial drive applications.

In 2026, the double-stage segment is expected to hold the largest share of this market, driven by its suitability for the moderate speed reduction ratios required across the broadest range of general industrial drive applications.

In 2026, the mining and minerals processing segment is expected to hold the largest share of this market, reflecting the sector's position as the highest-value consumer of heavy-duty helical gearboxes across grinding mill drives, conveyors, hoists, and mineral processing equipment.

The growth of this market is primarily driven by the sustained expansion of critical minerals mining investment driven by the global energy transition, continued infrastructure development and cement capacity expansion in developing economies, the tightening of energy efficiency regulations for electric motors and drivetrain systems across major industrial economies, growing adoption of hygienic helical gearboxes in food and beverage processing applications in emerging markets, and the integration of condition monitoring and digital connectivity into gearbox platforms that improves operational economics and enables service-based revenue models for leading manufacturers.

Key players in the global helical gearboxes market include FLENDER GmbH (Germany), SEW-Eurodrive GmbH & Co KG (Germany), Bonfiglioli Riduttori S.p.A. (Italy), Getriebebau NORD GmbH & Co. KG (Germany), Regal Rexnord Corporation (U.S.), Sumitomo Drive Technologies — Sumitomo Heavy Industries, Ltd. (Japan), Dana Incorporated (U.S.), Elecon Engineering Company Limited (India), Lenze SE (Germany), WEG S.A. (Brazil), Motovario S.p.A. (Italy), David Brown Santasalo (U.K.), and Varvel S.r.l. (Italy).

Middle East & Africa is expected to register the highest growth rate in the global helical gearboxes market during the forecast period 2026–2036, driven by large-scale industrial investment under Gulf Cooperation Council economic diversification programs, the accelerating development of critical minerals mining capacity across Sub-Saharan Africa, and the expansion of cement, food processing, and chemicals manufacturing capacity across the region.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Product Type

3.3 Market Analysis by Mounting Configuration

3.4 Market Analysis by Stage

3.5 Market Analysis by End-use Industry

3.6 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Sustained Growth of Critical Minerals Mining Investment Driving Demand for Heavy-Duty Helical Gearboxes

4.2.2 Expanding Cement and Infrastructure Construction Capacity in Developing Economies Generating Continuous Gearbox Procurement Demand

4.2.3 Tightening Energy Efficiency Regulations for Industrial Drivetrain Systems Compelling Gearbox Technology Upgrades

4.2.4 Rapid Expansion of Food and Beverage Processing Manufacturing in Emerging Markets Driving Adoption of Hygienic Gearbox Designs

4.3 Restraints

4.3.1 High Cost and Extended Lead Times for Custom-Engineered Mining and Cement Grade Helical Gearboxes Limiting Procurement Flexibility

4.3.2 Competitive Pressure from Refurbished and Remanufactured Gearbox Aftermarket in Price-Sensitive Emerging Economies

4.4 Opportunities

4.4.1 Critical Minerals Mining Expansion Across Sub-Saharan Africa and Latin America Opening New Heavy-Duty Gearbox Market Segments

4.4.2 Digital Condition Monitoring Integration Creating Service-Based Revenue Opportunities for Gearbox Manufacturers

4.4.3 Energy Efficiency Regulatory Cycles Driving Systematic Drivetrain Upgrade Investment Across European and Asian Industrial Operators

4.5 Challenges

4.5.1 Managing Application Diversity and Custom Engineering Complexity Across a Wide Range of Industrial End-use Specifications

4.5.2 Building and Maintaining Adequate Aftermarket Service Infrastructure Across Geographically Dispersed Mining and Industrial Operations

4.6 Porter's Five Forces Analysis

5. Helical Gearboxes Market, by Product Type

5.1 Overview

5.2 Inline/Parallel Shaft Helical Gearboxes

5.2.1 Standard Inline/Parallel Shaft Helical Gearboxes

5.2.2 Heavy-Duty Inline/Parallel Shaft Helical Gearboxes

5.3 Bevel Helical Gearboxes

5.3.1 Standard Bevel Helical Gearboxes

5.3.2 Heavy-Duty Bevel Helical Gearboxes

5.4 Helical Worm Gearboxes

5.4.1 Standard Helical Worm Gearboxes

5.4.2 Food-Grade Helical Worm Gearboxes

5.5 Shaft Mounted Helical Gearboxes

5.5.1 Standard Shaft Mounted Helical Gearboxes

5.5.2 High-Torque Shaft Mounted Helical Gearboxes

5.6 Coaxial Helical Inline Gearboxes

5.6.1 Standard Coaxial Helical Gearboxes

5.6.2 Compact Coaxial Helical Gearboxes

6. Helical Gearboxes Market, by Mounting Configuration

6.1 Overview

6.2 Foot Mounted

6.3 Flange Mounted

6.4 Shaft Mounted (Hollow Bore)

6.5 Torque Arm Mounted

7. Helical Gearboxes Market, by Stage

7.1 Overview

7.2 Single Stage

7.3 Double Stage

7.4 Triple Stage and Above

8. Helical Gearboxes Market, by End-use Industry

8.1 Overview

8.2 Mining & Minerals Processing

8.3 Cement & Construction Materials

8.4 Food & Beverage Processing

8.4.1 Food Processing

8.4.2 Beverage Processing

8.5 Metals & Steel

8.6 Chemical & Petrochemical Processing

8.7 Water & Wastewater Treatment

8.8 Power Generation

8.9 Packaging

8.10 Other End-use Industries

9. Helical Gearboxes Market, by Geography

9.1 Overview

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 Germany

9.3.2 U.K.

9.3.3 France

9.3.4 Italy

9.3.5 Spain

9.3.6 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 South Korea

9.4.5 Australia

9.4.6 Southeast Asia

9.4.7 Rest of Asia Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Chile

9.5.3 Rest of Latin America

9.6 Middle East & Africa

9.6.1 UAE

9.6.2 Saudi Arabia

9.6.3 South Africa

9.6.4 Rest of Middle East & Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Share/Ranking Analysis (2025)

11. Company Profiles

11.1 FLENDER GmbH

11.2 SEW-Eurodrive GmbH & Co KG

11.3 Bonfiglioli Riduttori S.p.A.

11.4 Getriebebau NORD GmbH & Co. KG

11.5 Regal Rexnord Corporation

11.6 Sumitomo Drive Technologies (Sumitomo Heavy Industries, Ltd.)

11.7 Dana Incorporated

11.8 Elecon Engineering Company Limited

11.9 Lenze SE

11.10 WEG S.A.

11.11 Motovario S.p.A.

11.12 David Brown Santasalo

11.13 Varvel S.r.l.

11.14 Others

12. Appendix

12.1 Questionnaire

12.2 Available Customization Options

12.3 Related Reports

Published Date: Jul-2024

Subscribe to get the latest industry updates