Resources

About Us

Dust Collection Systems Market Size, Share & Trends Analysis, by Product Type, Collection Method (Dry, Wet), Mobility (Stationary, Portable), End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

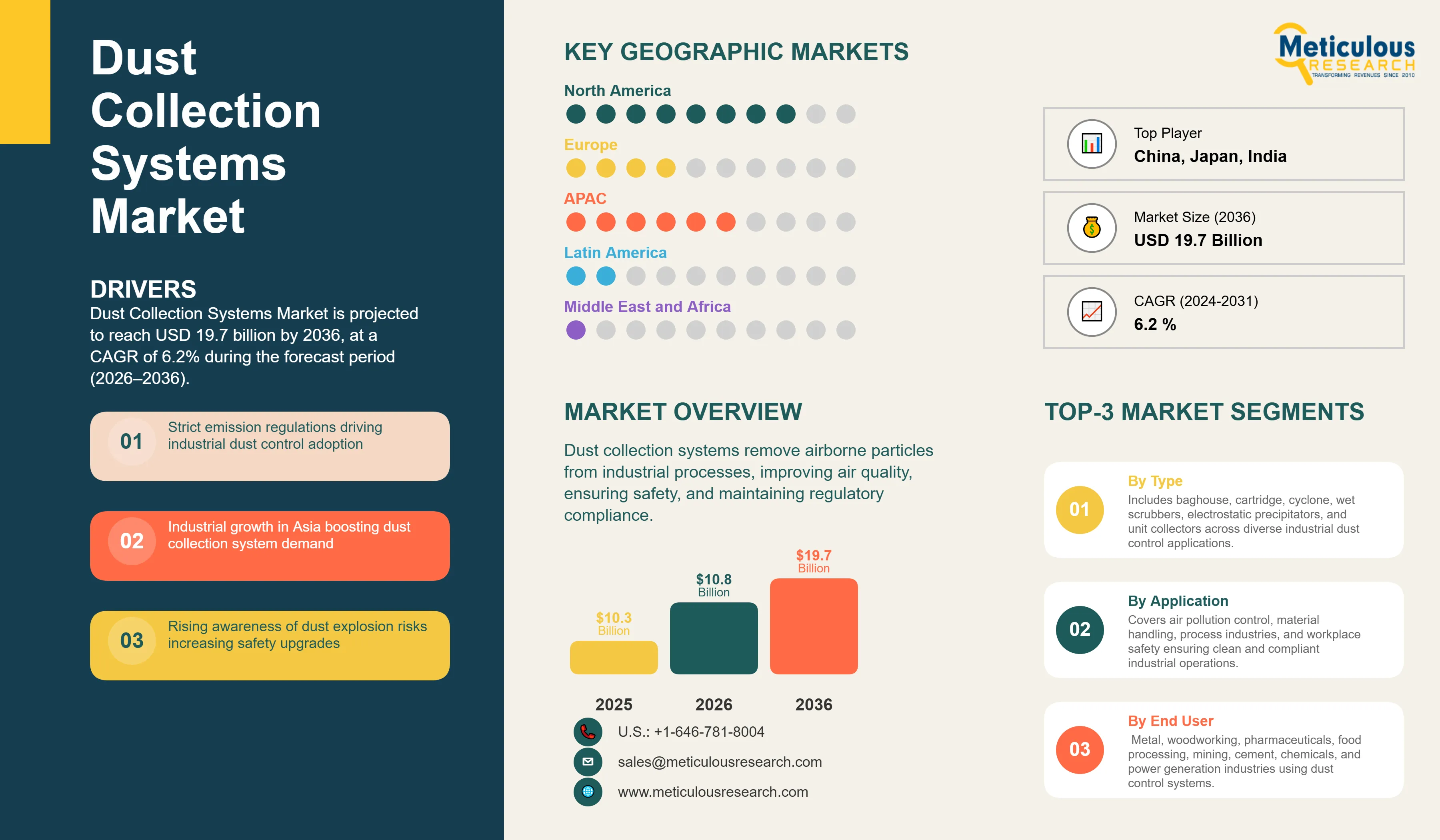

Report ID: MREP - 1041949 Pages: 278 Apr-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global Dust Collection Systems Market was valued at USD 10.3 billion in 2025. The market is projected to reach USD 19.7 billion by 2036, growing from USD 10.8 billion in 2026 at a CAGR of 6.2% during the forecast period (2026–2036).

Market Overview and Insights

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall dust collection systems industry covers the complete range of industrial equipment designed to capture and remove airborne particulate matter, dust, fumes, and other contaminants generated during industrial manufacturing and processing operations. The market includes baghouse dust collectors, cartridge dust collectors, cyclone dust collectors, wet scrubbers, electrostatic precipitators, and unit collectors deployed across a wide range of end-use industries including metalworking and metal fabrication, woodworking and furniture manufacturing, pharmaceutical and food processing, mining and mineral processing, cement and construction materials, chemical processing, and power generation.

These systems are integral to plant operations where airborne dust poses risks to worker health, equipment reliability, product quality, fire and explosion safety, and regulatory compliance. Dust collection systems operate across both dry and wet collection methods, and are available as stationary centralized installations serving entire production facilities as well as portable point-of-use units deployed at individual workstations or in field environments.

The growth of the dust collection systems market is primarily driven by the tightening of occupational health and environmental regulations across major industrial economies. In the United States, OSHA’s updated Combustible Dust National Emphasis Program, in effect since January 30, 2023, has led to increased unannounced inspections across industries such as wood manufacturing, food processing, chemical production, and metalworking. This has pushed operators to invest in compliant dust collection systems. The implementation of NFPA 660: Standard for Combustible Dusts and Particulate Solids, effective December 6, 2024, has further strengthened compliance-driven purchasing by requiring facilities handling combustible dust to conduct Dust Hazard Analyses and implement documented engineering controls, including dust collection solutions. Additionally, OSHA’s crystalline silica standard for general industry continues to support ongoing investment in high-efficiency dust collection systems, particularly in sectors like construction materials, foundries, and ceramics, where exposure to respirable crystalline silica poses significant occupational health risks.

In addition to regulatory compliance, growing awareness among industrial operators of the operational and financial costs associated with inadequate dust management, including equipment wear, product contamination, unplanned downtime, and insurance liabilities, is reinforcing demand for advanced dust collection technologies. The integration of industrial IoT capabilities into dust collection system platforms is further accelerating adoption by enabling predictive maintenance, real-time performance monitoring, and remote system diagnostics that reduce operational costs and extend system service life.

Despite strong growth fundamentals, the market faces challenges related to the high upfront capital expenditure associated with centralized dust collection system installation, particularly in retrofit applications were existing facility layouts complicate duct routing and system integration. Operational challenges including filter blinding in high-moisture or sticky dust environments, explosive dust handling requiring specialized system configurations and explosion protection equipment, and the complexity of managing dust disposal and secondary containment continue to influence procurement decisions and total cost of ownership calculations for industrial buyers.

The tightening of global combustible dust and air quality regulations is creating significant opportunities for system manufacturers offering integrated compliance solutions that combine dust collection equipment with Dust Hazard Analysis services, explosion protection engineering, and digital performance monitoring. The growing adoption of portable and modular dust collection systems is opening new addressable markets in small and mid-size manufacturing enterprises, maintenance and repair operations, and construction sectors that were previously underserved by conventional centralized system offerings. In addition, the rapid expansion of pharmaceutical and food processing manufacturing capacity in Asia Pacific and the Middle East, where product purity and cleanroom compliance requirements mandate high-efficiency dust capture, is creating a structurally new growth segment for cartridge and HEPA-rated dust collection technologies.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 19.7 Billion |

|

Market Size in 2026 |

USD 10.8 Billion |

|

Market Size in 2025 |

USD 10.3 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.2% |

|

Dominating Product Type |

Baghouse Dust Collectors |

|

Fastest Growing Product Type |

Cartridge Dust Collectors |

|

Dominating Collection Method |

Dry Dust Collection |

|

Fastest Growing Collection Method |

Wet Dust Collection |

|

Dominating Mobility |

Stationary Dust Collection Systems |

|

Fastest Growing Mobility |

Portable Dust Collection Systems |

|

Dominating End-use Industry |

Metalworking & Metal Fabrication |

|

Fastest Growing End-use Industry |

Pharmaceutical & Food Processing |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

NFPA 660 Adoption and Tightening Global Occupational Health Regulations Driving Mandatory Dust Collection System Investment

The enforcement of NFPA 660: Standard for Combustible Dusts and Particulate Solids on December 6, 2024, represents one of the most significant regulatory shifts in the global dust collection systems market in decades. This standard unifies six previously separate NFPA combustible dust standards—NFPA 652, 654, 655, 656, 61, and 484—into a single, comprehensive compliance framework. It requires all facilities handling potentially combustible dust to conduct a formal Dust Hazard Analysis, implement documented engineering controls such as compliant dust collection systems, and update these assessments every five years or after any process modification. According to OSHA estimates, around 30,000 facilities in the United States are at risk of combustible dust incidents, creating a large base of operations now subject to clearly defined compliance requirements that directly drive demand for dust collection systems.

Additionally, OSHA’s updated Combustible Dust National Emphasis Program, implemented in January 2023, has broadened its scope and intensified unannounced inspections across industries such as metalworking, wood manufacturing, food processing, pharmaceuticals, and chemical processing. In Europe, similar regulatory momentum is building following the revision of the EU Ambient Air Quality Directive, adopted in December 2024, which introduced tighter particulate matter limits in line with WHO guidelines and is pushing industrial operators to upgrade dust collection systems to meet stricter fugitive emission standards.

In the Asia Pacific region, ongoing enforcement of China’s Air Pollution Prevention and Control Law, along with India’s increasingly stringent air quality norms under the National Clean Air Programme, is driving compliance-led demand across the region’s extensive manufacturing sector. Taken together, these regulatory developments are shifting dust collection system investments from largely optional capital spending to essential, compliance-driven expenditure, significantly broadening the overall addressable market.

Industrial IoT Integration and Connected Monitoring Platforms Transforming Dust Collector Performance Management

The incorporation of industrial IoT sensors, connectivity, and advanced analytics into dust collection systems is becoming a key competitive differentiator for leading manufacturers, fundamentally reshaping both the economics and operational model of system ownership. Traditionally, dust collection systems functioned as standalone units, with filter replacements carried out at fixed maintenance intervals. This often led to inefficiencies either filters were replaced too early before reaching their full service life, or systems continued operating with clogged or underperforming filters, reducing efficiency and increasing energy consumption.

Connected dust collection systems, such as Donaldson Company, Inc.’s iCue Connected Filtration platform, leverage real-time differential pressure sensors, compressed air usage monitoring, and cloud-based analytics to give operators continuous insight into filter loading, airflow performance, and estimated filter replacement timing based on actual operating conditions rather than fixed maintenance schedules.

Similarly, Camfil’s Gold Series X-Flo dust collectors integrate intelligent monitoring features that help extend filter life by optimizing pulse-cleaning cycles based on real-time filter condition data. In parallel, Nederman offers digital monitoring solutions that enable remote performance tracking and alert-driven maintenance scheduling across multiple facilities, reducing the complexity and operational effort associated with managing distributed dust collection system networks.

The business case for connected dust collection platforms is becoming increasingly strong for large industrial operators, where unexpected dust collector downtime can disrupt production and where compliance risks linked to system underperformance may result in regulatory penalties and liability exposure. As a result, manufacturers that provide integrated connected filtration solutions combining equipment, software, and performance analytics are gaining a clear competitive edge over suppliers that offer traditional hardware-only systems. This trend is accelerating the shift from transactional equipment procurement toward longer-term service and performance-based engagement models that improve customer retention and create predictable aftermarket revenue streams for system manufacturers.

Cartridge Dust Collector Technology Displacing Conventional Baghouse Systems in New Industrial Installations

The sustained displacement of conventional woven fabric baghouse dust collection systems toward cartridge dust collectors in new industrial installations represents the most significant product-level technological change influencing the competitive landscape of the global dust collection systems market. Cartridge dust collectors utilize pleated filter media made from materials such as cellulose, polyester, or advanced nanofiber composites, offering a much higher filtration surface area within a far more compact footprint than conventional baghouse designs. This combination of space efficiency and high filtration performance makes cartridge systems particularly suitable for modern manufacturing facilities with limited installation space, as well as for an expanding range of dust types including fine metalworking particulates, pharmaceutical active ingredient powders, and food-grade materials that require filtration efficiencies of MERV 15 or higher to meet regulatory standards and product quality expectations.

Advanced nanofiber filtration media—such as Donaldson Company, Inc.’s UltraWeb technology and Parker Hannifin Corporation’s SynteQ filter media—enable cartridge dust collectors to deliver near-zero particulate penetration for submicron dust while maintaining relatively low pressure drop. This improves energy efficiency by reducing blower power requirements and provides higher capture performance compared to conventional baghouse filters.

The increasing use of nanofiber and expanded PTFE membrane-coated cartridges has also expanded the operational capabilities of cartridge systems into more challenging environments, including high-moisture conditions and processes involving sticky or adhesive dusts that were previously considered unsuitable for this technology.

In response to this shift, manufacturers such as Camfil (Camfil APC), Donaldson Company, Inc. (Donaldson Torit), Parker Hannifin Corporation, and Imperial Systems are expanding their cartridge dust collector portfolios with application-specific designs for metalworking, pharmaceuticals, food processing, and woodworking industries, underscoring the strong commercial momentum behind this technological transition.

By Product Type: In 2026, the Baghouse Dust Collectors Segment to Dominate the Global Dust Collection Systems Market

Based on product type, the dust collection systems industry is segmented into baghouse dust collectors, cartridge dust collectors, cyclone dust collectors, wet scrubbers, electrostatic precipitators, and unit collectors. In 2026, the baghouse dust collectors segment is expected to account for the largest share of this market. The leading position of this segment is attributed to the proven suitability of baghouse technology for managing the highest dust volume loads across the most demanding industrial applications, including cement manufacturing, coal-fired and biomass power generation, chemical processing, and large-scale metal smelting and casting operations. Pulse jet baghouse configurations, which account for the largest share within this segment, are capable of handling airflows from a few thousand cubic meters per hour to several million cubic meters per hour, making them the technology of choice for large-scale industrial installations where no alternative product type can cost-effectively match their throughput and operational reliability. Donaldson's Torit Baghouse product line and Camfil's modular fabric filter systems exemplify the continued product development investment sustaining this segment's competitive relevance.

However, the cartridge dust collectors segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating displacement of baghouse systems in new small and mid-size industrial installation projects, the growing adoption of high-efficiency nanofiber and membrane filter media that have expanded cartridge system performance envelopes into previously challenging applications, and the favourable total cost of ownership profile of cartridge systems in space-constrained manufacturing environments where compact footprint and easy filter serviceability translate into meaningful operational cost advantages.

By Collection Method: In 2026, the Dry Dust Collection Segment to Hold the Largest Share

Based on collection method, the dust collection systems industry is segmented into dry dust collection and wet dust collection. In 2026, the dry dust collection segment is expected to account for the largest share of this market. The growth of this segment driven by the broad applicability of dry collection technologies, encompassing baghouse, cartridge, cyclone, and electrostatic precipitator systems, across the full range of industrial dust types generated in metalworking, woodworking, pharmaceutical, food processing, mining, and general manufacturing environments. Dry collection systems benefit from comparatively lower operating costs, simpler dust disposal logistics, and compatibility with a broader range of secondary dust handling and disposal infrastructure, making them the default technology selection for the overwhelming majority of industrial dust management applications globally.

However, the wet dust collection segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the growing recognition of wet scrubbing technology's unique capabilities for managing dust types that present specific hazards or handling challenges in dry collection systems, including hygroscopic and water-soluble dusts that blind dry filter media, highly combustible dusts where water-based suppression provides an inherent explosion risk mitigation benefit, and dust generated in high-temperature processes where the cooling effect of wet collection systems provides additional engineering value. The increasing stringency of environmental discharge standards governing industrial air emissions is also elevating wet scrubber adoption in applications where simultaneous gas-phase contaminant removal alongside particulate capture is required.

By Mobility: In 2026, the Stationary Dust Collection Systems Segment to Account for the Largest Share

Based on mobility, the dust collection systems industry is segmented into stationary dust collection systems and portable dust collection systems. In 2026, the stationary dust collection systems segment is expected to account for the largest share of this market. This growth is mainly driven by the prevalent deployment of centralized, fixed-installation dust collection infrastructure across large industrial manufacturing facilities, where a single centralized system serves multiple production workstations through a network of ducting and hoods. Stationary systems are engineered to handle the sustained, high-volume dust loads characteristic of continuous manufacturing operations in sectors such as foundries, cement plants, woodworking facilities, and metal fabrication shops, and represent the primary capital investment category in dust collection system procurement at the facility level for large industrial operators.

However, the portable dust collection systems segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the growing adoption of flexible, point-of-use dust capture solutions among small and mid-size manufacturing enterprises that cannot justify the capital expenditure of centralized fixed installations, expanding deployment in construction and infrastructure maintenance operations where dust capture must follow the point of work generation rather than being routed to a fixed collection point, and the increasing regulatory obligation for portable dust control in sectors such as building renovation, where regulations governing lead and silica dust exposure require compliant source capture during tasks including concrete cutting, drilling, and drywall sanding.

By End-use Industry: In 2026, the Metalworking & Metal Fabrication Segment to Hold the Largest Share

Based on end-use industry, the dust collection systems industry is segmented into metalworking and metal fabrication, woodworking and furniture manufacturing, pharmaceutical and food processing, mining and mineral processing, cement and construction materials, chemical processing, power generation, and other end-use industries. In 2026, the metalworking and metal fabrication segment is expected to account for the largest share of this market, indicating the status of this sector as the broadest and most dust-intensive category of industrial manufacturing globally, encompassing grinding, cutting, welding, thermal spray, shot blasting, and powder coating operations that each generate distinct airborne particulate and fume types requiring dedicated collection systems. The expanding global installed base of robotic welding, laser cutting, and CNC machining equipment in automotive, aerospace, and heavy equipment manufacturing sectors is continuously adding dust generation point sources that require engineered collection solutions. OSHA's hexavalent chromium standard and general metal dust exposure guidelines sustain regulatory compliance procurement within this segment across North American and European markets.

However, the pharmaceutical and food processing segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the stringent dust containment and air quality requirements embedded in pharmaceutical manufacturing regulations including the U.S. FDA's Current Good Manufacturing Practice standards, the European Medicines Agency's GMP guidelines, and ISO cleanroom standards, which mandate high-efficiency dust collection systems capable of achieving HEPA or near-HEPA filtration performance for active ingredient powder handling, tablet compression, and granulation processes. The parallel expansion of food manufacturing capacity globally, driven by population growth, urbanization, and the rapid development of processed food production infrastructure in emerging markets, is creating sustained demand for food-grade dust collection systems compliant with FSMA, EHEDG, and 3-A Sanitary Standards that address hygiene, allergen containment, and combustible grain and sugar dust management requirements.

Based on geography, the overall dust collection systems market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This growth is driven by the most stringent and actively enforced industrial dust management regulatory environment globally, encompassing OSHA's Combustible Dust National Emphasis Program, the newly adopted NFPA 660 Standard for Combustible Dusts and Particulate Solids, the crystalline silica standard for general industry, and EPA National Emission Standards for Hazardous Air Pollutants that collectively compel sustained compliance-driven capital investment across the region's broad manufacturing base. The presence of leading system manufacturers including Donaldson Company, Parker Hannifin Corporation, CECO Environmental Corp., and Imperial Systems, Inc. ensures a deep local supply base and extensive aftermarket support infrastructure that reinforces procurement confidence among North American industrial buyers. The United States in particular benefits from a large installed base of aging dust collection systems across foundry, woodworking, and food processing sectors that are due for technology refresh driven by both compliance requirements and the operational cost benefits of modern high-efficiency filtration platforms.

However, the Asia Pacific dust collection systems market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of manufacturing capacity across China, India, South Korea, Japan, and Southeast Asia in sectors including steel and aluminum fabrication, cement and construction materials, electronics and semiconductor components, and automotive parts manufacturing, all of which generate significant dust management requirements. China's ongoing enforcement of its Air Pollution Prevention and Control Law and the continued implementation of emission reduction mandates targeting industrial particulate pollution are compelling large-scale adoption of advanced dust collection infrastructure across Chinese manufacturing industries that historically relied on less efficient control technologies. India's National Clean Air Programme, which targets a 40% reduction in particulate matter concentrations by 2026 across 131 cities, is creating increasing regulatory pressure on industrial operators in sectors including cement, power generation, and foundry manufacturing to invest in compliant dust collection systems. The rapid growth of pharmaceutical and food processing manufacturing across Southeast Asia, driven by foreign direct investment inflows and regional supply chain diversification, is additionally creating a new and expanding demand base for high-efficiency cartridge and HEPA-rated dust collection systems in these markets.

Europe is a large and well-established market for dust collection systems, supported by a strong regulatory framework that includes the Industrial Emissions Directive, the revised Ambient Air Quality Directive adopted in December 2024, and national occupational health regulations such as the UK’s Control of Substances Hazardous to Health (COSHH). Together, these regulations drive steady, compliance-led investment across the region’s industrial sectors. European manufacturers including Camfil AB, Nederman Holding AB, Höcker Polytechnik GmbH, ESTA Apparatebau GmbH & Co. KG, Herding GmbH Filtertechnik, and Dustcontrol AB maintain strong market positions in their home region supported by close customer relationships and deep application engineering expertise across European industrial sectors.

The global dust collection systems market is moderately consolidated at the system level, with competition primarily driven by filtration efficiency, system flexibility, compliance with industry-specific regulatory standards, and the strength of aftermarket filter and service offerings. Key differentiators include the availability of explosion-proof configurations certified under ATEX, NEC, and NFPA standards, the integration of digital monitoring and connectivity features, the level of application engineering expertise across end-use industries, and the scale and reach of global distribution and service networks.

Large diversified industrial filtration manufacturers such as Donaldson Company, Inc. and Parker Hannifin Corporation compete through comprehensive product portfolios covering multiple dust collection system technologies, extensive global distribution networks, and strong aftermarket filter supply positions that generate recurring revenue alongside capital equipment sales. Specialty dust collection system manufacturers including Camfil AB and Nederman Holding AB compete through superior filtration technology and deep application expertise, with Nederman having further strengthened its capabilities through the acquisition of RoboVent, a manufacturer of air purification systems for welding, cutting, and manufacturing applications. Regionally focused manufacturers including Höcker Polytechnik GmbH, ESTA Apparatebau GmbH & Co. KG, and Dustcontrol AB maintain strong competitive positions in European markets through customized engineering and local service capabilities, while Thermax Limited and FLSmidth A/S compete effectively in large-scale industrial and mining applications across Asia Pacific and other emerging market regions.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.Some of the key players operating in the global dust collection systems market include Donaldson Company, Inc. (U.S.), Camfil AB (Sweden), Parker Hannifin Corporation (U.S.), Nederman Holding AB (Sweden), CECO Environmental Corp. (U.S.), FLSmidth A/S (Denmark), Thermax Limited (India), Imperial Systems, Inc. (U.S.), Höcker Polytechnik GmbH (Germany), ESTA Apparatebau GmbH & Co. KG (Germany), Herding GmbH Filtertechnik (Germany), Schenck Process Group (Germany), Dustcontrol AB (Sweden), Ducon Technologies Inc. (U.S.), and Airflow Systems, Inc. (U.S.), among others.

The global dust collection systems market is expected to reach USD 19.7 billion by 2036 from an estimated USD 10.8 billion in 2026, at a CAGR of 6.2% during the forecast period 2026–2036.

In 2026, the baghouse dust collectors segment is expected to hold the largest share of this market, driven by its proven suitability for high-volume, high-dust-load industrial applications in cement, power generation, and chemical processing sectors.

The cartridge dust collectors segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating adoption of compact, high-efficiency cartridge systems in space-constrained manufacturing facilities and the growing performance advantages of nanofiber and membrane filtration media.

In 2026, the dry dust collection segment is expected to hold the largest share of this market, reflecting the broad applicability of dry collection technologies across the full range of industrial dust management applications.

In 2026, the stationary dust collection systems segment is expected to hold the largest share of this market, driven by the widespread deployment of centralized, fixed-installation dust collection infrastructure across large industrial manufacturing facilities.

In 2026, the metalworking and metal fabrication segment is expected to hold the largest share of this market, reflecting the broad and continuous dust generation profile of this sector across grinding, welding, cutting, and surface treatment operations.

The growth of this market is primarily driven by the tightening of occupational health and environmental regulations globally, including the adoption of NFPA 660, OSHA enforcement programs, and the EU Ambient Air Quality Directive revision, sustained industrial expansion in Asia Pacific, the integration of IoT-enabled monitoring into dust collection system platforms, and the growing adoption of high-efficiency cartridge and wet scrubbing technologies across pharmaceutical, food processing, and chemical manufacturing sectors.

Key players in the global dust collection systems market include Donaldson Company, Inc. (U.S.), Camfil AB (Sweden), Parker Hannifin Corporation (U.S.), Nederman Holding AB (Sweden), CECO Environmental Corp. (U.S.), FLSmidth A/S (Denmark), Thermax Limited (India), Imperial Systems, Inc. (U.S.), Höcker Polytechnik GmbH (Germany), ESTA Apparatebau GmbH & Co. KG (Germany), Herding GmbH Filtertechnik (Germany), Schenck Process Group (Germany), Dustcontrol AB (Sweden), Ducon Technologies Inc. (U.S.), and Airflow Systems, Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global dust collection systems market during the forecast period 2026–2036, driven by accelerating industrial expansion, tightening ambient air quality and occupational health regulations, and growing pharmaceutical and food processing manufacturing capacity across the region.

Published Date: May-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Jun-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates