Resources

About Us

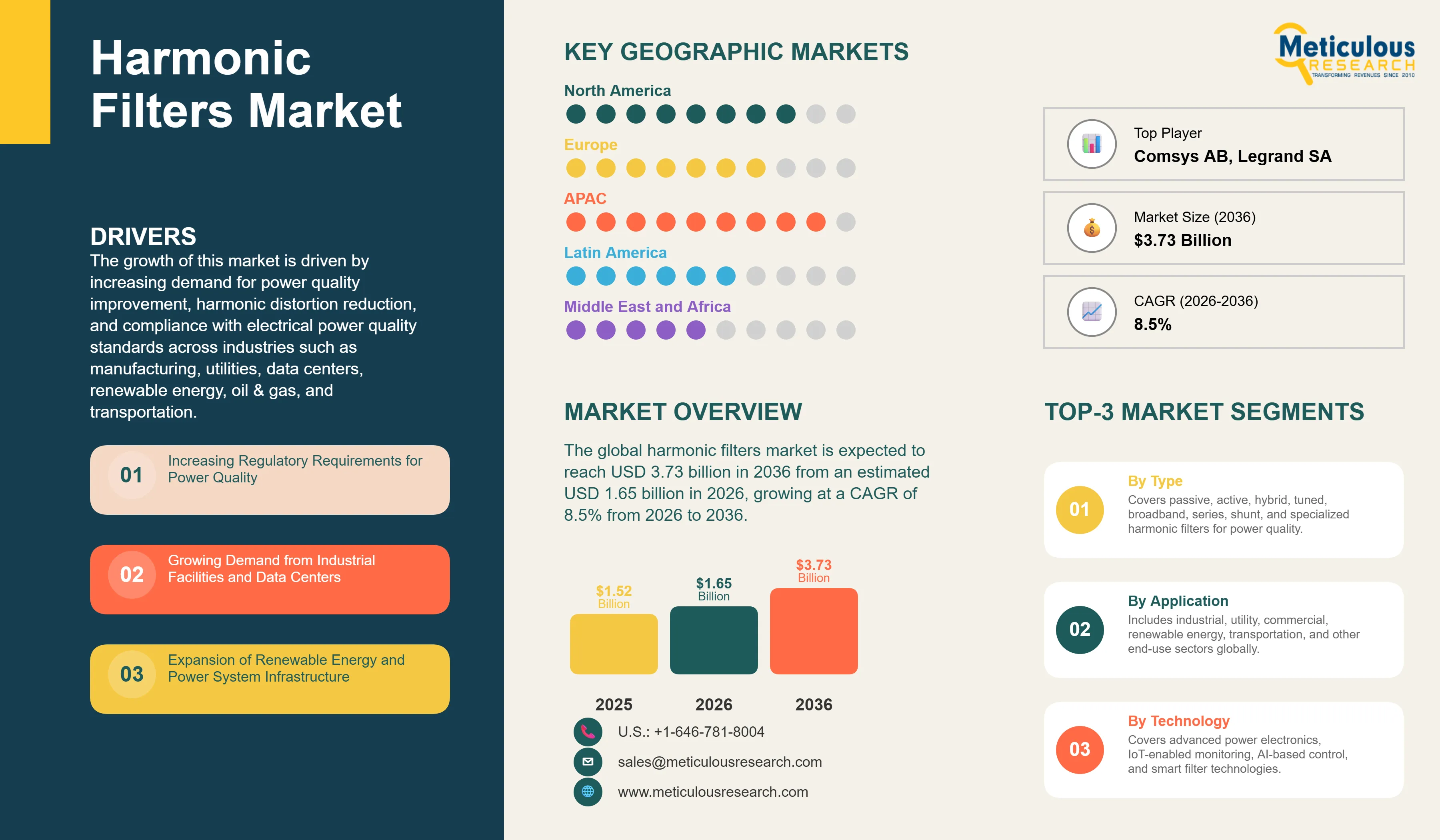

The global harmonic filters market size was valued at USD 1.52 billion in 2025. This market is expected to reach USD 3.73 billion in 2036 from an estimated USD 1.65 billion in 2026, growing at a CAGR of 8.5% from 2026 to 2036.

The growth of this market is driven by increasing demand for power quality improvement, harmonic distortion reduction, and compliance with electrical power quality standards across industries such as manufacturing, utilities, data centers, renewable energy, oil & gas, and transportation. The rapid expansion of industrial automation, variable frequency drives (VFDs), electric vehicle charging infrastructure, and renewable energy systems is increasing harmonic distortion in electrical networks, accelerating demand for advanced harmonic filtering solutions. According to the International Energy Agency (IEA), global electricity demand is expected to grow by around 4% annually through 2027, driven by electrification, industrial expansion, and digital infrastructure growth, increasing pressure on grid stability and power quality systems.

Growing investments in smart grids, industrial electrification, renewable energy integration, and energy-efficient infrastructure are further accelerating adoption of advanced harmonic filters capable of improving power factor, protecting sensitive equipment, and reducing energy losses. Increasing focus on operational reliability, energy efficiency, and compliance with IEEE and IEC power quality standards is creating opportunities for manufacturers offering intelligent and digitally integrated harmonic filter solutions for modern industrial and utility environments.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The harmonic filters market encompasses the design, manufacturing, installation, and maintenance of harmonic filter systems designed to reduce harmonic distortion and improve power quality in electrical systems. These systems are engineered to provide harmonic mitigation, power factor correction, and compliance with power quality standards in diverse electrical system environments. Harmonic filters are a fundamental component in industrial facilities, utility systems, renewable energy installations, and commercial buildings where power quality and equipment protection are essential.

The market includes various harmonic filter types designed for specific applications and performance requirements. Passive harmonic filters provide cost-effective harmonic mitigation. Active harmonic filters provide advanced distortion reduction. Hybrid harmonic filters provide combined passive and active compensation. Tuned harmonic filters provide targeted frequency mitigation. Broadband harmonic filters provide wide-spectrum distortion reduction. Series harmonic filters provide specialized mitigation. Shunt harmonic filters provide standard distortion reduction. Specialized harmonic filters serve unique applications.

The market is primarily driven by increasing power quality regulations adoption, growing demand for harmonic distortion reduction, technological advancements that enhance performance and efficiency, and the shift toward renewable energy integration. These systems find applications in industrial facilities, utility systems, renewable energy installations, and commercial buildings where power quality and equipment protection are essential.

Shift Towards Smart and Connected Power Quality Solutions

A significant trend in the harmonic filters market is the growing adoption of smart and connected power quality solutions with advanced monitoring capabilities. Smart filters enable collection and transmission of performance data to cloud systems. IoT connectivity enables remote monitoring and analysis of filter performance. The development of standardized IoT platforms has improved interoperability and reduced integration complexity.

The trend toward smart electrical systems and advanced power quality management is driving adoption of smart harmonic filters. The development of IoT technologies has enabled more sophisticated remote monitoring and analytics capabilities. The growing focus on data-driven decision making is driving adoption of systems with cloud connectivity. The trend toward predictive maintenance is driving adoption of filters with advanced monitoring capabilities. These smart and connected trends are creating significant growth opportunities in the harmonic filters market.

Growing Demand for Renewable Energy Integration and Power Quality

Another important trend driving growth in the harmonic filters market is the increasing demand for renewable energy integration and power quality. Renewable energy integration requires advanced harmonic mitigation. Advanced designs enable power quality with renewable sources. Integrated monitoring enables continuous optimization. Improved power quality reduces equipment damage.

The transition toward clean energy and electrification is accelerating demand for advanced harmonic mitigation solutions. According to the International Energy Agency (IEA), renewable energy is expected to account for nearly 95% of global power capacity additions through 2027, led by strong growth in solar and wind installations. At the same time, increasing investments in smart grids, industrial electrification, and distributed energy systems are intensifying the need for reliable power quality management technologies. Growing focus on energy efficiency, carbon reduction, and compliance with power quality standards is driving adoption of advanced harmonic filters capable of supporting renewable energy integration while improving operational reliability and reducing system losses.

|

Report Metric |

Details |

|---|---|

|

Market Size by 2036 |

USD 3.73 Billion |

|

Market Size in 2025 |

USD 1.65 Billion |

|

Market Size in 2026 |

USD 1.52 Billion |

|

Market Growth Rate (CAGR) 2026 to 2036 |

8.5% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Technology, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Increasing Regulatory Requirements for Power Quality

A key factor driving the growth of the harmonic filters market is the increasing regulatory requirements for power quality globally. Electrical systems require harmonic mitigation for regulatory compliance. Industrial facilities require power quality improvement. The expansion of electrical systems in emerging markets is creating substantial demand for filter equipment. The trend toward power quality standards is driving investment in advanced filter systems.

The need to improve power quality, energy efficiency, and regulatory compliance is accelerating adoption of advanced harmonic filters across industrial, commercial, and utility applications. According to the International Energy Agency (IEA), global electricity demand is projected to grow by around 4% annually through 2027, driven by industrial expansion, electrification, and digital infrastructure growth. In addition, the International Renewable Energy Agency (IRENA) reported that global renewable power capacity expanded by over 580 GW in 2024, marking the largest annual increase on record. The rapid deployment of renewable energy systems, EV charging infrastructure, data centers, and variable frequency drives (VFDs) is increasing harmonic distortion challenges in modern electrical networks, strengthening demand for reliable harmonic filtering technologies. Growing investments in smart grids, industrial automation, and electrification infrastructure are expected to further support demand for advanced harmonic filters and power quality management systems.

Growing Demand from Industrial Facilities and Data Centers

The growing demand from industrial facilities and data centers is a major driver of the harmonic filters market. Industrial facilities require harmonic mitigation for equipment protection. Data centers require power quality improvement for system reliability. The expansion of industrial and data center operations globally is creating substantial demand for filter equipment. The trend toward industrial modernization is driving adoption of advanced filter systems.

The increasing focus on energy efficiency, equipment protection, and operational reliability is accelerating investment in advanced harmonic filter systems. According to the International Energy Agency (IEA), global data center electricity consumption reached approximately 500 TWh in 2025, driven by growth in AI workloads, cloud computing, and hyperscale infrastructure. In parallel, the continued expansion of smart manufacturing and industrial electrification is increasing demand for advanced power quality solutions capable of reducing energy losses, minimizing equipment failures, and improving system reliability. Growing investments in sustainable industrial operations, data center expansion, and digital infrastructure modernization are expected to further strengthen demand for harmonic filters globally.

Expansion of Renewable Energy and Power System Infrastructure

The expansion of renewable energy and power system infrastructure globally is driving significant growth in the harmonic filters market. Renewable energy facilities are expanding operations and building new infrastructure requiring filter equipment. Power system operations are expanding globally creating demand for harmonic filters. The expansion of power systems in emerging markets is creating substantial demand for filter equipment. The trend toward grid modernization is driving investment in advanced filter systems.

The transition toward grid modernization and clean energy integration is further accelerating adoption of harmonic filters. According to the International Renewable Energy Agency (IRENA), global renewable power capacity increased by more than 580 GW in 2024, representing the largest annual capacity addition on record. In parallel, the International Energy Agency (IEA) estimates that global investment in grids and electricity networks exceeded USD 400 billion in 2025, supported by renewable integration, electrification, and smart infrastructure projects. The expansion of power systems in emerging economies, combined with growing investments in advanced energy management and grid reliability technologies, is expected to create sustained demand for sophisticated harmonic filter solutions worldwide.

High Initial Cost and Complex Installation Requirements

Despite its growth potential, the harmonic filters market faces significant challenges due to high initial cost and complex installation requirements. Advanced harmonic filters require substantial upfront investment, with complete systems costing thousands to hundreds of thousands of dollars. For small and medium-sized enterprises, these capital requirements represent a major barrier to adoption. The need for specialized installation and customization adds to total project costs. The complexity of filter system design and installation requires specialized expertise, adding to implementation costs.

Training and change management costs are substantial, as electrical personnel need to learn about new filter systems and their operation. The need for ongoing maintenance, technical support, and system upgrades adds to total cost of ownership. The risk of technology obsolescence and the need for periodic system upgrades can be costly. For price-sensitive manufacturers, particularly in developing economies, these financial barriers can slow adoption rates. The high installation complexity can restrict market growth among smaller facilities or those with limited technical expertise.

Lack of Standardization and Compatibility Challenges

The lack of standardization in filter designs and interfaces presents a significant restraint to market growth. Different manufacturers use different filter architectures and connection types, creating compatibility challenges. The need for custom installation work increases implementation costs and complexity. The lack of standardized interfaces limits the ability to quickly swap components or upgrade systems.

The complexity of ensuring compatibility between filter systems and different electrical equipment types can be challenging and costly. The need to maintain compatibility with legacy systems while adopting new technologies creates operational complexity. The uncertainty about which standards will become dominant can make investment decisions difficult. The fragmentation of the market with multiple competing standards can slow adoption and create barriers for smaller manufacturers. These standardization challenges can slow market adoption and create barriers for facilities seeking to implement advanced filter systems.

Expansion in Emerging Markets and Industrial Growth

The ongoing growth and industrialization in emerging economies presents a significant opportunity for the harmonic filters market. Countries in Asia-Pacific including China, India, Vietnam, Indonesia, and Thailand are experiencing rapid industrial expansion driven by economic growth, rising energy demand, and foreign direct investment. Industrial operations are expanding in these regions to serve growing domestic markets and export markets. The trend toward industrial automation in emerging markets is creating substantial demand for filter systems.

Government initiatives promoting industrial development and power quality are attracting investment and facility development. Infrastructure improvements including reliable power supply, transmission networks, and industrial parks are making these regions increasingly attractive for industrial operations. Latin America and parts of Africa are also experiencing industrial growth driven by economic development and foreign investment. The expansion of multinational corporations into emerging markets is bringing advanced manufacturing and industrial practices that drive demand for sophisticated filter technology. As these regions develop their industrial infrastructure, the installed base of harmonic filters will expand significantly.

Development of Specialized Applications and Advanced Technologies

The development of new and specialized applications for harmonic filters in emerging industries and advanced technologies is creating growth opportunities. Electric vehicle charging infrastructure requires specialized filters for power quality. Renewable energy systems require specialized filters for harmonic mitigation. Data center expansion requires specialized filters for system reliability. Advanced manufacturing requires specialized filters for equipment protection.

Energy storage systems require specialized filters for power quality. Smart grid applications require intelligent filter systems. Microgrid applications require specialized filter systems. Industrial IoT applications require advanced filters. These specialized applications, while currently representing smaller market segments, are growing rapidly and offer opportunities for filter manufacturers to develop innovative solutions and capture niche markets with higher margins.

Rapid Technological Change and Product Obsolescence

The rapid pace of technological change in filter technology and power quality management presents a significant challenge to the market. New technologies including advanced power electronics, AI integration, and IoT connectivity are emerging rapidly, potentially making existing filter designs obsolete. Manufacturers must continuously invest in research and development to stay competitive and meet evolving customer needs. The risk of technology obsolescence can discourage investment in harmonic filters, particularly among smaller manufacturers.

The challenge of maintaining compatibility between filter systems and evolving electrical equipment types can be complex and costly. The rapid pace of change means that training and skill development programs struggle to keep pace with new technologies. The need to support legacy systems while adopting new technologies creates operational complexity. The uncertainty about which technologies will become dominant can make investment decisions difficult. These technological challenges can slow market adoption and create barriers for smaller manufacturers or those lacking technical expertise.

Why are Passive Harmonic Filters Gaining Widespread Acceptance?

The passive harmonic filters segment commands the largest share of approximately 41% of the overall harmonic filters market in 2026. Passive harmonic filters lead the market because they offer excellent harmonic mitigation performance, have proven and reliable designs, provide cost-effective solutions for many applications, and have well-established service networks. These systems provide cost-effective harmonic mitigation. This proven technology makes passive harmonic filters ideal for industrial facilities, utility systems, and general applications where reliable harmonic mitigation is critical.

However, active harmonic filters are expected to witness the fastest CAGR during the forecast period. Active harmonic filters are gaining rapid adoption due to their ability to provide advanced harmonic mitigation, their superior performance in dynamic applications, and their advanced design capabilities compared to traditional filters. These systems provide advanced harmonic mitigation and dynamic support. Active harmonic filters are particularly valuable for applications requiring fast response or demanding conditions.

The renewable energy and industrial automation industries rely heavily on active harmonic filters for advanced harmonic mitigation. The trend toward renewable energy integration is driving adoption of active filter technology. Advances in active filter design have improved reliability and reduced costs, making them increasingly attractive for broader applications. The ability to provide dynamic harmonic mitigation makes active harmonic filters increasingly valuable in diverse applications. The growing demand for renewable energy integration is driving adoption of active filter technology.

How does Industrial Segment Dominate the Harmonic Filters Market?

The industrial segment holds the largest share of the harmonic filters market in 2026. This dominance reflects the critical importance of harmonic mitigation in industrial operations. Industrial facilities use harmonic filters extensively for equipment protection and power quality improvement. The industrial sector requires sophisticated filters for safe and efficient operations. The expansion of industrial operations globally is creating significant demand for filter equipment. The trend toward production optimization and efficiency is driving demand for advanced harmonic filters. The development of new industrial facilities and the modernization of existing operations drive demand for advanced filter systems. The trend toward advanced manufacturing is driving demand for high-performance filters. The expansion of industrial operations in emerging markets is creating significant demand for harmonic filters. The trend toward operational excellence drives investment in advanced harmonic mitigation technology.

However, the renewable energy segment is expected to witness the fastest CAGR during the forecast period. The renewable energy segment's growth is driven by expanding renewable energy capacity, development of new facilities, and increasing demand for sophisticated harmonic mitigation. Renewable energy facilities require harmonic filters for power quality. Wind and solar operations require specialized filters for harmonic mitigation.

The trend toward renewable energy production expansion is creating demand for specialized filters for power quality. The development of new renewable energy facilities creates demand for advanced harmonic filters. The expansion of renewable energy production globally is creating significant demand for filter systems. The growing demand for reliable and clean renewable energy integration drives demand for advanced filter systems. The trend toward environmental compliance and renewable energy adoption requires advanced harmonic mitigation systems.

How is Asia-Pacific Maintaining Dominance in the Harmonic Filters Market?

Asia-Pacific is expected to hold the largest share of the global harmonic filters market in 2026. This dominance comes from rapid industrialization, significant power system expansion, and growing renewable energy development across the region. China is a major industrial hub, creating enormous demand for harmonic filters. The expansion of industrial and renewable energy operations in China to serve the growing domestic market drives significant equipment demand. India's industrial sector is expanding rapidly, creating demand for filter equipment.

Vietnam, Indonesia, Thailand, and other Southeast Asian countries are experiencing rapid industrial growth driven by foreign direct investment and rising energy demand. The growing industrial and renewable energy operations across Asia-Pacific are creating substantial demand for filter equipment. Government initiatives promoting industrial development and power quality are attracting investment and facility development. Infrastructure improvements including reliable power supply, transmission networks, and industrial parks are making these regions increasingly attractive for industrial operations.

The region benefits from lower labor costs and growing industrial capacity, which makes it attractive for manufacturing and industrial operations. The presence of major multinational corporations establishing or expanding operations in the region is driving demand for modern filter equipment that meets global standards. The expansion of industrial operations in Asia-Pacific is creating demand for advanced harmonic filters. The trend toward automation in industrial operations is creating demand for intelligent filter systems with advanced capabilities.

Which Factors Support the North America Harmonic Filters Market Growth?

North America is expected to hold a significant share of the global harmonic filters market in 2026. This comes from substantial industrial operations, well-developed power quality infrastructure, and significant investment in industrial modernization. The United States has major industrial and power quality operations requiring advanced filter systems. Canada's industrial and power quality sectors, while smaller than the United States, include significant operations requiring filter equipment. Mexico is experiencing industrial growth and represents an emerging market for filter equipment.

The region has a well-developed market with established filter manufacturers, integrators, and service providers. Industrial companies in North America are early adopters of advanced technologies including AI-enabled harmonic mitigation systems. The region's focus on operational efficiency and equipment protection drives investment in advanced filter systems. Stringent regulatory requirements and power quality standards create demand for equipment that ensures compliance and safety.

The presence of major industrial companies with global operations drives demand for consistent, high-quality equipment across facilities. The trend toward nearshoring and facility expansion in North America is supporting equipment demand. Investment in industrial facility upgrades and modernization to improve efficiency continues to support market growth. The region's mature market is characterized by replacement demand for aging equipment and adoption of advanced technologies to improve efficiency and reliability.

Which Factors Support the Europe Harmonic Filters Market Growth?

Europe has a well-established industrial sector. Germany is a major industrial hub with strong engineering capabilities and a large industrial base. The region's stringent regulatory standards including power quality and environmental regulations drive manufacturers to invest in advanced equipment. The industrial and power quality sectors in Europe are well-developed with major harmonic mitigation requirements.

The European market is characterized by a focus on quality, reliability, and advanced manufacturing. Manufacturers are increasingly adopting advanced harmonic filters to improve efficiency and control. The industrial sectors in Europe are well-developed with significant operations requiring advanced filter systems. The region's focus on environmental compliance and stringent power quality standards drive investment in advanced filter systems. The industrial and power quality sectors in Europe require sophisticated harmonic mitigation systems.

The region benefits from a well-developed infrastructure including filter manufacturers, integrators, and technical expertise. The presence of major multinational corporations with European industrial operations drives demand for high-performance equipment. Investment in industrial facility upgrades to improve efficiency and sustainability continues to support market growth. The trend toward automation and Industry 4.0 integration is driving adoption of advanced filter systems with monitoring capabilities.

Some of the major companies operating in the global harmonic filters market include ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation plc, General Electric Company, Mitsubishi Electric Corporation, Danfoss A/S, Rockwell Automation, Crompton Greaves Consumer Electricals Ltd. (CG Power & Industrial Solutions), Emerson Electric Co., Hitachi Energy Ltd., TDK Corporation, Schaffner Holding AG, MTE Corporation, HYOSUNG Heavy Industries, Larsen & Toubro Limited, Toshiba Corporation, Comsys AB, Arteche Group, Legrand SA, Fuji Electric Co., Ltd., Yaskawa Electric Corporation, Delta Electronics, Inc., and EPCOS (a TDK Group company). These companies focus on developing advanced harmonic mitigation systems, active and passive harmonic filters, smart power quality solutions, and digitally connected power management technologies designed for applications across industrial facilities, renewable energy systems, utilities, data centers, transportation, and smart grid infrastructure. Increasing investments in industrial electrification, renewable energy integration, smart grids, IoT-enabled monitoring systems, and energy-efficient power infrastructure are intensifying competition and driving innovation in the global harmonic filters market.

The global harmonic filters market is expected to grow from USD 1.65 billion in 2026 to USD 3.73 billion by 2036.

The global harmonic filters market is projected to grow at a CAGR of 8.5% from 2026 to 2036.

The primary drivers include increasing demand for power quality improvement, harmonic distortion reduction, renewable energy integration, industrial electrification, and compliance with IEEE and IEC power quality standards. According to the IEA, global electricity demand is expected to grow by around 4% annually through 2027, while IRENA reported that global renewable power capacity expanded by over 580 GW in 2024, increasing demand for harmonic mitigation technologies across modern electrical networks.

The passive harmonic filters segment is expected to dominate the market in 2026, accounting for approximately 41% of the overall market share, driven by cost-effectiveness, reliability, and broad industrial adoption. The active harmonic filters segment is expected to witness the fastest CAGR during the forecast period due to superior dynamic harmonic mitigation capabilities and growing demand from renewable energy and industrial automation applications.

The industrial segment is expected to hold the largest share of the harmonic filters market in 2026, supported by rising industrial automation and increasing use of power electronics in manufacturing operations. The renewable energy segment is expected to witness the fastest growth during the forecast period, driven by expanding solar, wind, energy storage, and grid modernization projects globally.

Asia-Pacific is expected to dominate the global harmonic filters market in 2026, driven by rapid industrialization, renewable energy expansion, and increasing investments in electrical infrastructure across China, India, and Southeast Asia. North America is expected to witness steady growth due to stringent power quality standards, industrial modernization, and data center expansion.

Major trends include increasing adoption of smart and connected power quality solutions, IoT-enabled harmonic filters, predictive maintenance systems, and renewable energy-compatible harmonic mitigation technologies. Growing focus on grid modernization, industrial automation, energy efficiency, and advanced monitoring capabilities is accelerating demand for intelligent harmonic filtering systems.

Major companies operating in the global harmonic filters market include ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation plc, General Electric Company, Mitsubishi Electric Corporation, Danfoss A/S, Rockwell Automation, Crompton Greaves Consumer Electricals Ltd. (CG Power & Industrial Solutions), Emerson Electric Co., Hitachi Energy Ltd., TDK Corporation, Schaffner Holding AG, MTE Corporation, HYOSUNG Heavy Industries, Larsen & Toubro Limited, Toshiba Corporation, Comsys AB, Arteche Group, Legrand SA, Fuji Electric Co., Ltd., Yaskawa Electric Corporation, Delta Electronics, Inc., and EPCOS (a TDK Group company). These companies are investing in advanced power quality solutions, smart harmonic mitigation technologies, IoT-enabled monitoring systems, and renewable energy integration solutions to support modern industrial and utility applications.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Market Analysis, By Type

3.3. Market Analysis, By Application

3.4. Market Analysis, By Geography

3.5. Competitive Analysis

4. Market Insights

4.1. Introduction

4.2. Global Harmonic Filters Market: Impact Analysis of Market Drivers (2026-2036)

4.2.1. Increasing Regulatory Requirements for Power Quality

4.2.2. Growing Demand from Industrial Facilities and Data Centers

4.2.3. Expansion of Renewable Energy and Power System Infrastructure

4.3. Global Harmonic Filters Market: Impact Analysis of Market Restraints (2026-2036)

4.3.1. High Initial Cost and Complex Installation Requirements

4.3.2. Lack of Standardization and Compatibility Challenges

4.4. Global Harmonic Filters Market: Impact Analysis of Market Opportunities (2026-2036)

4.4.1. Expansion in Emerging Markets and Industrial Growth

4.4.2. Development of Specialized Applications and Advanced Technologies

4.5. Global Harmonic Filters Market: Impact Analysis of Market Challenges (2026-2036)

4.5.1. Rapid Technological Change and Product Obsolescence

4.6. Global Harmonic Filters Market: Impact Analysis of Market Trends (2026-2036)

4.6.1. Shift Towards Smart and Connected Power Quality Solutions

4.6.2. Growing Demand for Renewable Energy Integration and Power Quality

4.7. Porter's Five Forces Analysis

4.7.1. Threat of New Entrants

4.7.2. Bargaining Power of Suppliers

4.7.3. Bargaining Power of Buyers

4.7.4. Threat of Substitute Products

4.7.5. Competitive Rivalry

5. The Impact of Sustainability on the Global Harmonic Filters Market

5.1. Introduction to Sustainability in Power Quality Solutions

5.2. Energy Efficiency and Carbon Footprint Reduction

5.3. Extended Product Life and Durability

5.4. Waste Reduction and Material Recycling

5.5. Life Cycle Assessment and Environmental Impact

5.6. Green Manufacturing and Certifications

5.7. Impact on Market Growth and Investment Trends

6. Competitive Landscape

6.1. Introduction

6.2. Key Growth Strategies

6.2.1. Market Differentiators

6.2.2. Synergy Analysis: Major Deals & Strategic Alliances

6.3. Competitive Dashboard

6.3.1. Industry Leaders

6.3.2. Market Differentiators

6.3.3. Vanguards

6.3.4. Emerging Companies

6.4. Vendor Market Positioning

6.5. Market Ranking by Key Players

7. Global Harmonic Filters Market, By Type

7.1. Introduction

7.2. Passive Harmonic Filters

7.3. Active Harmonic Filters

7.4. Hybrid Harmonic Filters

7.5. Tuned Harmonic Filters

7.6. Broadband Harmonic Filters

7.7. Series Harmonic Filters

7.8. Shunt Harmonic Filters

7.9. Specialized Harmonic Filters

7.10. Others

8. Global Harmonic Filters Market, By Application

8.1. Introduction

8.2. Industrial

8.2.1. Manufacturing

8.2.2. Equipment Protection

8.2.3. Power Quality

8.3. Utility

8.3.1. Power Distribution

8.3.2. Grid Stability

8.3.3. Power Quality

8.4. Commercial

8.4.1. Office Buildings

8.4.2. Retail Facilities

8.4.3. Data Centers

8.5. Renewable Energy

8.5.1. Wind Energy

8.5.2. Solar Energy

8.5.3. Grid Integration

8.6. Transportation

8.6.1. Electric Vehicles

8.6.2. Rail Systems

8.6.3. Charging Infrastructure

8.7. Others

9. Harmonic Filters Market, By Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. India

9.4.3. Japan

9.4.4. South Korea

9.4.5. Australia

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Argentina

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. ABB Ltd.

10.2. Siemens

10.3. Schneider Electric

10.4. Eaton Corporation

10.5. General Electric

10.6. Mitsubishi Electric

10.7. Danfoss

10.8. Rockwell Automation

10.9. Crompton Greaves

10.10. Emerson Electric

10.11. Others

11. Appendix

11.1. Questionnaire

11.2. Available Customization

Published Date: Feb-2026

Published Date: Aug-2025

Published Date: Nov-2024

Published Date: Oct-2024

Published Date: Oct-2024

Subscribe to get the latest industry updates