Resources

About Us

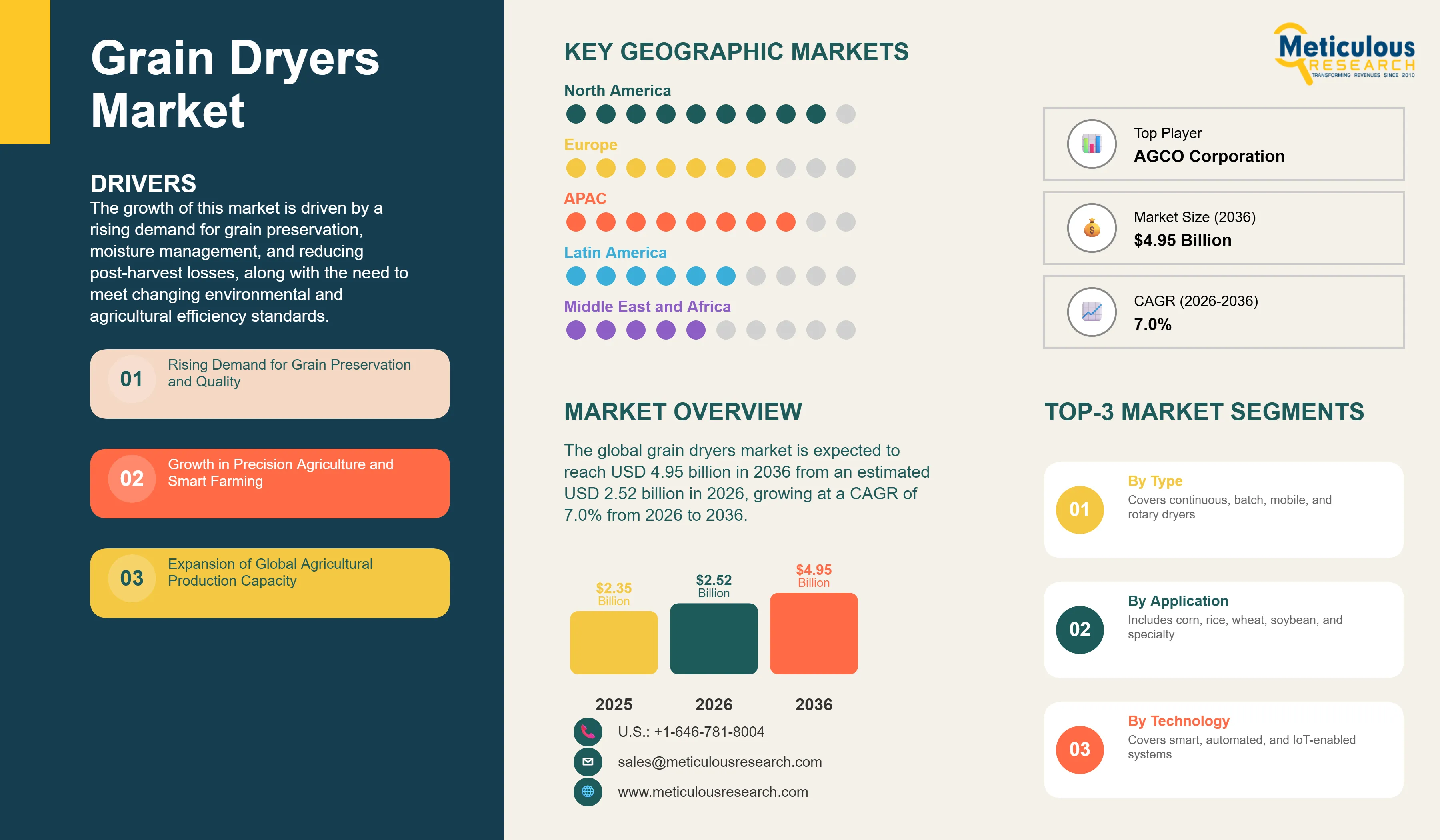

The global grain dryers market size was valued at USD 2.35 billion in 2025. This market is expected to reach USD 4.95 billion in 2036 from an estimated USD 2.52 billion in 2026, growing at a CAGR of 7.0% from 2026 to 2036.

The growth of this market is driven by a rising demand for grain preservation, moisture management, and reducing post-harvest losses, along with the need to meet changing environmental and agricultural efficiency standards. According to the FAO, global cereal production is expected to exceed 3 billion metric tons, while cereal use is projected to reach nearly 2.95 billion metric tons in 2025/26. This indicates increasing pressure on storage and post-harvest handling systems. Additionally, the OECD-FAO Agricultural Outlook 2025-2034 estimates that food loss and waste in the cereal sector remains about 19% of global cereal production. This underlines the need for better drying, storage, and processing technologies to minimize spoilage and maintain grain quality.

The growing use of modern grain dryer technologies is also fueled by a stronger emphasis on optimizing crop quality, improving energy efficiency, reducing emissions, and integrating with smart farming systems. Modern drying systems that feature automation, IoT-based monitoring, and precision moisture control are becoming popular as farmers and grain processors aim to boost operational efficiency, lower post-harvest losses, and meet sustainability goals in large-scale agriculture.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The grain dryers market encompasses the design, manufacturing, installation, and maintenance of dryer systems designed to efficiently reduce moisture content in harvested grains across agricultural operations. These systems are engineered to provide efficient grain drying, crop preservation, and compliance with environmental standards in diverse agricultural environments. Grain dryers are a fundamental component in modern agriculture where efficient grain preservation and quality maintenance are essential.

The market includes various dryer types designed for specific applications and performance requirements. Continuous flow dryers provide high-volume grain drying. Batch dryers provide controlled grain drying. Mobile dryers provide portable grain drying. In-bin dryers provide on-farm grain drying. Rotary dryers provide efficient moisture reduction. Recirculating dryers provide advanced grain conditioning. Cross-flow dryers provide uniform grain drying. Mixed-flow dryers provide optimized grain drying.

The market is primarily driven by increasing grain preservation demand, growing need for efficient moisture reduction, technological advancements that enhance performance and efficiency, and the shift toward precision agriculture. These systems find applications in corn drying, rice drying, and specialty grain drying where efficient grain preservation is essential.

How is Technology Innovation Transforming the Grain Dryers Market?

What are the Key Trends in the Grain Dryers Market?

Shift Towards Precision and Smart Grain Drying

The growth of this market is driven by a rising demand for grain preservation, moisture management, and reducing post-harvest losses, along with the need to meet changing environmental and agricultural efficiency standards. According to the FAO, global cereal production is expected to exceed 3 billion metric tons, while cereal use is projected to reach nearly 2.95 billion metric tons in 2025/26. This indicates increasing pressure on storage and post-harvest handling systems. Additionally, the OECD-FAO Agricultural Outlook 2025-2034 estimates that food loss and waste in the cereal sector remains about 19% of global cereal production. This underlines the need for better drying, storage, and processing technologies to minimize spoilage and maintain grain quality.

The growing use of modern grain dryer technologies is also fueled by a stronger emphasis on optimizing crop quality, improving energy efficiency, reducing emissions, and integrating with smart farming systems. Modern drying systems that feature automation, IoT-based monitoring, and precision moisture control are becoming popular as farmers and grain processors aim to boost operational efficiency, lower post-harvest losses, and meet sustainability goals in large-scale agriculture.

Growing Demand for Sustainable Grain Processing and Environmental Compliance: Another important trend driving growth in the grain dryers market is the increasing demand for sustainable grain processing and environmental compliance. Sustainable farming requires efficient grain drying for environmental protection. Advanced designs enable sustainable grain preservation. Integrated monitoring enables continuous optimization. Improved efficiency reduces environmental impact.

The trend toward sustainable agriculture is driving adoption of advanced dryers. The development of advanced drying technologies has enabled superior grain efficiency. The growing focus on environmental compliance is driving adoption of efficient dryer systems. The trend toward digital transformation is driving adoption of intelligent dryer systems. These sustainable grain processing and environmental compliance trends are creating opportunities for dryer manufacturers to develop innovative solutions and capture market share in sustainable farming applications.

|

Report Metric |

Details |

|---|---|

|

Market Size by 2036 |

USD 4.95 Billion |

|

Market Size in 2025 |

USD 2.35 Billion |

|

Market Size in 2026 |

USD 2.52 Billion |

|

Market Growth Rate (CAGR) 2026 to 2036 |

7.0% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Technology, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Increasing Demand for Grain Preservation and Quality Maintenance

A key factor driving the growth of the grain dryers market is the increasing demand for grain preservation, moisture management, and quality maintenance globally. Efficient grain drying is essential for reducing post-harvest losses, preventing spoilage, and maintaining crop quality during storage and transportation. According to the FAO, nearly 13% of food produced globally is lost between harvest and retail, highlighting the growing importance of improved post-harvest infrastructure and grain management systems. The expansion of agricultural production in emerging markets is creating substantial demand for advanced grain drying equipment and storage solutions.

The need to improve grain quality, reduce losses, and comply with evolving agricultural and environmental standards is accelerating adoption of advanced drying technologies. Growing investments in precision agriculture and modern farming systems are increasing demand for smart and energy-efficient dryers with improved monitoring capabilities. In addition, the development of new agricultural facilities, expansion of commercial farming operations, and increasing focus on food security are creating significant demand for reliable grain preservation solutions. The trend toward farm modernization and agricultural productivity improvement is expected to further support growth in the grain dryers market.

Growing Adoption of Precision Agriculture and Data-Driven Farming

The growing adoption of precision agriculture and data-driven farming is a major driver of the grain dryers market. Precision farming operations are expanding globally creating demand for efficient grain drying. Data-driven farming facilities are expanding creating demand for advanced dryer technology. The expansion of precision farming operations globally is creating substantial demand for dryer equipment. The trend toward agricultural modernization is driving adoption of advanced dryer systems.

The development of dryer systems that enable farming efficiency is enabling farmers to improve performance. The growing focus on grain quality optimization and resource efficiency is driving investment in advanced dryer systems. The trend toward sustainable farming is driving demand for efficient dryers. The expansion of precision farming operations globally is creating demand for dryers that improve grain drying precision. The trend toward facility expansion is driving demand for reliable grain preservation solutions.

Expansion of Agricultural and Farming Industries

The expansion of agricultural and farming industries globally is driving significant growth in the grain dryers market. Increasing agricultural production, modernization of farming operations, and investments in post-harvest infrastructure are creating strong demand for advanced grain drying equipment. According to the FAO, global cereal production is expected to exceed 3 billion metric tons, increasing the need for efficient grain handling, storage, and preservation systems. The expansion of agricultural activities in emerging markets is further supporting demand for grain dryer technologies.

The development of new agricultural facilities and growth in commercial farming operations are increasing adoption of advanced drying systems designed to improve grain quality and reduce post-harvest losses. In addition, the trend toward precision agriculture, automation, and smart farming technologies is driving investment in sophisticated grain dryers with enhanced monitoring and energy efficiency capabilities. The expansion of agricultural systems globally, coupled with increasing focus on food security and farm productivity, is expected to create significant demand for reliable grain preservation solutions.

High Initial Cost and Complex Integration Requirements

Despite its growth potential, the grain dryers market faces significant challenges due to high initial cost and complex integration requirements. Advanced dryers require substantial upfront investment, with complete systems costing thousands to millions of dollars. For smaller farms and agricultural businesses, these capital requirements represent a major barrier to adoption. The need for specialized integration and customization adds to total project costs. The complexity of dryer system design and integration requires specialized expertise, adding to implementation costs.

Training and change management costs are substantial, as agricultural personnel need to learn about new dryer systems and their operation. The need for ongoing maintenance, technical support, and system upgrades adds to total cost of ownership. The risk of technology obsolescence and the need for periodic system upgrades can be costly. For price-sensitive operators, particularly in developing economies, these financial barriers can slow adoption rates. The high integration complexity can restrict market growth among smaller farms or those with limited technical expertise.

Lack of Standardization and Compatibility Challenges

The lack of standardization in dryer designs and interfaces presents a significant restraint to market growth. Different manufacturers use different dryer architectures and connection types, creating compatibility challenges. The need for custom integration work increases implementation costs and complexity. The lack of standardized interfaces limits the ability to quickly swap components or upgrade systems.

The complexity of ensuring compatibility between dryer systems and different equipment types can be challenging and costly. The need to maintain compatibility with legacy systems while adopting new technologies creates operational complexity. The uncertainty about which standards will become dominant can make investment decisions difficult. The fragmentation of the market with multiple competing standards can slow adoption and create barriers for smaller manufacturers. These standardization challenges can slow market adoption and create barriers for farms seeking to implement advanced dryer systems.

Expansion in Emerging Markets and Agricultural Growth

The continued expansion of agricultural systems in emerging economies presents a significant growth opportunity for the grain dryers market. Countries across Asia-Pacific, including China, India, Vietnam, Indonesia, and Thailand, are witnessing increasing agricultural output driven by population growth, rising food demand, and investments in agricultural modernization. According to the FAO, global agricultural production must increase by nearly 50-70% by 2050 to meet rising food demand, accelerating the need for efficient post-harvest infrastructure and grain preservation technologies. The expansion of commercial farming and grain production in these regions is creating substantial demand for advanced drying systems.

Government initiatives promoting agricultural development and productivity are attracting investment and facility development. Infrastructure improvements including reliable power supply, transportation networks, and distribution systems are making these regions increasingly attractive for agricultural investments. Latin America and parts of Africa are also experiencing agricultural growth driven by economic development and foreign investment. The expansion of multinational corporations into emerging markets is bringing advanced agricultural technologies that drive demand for sophisticated dryer technology. As these regions develop their agricultural infrastructure, the installed base of dryers will expand significantly.

Development of Advanced Technologies and Specialized Applications

The development of advanced technologies and specialized applications for dryers is creating growth opportunities. Organic farming requires specialized dryers for organic grain preservation. Precision horticulture requires specialized dryers for targeted grain drying. Sustainable agriculture requires specialized dryer systems for environmental protection. Controlled environment agriculture requires specialized dryers for advanced grain management.

Regenerative agriculture systems require sophisticated dryers. Vertical farming applications require advanced dryers for adaptability. Smart farming applications require intelligent dryer systems. Environmental remediation systems require sophisticated dryers. These advanced applications, while currently representing smaller market segments, are growing rapidly and offer opportunities for dryer manufacturers to develop innovative solutions and capture niche markets with higher margins.

Rapid Technological Change and Product Obsolescence

The rapid pace of technological change in dryer technology and agricultural system management presents a significant challenge to the market. New technologies including advanced materials, AI integration, and IoT connectivity are emerging rapidly, potentially making existing dryer designs obsolete. Manufacturers must continuously invest in research and development to stay competitive and meet evolving customer needs. The risk of technology obsolescence can discourage investment in dryers, particularly among smaller manufacturers.

The challenge of maintaining compatibility between dryer systems and evolving equipment types can be complex and costly. The rapid pace of change means that training and skill development programs struggle to keep pace with new technologies. The need to support legacy systems while adopting new technologies creates operational complexity. The uncertainty about which technologies will become dominant can make investment decisions difficult. These technological challenges can slow market adoption and create barriers for smaller manufacturers or those lacking technical expertise.

Why are Continuous Flow Dryers Gaining Widespread Acceptance?

The continuous flow dryers segment is expected to command the largest share of the overall grain dryers market in 2026. Continuous flow dryers lead the market because they offer versatile grain drying, have proven and reliable designs, provide excellent performance for many applications, and have well-established service networks. These systems provide efficient grain drying at competitive cost. This proven technology makes continuous flow dryers ideal for corn drying, general grain preservation, and diverse agricultural applications where versatile grain drying is critical.

Continuous flow dryers work exceptionally well for conventional grain drying requiring efficient moisture reduction. They are widely used in agriculture for grain preservation. The farming sector uses continuous flow dryers for grain drying. Agricultural operations rely on continuous flow dryers for reliable grain preservation. Their proven design means they are reliable, require well-understood maintenance, and have extensive service networks across the industry. The availability of standardized designs allows for easy integration with different equipment types.

However, mobile grain dryers are expected to witness the fastest CAGR during the forecast period. Mobile grain dryers are gaining rapid adoption due to their portable grain drying capability, their superior performance in diverse applications, and their advanced customization capabilities compared to traditional dryers. These systems provide precision grain management and advanced customization. Mobile grain dryers are particularly valuable for applications requiring portable grain drying or advanced grain management.

The precision agriculture and data-driven farming industries rely heavily on mobile grain dryers for efficient grain preservation. The trend toward precision farming is driving adoption of mobile dryer technology. Advances in mobile dryer design have improved reliability and reduced costs, making them increasingly attractive for broader applications. The ability to provide portable grain drying makes mobile grain dryers increasingly valuable in diverse applications. The growing demand for precision agriculture is driving adoption of mobile dryer technology.

How does Corn Drying Dominate the Grain Dryers Market?

The corn drying segment is expected to hold the largest share of the grain dryers market in 2026. This dominance reflects the critical importance of grain drying in corn production. Corn drying systems use dryers extensively for grain preservation and quality maintenance. The corn drying industry requires sophisticated dryers for safe and efficient operations. The expansion of corn drying systems globally is creating significant demand for dryer equipment. The trend toward production optimization and grain quality improvement is driving demand for advanced dryers. The development of new corn drying facilities and the modernization of existing systems drive demand for advanced dryer systems. The trend toward advanced grain preservation is driving demand for high-performance dryers. The expansion of corn drying systems in emerging markets is creating significant demand for dryers. The trend toward operational excellence drives investment in advanced grain preservation technology.

However, the specialty grain drying segment is expected to witness the fastest CAGR during the forecast period. The specialty grain drying segment's growth is driven by expanding specialty grain capacity, development of new facilities, and increasing demand for grain quality optimization. Specialty grain drying facilities require dryers for efficient grain preservation and optimization. Specialty grain operations require specialized dryers for advanced grain management.

The trend toward specialty grain expansion is creating demand for specialized dryers for precision compliance. The development of new specialty grain drying facilities creates demand for advanced dryers. The expansion of specialty grain drying globally is creating significant demand for dryer systems. The growing demand for reliable and efficient grain preservation drives demand for advanced dryer systems. The trend toward precision compliance and advanced grain preservation adoption requires advanced grain preservation systems.

North America is expected to hold a significant share of the global grain dryers market in 2026. This comes from substantial agricultural infrastructure, well-developed precision agriculture sector, and significant investment in system modernization. The United States has major agricultural operations requiring advanced dryer systems. Canada's agricultural sector, while smaller than the United States, includes significant operations requiring dryer equipment. Mexico is experiencing agricultural growth and represents an emerging market for dryer equipment.

The region has a well-developed market with established dryer manufacturers, integrators, and service providers. Agricultural companies and farming operations in North America are early adopters of advanced technologies including AI-enabled grain preservation systems. The region's focus on efficiency and precision agriculture drives investment in advanced dryer systems. Stringent regulatory requirements and efficiency standards create demand for equipment that ensures compliance and efficiency.

The presence of major agricultural companies with global operations drives demand for consistent, high-quality equipment across facilities. The trend toward nearshoring and agricultural expansion in North America is supporting equipment demand. Investment in agricultural facility upgrades and modernization to improve efficiency continues to support market growth. The region's mature market is characterized by replacement demand for aging equipment and adoption of advanced technologies to improve efficiency and productivity.

However, Asia-Pacific is expected to hold the largest share of the global grain dryers market in 2026. This dominance comes from rapid agricultural expansion, significant farming development, and growing precision agriculture adoption across the region. China is the world's largest agricultural hub, creating enormous demand for dryers. The expansion of agricultural operations in China to serve the growing domestic market drives significant equipment demand. India's agricultural sector is expanding rapidly, creating demand for dryer equipment.

Vietnam, Indonesia, Thailand, and other Southeast Asian countries are experiencing rapid agricultural growth driven by foreign direct investment and rising food demand. The growing agricultural operations across Asia-Pacific are creating substantial demand for dryer equipment. Government initiatives promoting agricultural development and productivity are attracting investment and facility development. Infrastructure improvements including reliable power supply, transportation networks, and distribution systems are making these regions increasingly attractive for agricultural investments.

The region benefits from lower infrastructure costs and growing agricultural capacity, which makes it attractive for farming investments. The presence of major multinational corporations establishing or expanding operations in the region is driving demand for modern dryer equipment that meets global standards. The expansion of agricultural systems in Asia-Pacific is creating demand for advanced dryers. The trend toward agricultural modernization is creating demand for intelligent dryer systems with advanced capabilities.

Some of the major companies operating in the global grain dryers market include Bühler Group, AGCO Corporation, CNH Industrial, Cimbria, Sukup Manufacturing Co., GSI (Grain Systems, Inc.), Mathews Company (M-C), Brock Grain Systems, Alvan Blanch, Chief Industries, Shivvers Manufacturing, Mecmar Group, Perry Engineering, PETKUS Technologie GmbH, and CFCAI Group. These companies are focused on developing energy-efficient, automated, and IoT-enabled grain drying systems designed to improve grain quality, reduce post-harvest losses, and support precision agriculture practices. Increasing investments in smart drying technologies, sustainable farming solutions, and integrated grain handling systems are intensifying competition and driving innovation across the global grain dryers market.

The global grain dryers market is expected to grow from USD 2.52 billion in 2026 to USD 4.95 billion by 2036.

The global grain dryers market is projected to grow at a CAGR of 7.0% from 2026 to 2036.

The primary drivers include increasing demand for grain preservation, moisture management, and reduction of post-harvest losses, alongside rising investments in precision agriculture and smart farming. According to the FAO, nearly 13% of food produced globally is lost between harvest and retail, while global cereal production is projected to exceed 3 billion metric tons, increasing the need for efficient drying, storage, and grain handling systems.

The continuous flow dryers segment is expected to dominate the market in 2026, due to proven reliability, high-volume drying capability, and broad adoption in commercial grain operations. The mobile grain dryers segment is expected to witness the fastest CAGR during the forecast period, driven by growing demand for portable and precision agriculture solutions.

The corn drying segment is expected to hold the largest market share in 2026, supported by large-scale global corn production and increasing demand for grain quality preservation. The specialty grain drying segment is expected to register the fastest CAGR due to expanding specialty crop production and growing need for precision drying solutions.

Asia-Pacific is expected to lead the global grain dryers market in 2026, driven by rapid agricultural expansion, increasing food demand, and investments in farming modernization across China, India, and Southeast Asia. North America is expected to witness steady growth due to precision agriculture adoption and continued investments in agricultural modernization.

Major trends include the increasing adoption of IoT-enabled smart grain dryers, automation, AI-based monitoring systems, cloud connectivity, and precision moisture control technologies. Growing emphasis on sustainable farming, energy efficiency, and environmental compliance is also accelerating demand for advanced grain drying systems.

Major companies operating in the global grain dryers market include Bühler Group, AGCO Corporation, CNH Industrial, Cimbria, Sukup Manufacturing Co., GSI (Grain Systems, Inc.), Mathews Company (M-C), Brock Grain Systems, Alvan Blanch, Chief Industries, Shivvers Manufacturing, Mecmar Group, Perry Engineering, PETKUS Technologie GmbH, and CFCAI Group. These companies are investing in energy-efficient, automated, and IoT-enabled grain drying technologies to support precision agriculture and sustainable farming practices.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Market Analysis, By Type

3.3. Market Analysis, By Application

3.4. Market Analysis, By Geography

3.5. Competitive Analysis

4. Market Insights

4.1. Introduction

4.2. Global Grain Dryers Market: Impact Analysis of Market Drivers (2026-2036)

4.2.1. Increasing Demand for Grain Preservation and Quality Maintenance

4.2.2. Growing Adoption of Precision Agriculture and Data-Driven Farming

4.2.3. Expansion of Agricultural and Farming Industries

4.3. Global Grain Dryers Market: Impact Analysis of Market Restraints (2026-2036)

4.3.1. High Initial Cost and Complex Integration Requirements

4.3.2. Lack of Standardization and Compatibility Challenges

4.4. Global Grain Dryers Market: Impact Analysis of Market Opportunities (2026-2036)

4.4.1. Expansion in Emerging Markets and Agricultural Growth

4.4.2. Development of Advanced Technologies and Specialized Applications

4.5. Global Grain Dryers Market: Impact Analysis of Market Challenges (2026-2036)

4.5.1. Rapid Technological Change and Product Obsolescence

4.6. Global Grain Dryers Market: Impact Analysis of Market Trends (2026-2036)

4.6.1. Shift Towards Precision and Smart Grain Drying

4.6.2. Growing Demand for Sustainable Grain Processing and Environmental Compliance

4.7. Porter's Five Forces Analysis

4.7.1. Threat of New Entrants

4.7.2. Bargaining Power of Suppliers

4.7.3. Bargaining Power of Buyers

4.7.4. Threat of Substitute Products

4.7.5. Competitive Rivalry

5. The Impact of Sustainability on the Global Grain Dryers Market

5.1. Introduction to Sustainability in Agricultural Solutions

5.2. Energy Efficiency and Carbon Footprint Reduction

5.3. Extended Product Life and Durability

5.4. Waste Reduction and Material Recycling

5.5. Life Cycle Assessment and Environmental Impact

5.6. Green Manufacturing and Certifications

5.7. Impact on Market Growth and Investment Trends

6. Competitive Landscape

6.1. Introduction

6.2. Key Growth Strategies

6.2.1. Market Differentiators

6.2.2. Synergy Analysis: Major Deals & Strategic Alliances

6.3. Competitive Dashboard

6.3.1. Industry Leaders

6.3.2. Market Differentiators

6.3.3. Vanguards

6.3.4. Emerging Companies

6.4. Vendor Market Positioning

6.5. Market Ranking by Key Players

7. Global Grain Dryers Market, By Type

7.1. Introduction

7.2. Continuous Flow Dryers

7.3. Batch Dryers

7.4. Mobile Grain Dryers

7.5. In-Bin Dryers

7.6. Rotary Dryers

7.7. Recirculating Dryers

7.8. Cross-Flow Dryers

7.9. Mixed-Flow Dryers

7.10. Others

8. Global Grain Dryers Market, By Application

8.1. Introduction

8.2. Corn Drying

8.2.1. Grain Preservation

8.2.2. Quality Maintenance

8.2.3. Yield Improvement

8.3. Rice Drying

8.3.1. Precision Grain Preservation

8.3.2. Advanced Grain Management

8.3.3. Quality Assurance

8.4. Wheat Drying

8.4.1. Grain Preservation

8.4.2. Grain Optimization

8.4.3. Productivity Enhancement

8.5. Soybean Drying

8.5.1. Precision Grain Placement

8.5.2. Advanced Grain Management

8.5.3. Quality Assurance

8.6. Specialty Grain Drying

8.6.1. Precision Grain Preservation

8.6.2. Environmental Compliance

8.6.3. Sustainability Assurance

8.7. Others

9. Grain Dryers Market, By Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. India

9.4.3. Japan

9.4.4. South Korea

9.4.5. Australia

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Argentina

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Bühler Group

10.2. CFCAI Group

10.3. Cimbria

10.4. AGCO Corporation

10.5. CNH Industrial

10.6. Alvan Blanch

10.7. Westrup

10.8. Sukup Manufacturing

10.9. Mathews Company

10.10. Aeroglide Corporation

10.11. Others

11. Appendix

11.1. Questionnaire

11.2. Available Customization

Subscribe to get the latest industry updates