Resources

About Us

Biological Seed Treatment Market by Type (Microbial, Biochemical), Formulation (Liquid, Dry), Function (Seed Protection, Seed Enhancement), Application Technique (Seed Coating, Seed Pelleting, Seed Priming, Seed Dressing), and Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables) -— Global Opportunity Analysis and Industry Forecast (2026–2036)

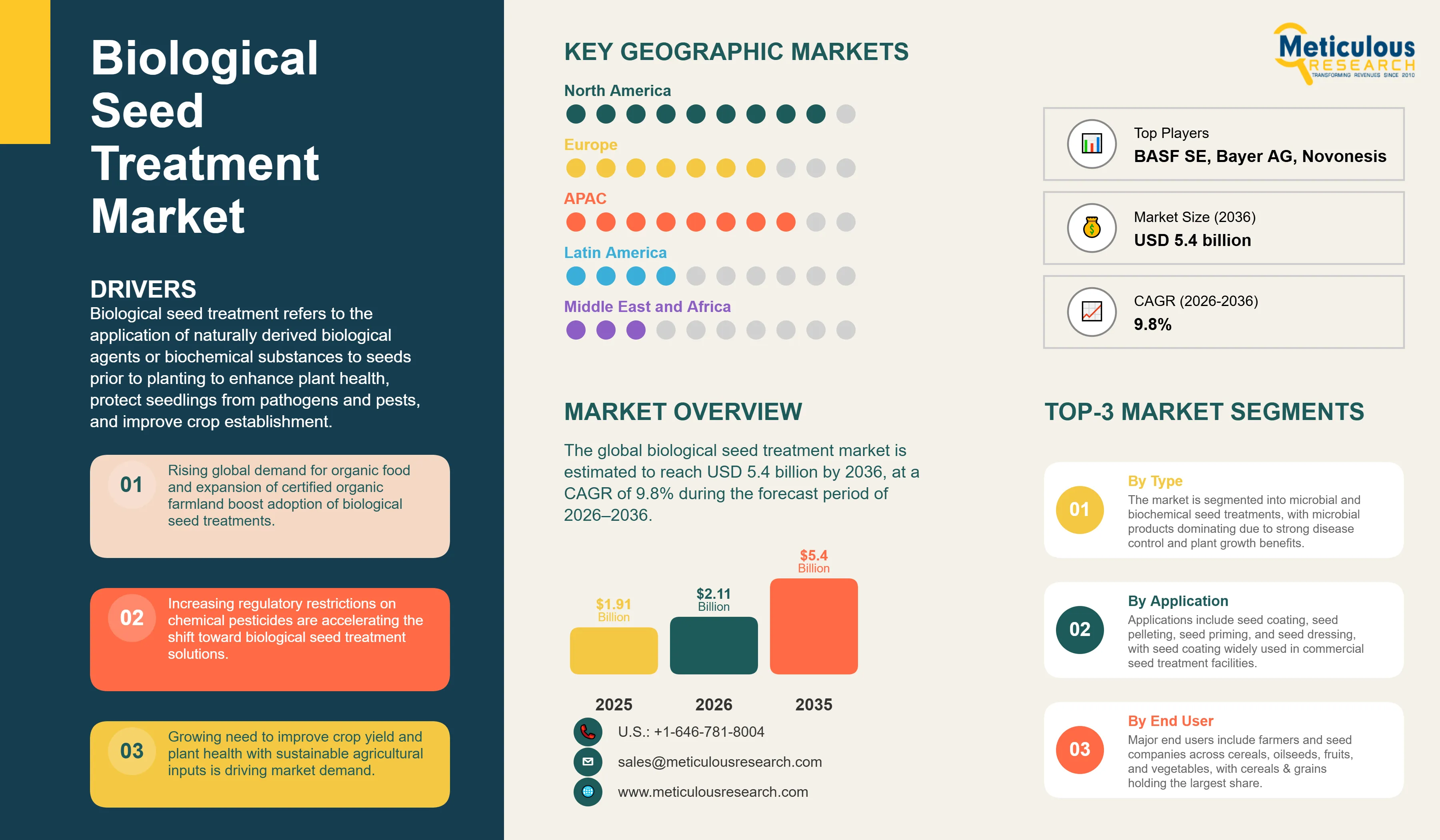

Report ID: MRAGR - 104652 Pages: 365 Mar-2026 Formats*: PDF Category: Agriculture Delivery: 24 to 48 Hours Download Free Sample ReportThe global biological seed treatment market was valued at USD 1.91 billion in 2025. This market is estimated to reach USD 5.4 billion by 2036 from USD 2.11 billion in 2026, at a CAGR of 9.8% during the forecast period of 2026–2036.

Biological seed treatment refers to the application of naturally derived biological agents or biochemical substances to seeds prior to planting to enhance plant health, protect seedlings from pathogens and pests, and improve crop establishment. These treatments typically contain beneficial microorganisms, such as bacteria and fungi or naturally derived biochemical compounds that promote plant growth and suppress harmful pathogens during early crop development.

Unlike conventional chemical seed treatments that rely on synthetic fungicides, insecticides, and nematicides, biological seed treatments operate through biological interactions between microorganisms, plant roots, and the surrounding soil microbiome. Beneficial bacterial species such as Bacillus, Rhizobium, and Pseudomonas colonize the rhizosphere and enhance nutrient uptake, nitrogen fixation, and plant defense responses. Similarly, beneficial fungi, including Trichoderma species and mycorrhizal fungi, provide biological control against soil-borne pathogens while improving plant access to water and soil nutrients. In addition, biochemical inputs such as humic substances, seaweed extracts, and amino acid–based biostimulants promote root development and improve plant tolerance to abiotic stresses.

Biological seed treatments are gaining importance within modern agricultural systems as farmers increasingly adopt sustainable crop protection solutions that reduce reliance on synthetic agrochemicals. The market is mainly driven by the growing regulatory pressure on conventional pesticides, rising consumer demand for residue-free food products, and the expansion of organic farming systems worldwide. Policies aimed at reducing pesticide use, including the European Union’s Farm to Fork Strategy, which targets a 50% reduction in chemical pesticide use by 2030, are encouraging the adoption of biological crop protection technologies.

The growth of the overall biological seed treatment market is also driven by technological advancements in microbial discovery, fermentation processes, and seed coating technologies. These innovations are enabling manufacturers to develop stable formulations with improved shelf life and enhanced field performance, expanding the commercial viability of biological seed treatment products.

Biological seed treatments are used across a wide range of crop categories, including major row crops such as corn, soybean, wheat, cotton, rice, and canola, as well as vegetables, fruits, and horticultural crops. Applications are typically carried out in commercial seed treatment facilities operated by seed companies or specialized service providers using automated seed coating systems, although on-farm seed treatment remains common in certain emerging agricultural markets.

Click here to: Get Free Sample Pages of this Report

The global biological seed treatment market was valued at USD 1.91 billion in 2025. This market is estimated to reach USD 5.4 billion by 2036 from USD 2.11 billion in 2026, at a CAGR of 9.8% during the forecast period of 2026–2036.

|

Market Size by 2036 |

USD 5.4 Billion |

|

Market Size in 2025 (Base Year) |

USD 1.91 Billion |

|

Market Size in 2026 |

USD 2.11 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of ~9.8% |

|

Dominating Region (2026) |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Type: Microbial (Bacteria [Rhizobium, Bacillus, Pseudomonas, Other Bacteria]; Fungi [Trichoderma, Mycorrhizae, Other Fungi]; Others), Biochemical (Humic Acid, Seaweed Extracts, Amino Acid-Based Products, Other Biochemicals) By Formulation: Liquid Formulation; Dry Formulation (Wettable Powder, Dry Flowable/Water-Dispersible Granule) By Function: Seed Protection; Seed Enhancement By Application Technique: Seed Coating; Seed Pelleting; Seed Priming; Seed Dressing By Crop Type: Cereals & Grains (Corn/Maize, Wheat, Rice, Other Cereals & Grains); Oilseeds & Pulses (Soybean, Canola/Rapeseed, Sunflower, Cotton, Other Oilseeds & Pulses); Fruits & Vegetables; Other Crop Types By Geography: North America; Europe; Asia-Pacific; Latin America; Middle East & Africa |

|

Countries Covered |

North America (U.S.; Canada; Mexico); Europe (Germany; France; U.K.; Italy; Spain; Rest of Europe); Asia-Pacific (China; India; Japan; Australia; South Korea; Rest of Asia-Pacific); Latin America (Brazil; Argentina; Rest of Latin America); Middle East & Africa |

|

Key Companies |

BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, Novonesis (formerly Novozymes A/S), UPL Limited, Koppert Biological Systems, Valent BioSciences LLC, Verdesian Life Sciences LLC, Plant Health Care plc, Rizobacter Argentina S.A. (part of Bioceres Crop Solutions), Marrone Bio Innovations (now part of Bioceres Crop Solutions), Certis USA LLC, Precision Laboratories LLC, Locus Agriculture, Indigo Ag Inc., BioConsortia Inc., Italpollina S.p.A. (Hello Nature Group), Incotec Group, and BioWorks Inc. |

Growing Demand for Organic Food and Expansion of Certified Organic Farmland

The expansion of organic agriculture is one of the key drivers for the growth of biological seed treatments market. According to the Research Institute of Organic Agriculture (FiBL) and IFOAM – Organics International, global organic farmland reached 98.9 million hectares in 2023, continuing a long-term expansion trend from approximately 11 million hectares in 1999. Organic certification frameworks, such as the EU Organic Regulation (EU) 2018/848, the USDA National Organic Program, and equivalent regulatory systems in Canada, Japan, India, and Brazil, significantly restrict the use of synthetic pesticides and fungicides in organic crop production. As a result, biological seed treatments based on microbial inoculants, plant extracts, and biochemical biostimulants is one of the primary seed-stage protection tools available to organic farmers.

The continued growth of organic farmland, driven by rising consumer demand for residue-free food and government sustainability programs, is therefore creating significant demand for biological seed treatment products.

Regulatory Restrictions on Chemical Seed Treatments Creating Demand for Biological Alternatives

Increasing regulatory scrutiny of synthetic crop protection chemicals is driving the transition toward biological seed treatment solutions. The European Union banned the outdoor use of three neonicotinoid insecticides—imidacloprid, clothianidin, and thiamethoxam—in 2018 due to their impact on pollinators. At the same time, the EU’s Farm to Fork Strategy aims to reduce the overall use and risk of chemical pesticides by 50% by 2030, reinforcing the policy shift toward biological crop protection technologies. Similar regulatory trends are emerging globally. In the U.S., the Environmental Protection Agency (EPA) continues to evaluate older pesticide active ingredients through its registration review process while maintaining comparatively streamlined approval pathways for biological pesticides. These policy trends are encouraging agricultural input suppliers and seed companies to drive the development and commercialization of biological seed treatments that provide disease suppression and plant growth benefits without triggering regulatory restrictions.

Rising Pressure to Increase Agricultural Productivity on Limited Arable Land

Global food demand is increasing as the world population continues to expand. According to the United Nations Department of Economic and Social Affairs (UN DESA), the global population is projected to reach 8.5 billion by 2030 and approximately 9.7 billion by 2050. At the same time, the availability of arable land per capita has declined significantly over the past several decades. According to the Food and Agriculture Organization (FAO), global demand for cereals is expected to exceed 3 billion tonnes by 2050, compared with roughly 2.8 billion tonnes in the early 2020s, showcasing increasing demand for both food and livestock feed. These structural pressures are driving the adoption of technologies that improve crop productivity without expanding cultivated land area. Biological seed treatments contribute to this objective by improving seed germination, protecting seedlings from soil-borne pathogens, and enhancing nutrient uptake and root development through plant growth-promoting microorganisms.

Shift Toward Multi-Strain Microbial Consortia and Integrated Biological Formulations

The biological seed treatment market is evolving from single-microbe inoculants toward multi-strain microbial consortia and stacked biological formulations. Early commercial products were typically based on individual microorganisms such as Rhizobium for nitrogen fixation or Trichoderma for fungal disease suppression. Newer formulations increasingly combine multiple microbial strains, including nitrogen-fixing bacteria, phosphate-solubilizing microorganisms, and biological control agents, to deliver broader agronomic benefits and more consistent performance across varying soil and climatic conditions. This shift reflects both advances in microbial discovery technologies and growing farmer demand for multi-functional biological inputs that provide disease suppression, nutrient efficiency, and plant growth stimulation through a single seed treatment application.

Expanding Adoption in Specialty Crops and High-Value Horticulture

While biological seed treatments were initially concentrated in large-acreage row crops such as corn, soybean, and wheat, adoption is expanding rapidly in specialty crops such as vegetables, fruits, and ornamental plants. These production systems often operate under stricter residue requirements and frequently rely on greenhouse or controlled-environment agriculture systems where biological inputs are preferred. The global greenhouse horticulture industry is expanding rapidly, mainly in Europe, North America, and the Asia-Pacific, creating favorable conditions for biological seed treatments that support seedling establishment while maintaining residue-free production systems. In addition, hybrid vegetable seeds are significantly more expensive than commodity crop seeds, making the incremental cost of biological seed treatment relatively small compared with the total seed value, which further supports adoption in high-value crop production.

North America: Largest Market for Biological Seed Treatment

North America is the largest market for biological seed treatments, driven by the advanced seed treatment infrastructure of the U.S. and high adoption of commercial hybrid seeds. The U.S. agricultural system relies heavily on professionally treated seeds, particularly for major row crops such as corn and soybean, where seed treatment is widely integrated into commercial seed distribution channels. The presence of leading agricultural input companies and biotechnology firms, combined with active biological research programs and supportive regulatory frameworks for biological pesticides, further drives the growth of the biological seed treatment market in this region.

Europe: Regulatory-Driven Market Transformation

Europe is a major market for biological seed treatments due to the stringent environmental policies and the growing organic farming sector in the region. According to Eurostat, organic farming accounts for approximately 10% of total agricultural land in the European Union, with several countries exceeding this average. The EU’s long-term agricultural policy direction, including pesticide reduction targets under the Farm to Fork Strategy, is driving the transition toward biological crop protection technologies. Countries such as Germany, France, Italy, Spain, and the U.K. are the primary markets for biological seed treatments within the region.

Asia-Pacific: Fastest-Growing Market for Biological Seed Treatment

The Asia-Pacific biological seed treatment market is expected to grow at the fastest CAGR from 2026 to 2036. The factors such as the rapid expansion of sustainable agriculture initiatives, increasing awareness of biological inputs, and government programs promoting reduced pesticide use are driving market growth in the region. India and China are the largest markets within Asia-Pacific due to their extensive agricultural land areas, expanding organic farming sectors, and growing domestic biological crop protection industries. Other countries such as Japan, Australia, and South Korea are mature markets characterized by strict food safety standards and increasing adoption of sustainable agricultural technologies.

Key Players in the Global Biological Seed Treatment Market

The report provides a competitive landscape based on an extensive assessment of the product portfolios, geographic presence, and key strategic developments adopted by leading players in the biological seed treatment market. The key companies profiled in this market include BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, Novonesis (formerly Novozymes A/S), UPL Limited, Koppert Biological Systems, Valent BioSciences LLC, Verdesian Life Sciences LLC, Plant Health Care plc, Rizobacter Argentina S.A. (part of Bioceres Crop Solutions), Marrone Bio Innovations (now part of Bioceres Crop Solutions), Certis USA LLC, Precision Laboratories LLC, Locus Agriculture, Indigo Ag Inc., BioConsortia Inc., Italpollina S.p.A. (Hello Nature Group), Incotec Group, and BioWorks Inc., among others.

These companies are actively engaged in developing microbial seed treatments, biostimulants, and biological crop protection solutions aimed at improving seed performance, enhancing crop resilience, and supporting sustainable agricultural practices. Market leaders leverage extensive microbial strain libraries, fermentation technologies, and global distribution networks, while emerging biological technology firms focus on advanced microbiome discovery platforms, seed microbiome engineering, and crop-specific biological formulations.

Biological Seed Treatment Market, by Type

Biological Seed Treatment Market, by Formulation

Biological Seed Treatment Market, by Function

Biological Seed Treatment Market, by Application Technique

Biological Seed Treatment Market, by Crop Type

Biological Seed Treatment Market, by Geography

The global biological seed treatment market was valued at USD 1.91 billion in 2025 and is estimated to reach USD 2.11 billion in 2026. The market is projected to reach USD 5.37 billion by 2036, growing at a CAGR of 9.8% during the forecast period (2026–2036).

The microbial seed treatment segment is expected to account for the largest share of the market in 2026. Microbial products—including Bacillus, Rhizobium, Pseudomonas, and Trichoderma-based treatments—are widely adopted due to their proven efficacy in disease suppression, nitrogen fixation, and root development.

The seed enhancement segment is projected to register the highest growth during the forecast period. Increasing demand for biostimulant-based treatments that improve germination, nutrient uptake, and early plant vigor is driving growth in this segment.

The cereals & grains segment accounts for the largest share of the market, supported by the extensive global cultivation area of corn/maize, wheat, and rice and increasing adoption of biological seed treatments in large-scale row crop farming systems.

North America is expected to account for the largest share of the biological seed treatment market in 2026, driven by the region’s advanced seed treatment infrastructure, high adoption of commercial hybrid seeds, and strong biological crop protection R&D ecosystem.

The Asia-Pacific region is projected to register the highest CAGR during the forecast period, driven by rapid expansion of organic farming, government initiatives promoting sustainable agriculture, and increasing biological input adoption in India and China.

Key companies operating in this market include BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, Novonesis, UPL Limited, Koppert Biological Systems, Valent BioSciences, Verdesian Life Sciences, Plant Health Care plc, Rizobacter Argentina, Marrone Bio Innovations, Certis USA, Precision Laboratories, Locus Agriculture, Indigo Ag, BioConsortia, Italpollina, Incotec Group, and BioWorks Inc.

Market growth is driven by increasing demand for sustainable crop protection solutions, expanding organic farming area, regulatory restrictions on synthetic pesticides, and growing adoption of microbial and biostimulant-based seed technologies.

Key opportunities include advancements in microbial strain discovery, seed microbiome engineering, integration of biologicals with precision agriculture platforms, and expanding demand for residue-free crop production systems.

Challenges include limited shelf life of microbial products, variability in field performance under different environmental conditions, and complex regulatory approval processes in certain regions.

Published Date: Mar-2026

Published Date: Apr-2025

Published Date: Feb-2024

Published Date: Jan-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates