Resources

About Us

Plant Breeding Market by Method (Conventional & Biotechnological Breeding), Trait (Herbicide Tolerance, Disease Resistance, Abiotic Stress, Drought, Yield Improvement, Nutritional Quality), and Application (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Turf & Ornamentals) – Global Forecast to 2036

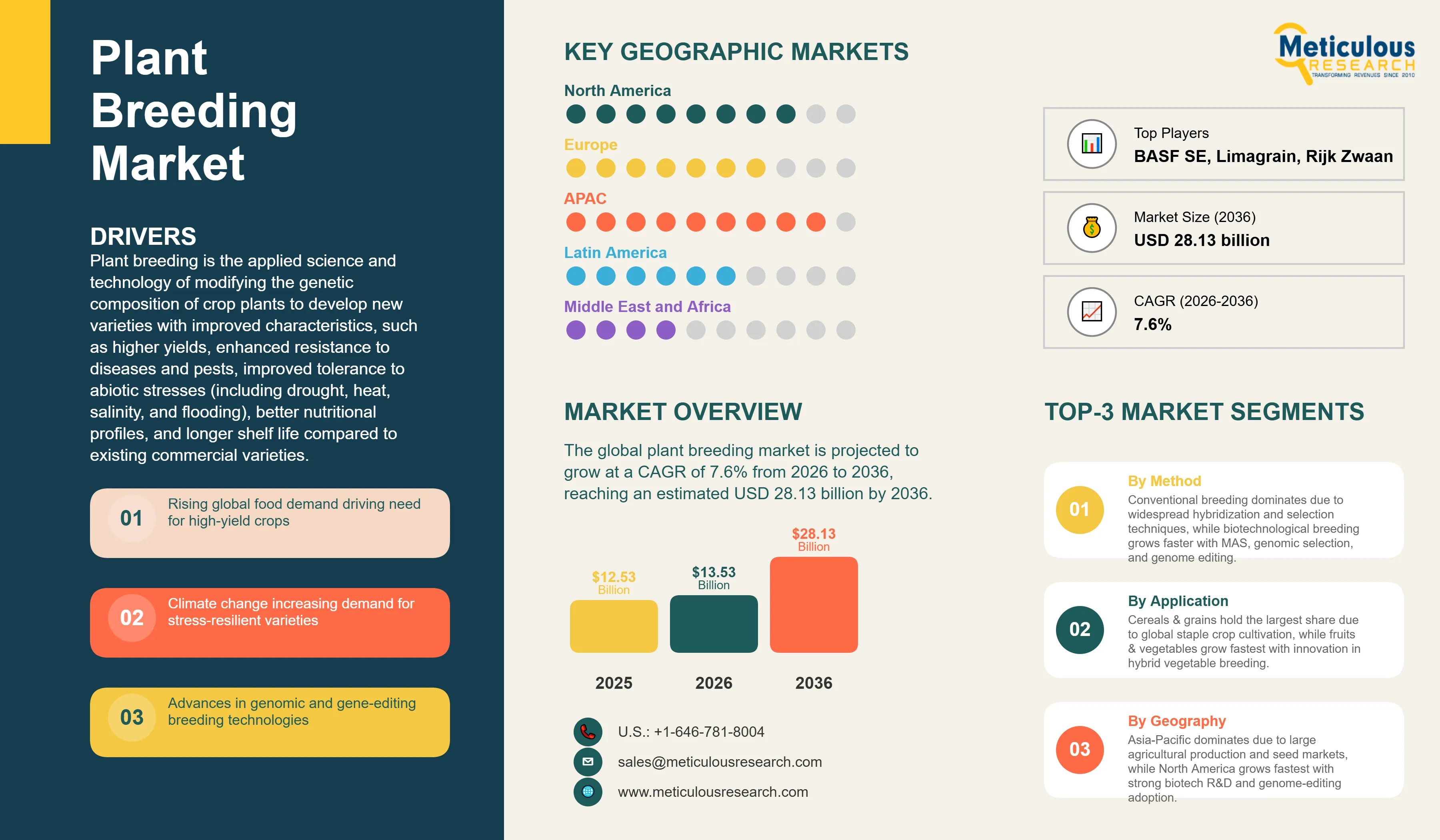

Report ID: MRAGR - 104703 Pages: 290 Mar-2026 Formats*: PDF Category: Agriculture Delivery: 24 to 48 Hours Download Free Sample ReportThe global plant breeding market was valued at USD 12.53 billion in 2025. This market is projected to grow at a CAGR of 7.6% from 2026 to 2036, reaching an estimated USD 28.13 billion by 2036 from USD 13.53 billion in 2026.

Plant breeding is the applied science and technology of modifying the genetic composition of crop plants to develop new varieties with improved characteristics, such as higher yields, enhanced resistance to diseases and pests, improved tolerance to abiotic stresses (including drought, heat, salinity, and flooding), better nutritional profiles, and longer shelf life compared to existing commercial varieties.

Modern plant breeding integrates a wide range of technologies spanning traditional field-based selection and controlled hybridization methods developed and refined since the foundational genetic work of Gregor Mendel in the 19th century to advanced molecular and computational approaches. These include marker-assisted selection (MAS), genomic selection (GS), doubled haploid technology, high-throughput phenotyping, and genome-editing tools such as CRISPR-Cas systems, transcription activator-like effector nucleases (TALENs), zinc finger nucleases (ZFNs), and oligonucleotide-directed mutagenesis (ODM). Increasing integration of artificial intelligence (AI), machine learning, and large-scale genomic datasets is improving breeding efficiency, enabling faster trait discovery and shortening breeding cycles in several crop improvement programs.

The importance of plant breeding has grown significantly in recent years due to increasing global food demand and climate-related agricultural challenges. According to United Nations projections, the global population is expected to reach approximately 9.7 billion by 2050, which will require substantial increase in agricultural productivity to meet rising food demand. At the same time, climate change is expected to adversely affect crop productivity in many regions. For example, climate modeling research published in Nature Food indicates that maize yields could decline significantly under high greenhouse gas emission scenarios, while rising temperatures and shifting rainfall patterns are already contributing to increased crop stress and yield variability in several agricultural regions.

In addition, regulatory and policy developments aimed at reducing the environmental impact of agriculture are influencing crop development priorities. For instance, the European Union’s Farm to Fork Strategy aims to reduce chemical pesticide use and associated risks by 50% by 2030, encouraging the development of crop varieties with improved pest and disease resistance. These factors are increasing the importance of plant breeding technologies that enable the development of more resilient, productive, and sustainable crop varieties.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

|

Market Size by 2036 |

USD 28.13 Billion |

|

Market Size in 2025 (Base Year) |

USD 12.53 Billion |

|

Market Size in 2026 |

USD 13.53 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 7.6% |

|

Dominating Region (2026) |

Asia-Pacific |

|

Fastest Growing Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Method: Conventional Breeding Method (Hybridization: Pedigree, Bulk, Back-Cross, Other Methods; Selection: Mass Selection, Pure Line Selection; Mutation Breeding), Biotechnological Breeding Method (Hybrid Breeding; Molecular Breeding; Genetic Engineering; Genome Editing [CRISPR-Cas9, Base Editing, Prime Editing, TALEN, ZFN, ODM]) By Trait: Herbicide Tolerance; Disease Resistance; Temperature & Abiotic Stress Tolerance; Drought Resistance; Yield Improvement; Nutritional Quality Enhancement; Other Traits By Application: Cereals & Grains (Wheat; Maize/Corn; Rice; Other Cereals & Grains); Oilseeds & Pulses; Fruits & Vegetables; Turf & Ornaments; Other Crop Types By Geography: North America; Europe; Asia-Pacific; Latin America; Middle East & Africa |

|

Countries Covered |

North America (U.S.; Canada); Europe (Germany; France; U.K.; Italy; Spain; Rest of Europe); Asia-Pacific (China; Japan; India; Australia; Philippines; Thailand; Vietnam; Rest of Asia-Pacific); Latin America (Brazil; Argentina; Mexico; Chile; Rest of Latin America); Middle East & Africa |

|

Key Companies |

Bayer AG, Syngenta Group, KWS SAAT SE & Co. KGaA, Corteva Agriscience, Limagrain, BASF SE, DLF Seeds A/S, Bioceres Crop Solutions Corp., UPL Limited, Benson Hill, Inc., Equinom Ltd., Rijk Zwaan, Sakata Seed Corporation, Pairwise, Cibus Inc., Evogene Ltd., Inari Agriculture, Inc., KeyGene, Takii & Co., Ltd., and East-West Seed. |

Intensifying Global Food Security Imperatives Amid Population Growth and Climate Disruption

One of the primary drivers of the plant breeding market is the growing need to improve global agricultural productivity in response to rising food demand and increasing climate-related risks to crop production. According to estimates from the Food and Agriculture Organization (FAO), global food production will need to increase by approximately 70% by 2050 to meet the needs of a growing global population.

At the same time, climate change is expected to place increasing pressure on agricultural systems worldwide. Research published in Nature Food indicates that global maize yields could decline by up to approximately 24% by 2030 under high greenhouse gas emission scenarios, highlighting the potential impact of rising temperatures and changing precipitation patterns on crop productivity.

In addition, climate variability is contributing to the expansion of crop pests and diseases into new geographic regions and increasing the frequency of droughts and extreme weather events that can significantly reduce crop yields. These challenges are increasing the importance of developing crop varieties with improved yield potential, stress tolerance, and disease resistance, which is driving demand for advanced plant breeding technologies and breeding programs globally.

Declining Costs and Increasing Accessibility of Genomic and Gene-Editing Technologies

Advances in genomic technologies and molecular breeding tools are also driving innovation in plant breeding. The cost of genome sequencing has declined dramatically over the past two decades from approximately USD 100 million for the first human genome sequence in 2001 to less than USD 1,000 today, according to data from the U.S. National Human Genome Research Institute (NHGRI). These cost reductions have enabled breeders to analyze large plant populations at the genomic level, significantly improving the efficiency of breeding programs.

Similarly, advances in next-generation sequencing (NGS), bioinformatics, and genome-editing technologies such as CRISPR-based systems have made molecular breeding approaches increasingly accessible to research institutions, biotechnology companies, and commercial seed developers. The availability of commercial gene-editing tools, reagents, and specialized research services has further expanded access to these technologies.

As a result, breeding programs are increasingly integrating marker-assisted selection, genomic selection, and genome-editing technologies to accelerate trait discovery and improve breeding efficiency, thereby driving the growth of the plant breeding market during the forecast period.

CRISPR Commercialization Accelerating Across Multiple Crop Categories

Genome-editing technologies, especially CRISPR-based systems, are increasingly transitioning from research-stage applications to commercial crop development. Several gene-edited crop products have already entered the market or are in advanced development stages across multiple crop categories. Early commercial examples of CRISPR-edited crops include the high-GABA tomato commercialized by Sanatech in Japan in 2021 and Pairwise’s CRISPR-derived mustard greens launched in the U.S. in 2023. These products marked some of the first consumer-facing applications of genome editing in agriculture. Since then, several companies, including Corteva Agriscience, Cibus, and Inari Agriculture, have expanded genome-editing pipelines targeting traits such as yield improvement, drought tolerance, and input efficiency across major crops such as corn, soybean, and wheat.

Several companies are also advancing genome-editing applications in major row crops. Cibus is developing gene-edited traits for canola, while Inari Agriculture is using multiplex gene-editing approaches combined with computational breeding platforms to develop improved varieties of corn, soybean, and wheat.

At the same time, ongoing advances in genome-editing technologies, including base editing and prime editing approaches that enable highly targeted genetic modifications without introducing double-strand DNA breaks, are expanding the range of traits that can be modified using precision breeding tools. These developments are expected to accelerate the commercialization of gene-edited crop varieties over the coming decade.

Expansion of Vegetable Seed Breeding Innovation

The fruits and vegetables segment is witnessing increasing innovation in plant breeding, driven by the high commercial value of hybrid vegetable seeds and strong market demand for improved horticultural traits. Compared to field crops, vegetable seeds command significantly higher prices due to the intensive breeding required to develop new varieties with desirable characteristics such as disease resistance, improved yield stability, longer shelf life, enhanced flavor profiles, and improved nutritional content.

Breeding programs in this segment are increasingly integrating molecular breeding tools, genomic selection, and digital phenotyping platforms to accelerate variety development and improve breeding efficiency. These technologies enable breeders to identify desirable genetic traits more quickly and shorten breeding cycles.

Several leading seed companies are expanding investments in vegetable breeding infrastructure and germplasm development. For example, Limagrain’s Hazera brand expanded its tomato breeding R&D capabilities in the Netherlands in 2024 through the development of a high-tech greenhouse research facility, while Syngenta Vegetable Seeds entered a licensing partnership with Apricus Seeds in 2025 to access new cucurbit germplasm.

Major vegetable seed companies such as Rijk Zwaan, Sakata Seed Corporation, Takii & Co., Ltd., and East-West Seed continue to invest in genomic breeding technologies and digital breeding platforms to accelerate the development of improved vegetable varieties. Similarly, Bayer expanded its fruit breeding capabilities through the acquisition of NIAB’s strawberry breeding program in 2023, highlighting the growing strategic importance of high-value horticultural crop breeding.

Asia-Pacific: Largest Regional Market for Plant Breeding

Asia-Pacific is expected to account for the largest share of the global plant breeding market in 2026, with its huge agricultural scale, the rapidly growing commercial seed markets in China, India, and Southeast Asia, and the competitive investment by both domestic companies and international players to establish and expand regional breeding and commercial seed operations. China is the largest Asia-Pacific market, driven by a strong government-backed agricultural modernization program, large state-owned seed companies (CNSG/China National Seed Group, Beijing Dabeinong), rapidly expanding commercial plant breeding capabilities, and a national priority on seed self-sufficiency and food security. India is one of the highest-growth plant breeding markets globally, driven by the enormous scale of Indian agriculture, the growing shift from traditional farm-saved seed to commercial hybrid seeds (particularly in hybrid rice, sorghum, and vegetable crops), and the substantial investments by multinational seed companies in India-specific breeding programs.

North America: Fastest-Growing Regional Market for Plant Breeding

North America is expected to grow at the fastest CAGR during the 2026–2036 forecast period, driven by the leading position of the U.S. in agricultural biotechnology R&D, a highly favorable regulatory environment for genome-edited crops, the commercial leadership of Corteva, Bayer CropScience, and a growing cohort of precision breeding innovators (Pairwise, Inari Agriculture, Benson Hill, Cibus), and government investment in agricultural genomics research through USDA NIFA and related programs. The large areas under corn and soybean cultivation, the high adoption rate of hybrid and biotech-trait seeds, and the strong commercial infrastructure for seed licensing and distribution make North America the global proving ground for new plant breeding innovations that subsequently diffuse to other markets. Canada is also a significant and growing market, particularly in canola breeding, where Cibus and Corteva are advancing CRISPR-edited varieties and pulse crops.

Europe: Regulatory Transformation Opening New Commercial Opportunities

Europe ranks among the world's top plant breeding regions, but strict EU GMO rules held it back for years. Even precisely edited crops faced the same heavy regulation as older GM technology under the 2001 rules. The 2018 court decision treating CRISPR like traditional GMOs discouraged investment across the EU.

The new Genomic Techniques Regulation, passed in 2024, changes everything. Plants with simple edits (NGT-1) matching conventional breeding now skip GMO requirements entirely. More complex edits (NGT-2) get a faster approval track. Germany, France, the UK (which launched its own Precision Breeding law in 2023), Italy, Spain, and the Netherlands lead Europe's breeding markets.

Companies are already moving: Germany's KWS rolled out new sugar beet varieties across Europe in February 2025. Limagrain opened a cutting-edge tomato research greenhouse in the Netherlands last November. Syngenta keeps expanding facilities in Spain and Thailand. These regulatory shifts finally unlock commercial potential for precision breeding in Europe.

Latin America: Biotech-Friendly Regulatory Environment Driving Adoption

Latin America is a high-growth plant breeding market, driven by science-based regulatory frameworks for new breeding techniques, large and expanding commercial agriculture sectors, and significant multinational and domestic investment in breeding programs aligned with Latin America’s major commodity crops such as soybean, corn, sugarcane, cotton, and sunflower.

Brazil and Argentina are the primary markets, collectively accounting for the majority of the plant breeding market value in Latin America. Bioceres Crop Solutions (Argentina), one of the key companies in LATAM, has developed an HB4 drought tolerance technology platform based on sunflower gene expression that has been approved in Argentina, Brazil, the U.S., Canada, and other markets for application in wheat and soybean, representing a Latin American-developed precision breeding innovation with global commercial reach.

The global plant breeding market is characterized by the presence of several large seed and agricultural biotechnology companies with extensive germplasm resources, advanced breeding technologies, and global seed production and distribution networks. The key companies profiled in this report include Bayer AG, Syngenta Group, KWS SAAT SE & Co. KGaA, Corteva Agriscience, Limagrain, BASF SE, DLF Seeds A/S, Bioceres Crop Solutions Corp., UPL Limited, Benson Hill, Inc., Equinom Ltd., Rijk Zwaan, Sakata Seed Corporation, Pairwise, Cibus Inc., Evogene Ltd., Inari Agriculture, Inc., KeyGene, Takii & Co., Ltd., and East-West Seed, among others.

Plant Breeding Market, by Method

Plant Breeding Market, by Trait

Plant Breeding Market, by Application

Plant Breeding Market, by Geography

The global plant breeding market was valued at USD 12.53 billion in 2025 and is projected to reach USD 28.13 billion by 2036, growing at a CAGR of 7.6% from 2026 to 2036. The market is expected to reach USD 13.53 billion in 2026.

The conventional breeding segment is expected to account for the largest share of the plant breeding market in 2026 due to the widespread adoption of hybridization and selection techniques in commercial seed programs. However, the biotechnological breeding segment is projected to register the fastest growth during the forecast period, driven by increasing adoption of marker-assisted breeding, genomic selection, and genome-editing technologies.

The abiotic stress tolerance segment, including drought and heat tolerance traits, is expected to record the fastest growth during the forecast period due to increasing climate variability and the growing need for climate-resilient crops. Herbicide tolerance and disease resistance remain among the most commercially important traits in major row crops.

The cereals & grains segment is expected to account for the largest share of the global plant breeding market due to the global cultivation scale of staple crops such as maize, wheat, and rice. The fruits & vegetables segment is projected to register strong growth driven by increasing innovation in vegetable seed breeding and rising demand for improved horticultural varieties.

The Asia-Pacific region is expected to account for the largest share of the global plant breeding market, supported by the region’s large agricultural sector and expanding commercial seed markets in countries such as China and India. North America is expected to register strong growth during the forecast period, driven by high R&D investment and favorable regulatory frameworks for advanced breeding technologies.

Key companies operating in the plant breeding market include Bayer AG, Syngenta Group, KWS SAAT SE & Co. KGaA, Corteva Agriscience, Limagrain, BASF SE, DLF Seeds A/S, Bioceres Crop Solutions Corp., UPL Limited, Benson Hill, Inc., Equinom Ltd., Rijk Zwaan, Sakata Seed Corporation, Pairwise, Cibus Inc., Evogene Ltd., Inari Agriculture, Inc., KeyGene, Takii & Co., Ltd., and East-West Seed, among others.

Published Date: Mar-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates