Resources

About Us

Floating Wind Turbine Market Size, Share & Trends Analysis by Platform Type (Spar-Buoy, Semi-Submersible), Water Depth, Turbine Capacity (Up to 5 MW, 5-10 MW), Application, and Project Stage - Global Opportunity Analysis & Industry Forecast (2026-2036)

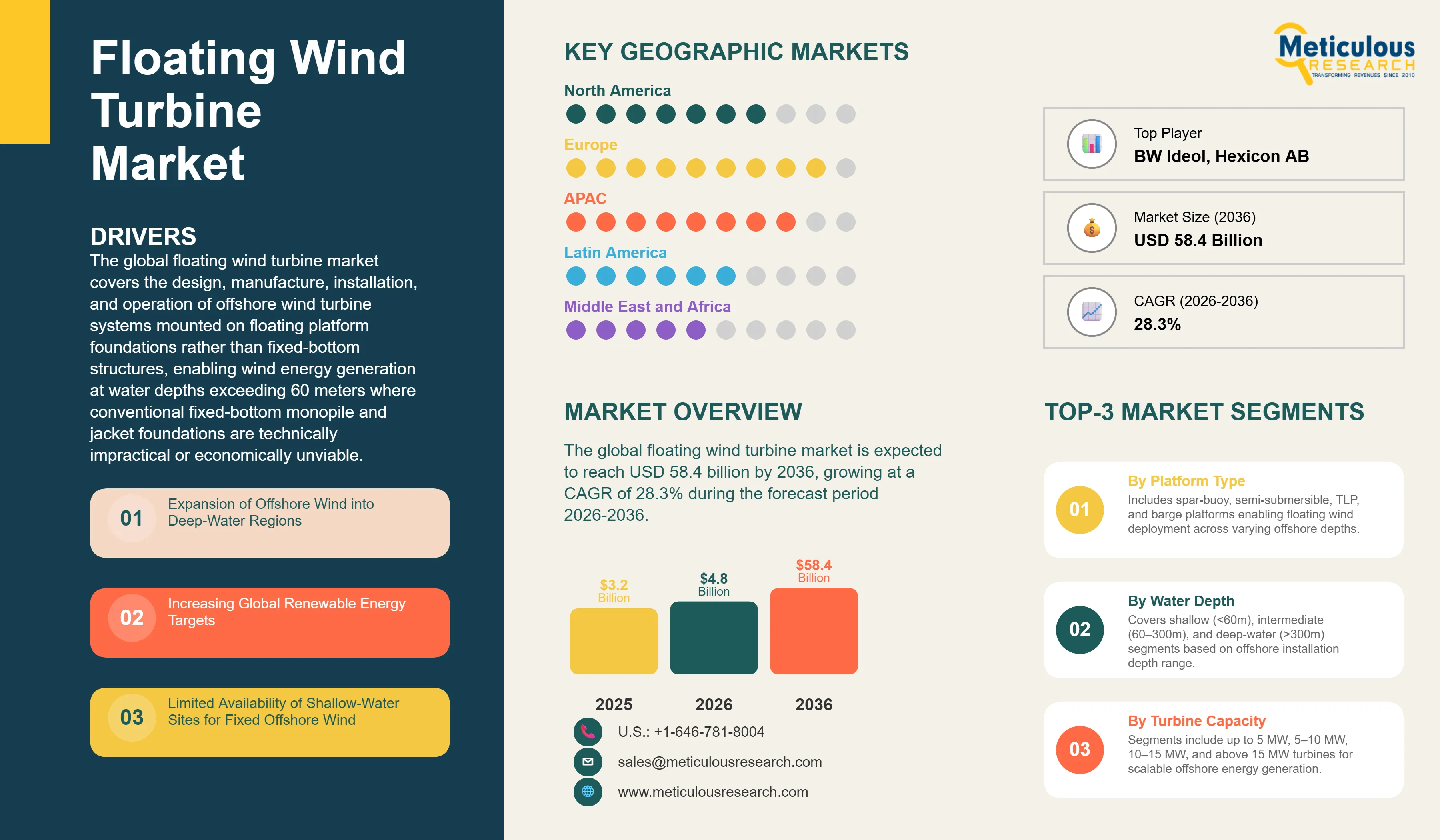

Report ID: MREP - 1041880 Pages: 290 Apr-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global floating wind turbine market was valued at USD 3.2 billion in 2025. This market is expected to reach USD 58.4 billion by 2036 from an estimated USD 4.8 billion in 2026, growing at a CAGR of 28.3% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global floating wind turbine market covers the design, manufacture, installation, and operation of offshore wind turbine systems mounted on floating platform foundations rather than fixed-bottom structures, enabling wind energy generation at water depths exceeding 60 meters where conventional fixed-bottom monopile and jacket foundations are technically impractical or economically unviable. The market encompasses all major floating platform architectures, including spar-buoy, semi-submersible, tension leg platform, and barge configurations, across the full project lifecycle from development and manufacturing through installation, grid connection, and operations and maintenance.

The growth of the global floating wind turbine market is primarily driven by the progressive exhaustion of accessible shallow-water fixed-bottom offshore wind sites in mature markets including the U.K., Germany, Denmark, and the Netherlands, which is pushing new offshore wind development into deeper waters where floating foundations are required. The availability of significantly stronger and more consistent wind resources at deep-water offshore locations, combined with the removal of visual impact and shipping lane conflict constraints that affect near-shore fixed-bottom developments, provides a compelling resource quality case for floating wind. The national renewable energy transition targets of Japan, South Korea, Norway, France, the U.K., and the United States all specifically identify floating wind as a critical technology for meeting long-term offshore wind capacity ambitions that cannot be met through fixed-bottom resources alone.

However, the market faces key constraints. The levelized cost of energy for floating wind projects currently ranges from USD 100 to 200 per megawatt-hour, representing a substantial premium over fixed-bottom offshore wind costs of USD 60 to 100 per megawatt-hour and an even larger premium over onshore wind. The specialized marine infrastructure required for floating wind installation, including heavy-lift vessels capable of turbine installation at deep-water sites and purpose-built installation ports with sufficient draft for float-out operations, represents a significant supply chain gap that is constraining the pace of project delivery.

Despite these challenges, the market outlook is strongly positive. The learning curve trajectory of floating wind costs is expected to deliver significant LCOE reductions through the forecast period as manufacturing scale increases, installation efficiency improves, and platform designs are standardized. The growing pipeline of commercial-scale floating wind projects in Europe, Asia-Pacific, and North America is creating the demand volume required to drive supply chain investment and manufacturing cost reduction. The strategic entry of major oil and gas companies including Equinor, Shell, TotalEnergies, and Aker Solutions into floating wind is bringing substantial capital, offshore project management expertise, and marine engineering capabilities that are accelerating the technology's commercial maturation.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 58.4 Billion |

|

Market Size in 2026 |

USD 4.8 Billion |

|

Market Size in 2025 |

USD 3.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 28.3% |

|

Dominating Platform Type |

Semi-Submersible |

|

Fastest Growing Platform Type |

Tension Leg Platform (TLP) |

|

Dominating Water Depth |

Intermediate Depth (60-300m) |

|

Fastest Growing Water Depth |

Deep Water (>300m) |

|

Dominating Turbine Capacity |

10-15 MW |

|

Fastest Growing Turbine Capacity |

Above 15 MW |

|

Dominating Application |

Utility-Scale Power Generation |

|

Fastest Growing Application |

Offshore Hydrogen Production |

|

Dominating Project Stage |

Pilot & Demonstration Projects |

|

Fastest Growing Project Stage |

Commercial Projects |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Shift Toward Commercial-Scale Floating Wind Projects

The transition of the floating wind industry from pilot and demonstration-scale deployments toward pre-commercial and commercial projects representing gigawatt-scale capacity is the defining market development trend of the current period. Equinor's Hywind Tampen project in Norway, a 88 MW floating wind farm supplying power to offshore oil and gas platforms, represents the current largest operational floating wind project and demonstrates the technical and commercial viability of floating wind at near-commercial scale. The U.K.'s ScotWind leasing round has allocated floating wind development rights covering approximately 4 GW of floating wind capacity, and the Celtic Sea floating wind program is targeting 4 GW of commercial capacity by 2035.

France's floating wind commercial tender program, Norway's Utsira Nord leasing process, and Portugal's WindFloat Atlantic expansion all represent advancing commercial-scale project pipelines that are driving supply chain investment and cost reduction programs across the floating wind value chain. The global floating wind project pipeline tracked by industry organizations including WindEurope and the Global Wind Energy Council has exceeded 250 GW in announced pre-commercial and commercial development capacity, providing the demand signal required to mobilize manufacturing scale investment in floating platforms, dynamic cables, and specialized installation infrastructure.

Strategic Entry of Oil and Gas Companies

The large-scale strategic entry of major international oil and gas companies into the floating wind sector is a distinctive and commercially significant trend that is distinguishing floating wind development from the utility-led model that characterized early fixed-bottom offshore wind. Equinor has established itself as the global technology leader in floating wind through the Hywind Scotland and Hywind Tampen projects and its major stakes in U.K. ScotWind and U.S. East Coast floating wind developments. Shell has entered floating wind through investments in the Sierra Madre floating wind project off California and through the North Sea and Atlantic margin development pipeline. TotalEnergies and Aker Solutions are advancing floating wind developments across European and Asian markets.

Oil and gas companies bring several competitive advantages to floating wind development that are reshaping the industry's competitive dynamics. Their deep experience in floating offshore structure engineering, subsea cable and mooring installation, and remote offshore operations and maintenance translates directly to floating wind project execution capabilities. Their access to capital markets and project finance at the scale required for gigawatt floating wind developments provides funding capacity unavailable to most renewable energy developers. Their existing relationships with offshore supply chain contractors, marine logistics providers, and regulatory authorities in offshore energy jurisdictions accelerate project development timelines. This strategic convergence of hydrocarbon and renewable energy expertise is creating a distinct competitive tier of integrated energy company floating wind developers that are advancing the sector's commercial maturity.

Increasing Turbine Size Toward and Beyond 15 MW

The progressive scaling of offshore wind turbine nameplate capacity toward and beyond 15 MW represents a critical commercial strategy for reducing the LCOE of floating wind by spreading the fixed costs of floating platform fabrication, mooring systems, dynamic cables, and installation operations across larger energy generation capacity per unit. Siemens Gamesa's SG 14-222 DD, Vestas's V236-15.0 MW, and GE Vernova's Haliade-X 14-15 MW platforms represent the current commercial generation of large offshore wind turbines being adapted for floating foundation deployment. Next-generation turbine platforms targeting 18 to 20 MW and beyond are in advanced development at all major turbine OEMs, targeting the floating wind market specifically as the primary application where the cost reduction benefit of maximum turbine scaling is most commercially impactful.

The deployment of 15 MW and larger turbines on floating foundations requires advancement in dynamic cable technology capable of handling higher power transmission loads, mooring system design optimization to manage the larger dynamic loads generated by multi-megawatt turbines, and floating platform buoyancy and structural engineering scaled for the greater nacelle and rotor mass of next-generation turbines. These engineering challenges are driving significant R&D investment across the floating wind supply chain and are creating competitive differentiation opportunities for technology providers that successfully develop commercially validated solutions for very large turbine floating foundation integration.

Expansion of Offshore Wind into Deep-Water Regions

The primary structural driver of the global floating wind turbine market is the progressive depletion of accessible shallow-water fixed-bottom offshore wind development sites in countries with mature offshore wind programs, which is driving the industry's geographic expansion into deeper waters where floating foundations are the only technically viable installation method. The U.K.'s North Sea shelf, the German Bight, and the Dutch North Sea exclusive economic zone all have limited remaining shallow-water development capacity after decades of fixed-bottom offshore wind buildout, and the government renewable capacity targets that require continued offshore wind expansion in these markets necessitate a transition to floating wind in deeper water locations. Similarly, the deep continental shelf topography of Japan, Norway's Atlantic coast, the U.S. Pacific Coast states, and much of the Mediterranean coastline means that the majority of the available offshore wind resource in these markets requires floating foundations, making floating wind technology development a strategic national energy priority rather than an optional premium technology.

Increasing Global Renewable Energy Targets

The escalating national and supranational renewable energy targets adopted across major economies in response to the Paris Agreement climate commitments and the energy security implications of the 2022 European energy crisis are driving unprecedented offshore wind capacity expansion ambitions that explicitly depend on floating wind technology to achieve their most ambitious targets. The European Union's REPowerEU program raised the EU offshore wind capacity target to 300 GW by 2050, with floating wind identified as providing 30 GW or more of this target. The U.K.'s North Sea Transition Deal and offshore wind sector deal identify floating wind as a priority technology for delivering the 50 GW offshore wind target for 2030 that cannot be met entirely from fixed-bottom resources. Japan's GW-class floating wind targets, South Korea's 14.3 GW offshore wind program incorporating substantial floating components, and the U.S. federal government's identification of floating wind as critical for Pacific and Atlantic deep-water leasing all translate directly into project development pipeline and technology investment demand.

Large Untapped Wind Potential in Deep-Sea Locations

The vast and largely unexploited offshore wind resource at water depths exceeding 60 meters represents the fundamental long-term commercial opportunity underpinning the floating wind market. The technical wind resource accessible to floating wind platforms covers ocean areas with exceptional wind speeds, high capacity factors, and large site extents that could theoretically supply multiples of current global electricity demand. Key strategic deep-water wind resource zones including the U.S. Pacific Coast, the Norwegian Sea, the Japanese Pacific coast, the Atlantic margins of Portugal, Spain, and Ireland, and the deep-water sites off South Korea and Taiwan collectively represent several hundred gigawatts of high-quality floating wind development potential that represents the growth pipeline for the floating wind industry through and beyond the 2026 to 2036 forecast period.

Hybrid Projects with Offshore Hydrogen Production

The growing interest in combining floating wind generation with offshore electrolysis infrastructure for green hydrogen production represents a significant near-term application and commercial opportunity that could substantially accelerate floating wind deployment by enabling projects to produce hydrogen for industrial offtake in addition to or instead of grid-connected electricity. Offshore hydrogen production eliminates the need for long-distance undersea grid connection cables, which represent 15 to 25% of floating wind project CapEx for distant deep-water sites, and allows hydrogen pipeline export to shore as an alternative to electricity cable infrastructure. Several European and Japanese development programs are advancing hybrid floating wind and offshore hydrogen concepts, including the HyDeal Ambition project targeting offshore hydrogen production from floating wind off France and Spain.

By Platform Type: In 2026, Semi-Submersible to Dominate

Based on platform type, the global floating wind turbine market is segmented into spar-buoy, semi-submersible, tension leg platform, and barge. In 2026, the semi-submersible segment is expected to account for the largest share of the global floating wind turbine market. The large share of this segment is attributed to the semi-submersible design's superior versatility across water depths from 60 to over 1,000 meters, the broader commercial development pipeline associated with semi-submersible concepts from developers including Principle Power's WindFloat platform, BW Ideol's damping pool design, and Hexicon's TwinWind multi-turbine semi-submersible, and the port-side assembly and wet-tow installation methodology that avoids the need for specialized heavy-lift vessel operations required by spar-buoy installations.

However, the tension leg platform (TLP) segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to TLP technology's particularly favorable motion characteristics that minimize dynamic loads on turbine components, the smaller structural material requirement relative to semi-submersible designs at moderate water depths, and the growing commercial interest in TLP concepts from developers targeting deployments in the 60 to 200 meter depth range where TLP designs offer compelling cost and performance advantages.

By Water Depth: In 2026, Intermediate Depth (60-300m) to Hold the Largest Share

Based on water depth, the global floating wind turbine market is segmented into shallow depth (below 60m), intermediate depth (60-300m), and deep water (above 300m). In 2026, the intermediate depth segment is expected to account for the largest share of the global floating wind turbine market. This dominance reflects the concentration of current and near-term floating wind project development in the 60 to 300 meter depth range, where established floating platform technologies including spar-buoy and semi-submersible designs have demonstrated commercial viability and where the strongest project pipelines across Europe, Asia-Pacific, and North America are located. The intermediate depth range also benefits from existing subsea cable and grid connection infrastructure proximity in the North Sea and Japanese offshore energy zones.

However, the deep water segment (above 300m) is projected to register the highest CAGR during the forecast period. This growth is driven by the progressive expansion of commercial floating wind development into deeper offshore zones as platform technology matures and LCOE declines, the large and high-quality wind resource available in deep-water locations off Japan's Pacific coast, the U.S. West Coast, and the Atlantic margins of Europe, and the strategic importance of very deep water floating wind development for countries including Japan and the U.S. Pacific states where the majority of offshore wind resource lies in water depths exceeding 300 meters.

By Turbine Capacity: In 2026, the 10-15 MW Segment to Hold the Largest Share

Based on turbine capacity, the global floating wind turbine market is segmented into up to 5 MW, 5-10 MW, 10-15 MW, and above 15 MW. In 2026, the 10-15 MW segment is expected to account for the largest share of the global floating wind turbine market. This dominance reflects the deployment of current-generation commercial offshore wind turbines from Siemens Gamesa, Vestas, and GE Vernova in the 10 to 15 MW class on floating foundations across the expanding pipeline of pilot, pre-commercial, and early commercial floating wind projects, where this turbine size range represents the optimal balance of available turbine technology maturity, platform engineering compatibility, and energy cost economics.

However, the above 15 MW segment is projected to register the highest CAGR during the forecast period. This growth is driven by the development of next-generation turbine platforms specifically targeting 18 to 22 MW capacity for floating wind applications, the strong cost reduction incentive of maximizing turbine capacity to spread fixed floating foundation costs across greater energy output, and the commitment of major turbine OEMs to develop and commercialize ultra-large offshore turbine platforms specifically optimized for floating wind deployments where the cost reduction benefit of maximum turbine scaling is most pronounced.

By Application: In 2026, Utility-Scale Power Generation to Hold the Largest Share

Based on application, the global floating wind turbine market is segmented into utility-scale power generation, offshore hydrogen production, hybrid renewable systems (wind and storage), and remote power supply for islands and offshore facilities. In 2026, the utility-scale power generation segment is expected to account for the largest share of the global floating wind turbine market. This dominance reflects the focus of the current commercial floating wind project pipeline on grid-connected power generation, driven by the offshore wind capacity targets of European, Asian, and North American governments that are stimulating the development of floating wind farms primarily as large-scale renewable electricity generation assets.

However, the offshore hydrogen production segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapidly expanding global green hydrogen program pipeline, the technical and economic advantages of combining floating wind generation with offshore electrolysis to produce hydrogen for export by pipeline rather than submarine power cable, and the strategic interest of oil and gas companies in developing offshore hydrogen production capabilities that leverage their existing offshore infrastructure expertise and hydrogen distribution relationships.

By Project Stage: In 2026, Pilot & Demonstration Projects to Hold the Largest Share

Based on project stage, the global floating wind turbine market is segmented into pilot and demonstration projects, pre-commercial projects, and commercial projects. In 2026, the pilot and demonstration projects segment is expected to account for the largest share of the global floating wind turbine market by installed capacity and value, reflecting the current market maturity stage where the majority of operational floating wind capacity globally consists of first-of-kind demonstration deployments including Hywind Scotland, Hywind Tampen, WindFloat Atlantic, Provence Grand Large, and the EDP Kincardine project that collectively represent the operational technology validation base of the industry.

However, the commercial projects segment is projected to register the highest CAGR during the forecast period. This growth is driven by the transition of the global floating wind pipeline from demonstration and pre-commercial stages toward full commercial project delivery, supported by the advancing government tender programs in the U.K., France, Norway, Japan, and South Korea that are awarding commercial floating wind development rights, the accumulating operational evidence from pioneer deployments that is enabling project finance underwriting of commercial-scale projects, and the supply chain investment being mobilized in response to the commercial project pipeline.

Floating Wind Turbine Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global floating wind turbine market is segmented into Europe, Asia-Pacific, North America, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global floating wind turbine market. The largest share of this region is mainly due to Europe's first-mover advantage in floating wind technology development and deployment, anchored by Equinor's Hywind Scotland project as the world's first commercial floating wind farm since 2017, the strong national floating wind development programs in the U.K., Norway, France, and Portugal, and the European offshore wind industry's accumulated technical expertise, established supply chain, and regulatory frameworks that provide a structural head start over other regions. The U.K.'s ScotWind leasing round awards representing the largest commercial floating wind capacity allocation globally to date, Norway's Utsira Nord development process, France's 250 MW commercial floating tender program, and Portugal's Atlantic offshore wind zone development collectively constitute the world's most advanced commercial floating wind pipeline.

However, the Asia-Pacific floating wind turbine market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by Japan's geographic imperative for floating wind given the deep-water bathymetry surrounding most of the country's coastline, the Japanese government's designated floating wind promotion zones and capacity targets representing several gigawatts of commercial pipeline, South Korea's 14.3 GW offshore wind target that incorporates substantial floating wind components in deep-water sites off the southwestern and eastern coasts, China's expansion of offshore wind development into deep-water East China Sea and South China Sea zones, and Taiwan's emerging floating wind program driven by the deep-water conditions off its eastern coast. The strong domestic turbine manufacturing capability of China's Mingyang Smart Energy and the technical collaboration programs between Korean shipbuilders and floating wind developers are creating Asia-Pacific supply chain capabilities that will support the region's commercial floating wind scale-up.

North America is establishing a substantial floating wind development pipeline concentrated on the U.S. West Coast states of California, Oregon, and Washington, where the deep-water continental shelf makes floating wind the only viable offshore wind technology, and on the U.S. East Coast deep-water lease areas in the Gulf of Maine. The Biden administration's 15 GW floating wind target for 2035 and the Bureau of Ocean Energy Management's floating wind commercial lease auctions for the Pacific Coast and Gulf of Maine are creating a large U.S. floating wind development pipeline. The strong involvement of oil and gas companies including Shell and TotalEnergies in U.S. floating wind lease holdings and development programs is providing capital and technical resources that are advancing the U.S. market toward commercial project delivery.

The global floating wind turbine market is characterized by a diverse competitive ecosystem encompassing turbine original equipment manufacturers, specialist floating platform technology developers, integrated energy companies providing both platform and project development expertise, and major renewable energy developers and utilities advancing the commercial project pipeline. Competition is currently focused on platform technology validation, project development capability, supply chain access, and technology cost reduction roadmaps rather than on commercial revenue scale.

Equinor leads the market in both installed capacity and commercial project pipeline, with operational projects at Hywind Scotland and Hywind Tampen and major development stakes across the U.K., U.S., and Norwegian floating wind markets. Siemens Gamesa, Vestas, and GE Vernova dominate turbine supply across all operational and planned floating wind projects. Principle Power's WindFloat semi-submersible platform has been deployed at the Kincardine and WindFloat Atlantic commercial projects. BW Ideol's concrete barge platform has been deployed at the Provence Grand Large demonstrator and forms the basis for multiple commercial project applications. Hexicon AB's TwinWind dual-turbine semi-submersible concept is advancing through development programs in South Korea and Sweden.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' technology platforms, project portfolios, geographic presence, and key strategic developments. Some of the key players operating in the global floating wind turbine market include Siemens Gamesa Renewable Energy (Spain), Vestas Wind Systems A/S (Denmark), GE Vernova (U.S.), Equinor ASA (Norway), Orsted A/S (Denmark), Principle Power Inc. (U.S.), BW Ideol (France), Aker Solutions ASA (Norway), Hexicon AB (Sweden), Mingyang Smart Energy (China), Iberdrola S.A. (Spain), Shell plc (U.K./Netherlands), TotalEnergies SE (France), EDF Renewables (France), and RWE Renewables (Germany), among others.

The global floating wind turbine market is expected to reach USD 58.4 billion by 2036 from an estimated USD 4.8 billion in 2026, at a CAGR of 28.3% during the forecast period 2026-2036.

In 2026, the semi-submersible segment is expected to hold the largest share of the global floating wind turbine market, driven by the semi-submersible design's versatility across water depths and the broadest commercial project pipeline concentration among platform technology categories.

The tension leg platform (TLP) segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by TLP technology's superior motion characteristics, smaller structural material requirements at moderate water depths, and growing commercial interest in TLP deployments in the 60 to 200 meter depth range.

In 2026, the 10-15 MW turbine capacity segment is expected to hold the largest share of the global floating wind turbine market, reflecting the deployment of current-generation commercial offshore wind turbines in this capacity class across the expanding floating wind project pipeline.

In 2026, the utility-scale power generation segment is expected to hold the largest share of the global floating wind turbine market, driven by the focus of the current commercial floating wind pipeline on grid-connected renewable electricity generation.

The growth of this market is primarily driven by the progressive depletion of accessible shallow-water fixed-bottom offshore wind sites in mature wind markets, the deep-water bathymetry of key markets including Japan, the U.S. Pacific Coast, and Atlantic-facing Europe that makes floating wind the only technically viable offshore wind option, and the escalating national offshore wind capacity targets that explicitly depend on floating wind technology to meet their long-term ambitions.

Key players are Siemens Gamesa Renewable Energy (Spain), Vestas Wind Systems A/S (Denmark), GE Vernova (U.S.), Equinor ASA (Norway), Orsted A/S (Denmark), Principle Power Inc. (U.S.), BW Ideol (France), Aker Solutions ASA (Norway), Hexicon AB (Sweden), Mingyang Smart Energy (China), Iberdrola S.A. (Spain), Shell plc (U.K./Netherlands), TotalEnergies SE (France), EDF Renewables (France), and RWE Renewables (Germany), among others.

Asia-Pacific is expected to register the highest growth rate in the global floating wind turbine market during the forecast period 2026-2036, driven by Japan's geographic imperative for floating wind, South Korea's large commercial floating wind pipeline, China's deep-water offshore wind expansion, and Taiwan's emerging floating wind program.

Published Date: Aug-2025

Published Date: Sep-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates