Resources

About Us

Europe Pet Food Protein Ingredients Market by Source (Animal Byproducts, Feed Grains, Soybean Byproducts, Novel Proteins), by Application (Dry Foods, Wet Foods, Veterinary Diets, Treats and Snacks) – Forecast to 2036

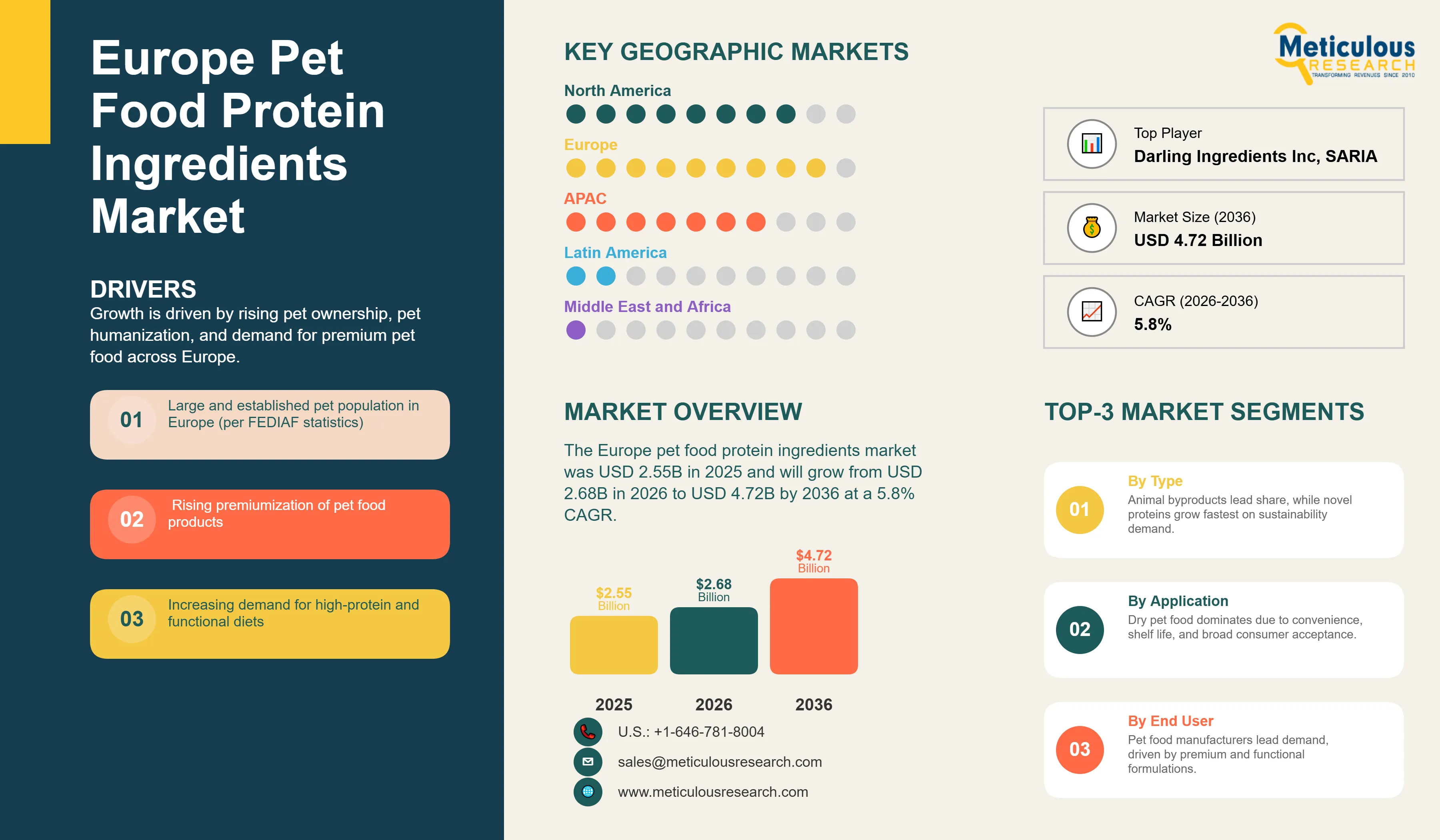

Report ID: MRFB - 104516 Pages: 150 Feb-2026 Formats*: PDF Category: Food and Beverages Delivery: 24 to 48 Hours Download Free Sample ReportThe Europe pet food protein ingredients market was valued at approximately USD 2.55 billion in 2025. This market is expected to reach approximately USD 4.72 billion by 2036 from USD 2.68 billion in 2026, growing at a CAGR of 5.8% from 2026 to 2036. The growth of this market is primarily driven by the increasing pet population in Europe, the growing trend of pet humanization, and the rising demand for premium and specialized pet food products. According to FEDIAF (the European Pet Food Industry Federation), Europe is home to approximately 299 million companion animals, with nearly 139 million households (around 49% of all households) owning at least one pet. This large pet population creates significant demand for pet food and its protein ingredients.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The Europe pet food protein ingredients market includes a wide range of protein sources used in the formulation of pet food products. These ingredients are essential for providing the necessary amino acids for pets to thrive. The market is characterized by a growing demand for high-quality, sustainable, and functional protein ingredients, driven by the increasing awareness among pet owners about the importance of pet nutrition.

The trend of pet humanization, where pets are treated as family members, has led to a significant shift in consumer purchasing behavior. Pet owners are increasingly seeking out pet food products that mirror their own dietary preferences, such as natural, organic, and grain-free options. This has created a demand for premium pet food products with high-quality protein ingredients. For example, brands like Lily's Kitchen and Orijen have gained popularity by offering pet food with high meat content and natural ingredients.

Regulatory bodies, such as the European Food Safety Authority (EFSA) and FEDIAF, play a crucial role in ensuring the safety and quality of pet food ingredients. FEDIAF provides nutritional guidelines for complete and complementary pet food for cats and dogs, which are widely adopted by the European pet food industry. These guidelines help ensure that pet food products meet the nutritional needs of pets and are safe for consumption.

What are the Key Trends in the Europe Pet Food Protein Ingredients Market?

Rising Demand for Novel and Alternative Protein Sources

There is a growing interest in novel and alternative protein sources in the European pet food market. These include insect protein, single-cell protein, and plant-based proteins from sources like peas, lentils, and algae. This trend is driven by concerns about the sustainability of traditional animal-based proteins, as well as the demand for hypoallergenic and functional pet food products. For instance, Yora Pet Foods offers a range of dog food products made from insect protein.

Increasing Focus on Sustainable and Ethically Sourced Ingredients

Sustainability and ethical sourcing are becoming increasingly important factors in the European pet food market. Pet owners are more conscious of the environmental and social impact of the products they buy, and this is reflected in their purchasing decisions. This has led to a growing demand for pet food with ingredients that are sustainably sourced, such as fish from certified sustainable fisheries or meat from animals raised in high-welfare systems. Brands like Beco Pets are known for their focus on sustainability and ethical sourcing.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 4.72 Billion |

|

Market Size in 2026 |

USD 2.68 Billion |

|

Market Size in 2025 |

USD 2.55 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 5.8% |

|

Dominating Source |

Animal Byproducts |

|

Fastest Growing Source |

Novel Proteins |

|

Largest Application Segment |

Dry Pet Foods |

|

Dominating Country |

Germany |

|

Fastest Growing Countries |

France, Spain |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Drivers: Increasing Pet Ownership and Humanization Trend

The growing pet population across Europe, coupled with the continuing trend of pet humanization, represents a major driver of the European pet food protein ingredients market. According to FEDIAF, approximately 139 million European households, around 49% of all households, own at least one companion animal. This large and stable pet ownership base underpins sustained demand for pet nutrition products.

As pets are increasingly regarded as family members, owners are placing greater emphasis on health, longevity, and overall well-being, mirroring human dietary preferences. This shift is translating into higher spending on premium, high-protein, and functionally enhanced pet food formulations. Consequently, demand is rising for quality protein ingredients, including animal-based proteins, specialty plant proteins, and emerging alternative sources, which support digestibility, muscle maintenance, and targeted health benefits. This trend directly strengthens the growth outlook for protein ingredient suppliers across the region.

Opportunity: Growing Demand for Specialized and Functional Pet Food

The growing demand for specialized and functional pet food products presents a significant opportunity for the market. Pet owners are increasingly seeking out products that address specific health needs, such as weight management, joint health, and digestive support. This has created a demand for functional protein ingredients that offer specific health benefits, such as hydrolyzed proteins for hypoallergenic diets and proteins with high digestibility for sensitive stomachs.

Why Do Animal Byproducts Dominate the Market?

Based on source, the animal byproducts segment is expected to account for the largest share of the market, in 2026. Animal byproducts, such as meat and bone meal, poultry byproduct meal, and fish meal, are traditional and cost-effective sources of protein for pet food. They are widely available and provide a good balance of essential amino acids. However, the demand for novel and alternative protein sources is growing, which may impact the market share of this segment in the long term.

How Does the Dry Pet Foods Segment Lead the Market?

The dry pet foods segment is expected to account for the largest share of the market by application, in 2026. Dry pet food is convenient, has a long shelf life, and is generally more affordable than wet pet food. It is also beneficial for dental health, as the crunchy texture helps to clean teeth and reduce tartar buildup. The wide availability and variety of dry pet food products also contribute to the growth of this segment.

How is Germany Maintaining Its Leadership?

Germany is projected to account for the largest share of the Europe pet food protein ingredients market during the forecast period. This is supported by a large and well-established pet population, coupled with comparatively high per capita expenditure on pet care and nutrition. Germany also benefits from a mature and technologically advanced pet food manufacturing industry, characterized by strong supply chains, high-quality production standards, and a focus on premium and functional formulations.

Consumer preferences in Germany increasingly favor high-protein, natural, and sustainably sourced ingredients, which drives demand for specialized protein inputs, including animal-derived proteins and emerging alternative sources. Additionally, the presence of leading ingredient suppliers and processors, along with stringent quality and safety regulations, further strengthens its position as a key hub for pet food protein ingredient production and consumption in Europe.

Which Countries Are Experiencing Rapid Growth?

France and Spain are expected to register some of the fastest growth rates in the Europe pet food protein ingredients market. This growth is driven by rising pet ownership levels, increasing disposable incomes, and a growing trend toward pet humanization, which encourages higher spending on nutritionally balanced and premium pet food products.

In both countries, increasing awareness among pet owners regarding the importance of protein quality, digestibility, and functional benefits is supporting the shift toward higher-value ingredients. Expanding retail distribution networks, growth of specialty pet food brands, and the rising availability of premium and veterinary diet products are also contributing to stronger demand for advanced protein ingredients in these markets.

The Europe pet food protein ingredients market is moderately consolidated, with competition focused on raw material sourcing capabilities, processing technologies, and the ability to supply high-quality, traceable protein ingredients. Key companies profiled in this report include Darling Ingredients Inc., SARIA SE & Co. KG, BHJ A/S (a part of the Lauridsen Group), and Advanced Proteins Ltd, among others. These players focus on expanding their processing capacities, enhancing product portfolios with value-added protein ingredients, and strengthening sustainable sourcing practices to maintain their competitive positions.

The Europe pet food protein ingredients market is expected to grow from USD 2.68 billion in 2026 to USD 4.72 billion by 2036.

The Europe pet food protein ingredients market is expected to grow at a CAGR of 5.8% from 2026 to 2036.

The key players operating in the Europe pet food protein ingredients market include Darling Ingredients Inc., SARIA SE & Co. KG, BHJ A/S (a part of the Lauridsen Group), and Advanced Proteins Ltd.

The main factors include the increasing pet population in Europe, the growing trend of pet humanization, and the rising demand for premium and specialized pet food products.

Germany will lead the Europe pet food protein ingredients market during the forecast period 2026 to 2036, while France and Spain are expected to witness the fastest growth.

Published Date: Jan-2025

Published Date: Aug-2024

Published Date: Mar-2024

Published Date: Jan-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates