Resources

About Us

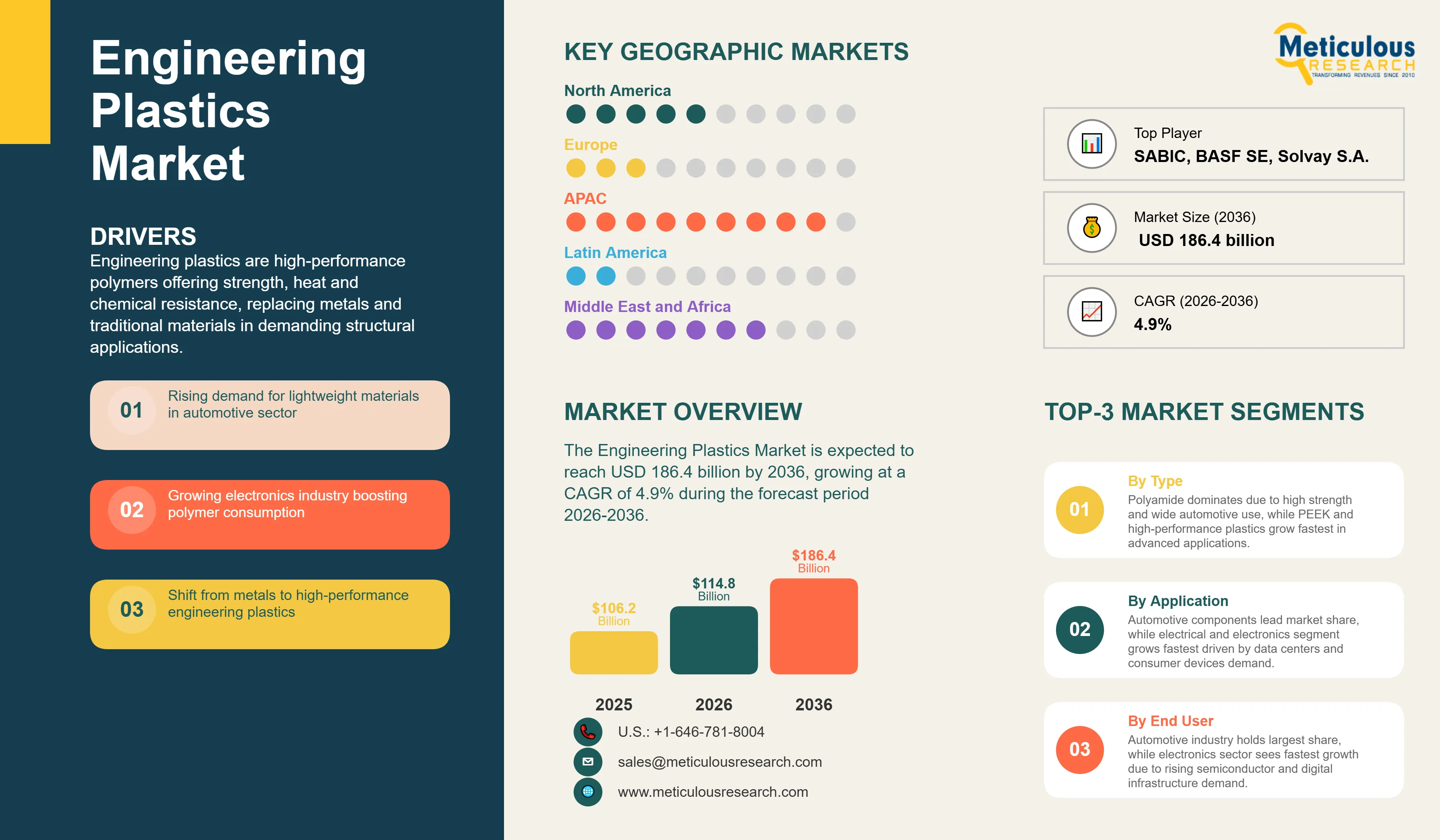

The Engineering Plastics Market was valued at USD 106.2 billion in 2025. This market is expected to reach USD 186.4 billion by 2036 from an estimated USD 114.8 billion in 2026, growing at a CAGR of 4.9% during the forecast period 2026-2036. Engineering plastics are high-performance polymer materials that deliver mechanical strength, thermal resistance, chemical stability, and dimensional precision that commodity plastics cannot provide, making them the materials of choice wherever performance matters more than cost in automotive, electronics, medical, and industrial applications globally

Market Overview and Insights

Click here to: Get Free Sample Pages of this Report

Engineering plastics are a family of polymer materials that sit above commodity plastics such as polyethylene and polypropylene in the performance hierarchy, offering superior mechanical properties, heat resistance, dimensional stability, and chemical resistance that allow them to replace metals, ceramics, and other traditional materials in demanding structural and functional applications. A glass-fiber-reinforced polyamide 66 gear can replace a machined aluminum gear in an automotive transmission, cutting weight by over 50% while maintaining comparable strength and wear resistance. A polycarbonate housing for a medical device delivers dimensional precision, sterilization resistance, and transparency that no metal or ceramic can match at comparable cost. A PEEK component in an aerospace application retains its mechanical properties at 250 degrees Celsius and resists aircraft fuels, hydraulic fluids, and lubricants while weighing a fraction of the metal part it replaces.

The market is growing because the industries that depend on engineering plastics are expanding and because the performance requirements they place on materials are intensifying. According to the IEA's Global EV Outlook 2025, global electric vehicle sales reached approximately 17 million units in 2024, continuing to grow strongly. Each EV uses more engineering plastics per vehicle than a conventional ICE vehicle because the battery housing, thermal management components, high-voltage connector systems, and lightweight structural elements that define EV architecture all require engineering plastic grades with very specific electrical, thermal, and mechanical properties. According to OICA’s latest reported data, global motor vehicle production was about 92.7 million units in 2024 and increased to 96.4 million in 2025, supporting a very large automotive materials demand base, including engineering plastics and EV-related plastics.

Two opportunities are particularly commercially significant for the forecast period. The electric vehicle transition is creating accelerating demand for flame-retardant polyamide grades for battery module housings, polycarbonate-ABS blends for charge port bezels and interior trim, and PBT and PET compounds with excellent electrical insulation for connector and wiring systems. In parallel, the additive manufacturing sector is progressively qualifying engineering plastic powders and filaments for production-grade parts in medical, aerospace, and industrial applications, with the global 3D printing materials market for engineering polymers growing at above-average rates. According to Wohlers Report 2025, the global additive manufacturing industry grew 9.1% in 2024 to USD 21.9 billion, with materials continuing to be a meaningful growth area and high-performance polymers remaining important for industrial applications

|

Parameters |

Details |

|

Market Size by 2036 |

USD 186.4 Billion |

|

Market Size in 2026 |

USD 114.8 Billion |

|

Market Size in 2025 |

USD 106.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 4.9% |

|

Dominating Polymer Type |

Polyamide (PA/Nylon) |

|

Fastest Growing Polymer Type |

PEEK and High-Performance Plastics |

|

Dominating Application |

Automotive Components |

|

Fastest Growing Application |

Electrical and Electronics |

|

Dominating End-Use Industry |

Automotive |

|

Fastest Growing End-Use Industry |

Electrical & Electronics |

|

Dominating Processing Method |

Injection Molding |

|

Fastest Growing Processing Method |

3D Printing (Additive Manufacturing) |

|

Dominating Reinforcement Type |

Glass Fiber Reinforced |

|

Fastest Growing Reinforcement Type |

Carbon Fiber Reinforced |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

EV Architecture Driving a New Specification Cycle for Engineering Plastics

The transition from internal combustion engine vehicles to electric vehicles is fundamentally reshaping which engineering plastic grades are in demand, as EVs require materials with specific electrical, thermal, and flame-retardant properties that ICE vehicle applications do not. Battery module housings must be made from materials that are both lightweight and flame-retardant to meet battery safety standards. Connector systems for high-voltage power distribution within the battery pack and the drive system require plastics with very high electrical tracking resistance, dimensional stability under thermal cycling, and resistance to the chemical environment of battery electrolytes. According to BASF's 2025 Automotive Insights report, polyamide compounds specifically formulated for e-mobility applications are among the fastest-growing segments in its engineering plastics portfolio, with EV-specific grades growing at above-average rates as automakers qualify new materials for their electric vehicle platforms.

The under-the-hood environment in an EV is different from an ICE vehicle because the heat sources and thermal gradients are different, and the materials that worked in ICE engine compartments are not always optimal for the EV powertrain environment. High-temperature polyamides, polyphthalamide (PPA), and PEEK-based compounds are seeing growing demand for EV thermal management system components, cooling system parts, and power electronics housings where temperatures and chemical exposures exceed what PA66 can reliably manage. Covestro reported in its 2025 interim results that its EV-relevant polycarbonate compounding business was growing at a premium to its overall automotive performance, reflecting this EV specification cycle generating above-market demand for specific high-performance grades

Sustainability Pressure Accelerating Bio-Based and Recycled Engineering Plastics

The engineering plastics industry is under growing pressure from major automotive and electronics customers to provide materials with lower carbon footprints, higher recycled content, and end-of-life recyclability, reflecting the corporate sustainability commitments these industries have made under EU and international regulatory frameworks. BASF's Ultramid RE polyamide, produced from recycled raw materials through a mass balance approach, and Lanxess's bio-based polyamide products based on castor oil-derived sebacic acid are commercial examples of the industry's response to these sustainability requirements. According to BASF's 2025 Sustainability Report, demand for its chemically recycled and bio-attributed engineering plastic products grew at double-digit rates in 2024, driven primarily by automotive and electronics customers with near-term recycled content targets to meet.

The EU's End-of-Life Vehicles Regulation, which in its 2025 draft form proposes significantly higher recycled plastic content requirements for new vehicle manufacturing than the current directive mandates, is a major regulatory driver of engineering plastics sustainability development. If adopted in its proposed form, the regulation would require automakers to incorporate specified percentages of recycled plastic in new vehicles by defined dates, creating commercially mandatory demand for automotive-grade recycled and recyclable engineering plastic compounds that meet performance requirements. SABIC's LNP ELCRIN iQ compounds incorporating recycled content, and Envalior's sustainable polyamide grades from the former DSM Engineering Materials business, represent the commercial response to this anticipated regulatory requirement

PEEK and High-Performance Polymers Expanding Beyond Aerospace into Medical and Electronics

Polyether ether ketone and other high-performance engineering polymers including PPS, PEI, and high-temperature polyamides have historically been used primarily in aerospace and specialty industrial applications where their exceptional performance at elevated temperatures and in aggressive chemical environments justified their high cost. A trend that has been building through 2024 and into 2025 is the expansion of PEEK and similar materials into medical device and electronics applications as the performance requirements of these sectors intensify and as manufacturing scale drives incremental cost reduction. According to Victrex, the world's largest PEEK manufacturer, its medical segment grew at above-average rates in 2024 as PEEK's combination of biocompatibility, sterilization resistance, and radiolucency, which means it does not interfere with X-ray imaging unlike metal implants, makes it increasingly valuable in spinal, dental, and orthopedic implant applications.

In the electronics sector, PEEK and polyphenylene sulfide compounds are finding growing applications in semiconductor manufacturing equipment, printed circuit board handling systems, and advanced packaging components where dimensional stability at processing temperatures and resistance to the aggressive cleaning chemicals used in semiconductor fabrication are essential. According to Solvay's 2025 first quarter results commentary, its specialty polymers division, which includes PEEK-equivalent KetaSpire and other high-performance engineering polymers, was seeing strong demand from semiconductor equipment customers as chipmakers invest in advanced packaging and heterogeneous integration manufacturing capacity

Increasing Demand for Lightweight Materials in Automotive and Aerospace

Lightweighting through engineering plastic substitution for metal parts remains one of the most commercially active drivers of engineering plastics demand, amplified by the EV transition that creates a particularly strong incentive for every kilogram of weight reduction because reduced vehicle mass directly extends battery range. According to the IEA's Global EV Outlook 2025, global EV sales reached approximately 17 million units in 2024, and the automotive engineering plastics demand from this growing EV fleet adds a fast-growing incremental demand layer above the established ICE vehicle engineering plastics base. OICA's 2025 data showing global vehicle production at approximately 96 million units in 2025 confirms the sustained scale of baseline automotive engineering plastics demand. In aerospace, the ongoing fleet renewal programs of Boeing and Airbus with their composite and high-performance polymer-intensive airframe designs continue to drive demand for PEEK, PEI, and specialty engineering polymers in structural and functional aircraft components

Growth in Electrical & Electronics Industry

The electronics industry is a major and growing consumer of engineering plastics, particularly polycarbonate, ABS, PBT, and high-performance polyamides, across applications from consumer device housings to connector systems for telecommunications infrastructure. According to the Semiconductor Industry Association's 2025 Global Semiconductor Sales report, global semiconductor sales grew to approximately USD 630 billion in 2024, representing a major recovery and growth cycle that is driving investment in electronics manufacturing equipment, printed circuit boards, and electronic assemblies that each consume engineering plastics. The expansion of data center infrastructure to support AI workloads, with the major hyperscale operators continuing their unprecedented capital expenditure in 2025, is driving growing demand for polycarbonate and engineering polymer housings, frames, and structural components in server and networking equipment

Growth in Electric Vehicles (EVs) and Battery Systems

The EV transition is creating new engineering plastics application categories that did not exist at scale just five years ago: battery module and pack housings requiring flame-retardant polyamide or polycarbonate compounds; thermal interface materials and cooling system components requiring chemically resistant engineering polymers; high-voltage connector and busbar insulation systems requiring tracking-resistant PBT, PPS, and high-temperature polyamide grades; and structural battery enclosures requiring engineering plastic composites with very high stiffness-to-weight ratios. According to Covestro's 2025 interim financial results, its EV-relevant polycarbonate and polyurethane businesses were growing at rates significantly above its overall average, directly reflecting the EV specification cycle. BASF's 2025 Automotive Insights publication specifically highlighted that polyamide demand for EV applications including battery and e-drive components was growing at above-average rates across its portfolio

Expansion in 3D Printing Applications

The additive manufacturing market for engineering plastic materials is growing rapidly as qualification of printed engineering polymer parts for functional end-use applications extends from prototyping into serial production in medical, aerospace, and industrial sectors. PEEK, high-temperature nylon (PA12, PA11), and carbon fiber-reinforced engineering plastic filaments and powders are enabling production-grade 3D-printed components that were impossible or uneconomical to produce by conventional molding for low to medium volume applications. According to Wohlers Associates' 2025 Additive Manufacturing State of the Industry report, the production parts segment of the additive manufacturing market grew at approximately 9% in 2024, with functional polymer materials representing a significant share of this growth. BASF Forward AM, Evonik's Vestosint specialty PA12 powders, and Solvay's KetaSpire PEEK filaments are all commercial products addressing this growing application channel, and the progressive qualification of 3D-printed engineering polymer parts in medical implants and aerospace components is opening significant new market segments

Based on polymer type, the global engineering plastics market is segmented into polyamide (PA6, PA66, and other polyamides), polycarbonate, polyoxymethylene (acetal), ABS, PBT, PET, fluoropolymers (PTFE and PVDF), PEEK, and other engineering plastics. In 2026, the polyamide segment is expected to account for the largest share of the global engineering plastics market. Polyamide is the most broadly and heavily used engineering plastic globally, with PA6 and PA66 grades consumed in very large volumes across automotive under-the-hood components, gear systems, bearing cages, electrical connectors, and industrial components. The automotive sector's strong adoption of glass-fiber-reinforced PA66 for engine covers, air intake manifolds, cooling system components, and structural brackets makes polyamide the dominant engineering plastic by volume across the industry's largest end-use sector. According to BASF's 2025 portfolio communications, polyamide remains the highest-volume engineering plastic in its Ultramid range, and Ascend Performance Materials, one of the world's largest integrated PA66 producers, has invested in capacity expansion to serve growing EV and automotive demand.

However, the PEEK and high-performance plastics segment is projected to register the highest CAGR during the forecast period. The expansion of PEEK and related high-performance polymers into medical device, semiconductor equipment, and EV powertrain applications is growing faster than the broader engineering plastics market. According to Victrex's 2025 half-year results, its medical and electronics segments grew at above-average rates, driven by PEEK implant adoption and semiconductor equipment applications

By Application: In 2026, Automotive Components to Hold the Largest Share

Based on application, the global engineering plastics market is segmented into automotive components (interior, exterior, and under-the-hood), electrical and electronics, industrial and machinery, medical and healthcare devices, packaging, aerospace and defense, and other applications. In 2026, the automotive components segment is expected to account for the largest share of the global engineering plastics market. The automotive industry is by far the largest single end-use application for engineering plastics globally, consuming polyamide, polycarbonate, PBT, ABS, POM, and other engineering polymers across thousands of individual part applications in every vehicle. According to OICA's 2025 data, global motor vehicle production reached approximately 96 million units in 2025, and at an estimated average of 15 to 20 kilograms of engineering plastics per vehicle across the full range from economy to premium models, this represents several million tonnes of annual consumption.

However, the electrical and electronics segment is projected to register the highest CAGR during the forecast period. The growth of data center infrastructure, AI computing equipment, 5G telecommunications, consumer electronics, and EV charging stations is driving above-average growth in engineering plastics demand for electronic component housings, connector systems, and thermal management structures. According to the Semiconductor Industry Association's 2025 report, the USD 630 billion global semiconductor market in 2024 underpins a large and growing electronics manufacturing base that requires engineering plastic materials throughout the supply chain

By Processing Method: In 2026, Injection Molding to Hold the Largest Share

Based on processing method, the global engineering plastics market is segmented into injection molding, extrusion, blow molding, compression molding, and 3D printing. In 2026, the injection molding segment is expected to account for the largest share of the global engineering plastics market. Injection molding is the dominant processing method for engineering plastics by volume, enabling the high-volume, high-precision production of complex three-dimensional engineering plastic parts that is the standard manufacturing approach across automotive, electronics, and consumer goods industries. The very large installed base of injection molding machines globally and the economics of high-volume precision part production make this the most widely used processing method for engineering polymers.

However, the 3D printing segment is projected to register the highest CAGR during the forecast period. The growing qualification of engineering polymer additive manufacturing for production-grade end-use parts in medical, aerospace, and industrial applications is driving strong growth in engineering plastic filaments and powders for 3D printing from a currently small but rapidly growing base

Engineering Plastics Market by Region: Asia-Pacific Leading by Share, Middle East and Africa by Growth

Based on geography, the global engineering plastics market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa. In 2026, Asia-Pacific is expected to account for the largest share of the global engineering plastics market. The region's dominance reflects China's position as the world's largest vehicle producing country, the world's largest electronics manufacturing base, and the home of the world's largest engineering plastics consumption. According to OICA's 2025 preliminary data, China produced approximately 31 million vehicles in 2024, sustaining its position as the world's single largest automotive engineering plastics market. China is also the world's largest EV market, with the China Passenger Car Association reporting over 12 million new energy vehicle sales in 2024, generating very large and growing demand for EV-specific engineering plastic grades. Japan, South Korea, and Taiwan are home to leading electronics and semiconductor manufacturers including Samsung, SK Hynix, TSMC, Sony, and Toyota that are major engineering plastics consumers, and India's rapidly growing automotive and electronics industries are adding significant incremental demand as Indian vehicle production and domestic electronics manufacturing scale up. India remains one of the world’s major automotive manufacturing bases, with SIAM reporting strong production volumes in 2025 and the sector continuing to support growing demand for automotive engineering plastics.

However, the Middle East and Africa region is expected to grow at the fastest CAGR during the forecast period. The rapid industrialization and infrastructure development underway across the Gulf Cooperation Council states under national Vision programs, combined with the development of downstream plastics processing industries in Saudi Arabia and the UAE that are supported by petrochemical feedstock advantages, is generating above-average engineering plastics demand growth. Saudi Arabia's ambitious plans to develop domestic manufacturing industries and automotive assembly operations under Vision 2030 are creating new engineering plastics consumption alongside the established construction, oil and gas, and consumer goods sectors. Sub-Saharan Africa and North Africa are experiencing growing industrialization and domestic manufacturing investment that is progressively expanding engineering plastics consumption from a relatively low current base.

North America is a large and technologically sophisticated engineering plastics market, with the United States being a major consumer across automotive, medical device, electronics, and industrial applications. The U.S. automotive sector's production of approximately 10.4 million vehicles in 2024 according to OICA 2025 data sustains large polyamide, polycarbonate, and PBT consumption. The strong U.S. medical device industry, supported by the world's largest healthcare spending base, is a premium consumer of PEEK, polycarbonate, and medical-grade engineering polymers. Europe is characterized by very high engineering plastics quality standards, strong sustainability regulation driving bio-based and recycled content demand, and world-leading companies including BASF, Covestro, Lanxess, and Solvay that both manufacture and consume engineering plastics at very large scale. Germany's automotive industry, which despite structural challenges remains the largest single engineering plastics consuming industry in Europe, sustains the majority of European polyamide and technical polymer demand

The engineering plastics market is dominated by large diversified chemical companies with broad polymer portfolios serving multiple end-use industries, alongside specialist high-performance polymer producers focused on specific material families or application segments. Competition is based on polymer performance specifications, application development support and technical service capabilities, breadth of formulation range across filled and unfilled grades, sustainability and recycled content offering, and pricing competitiveness in commodity-adjacent grades

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, geographic presence, sustainability initiatives, and recent strategic developments. Some of the key players operating in the global engineering plastics market include BASF SE (Germany), SABIC (Saudi Arabia), Covestro AG (Germany), DuPont de Nemours Inc. (U.S.), DSM Engineering Materials/Envalior (Netherlands/Germany), Celanese Corporation (U.S.), Lanxess AG (Germany), Mitsubishi Chemical Group Corporation (Japan), Solvay S.A. (Belgium), Arkema S.A. (France), Toray Industries Inc. (Japan), LG Chem Ltd. (South Korea), Teijin Limited (Japan), RTP Company (U.S.), and Ascend Performance Materials (U.S.), among others

The global engineering plastics market is expected to reach USD 186.4 billion by 2036 from an estimated USD 114.8 billion in 2026, at a CAGR of 4.9% during the forecast period 2026-2036.

In 2026, the polyamide (nylon) segment is expected to hold the largest share of the global engineering plastics market. BASF's Ultramid polyamide range remains the highest-volume engineering plastic in its portfolio, and Ascend Performance Materials has been investing in PA66 capacity expansion to meet growing EV and automotive demand per the company's 2025 communications.

The PEEK and high-performance plastics segment is projected to register the highest CAGR during the forecast period. According to Victrex's 2025 half-year results, its medical and electronics segments grew at above-average rates, with PEEK implant adoption and semiconductor equipment applications driving growth well above the broader engineering plastics market average.

According to BASF's 2025 Automotive Insights report, polyamide compounds for EV applications including battery and e-drive components are growing at above-average rates. Covestro's 2025 interim results confirmed that its EV-relevant polycarbonate business was growing at a premium to its overall automotive performance. The IEA's Global EV Outlook 2025 documenting approximately 17 million EV sales in 2024 indicates that EV-specific engineering plastics demand is now a significant and growing market layer above the established ICE vehicle base.

The market is primarily driven by the growing automotive engineering plastics base supported by OICA's 2025 data showing 96 million vehicles produced in 2024, amplified by the EV transition creating new demand for flame-retardant, electrically insulating, and thermally resistant grades, alongside the above-average growth of the electronics sector with the Semiconductor Industry Association reporting USD 630 billion in 2024 semiconductor revenues per its 2025 report

Key players are BASF SE (Germany), SABIC (Saudi Arabia), Covestro AG (Germany), DuPont de Nemours Inc. (U.S.), DSM Engineering Materials/Envalior (Netherlands/Germany), Celanese Corporation (U.S.), Lanxess AG (Germany), Mitsubishi Chemical Group Corporation (Japan), Solvay S.A. (Belgium), Arkema S.A. (France), Toray Industries Inc. (Japan), LG Chem Ltd. (South Korea), Teijin Limited (Japan), RTP Company (U.S.), and Ascend Performance Materials (U.S.), among others.

The Middle East and Africa region is expected to register the highest growth rate in the global engineering plastics market during the forecast period 2026-2036. The development of domestic manufacturing and processing industries in Saudi Arabia and the UAE under Vision 2030 programs, combined with growing industrialization across Africa, is creating above-average demand growth from a currently lower base than mature markets.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Demand for Lightweight Materials in Automotive and Aerospace

4.2.1.2 Growth in Electrical & Electronics Industry

4.2.1.3 Replacement of Metals with High-Performance Plastics

4.2.1.4 Rising Demand in Healthcare and Medical Devices

4.2.2 Restraints

4.2.2.1 High Cost Compared to Commodity Plastics

4.2.2.2 Recycling and Environmental Concerns

4.2.2.3 Volatility in Petrochemical Feedstock Prices

4.2.3 Opportunities

4.2.3.1 Development of Bio-Based and Recyclable Engineering Plastics

4.2.3.2 Growth in Electric Vehicles (EVs) and Battery Systems

4.2.3.3 Expansion in 3D Printing Applications

4.2.3.4 Increasing Use in Renewable Energy Systems

4.2.4 Challenges

4.2.4.1 Processing Complexity

4.2.4.2 Performance Limitations Under Extreme Conditions4.3 Technology and Material Landscape

4.3.1 Polymer Compounding and Blending

4.3.2 Reinforced and Fiber-Filled Plastics

4.3.3 High-Performance Engineering Plastics

4.3.4 Additive Manufacturing Materials

4.3.5 Recycling and Circular Polymer Technologies

4.4 Engineering Plastics Value Chain

4.4.1 Raw Material Suppliers (Petrochemicals)

4.4.2 Polymer Manufacturers

4.4.3 Compounders and Processors

4.4.4 Distributors

4.4.5 End Users

4.5 Value Chain Analysis

4.5.1 Feedstock Production

4.5.2 Polymerization and Compounding

4.5.3 Processing and Fabrication

4.5.4 Distribution and Supply

4.5.5 End Use and Recycling

4.6 Regulatory and Standards Landscape

4.6.1 Environmental Regulations (REACH, RoHS)

4.6.2 Product Safety Standards

4.6.3 Recycling and Sustainability Regulations

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Growth in Sustainable Polymers

4.8.2 Expansion of EV and Electronics Markets

4.8.3 Mergers and Acquisitions

4.9 Cost and Pricing Analysis

4.9.1 Cost by Polymer Type

4.9.2 Processing Costs

4.9.3 Price Trends by End-Use Industry

5. Engineering Plastics Market, by Polymer Type

5.1 Introduction

5.2 Polyamide (PA/Nylon)

5.2.1 PA6

5.2.2 PA66

5.2.3 Other Polyamides

5.3 Polycarbonate (PC)

5.4 Polyoxymethylene (POM/Acetal)

5.5 Acrylonitrile Butadiene Styrene (ABS)

5.6 Polybutylene Terephthalate (PBT)

5.7 Polyethylene Terephthalate (PET)

5.8 Fluoropolymers

5.8.1 PTFE

5.8.2 PVDF

5.9 Polyether Ether Ketone (PEEK)

5.10 Other Engineering Plastics

6. Engineering Plastics Market, by Application

6.1 Introduction

6.2 Automotive Components

6.2.1 Interior Components

6.2.2 Exterior Components

6.2.3 Under-the-Hood Applications

6.3 Electrical and Electronics

6.3.1 Connectors and Switches

6.3.2 Consumer Electronics Housings

6.4 Industrial and Machinery

6.5 Medical and Healthcare Devices

6.6 Packaging

6.7 Aerospace and Defense

6.8 Other Applications

7. Engineering Plastics Market, by End-Use Industry

7.1 Introduction

7.2 Automotive

7.3 Electrical & Electronics

7.4 Industrial Machinery

7.5 Healthcare

7.6 Packaging

7.7 Aerospace & Defense

7.8 Consumer Goods

7.9 Others

8. Engineering Plastics Market, by Processing Method

8.1 Introduction

8.2 Injection Molding

8.3 Extrusion

8.4 Blow Molding

8.5 Compression Molding

8.6 3D Printing (Additive Manufacturing)

9. Engineering Plastics Market, by Reinforcement Type

9.1 Introduction

9.2 Glass Fiber Reinforced

9.3 Carbon Fiber Reinforced

9.4 Mineral Filled

9.5 Unreinforced

10. Engineering Plastics Market, by Geography

10.1 Introduction

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 Germany

10.3.2 U.K.

10.3.3 France

10.3.4 Italy

10.3.5 Spain

10.3.6 Netherlands

10.3.7 Sweden

10.3.8 Switzerland

10.3.9 Rest of Europe

10.4 Asia-Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 South Korea

10.4.5 Taiwan

10.4.6 Australia

10.4.7 Indonesia

10.4.8 Thailand

10.4.9 Rest of Asia-Pacific

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Argentina

10.5.4 Chile

10.5.5 Colombia

10.5.6 Rest of Latin America

10.6 Middle East & Africa

10.6.1 Saudi Arabia

10.6.2 UAE

10.6.3 South Africa

10.6.4 Turkey

10.6.5 Egypt

10.6.6 Rest of Middle East & Africa

11. Competitive Landscape

11.1 Overview

11.2 Key Growth Strategies

11.3 Competitive Benchmarking

11.4 Competitive Dashboard

11.4.1 Industry Leaders

11.4.2 Market Differentiators

11.4.3 Vanguards

11.4.4 Emerging Companies

11.5 Market Ranking/Positioning Analysis of Key Players, 2025

12. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

12.1 BASF SE

12.2 SABIC

12.3 Covestro AG

12.4 DuPont de Nemours, Inc.

12.5 DSM Engineering Materials (Envalior)

12.6 Celanese Corporation

12.7 Lanxess AG

12.8 Mitsubishi Chemical Group Corporation

12.9 Solvay S.A.

12.10 Arkema S.A.

12.11 Toray Industries, Inc.

12.12 LG Chem Ltd.

12.13 Teijin Limited

12.14 RTP Company

12.15 Ascend Performance Materials

13. Appendix

13.1 Additional Customization

13.2 Related Reports

Published Date: Sep-2024

Subscribe to get the latest industry updates