Resources

About Us

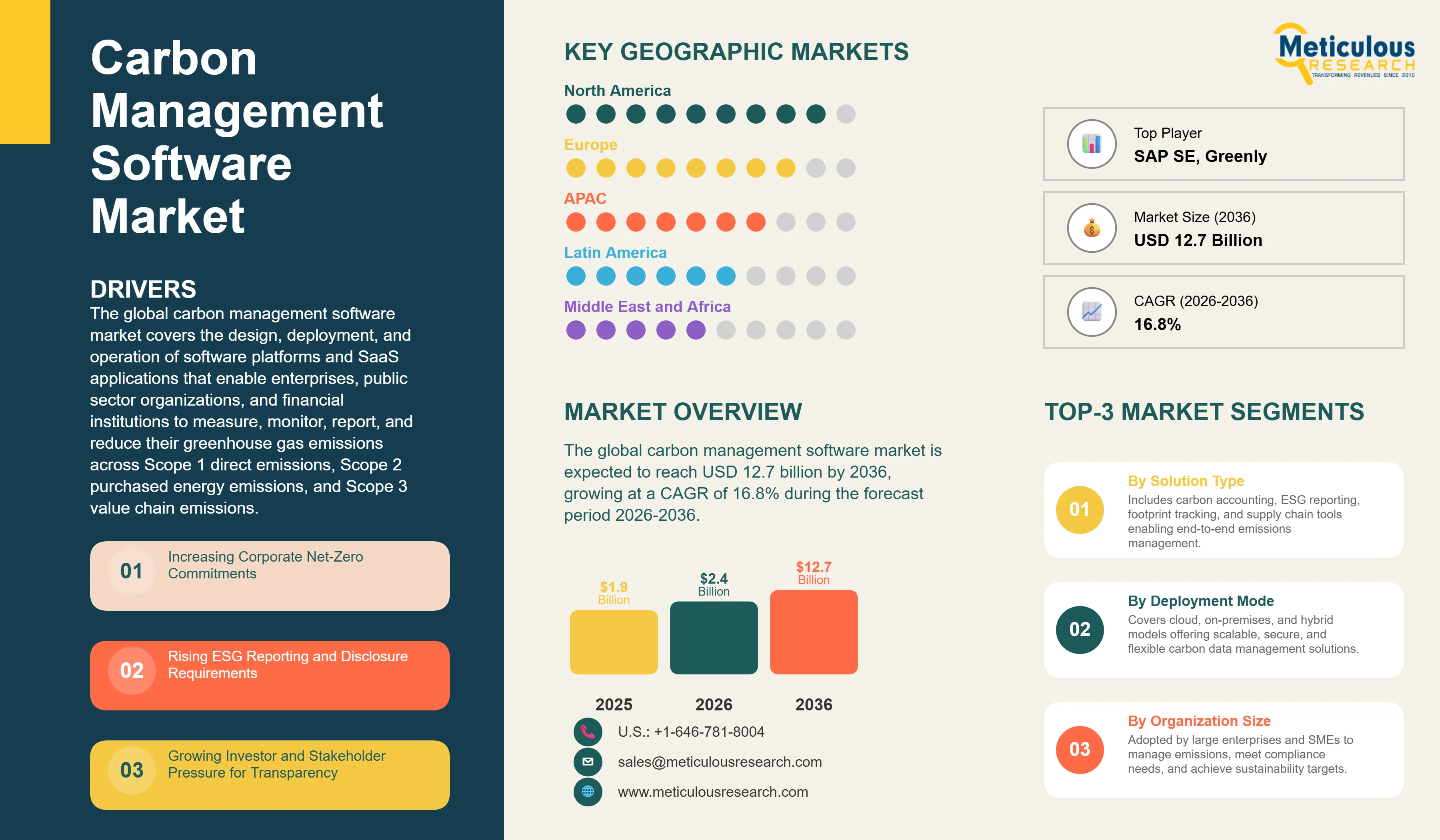

The global carbon management software market was valued at USD 1.9 billion in 2025. This market is expected to reach USD 12.7 billion by 2036 from an estimated USD 2.4 billion in 2026, growing at a CAGR of 16.8% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global carbon management software market covers the design, deployment, and operation of software platforms and SaaS applications that enable enterprises, public sector organizations, and financial institutions to measure, monitor, report, and reduce their greenhouse gas emissions across Scope 1 direct emissions, Scope 2 purchased energy emissions, and Scope 3 value chain emissions. The market encompasses the full spectrum of solution categories including dedicated carbon accounting engines, corporate carbon footprint management platforms, ESG reporting and disclosure tools, energy management integration solutions, carbon offset and credit management platforms, and supply chain emissions tracking systems as well as the supporting ecosystem of data providers, implementation consultants, and systems integrators that collectively constitute the carbon management software value chain.

The growth of the global carbon management software market is primarily driven by the accelerating convergence of binding regulatory disclosure mandates, expanding corporate net-zero commitments, and investor-led ESG due diligence requirements that are simultaneously obligating and incentivizing organizations across sectors and geographies to implement structured, auditable, and technology-enabled carbon management capabilities. The European Union’s Corporate Sustainability Reporting Directive, which entered phased application from fiscal year 2024 for large listed companies and will extend to all large companies and listed SMEs by 2027, mandates detailed greenhouse gas inventory reporting aligned with the GHG Protocol and European Sustainability Reporting Standards that cannot be practically fulfilled without dedicated carbon accounting software. The U.S. Securities and Exchange Commission’s climate-related disclosure rules, requiring material climate risk and Scope 1 and 2 emissions disclosure from registered public companies, and the International Sustainability Standards Board’s IFRS S1 and S2 standards gaining adoption across the United Kingdom, Australia, Canada, Japan, and Singapore, are collectively expanding the regulatory compliance demand for carbon management software beyond its European origin market to encompass the full spectrum of global capital market participants.

However, the market faces important structural constraints. The persistent fragmentation and inconsistency of emissions data across enterprise IT systems including ERP platforms, utility billing systems, fleet management tools, IoT sensor networks, and supplier reporting portals creates data integration complexity that substantially increases implementation timelines and costs for enterprise carbon management deployments and limits the real-time accuracy of emissions calculations for organizations with large and geographically dispersed operational footprints. The absence of a universally adopted, mandatory methodology standard for Scope 3 value chain emissions calculation where the GHG Protocol’s Scope 3 Standard provides a framework but affords substantial methodological discretion in spend-based versus activity-based versus supplier-specific emission factor selection creates comparability limitations in disclosed emissions data that undermine investor confidence and complicate regulatory verification.

Despite these challenges, the market outlook is strongly positive. The rapid maturation of AI-powered emissions forecasting, scenario modeling, and decarbonization pathway optimization capabilities within leading carbon management platforms is substantially expanding the decision-support value proposition of carbon software beyond compliance reporting toward strategic business intelligence that resonates with C-suite and board-level sustainability leadership. The integration of carbon management APIs with ERP systems from SAP, Oracle, and Microsoft Dynamics, IoT emissions monitoring infrastructure from Schneider Electric, Siemens, and Honeywell, and financial accounting platforms is progressively reducing the data integration burden that has historically been the primary implementation barrier for enterprise carbon management adoption. The strategic entry of global technology leaders including SAP, Salesforce, and Microsoft into the carbon management software market is validating the category’s commercial scale and accelerating enterprise buyer confidence in committing to multi-year SaaS subscriptions.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 12.7 Billion |

|

Market Size in 2026 |

USD 2.4 Billion |

|

Market Size in 2025 |

USD 1.9 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 16.8% |

|

Dominating Solution Type |

Carbon Accounting Software |

|

Fastest Growing Solution Type |

Supply Chain Carbon Management Solutions |

|

Dominating Deployment Mode |

Cloud-Based (SaaS) |

|

Fastest Growing Deployment Mode |

Hybrid Deployment |

|

Dominating Organization Size |

Large Enterprises |

|

Fastest Growing Organization Size |

Small & Medium Enterprises (SMEs) |

|

Dominating Application |

Emissions Monitoring & Reporting |

|

Fastest Growing Application |

Carbon Reduction & Decarbonization Planning |

|

Dominating End-Use Industry |

Energy & Utilities |

|

Fastest Growing End-Use Industry |

BFSI |

|

Dominating Emission Scope Coverage |

Scope 1 & 2 Management |

|

Fastest Growing Scope Coverage |

Full Scope (1, 2, and 3) Integrated Platforms |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Shift Toward End-to-End Carbon Management Platforms

The progressive consolidation of point-solution carbon accounting tools into comprehensive end-to-end carbon management platforms that integrate emissions data collection, calculation, scenario modeling, regulatory reporting, and carbon credit management within a unified software architecture is the defining commercial development reshaping competitive dynamics in the carbon management software market. Enterprise sustainability buyers are increasingly seeking to replace fragmented best-of-breed tool stacks where separate vendors provide carbon accounting, ESG reporting, energy management, and offset tracking capabilities that require manual data transfer and reconciliation between systems with integrated platform solutions that deliver a single source of truth for all carbon and sustainability data across the enterprise. SAP’s Sustainability Control Tower, Salesforce’s Net Zero Cloud, and Microsoft’s Cloud for Sustainability represent the platform consolidation strategy of global enterprise software leaders entering the carbon management market with broad integrations across their existing ERP, CRM, and productivity ecosystems, while purpose-built leaders including Sphera, Enablon, and Persefoni are expanding their core carbon accounting capabilities to incorporate adjacent ESG reporting, energy management, and supply chain sustainability modules that compete directly with enterprise platform consolidators.

The platform consolidation trend is fundamentally reshaping the competitive dynamics of the carbon management software market, creating significant pressure on point-solution vendors to either expand their functionality scope or position their products as best-of-breed components within open integration ecosystems. The outcome for enterprise buyers is a software landscape offering greater functional breadth per vendor relationship, reduced integration cost and data reconciliation burden, and improved auditability of the end-to-end emissions accounting trail from raw activity data through to disclosed regulatory filing.

Increasing Adoption of Real-Time Emissions Tracking

The transition of enterprise carbon management practice from annual or quarterly emissions inventory compilation in which operational activity data is retrospectively assembled and processed into GHG inventory reports after the close of each reporting period toward continuous real-time or near-real-time emissions monitoring and calculation represents a significant technology maturation trend that is expanding the operational value of carbon management software from compliance reporting tool toward live operational decision-support system. Real-time emissions tracking capabilities, enabled by direct integration with smart meter data streams, IoT-connected industrial equipment, fleet telematics systems, and utility billing APIs, allow operational managers to observe the carbon impact of energy consumption, production scheduling, logistics routing, and procurement decisions as they occur, creating actionable carbon intelligence that can inform day-to-day operational choices rather than only retrospective annual performance reporting.

The commercial deployment of real-time emissions monitoring by Schneider Electric’s EcoStruxure platform, Siemens’ Xcelerator sustainability management suite, and the IoT-integrated carbon tracking capabilities being developed by industrial software companies including Aveva and OSIsoft is creating enterprise customer expectations for real-time carbon data granularity that are establishing a new performance benchmark for carbon management software functionality. The convergence of real-time emissions data with AI-driven anomaly detection which can flag unexpected emission spikes from equipment malfunction, process inefficiency, or supplier substitution events is creating proactive carbon management capabilities that substantially increase the operational value proposition of continuous emissions monitoring relative to periodic batch inventory processes.

Increasing Corporate Net-Zero Commitments

The proliferation of corporate net-zero and science-based emissions reduction targets across multinational enterprises with the Science Based Targets initiative reporting over 7,000 companies globally with approved or committed science-based targets as of 2025 represents the foundational commercial demand driver for carbon management software by creating an enduring organizational requirement for structured, consistent, and technically defensible GHG inventory data that demonstrates credible progress against disclosed emissions reduction commitments. Net-zero commitments require enterprises to establish accurate emissions baselines across Scope 1, 2, and 3 categories, track year-on-year performance against interim reduction milestones, identify and prioritize decarbonization initiatives based on marginal abatement cost analysis, and report progress to investor, customer, and regulatory audiences in a manner that withstands third-party assurance verification. None of these requirements are practically achievable at enterprise scale through spreadsheet-based manual processes, creating an organizational technology mandate for dedicated carbon management software that is independent of the regulatory compliance driver and persists regardless of the pace of mandatory disclosure rule adoption. The growing market expectation that supplier decarbonization is a condition of continued commercial relationship with major enterprise buyers reflected in the CDP Supply Chain program’s 280 signatory member companies requesting emissions data from over 24,000 suppliers is progressively extending the carbon management software demand from first-tier enterprise adopters down through supply chain tiers to mid-market and SME organizations.

Rising ESG Reporting and Disclosure Requirements

The rapid expansion of mandatory ESG reporting and climate disclosure requirements across major capital market jurisdictions is creating a binding regulatory demand for carbon management software among public companies, large private enterprises, and financial institutions that must now produce externally assured, regulator-auditable GHG emissions data as part of their statutory reporting obligations. The EU Corporate Sustainability Reporting Directive, replacing the Non-Financial Reporting Directive, mandates double materiality-based sustainability reporting under European Sustainability Reporting Standards that include detailed GHG inventory disclosure, climate-related risk and opportunity assessment aligned with TCFD recommendations, and biodiversity, water, social, and governance metrics, applicable to approximately 50,000 companies operating in European markets. The International Sustainability Standards Board’s IFRS S1 and S2 climate disclosure standards, endorsed for application by the U.K., Australia, Canada, Japan, Singapore, and multiple other jurisdictions, are establishing a converging global mandatory climate disclosure baseline that is expanding the enterprise carbon management software addressable market well beyond its initial European regulatory anchor. Financial institutions face additional regulatory pressure from the European Central Bank’s supervisory expectations for climate risk integration, the Task Force on Climate-related Financial Disclosures adoption by the Bank of England, and national green finance taxonomies in the EU, U.K., and Singapore that require portfolio-level emissions and climate alignment metrics.

Integration with ERP, IoT, and Supply Chain Systems

The deep, native integration of carbon management software with leading enterprise resource planning systems principally SAP S/4HANA, Oracle Fusion Cloud, Microsoft Dynamics 365, and Infor CloudSuite represents the highest-impact near-term opportunity for reducing the data integration burden that is the primary barrier to enterprise carbon management software adoption at scale. Native ERP integration enables automatic extraction of procurement spend data for Scope 3 Category 1 calculation, energy procurement records for Scope 2 calculation, fuel consumption data for Scope 1 calculation, and logistics freight data for Scope 3 Category 4 calculation without manual data export and transformation workflows, dramatically reducing inventory compilation time and improving data completeness. SAP’s Sustainability Footprint Management module, natively embedded within the SAP S/4HANA ERP environment and leveraging SAP’s product carbon footprint calculation engine, represents the most advanced current embodiment of this ERP-native carbon management integration strategy and is establishing a competitive benchmark that is compelling Microsoft, Oracle, and Infor to develop comparable native sustainability data integration capabilities within their respective ERP platforms.

AI-Driven Emissions Forecasting and Optimization

The application of machine learning algorithms and predictive AI models to enterprise carbon management data is creating a significant product differentiation and value-creation opportunity for carbon management software vendors to expand their value proposition beyond retrospective GHG inventory reporting toward forward-looking emissions forecasting, decarbonization pathway optimization, and AI-guided carbon reduction opportunity identification that resonates with the strategic sustainability decision-making needs of C-suite leadership and board sustainability committees. AI-powered emissions forecasting which applies regression, time-series, and scenario analysis models to historical emissions data, energy consumption patterns, production schedules, and macroeconomic variables to project future emissions trajectories under different operational and policy scenarios enables enterprise sustainability teams to assess their anticipated progress against science-based targets under current trajectories and model the emissions impact of alternative operational strategies, capital investment decisions, and supplier substitution choices before commitment. The integration of generative AI capabilities within carbon management platforms to automate disclosure narrative generation, interpret regulatory requirement changes, and synthesize decarbonization recommendations from pattern analysis across peer company benchmarking data represents an emerging competitive frontier that leading platform developers including Persefoni, Watershed, and Microsoft’s Cloud for Sustainability are actively investing in.

By Solution Type: In 2026, Carbon Accounting Software to Dominate

Based on solution type, the global carbon management software market is segmented into carbon accounting software, carbon footprint management platforms, ESG reporting and disclosure software, energy management integration solutions, carbon offset management platforms, supply chain carbon management solutions, and others. In 2026, the carbon accounting software segment is expected to account for the largest share of the global carbon management software market. The large share of this segment is attributed to carbon accounting software’s status as the foundational technology requirement for all downstream carbon management activities with accurate GHG inventory data being a prerequisite for ESG reporting, decarbonization planning, regulatory disclosure, and carbon credit management and the maturity of dedicated carbon accounting platforms from established vendors including Sphera, Enablon, and Persefoni that have accumulated large enterprise client bases over multiple regulatory reporting cycles. The mandatory Scope 1 and 2 emissions disclosure requirements of the EU CSRD and SEC climate rules are creating immediate compliance-driven demand for carbon accounting software across the population of obligated reporting entities.

However, the supply chain carbon management solutions segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the rapidly intensifying enterprise demand for supplier-level Scope 3 emissions data driven by regulatory Scope 3 disclosure requirements, CDP Supply Chain program participation, and SBTi supplier engagement criteria, combined with the technical complexity of multi-tier supply chain emissions data collection and calculation that requires purpose-built software infrastructure beyond the capabilities of general-purpose carbon accounting platforms.

By Deployment Mode: In 2026, Cloud-Based (SaaS) to Hold the Largest Share

Based on deployment mode, the global carbon management software market is segmented into cloud-based (SaaS), on-premise, and hybrid deployment. In 2026, the cloud-based segment is expected to account for the largest share of the global carbon management software market. This dominance reflects the structural advantages of SaaS deployment for carbon management applications including automatic regulatory content updates, multi-party supplier data collaboration, scalable data storage for large-volume emissions activity datasets, and lower total cost of ownership relative to on-premise alternatives that are particularly valuable given the continuous evolution of carbon accounting standards and the multi-stakeholder data sharing requirements of Scope 3 supply chain emissions calculation. The dominant SaaS delivery model of all major pure-play carbon management software vendors, including Persefoni, Watershed, Plan A, Sweep, Greenly, and Normative, reflects the native cloud architecture of the new-generation purpose-built carbon management platforms that are capturing the majority of new enterprise buyer adoption.

However, the hybrid deployment segment is projected to register the highest CAGR during the forecast period. This growth is driven by the requirements of regulated industries including financial services, energy utilities, and government entities where data sovereignty regulations, internal IT security policies, and sensitive operational data governance frameworks require certain emissions data components to be processed and stored on-premise while leveraging cloud-based reporting, benchmarking, and regulatory disclosure submission capabilities.

By Organization Size: In 2026, Large Enterprises to Hold the Largest Share

Based on organization size, the global carbon management software market is segmented into large enterprises and small and medium enterprises. In 2026, the large enterprises segment is expected to account for the largest share of the global carbon management software market. This dominance reflects the concentration of mandatory regulatory disclosure obligations, investor ESG scrutiny, and CDP response requirements in the large enterprise segment, the availability of dedicated sustainability team resources and IT integration budgets required for full-scope carbon management software deployment, and the established multi-year procurement relationships between enterprise software vendors and large corporate buyers that are being leveraged for carbon management solution sales by ERP-native vendors including SAP and Microsoft.

However, the small and medium enterprises segment is projected to register the highest CAGR during the forecast period. This growth is driven by the extension of EU CSRD mandatory reporting obligations to listed SMEs from fiscal year 2026, the escalating Scope 3 supplier data requests from large enterprise CDP Supply Chain program participants, the proliferation of simplified SME-focused SaaS carbon management platforms at accessible price points, and the growing availability of SME sustainability financing incentives from European banking institutions that require carbon footprint assessment and management plan documentation.

By Application: In 2026, Emissions Monitoring & Reporting to Hold the Largest Share

Based on application, the global carbon management software market is segmented into emissions monitoring and reporting, carbon reduction and decarbonization planning, regulatory compliance management, carbon credit and offset management, and sustainability performance management. In 2026, the emissions monitoring and reporting segment is expected to account for the largest share of the global carbon management software market. This dominance reflects the foundational role of emissions monitoring and reporting as the entry-point application driving the majority of initial carbon management software adoption as organizations implement GHG measurement capabilities to fulfill immediate regulatory disclosure obligations and investor ESG data requests before progressing to more advanced decarbonization planning and offset management capabilities. The immediate compliance deadline pressure of CSRD, SEC climate rules, and ISSB S2 adoption across multiple jurisdictions is ensuring that emissions monitoring and reporting remains the primary procurement driver for carbon management software through the near term of the forecast period.

However, the carbon reduction and decarbonization planning segment is projected to register the highest CAGR during the forecast period. This growth is driven by the maturation of enterprise carbon management programs beyond initial compliance reporting toward strategic decarbonization planning, the SBTi’s requirement for net-zero pathway documentation and interim milestone progress reporting that necessitates structured decarbonization roadmap planning software capabilities, and the growing enterprise investment in AI-assisted scenario modeling and marginal abatement cost analysis tools that optimize decarbonization investment allocation across operational, supply chain, and product portfolio dimensions.

By End-Use Industry: In 2026, Energy & Utilities to Hold the Largest Share

Based on end-use industry, the global carbon management software market is segmented into energy and utilities, manufacturing, transportation and logistics, BFSI, IT and telecom, retail and consumer goods, healthcare, government and public sector, and others. In 2026, the energy and utilities segment is expected to account for the largest share of the global carbon management software market. This dominance reflects the energy and utilities sector’s position as the economy’s largest direct greenhouse gas emitter, its long-established obligation to participate in emissions trading systems including the EU ETS and California Cap-and-Trade Program that require precise emissions metering and registry-linked reporting, and the sector’s advanced regulatory sophistication in carbon data management relative to other industries. The energy sector’s dense IoT instrumentation of generation, transmission, and distribution assets, combined with the regulatory requirement for facility-level emissions reporting under EPA’s Mandatory Greenhouse Gas Reporting Rule and EU ETS monitoring, reporting, and verification requirements, creates both the data infrastructure and the compliance driver for advanced carbon management software deployment at greater functional depth than most other sectors.

However, the BFSI segment is projected to register the highest CAGR during the forecast period. This growth is driven by the financial services sector’s rapidly escalating regulatory pressure to measure and disclose financed emissions across loan and investment portfolios under PCAF methodology, the ECB’s supervisory expectations for climate risk integration in bank risk management frameworks, the Net-Zero Banking Alliance’s and Net-Zero Asset Managers Initiative’s commitments covering over USD 130 trillion in assets under management, and the specialized technical complexity of financial institution carbon accounting that is driving significant investment in purpose-built financial sector carbon management software from vendors including Persefoni, Watershed, and Carbon Account.

By Emission Scope: In 2026, Scope 1 & 2 Management to Hold the Largest Share

Based on emission scope coverage, the global carbon management software market is segmented into Scope 1 and 2 management, Scope 3 management, and full scope (1, 2, and 3) integrated platforms. In 2026, the Scope 1 and 2 management segment is expected to account for the largest share of the global carbon management software market. This dominance reflects the greater data availability, methodological maturity, and immediate regulatory compliance priority of Scope 1 and 2 emissions calculation relative to the technically more complex and data-scarce Scope 3 category with the initial phase of regulatory mandatory disclosure under CSRD and SEC climate rules focusing primarily on Scope 1 and 2 emissions with external assurance requirements, providing the immediate compliance deadline that is driving the majority of current enterprise carbon management software procurement decisions.

However, the full scope (1, 2, and 3) integrated platforms segment is projected to register the highest CAGR during the forecast period. This growth reflects the increasing regulatory and investor pressure for comprehensive Scope 3 disclosure, the SBTi’s requirement that near-term science-based targets cover Scope 3 emissions for companies where Scope 3 exceeds 40% of total footprint, and the growing enterprise recognition that value chain emissions reduction which requires Scope 3 measurement as the foundation for supplier engagement and procurement decarbonization strategies is essential for achieving net-zero commitments when Scope 3 represents the dominant share of most corporate carbon footprints. This segment is particularly critical for differentiation and premium pricing within the carbon management software market.

Carbon Management Software Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global carbon management software market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global carbon management software market. The largest share of this region is mainly due to North America’s concentration of the world’s largest technology software companies including SAP America, Salesforce, Microsoft, IBM, and a dense ecosystem of venture-backed carbon management SaaS startups including Persefoni, Watershed, Sweep, and Watershed whose global enterprise customer relationships, established software procurement channels, and integration with dominant U.S. ERP and CRM platforms provide structural distribution advantages for carbon management software adoption. The United States’ population of approximately 6,600 SEC-registered public companies subject to phased climate disclosure compliance obligations, combined with the voluntary adoption of SBTi targets and CDP response commitments across the S&P 500 and Russell 1000 corporate universe, provides a large and commercially sophisticated enterprise buyer base for carbon management software that is driving the region’s revenue leadership. California’s Climate Corporate Data Accountability Act, requiring large companies doing business in California to report Scope 1, 2, and 3 emissions from 2026, adds a significant state-level regulatory compliance driver that reinforces the federal SEC disclosure mandate for the large corporate population conducting significant California business.

Europe represents the second largest regional market for carbon management software and the regulatory epicenter of mandatory climate disclosure, anchored by the EU Corporate Sustainability Reporting Directive’s application to approximately 50,000 European and non-EU companies with substantial European operations. Germany’s industrial enterprise base, the U.K.’s TCFD mandatory reporting framework for premium listed companies and large private enterprises, France’s Grenelle II law requirements, and the Netherlands’ strong financial services sector facing PCAF financed emissions disclosure obligations collectively make Europe the highest regulatory compliance intensity market for carbon management software globally. The European carbon management software ecosystem is anchored by established vendors including Enablon, Plan A, Sweep, and Normative alongside the European operations of global enterprise platform vendors, with the GreenTech sector’s strong investment activity across Germany, the U.K., Sweden, and France providing ongoing innovation in purpose-built European carbon management software.

However, the Asia-Pacific carbon management software market is expected to grow at the fastest CAGR during the forecast period. The region’s rapid growth is driven by Japan’s mandatory climate-related financial disclosure requirements for Tokyo Stock Exchange Prime Market-listed companies under the Financial Services Agency’s TCFD-aligned framework, Australia’s Treasury Laws Amendment Act mandating ISSB-aligned climate disclosure for large corporations from fiscal year 2025, Singapore’s Sustainability Reporting Advisory Committee roadmap for mandatory climate reporting under SGX listing rules, and South Korea’s mandatory ESG disclosure framework for KOSPI-listed companies expanding to cover all listed companies by 2030. China’s national carbon emissions trading system expansion from power generation to cement, steel, aluminum, aviation, and petrochemicals, combined with the Chinese Securities Regulatory Commission’s sustainability disclosure guidelines for A-share listed companies, is creating a large and rapidly expanding regulatory compliance demand for carbon management software in the world’s largest emitting economy. The concentration of global manufacturing supply chains in Asia-Pacific particularly in China, India, Bangladesh, and Vietnam is creating growing Scope 3 supplier data provision obligations for Asian manufacturers serving European and North American enterprise customers subject to CSRD and SBTi supply chain engagement requirements.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players’ product platforms, technology capabilities, geographic footprint, regulatory coverage depth, and key strategic developments. Key players operating in the global carbon management software market include SAP SE (Germany), Salesforce Inc. / Net Zero Cloud (U.S.), Microsoft Corporation / Cloud for Sustainability (U.S.), IBM Corporation (U.S.), Schneider Electric SE (France), Sphera Solutions (U.S.), Enablon / Wolters Kluwer (France/Netherlands), Persefoni AI Inc. (U.S.), Plan A (Germany), Watershed Technology Inc. (U.S.), Sweep (France), Normative.io (Sweden), Greenly (France), Diligent Corporation (U.S.), and Intelex Technologies (Canada), among others.

The global carbon management software market is expected to reach USD 12.7 billion by 2036 from an estimated USD 2.4 billion in 2026, at a CAGR of 16.8% during the forecast period 2026-2036.

In 2026, the carbon accounting software segment is expected to hold the largest share of the global carbon management software market, driven by its foundational role as the prerequisite technology for all downstream carbon management activities and the immediate compliance demand from CSRD and SEC climate disclosure regulatory obligations across the enterprise buyer population.

The supply chain carbon management solutions segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the rapidly intensifying enterprise demand for Scope 3 supplier-level emissions data from regulatory disclosure requirements, CDP Supply Chain program participation, and SBTi supplier engagement criteria that require purpose-built supply chain carbon data infrastructure beyond the capabilities of general-purpose carbon accounting platforms.

The full scope (1, 2, and 3) integrated platforms segment is the most strategically significant for market differentiation and premium pricing, as comprehensive Scope 3 integration capability covering all 15 GHG Protocol categories with both spend-based and primary data collection methodologies represents the highest technical complexity and the greatest unmet need in enterprise carbon management. This segment is projected to register the highest CAGR during the forecast period, driven by SBTi net-zero target requirements and escalating regulatory Scope 3 disclosure mandates.

The BFSI segment is expected to register the highest CAGR during the forecast period, driven by the financial services sector’s rapidly escalating regulatory pressure to measure and disclose financed emissions under PCAF methodology, ECB supervisory climate risk expectations, and the Net-Zero Banking Alliance’s commitments covering over USD 130 trillion in assets under management that require specialized financial institution carbon management software capabilities.

The growth of this market is primarily driven by the accelerating convergence of binding regulatory disclosure mandates including EU CSRD and SEC climate rules, the proliferation of corporate net-zero and science-based emissions reduction commitments across the global enterprise universe, the growing investor-led ESG due diligence requirements for auditable GHG inventory data, and the rapidly expanding demand for Scope 3 value chain emissions tracking that is progressively extending carbon management software adoption from large enterprise buyers down through supply chain tiers to mid-market and SME organizations.

Asia-Pacific is expected to register the highest growth rate in the global carbon management software market during the forecast period 2026-2036, driven by Japan’s mandatory TCFD-aligned climate disclosure for Tokyo Stock Exchange Prime Market companies, Australia’s ISSB-aligned mandatory reporting from fiscal year 2025, Singapore’s SGX climate disclosure roadmap, South Korea’s expanding ESG disclosure framework, and China’s national ETS expansion and listed company sustainability disclosure guidelines that collectively constitute the fastest-expanding regulatory compliance demand for carbon management software across any global region.

Key players are SAP SE (Germany), Salesforce Inc. / Net Zero Cloud (U.S.), Microsoft Corporation / Cloud for Sustainability (U.S.), IBM Corporation (U.S.), Schneider Electric SE (France), Sphera Solutions (U.S.), Enablon / Wolters Kluwer (France/Netherlands), Persefoni AI Inc. (U.S.), Plan A (Germany), Watershed Technology Inc. (U.S.), Sweep (France), Normative.io (Sweden), Greenly (France), Diligent Corporation (U.S.), and Intelex Technologies (Canada), among others.

The carbon management software market is served by three primary pricing model structures: SaaS subscription pricing based on user seat count and module selection, which dominates the SME and mid-market segments with annual fees typically ranging from USD 500 to USD 100,000; tiered enterprise pricing based on organizational revenue, headcount, or emissions volume that scales license fees with organizational complexity; and modular pricing based on data point volume, emission category coverage, and subsidiary count that aligns software cost with the scope and complexity of the buyer’s GHG inventory program. Enterprise platform vendors including SAP and Salesforce typically bundle carbon management modules within broader platform subscription agreements, while pure-play vendors offer standalone carbon management subscriptions with implementation professional services priced separately.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.2 Restraints

4.2.3 Opportunities

4.2.4 Challenges

4.3 Key Market Trends

4.4 Technology Landscape

4.5 Carbon Management Software Architecture

4.6 Value Chain Analysis

4.7 Regulatory and Standards Landscape

4.8 Porter’s Five Forces Analysis

4.9 Investment and Funding Landscape

4.10 Pricing Analysis

5. Carbon Management Software Market, by Solution Type

5.1 Introduction

5.2 Carbon Accounting Software

5.3 Carbon Footprint Management Platforms

5.4 ESG Reporting & Disclosure Software

5.5 Energy Management Integration Solutions

5.6 Carbon Offset Management Platforms

5.7 Supply Chain Carbon Management Solutions

5.8 Others

6. Carbon Management Software Market, by Deployment Mode

6.1 Introduction

6.2 Cloud-Based (SaaS)

6.3 On-Premise

6.4 Hybrid Deployment

7. Carbon Management Software Market, by Organization Size

7.1 Introduction

7.2 Large Enterprises

7.3 Small & Medium Enterprises (SMEs)

8. Carbon Management Software Market, by Application

8.1 Introduction

8.2 Emissions Monitoring & Reporting

8.3 Carbon Reduction & Decarbonization Planning

8.4 Regulatory Compliance Management

8.5 Carbon Credit & Offset Management

8.6 Sustainability Performance Management

9. Carbon Management Software Market, by End-Use Industry

9.1 Introduction

9.2 Energy & Utilities

9.3 Manufacturing

9.4 Transportation & Logistics

9.5 BFSI

9.6 IT & Telecom

9.7 Retail & Consumer Goods

9.8 Healthcare

9.9 Government & Public Sector

9.10 Others

10. Carbon Management Software Market, by Emission Scope Coverage

10.1 Introduction

10.2 Scope 1 & 2 Management

10.3 Scope 3 Management

10.4 Full Scope (1, 2, and 3) Integrated Platforms

11. Carbon Management Software Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Netherlands

11.3.5 Sweden

11.3.6 Norway

11.3.7 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Chile

11.5.4 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 SAP SE

13.2 Salesforce, Inc. (Net Zero Cloud)

13.3 Microsoft Corporation (Cloud for Sustainability)

13.4 IBM Corporation

13.5 Schneider Electric SE

13.6 Sphera Solutions

13.7 Enablon (Wolters Kluwer)

13.8 Persefoni AI Inc.

13.9 Plan A

13.10 Watershed Technology Inc.

13.11 Sweep

13.12 Normative.io

13.13 Greenly

13.14 Diligent Corporation

13.15 Intelex Technologies

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: May-2025

Subscribe to get the latest industry updates