Resources

About Us

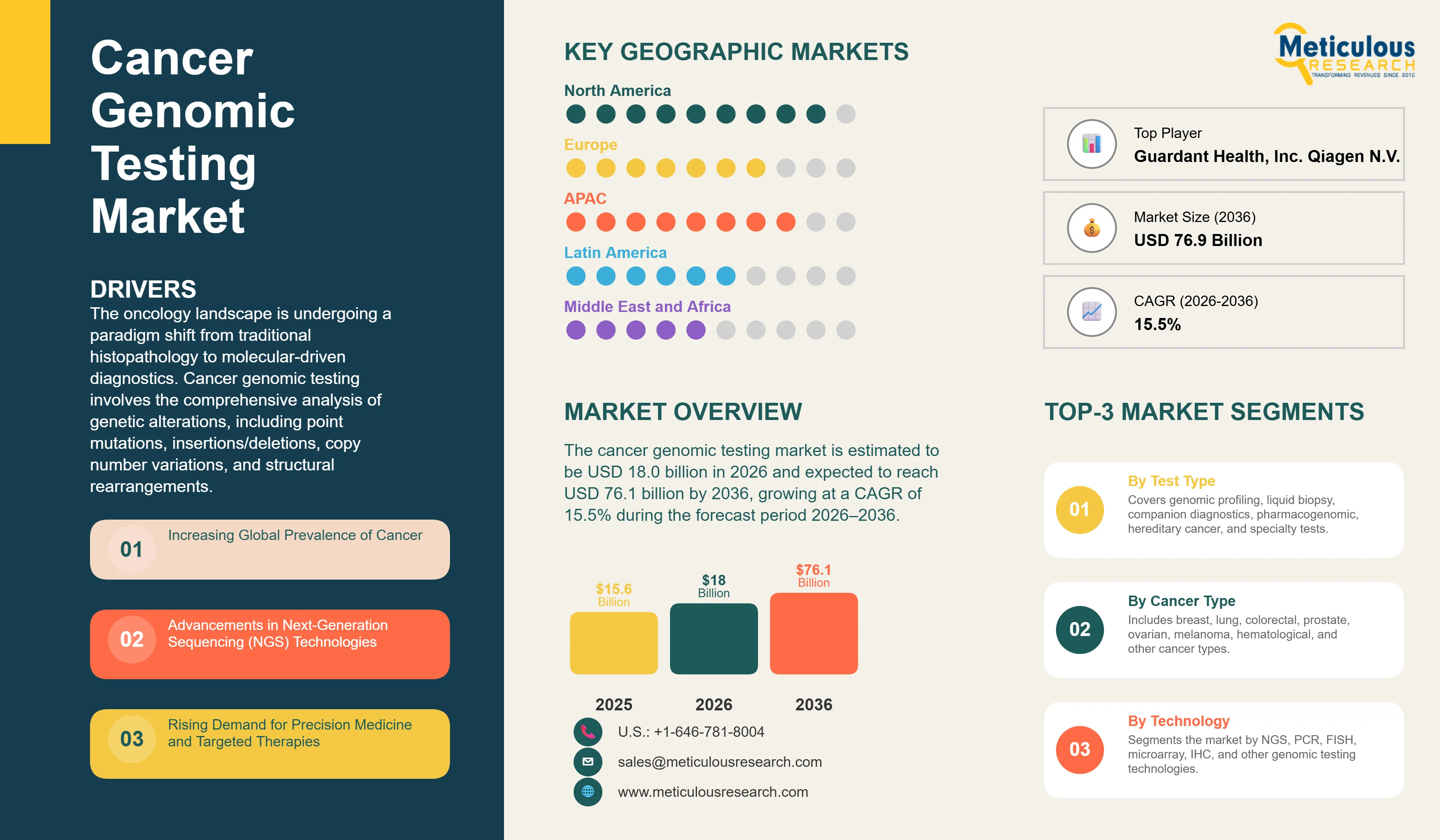

The global cancer genomic testing market is estimated to be USD 18.0 billion in 2026. This market is expected to reach USD 76.1 billion by 2036, growing at a CAGR of 15.5% during the forecast period 2026–2036. The growth of this market is driven by the increasing prevalence of cancer globally, the rising demand for precision medicine, advancements in next-generation sequencing (NGS) technologies, and favorable reimbursement policies for genomic testing in developed regions. Furthermore, the integration of artificial intelligence (AI) in genomic data interpretation and the growing number of FDA-approved companion diagnostics are expected to offer significant growth opportunities for market players.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The oncology landscape is undergoing a paradigm shift from traditional histopathology to molecular-driven diagnostics. Cancer genomic testing involves the comprehensive analysis of genetic alterations, including point mutations, insertions/deletions, copy number variations, and structural rearrangements. This molecular insight is fundamental to precision oncology, enabling clinicians to tailor therapeutic interventions based on the unique genomic signature of a patient's tumor. According to the World Health Organization (WHO), cancer remains a leading cause of death worldwide, with nearly 10 million deaths recorded in 2020. As the global cancer burden is projected to rise to 28.4 million cases by 2040, the demand for robust cancer sequencing and biomarker testing has become imperative for effective disease management.

Tumor genomic profiling has transitioned from research-only applications to routine clinical practice. The advent of Next-Generation Sequencing (NGS) has significantly reduced the cost and time required for whole-exome and whole-genome sequencing. The National Cancer Institute (NCI) emphasizes that genomic testing not only aids in therapy selection but also plays a critical role in clinical trial matching and identifying hereditary cancer syndromes. As precision oncology diagnostics become more accessible, the market is witnessing an influx of multi-gene panels and liquid biopsy assays that provide a non-invasive alternative to traditional tissue biopsies. The shift toward oncology genomics is further supported by the development of standardized reporting guidelines and the establishment of molecular tumor boards in leading cancer centers worldwide.

NGS cancer testing has revolutionized the diagnostic workflow by allowing for the simultaneous assessment of hundreds of genes. This high-throughput capability is essential for identifying actionable mutations in solid tumors and hematological malignancies. The integration of cancer biomarker testing into standard care pathways is being accelerated by the falling costs of sequencing and the increasing availability of targeted therapies. Industry associations like the American Society of Clinical Oncology (ASCO) and the European Society for Medical Oncology (ESMO) have incorporated genomic testing recommendations into their clinical practice guidelines, underscoring its clinical utility in improving patient survival rates.

Drivers

Increasing Global Prevalence of Cancer

The escalating incidence of cancer worldwide remains the primary driver for the cancer genomic testing market. According to the International Agency for Research on Cancer and the World Health Organization, approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported globally in 2022, making cancer one of the leading causes of mortality worldwide. Furthermore, breast cancer remains the most commonly diagnosed cancer globally, accounting for approximately 2.3 million new cases annually. The global cancer burden is projected to increase significantly, with the International Agency for Research on Cancer estimating that new cancer cases will exceed 35 million annually by 2050, representing a 77% increase compared with 2022 levels. This growing disease burden is intensifying the demand for precision oncology and advanced molecular diagnostics. Genomic testing enables the identification of actionable genetic alterations, supporting targeted therapy selection, treatment monitoring, and personalized disease management, ultimately improving clinical outcomes and healthcare efficiency.

Advancements in Next-Generation Sequencing (NGS) Technologies

Technological breakthroughs in NGS have revolutionized oncology genomics by significantly reducing sequencing costs and turnaround times. The launch of high-throughput platforms, such as Illumina's TruSight Oncology (TSO) Comprehensive in March 2022, has made comprehensive genomic profiling (CGP) more accessible in clinical settings. These advancements enable the simultaneous assessment of multiple tumor genes and biomarkers, facilitating precision medicine decisions. The shift from single-gene testing to large-scale genomic panels is a direct result of these technological improvements, allowing for more comprehensive tumor characterization.

Restraints

High Cost of Advanced Genomic Testing and Bioinformatics

Despite falling sequencing costs, the total expenditure for comprehensive genomic profiling remains a significant barrier. The costs associated with library preparation, complex bioinformatics analysis, and expert clinical interpretation can exceed $3,000 to $5,000 per test. In many developing regions, these costs are not fully covered by insurance, limiting patient access. Additionally, the infrastructure required for high-volume genomic data storage and processing adds to the financial burden for diagnostic laboratories.

Stringent Regulatory Landscape and Reimbursement Hurdles

The regulatory environment for genomic assays is increasingly complex. The FDA's 2024 final rule on Laboratory Developed Tests (LDTs) has introduced more rigorous oversight, requiring many diagnostic labs to seek formal FDA approval for their proprietary tests. This increases the compliance cost and may delay the market entry of innovative sequencing solutions. Furthermore, reimbursement policies for multi-gene panels vary significantly across regions, with some payers still viewing large-scale genomic profiling as experimental, thereby hindering widespread clinical adoption.

Opportunities

Expansion of Liquid Biopsy for Early Detection and Monitoring

Liquid biopsy offers a transformative, minimally invasive opportunity for the market. By analyzing circulating tumor DNA (ctDNA) from blood samples, clinicians can monitor treatment response and detect recurrence much earlier than traditional imaging. In May 2023, Labcorp launched its Plasma Focus liquid biopsy test for advanced solid tumors, highlighting the commercial momentum in this space. The potential for multi-cancer early detection (MCED) tests to screen high-risk populations represents a multi-billion dollar opportunity for genomic testing providers.

Integration of Artificial Intelligence (AI) in Genomic Data Interpretation

The integration of AI and machine learning algorithms presents a significant opportunity to enhance the accuracy and efficiency of genomic diagnostics. AI can process vast amounts of sequencing data to identify rare variants and predict patient responses to specific therapeutic combinations. This is particularly relevant for immunotherapy, where AI-driven biomarkers can help stratify patients more effectively. Strategic investments in AI-enabled bioinformatics platforms are expected to be a key differentiator for market players in the coming years.

Challenges

Data Privacy and Cybersecurity Concerns

As genomic data is highly sensitive and personal, ensuring its security is a critical challenge. The increasing use of cloud-based platforms for genomic data storage makes healthcare institutions vulnerable to cyberattacks and data breaches. Establishing robust cybersecurity frameworks and ensuring compliance with data protection regulations (like GDPR and HIPAA) is essential to maintain patient trust and regulatory standing.

Shortage of Skilled Bioinformaticians and Genetic Counselors

The rapid expansion of the oncology genomics market has outpaced the supply of trained professionals capable of interpreting complex genomic data. There is a global shortage of bioinformaticians who can develop and manage sequencing pipelines, as well as genetic counselors who can effectively communicate molecular findings to patients and their families. This human resource gap can lead to bottlenecks in clinical reporting and limit the impact of genomic testing on patient care.

Trends

Shift from Single-Gene Testing to Comprehensive Genomic Profiling (CGP)

A major trend in the market is the transition toward CGP, which assesses hundreds of genes simultaneously. This approach is more efficient than sequential single-gene testing, which can deplete tissue samples and delay treatment. CGP provides a more holistic view of the tumor's molecular landscape, including complex biomarkers like TMB and MSI. This trend is being driven by the inclusion of CGP in clinical guidelines from organizations like ASCO and ESMO.

Decentralization of NGS Testing to Community Hospital Settings

While large reference laboratories still dominate, there is a clear trend toward the decentralization of genomic testing. The development of automated, easy-to-use benchtop sequencers is enabling community hospitals to bring NGS testing in-house. This reduces the turnaround time for critical diagnostic results from weeks to days, allowing for faster treatment initiation. Companies are increasingly offering 'turnkey' solutions that include both sequencing hardware and automated reporting software to support this shift.

Analysis by Test Type

The genomic profiling tests segment is estimated to account for the largest share of the global cancer genomic testing market in 2026. This dominance is attributed to the rising adoption of CGP in clinical guidelines, such as those from the National Comprehensive Cancer Network (NCCN). Conversely, the liquid biopsy segment is expected to grow at the fastest CAGR. This is driven by its application in 'real-time' monitoring of tumor evolution and the increasing clinical utility of circulating tumor DNA (ctDNA) for detecting recurrence months before traditional imaging.

Analysis by Technology

Next-generation sequencing (NGS) is the leading technology segment. Its ability to perform high-throughput sequencing of millions of DNA fragments simultaneously makes it indispensable for modern oncology. While PCR remains relevant for specific, high-sensitivity tests (like KRAS mutations), the comprehensive nature of NGS is driving its displacement of older technologies like FISH in many diagnostic workflows.

Regional Market Analysis and Growth Prospects

North America is expected to hold the largest market share in 2026. The region's leadership is underpinned by a robust ecosystem of biotechnology companies, favorable Medicare coverage for NGS-based tests, and a high rate of personalized medicine adoption. The Asia-Pacific region is projected to be the fastest-growing market, with a projected CAGR of 22.6%. This growth is fueled by increasing healthcare investments in China and India, a large patient pool, and the expansion of global diagnostic giants into these emerging markets. Europe follows North America, with strong government support for genomics initiatives in countries like the U.K., Germany, and France.

The global cancer genomic testing market is highly competitive and fragmented, with several key players dominating the NGS and companion diagnostics segments. Companies are focusing on product launches, strategic partnerships, and acquisitions to expand their test portfolios and geographic reach. For instance, the acquisition of smaller bioinformatics firms by major diagnostic players is a common strategy to enhance data interpretation capabilities and offer 'end-to-end' solutions to clinicians.

The key companies operating in the global cancer genomic testing market include Illumina, Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), F. Hoffmann-La Roche Ltd (Switzerland), Qiagen N.V. (Netherlands), Agilent Technologies, Inc. (U.S.), Myriad Genetics, Inc. (U.S.), Exact Sciences Corporation (U.S.), Guardant Health, Inc. (U.S.), Foundation Medicine, Inc. (U.S.), Natera, Inc. (U.S.), NeoGenomics Laboratories, Inc. (U.S.), Veracyte, Inc. (U.S.), Tempus Labs, Inc. (U.S.), BGI Group (China), Caris Life Sciences (U.S.), Personalis, Inc. (U.S.), Burning Rock Biotech Limited (China), Fulgent Genetics, Inc. (U.S.), and Nanostring Technologies, Inc. (U.S.).

What is the current market size and the projected growth rate for the cancer genomic testing market?

The market is estimated to reach $76.01 billion by 2036, growing at a CAGR of 15.5% from 2026 to 2036.

Next-generation sequencing (NGS) dominates due to its high-throughput capabilities and ability to detect complex genomic alterations simultaneously.

The rising incidence of non-small cell lung cancer (NSCLC) and the availability of multiple FDA-approved targeted therapies requiring biomarker testing drive this segment.

AI is accelerating data interpretation, improving the accuracy of variant calling, and enabling the discovery of novel multi-omic biomarkers.

The Asia-Pacific region is projected to grow at the fastest CAGR due to increasing healthcare infrastructure and rising cancer awareness.

1. Introduction

1.1. Market Definition & Scope

1.2. Currency & Pricing

1.3. Market Stakeholders

2. Research Methodology

2.1. Research Process

2.2. Data Mining & Secondary Research

2.3. Primary Research & Expert Interviews

2.4. Market Size Estimation

2.4.1. Bottom-up Approach

2.4.2. Top-down Approach

2.5. Assumptions & Limitations

3. Executive Summary

3.1. Market Overview

3.2. Segmental Highlights

3.3. Regional Highlights

3.4. Competitive Insights

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Global Prevalence of Cancer

4.2.1.2. Advancements in Next-Generation Sequencing (NGS) Technologies

4.2.1.3. Rising Demand for Precision Medicine and Targeted Therapies

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Genomic Testing and Bioinformatics

4.2.2.2. Stringent Regulatory Landscape and Reimbursement Hurdles

4.2.3. Opportunities

4.2.3.1. Expansion of Liquid Biopsy for Early Detection and Monitoring

4.2.3.2. Integration of Artificial Intelligence (AI) in Genomic Data Interpretation

4.2.4. Challenges

4.2.4.1. Data Privacy and Cybersecurity Concerns

4.2.4.2. Shortage of Skilled Bioinformaticians and Genetic Counselors

4.2.5. Trends

4.2.5.1. Shift from Single-Gene Testing to Comprehensive Genomic Profiling (CGP)

4.2.5.2. Decentralization of NGS Testing to Community Hospital Settings

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.4.1. North America (FDA, CMS)

4.4.2. Europe (EMA, IVDR)

4.4.3. Asia-Pacific (NMPA, PMDA)

4.5. Value Chain Analysis

4.6. Pricing Analysis

5. Global Cancer Genomic Testing Market Assessment, by Test Type

5.1. Introduction

5.2. Genomic Profiling Tests

5.3. Liquid Biopsy Tests

5.4. Companion Diagnostic Tests

5.5. Pharmacogenomic Tests

5.6. Hereditary Cancer Tests

5.7. Other Specialized Genomic Tests

6. Global Cancer Genomic Testing Market Assessment, by Cancer Type

6.1. Introduction

6.2. Breast Cancer

6.3. Lung Cancer

6.4. Colorectal Cancer

6.5. Prostate Cancer

6.6. Ovarian Cancer

6.7. Melanoma

6.8. Hematological Malignancies

6.8.1. Leukemia

6.8.2. Lymphoma

6.9. Other Specific Cancer Types

7. Global Cancer Genomic Testing Market Assessment, by Technology

7.1. Introduction

7.2. Next-Generation Sequencing (NGS)

7.3. Polymerase Chain Reaction (PCR)

7.4. Fluorescence In Situ Hybridization (FISH)

7.5. Microarray

7.6. Immunohistochemistry (IHC)

7.7. Other Genomic Testing Technologies

8. Global Cancer Genomic Testing Market Assessment, by End User

8.1. Introduction

8.2. Hospitals

8.3. Diagnostic Laboratories

8.4. Academic & Research Institutions

8.5. Cancer Centers

8.6. Other Healthcare Providers

9. Global Cancer Genomic Testing Market Assessment, by Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Australia

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Introduction

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share/Ranking Analysis

11. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments)

11.1. Illumina, Inc.

11.2. Thermo Fisher Scientific Inc.

11.3. F. Hoffmann-La Roche Ltd

11.4. Qiagen N.V.

11.5. Agilent Technologies, Inc.

11.6. Myriad Genetics, Inc.

11.7. Exact Sciences Corporation

11.8. Guardant Health, Inc.

11.9. Foundation Medicine, Inc.

11.10. Natera, Inc.

11.11. NeoGenomics Laboratories, Inc.

11.12. Veracyte, Inc.

11.13. Tempus Labs, Inc.

11.14. BGI Group

11.15. Caris Life Sciences

11.16. Personalis, Inc.

11.17. Burning Rock Biotech Limited

11.18. Fulgent Genetics, Inc.

11.19. NanoString Technologies, Inc.

12. Appendix

Published Date: Jan-2025

Published Date: Feb-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates