Resources

About Us

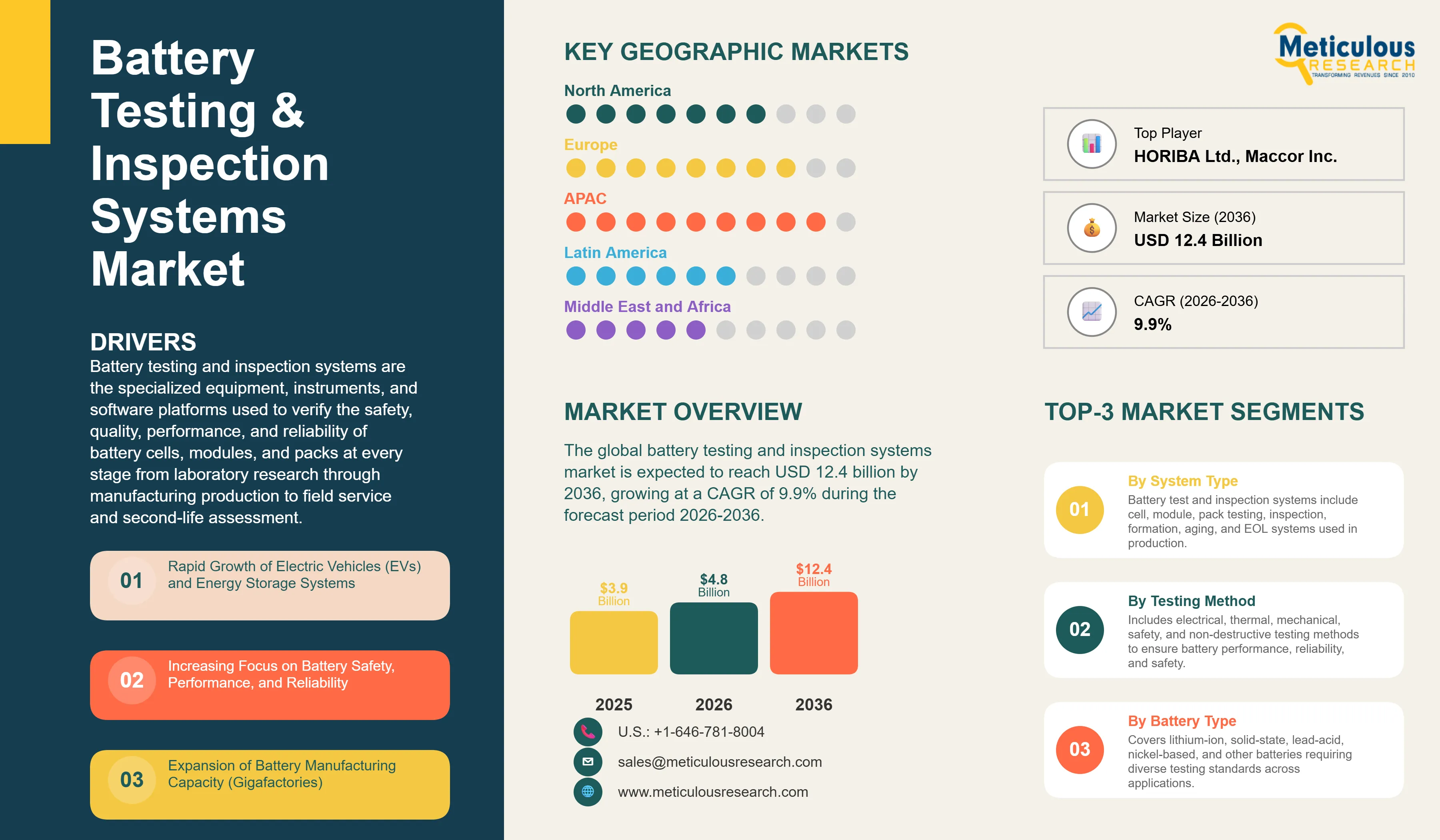

The global battery testing and inspection systems market was valued at USD 3.9 billion in 2025. This market is expected to reach USD 12.4 billion by 2036 from an estimated USD 4.8 billion in 2026, growing at a CAGR of 9.9% during the forecast period 2026-2036. According to the IEA's Global EV Outlook 2025, global EV sales reached 17-18 million in 2024, and the associated battery manufacturing industry is scaling at an extraordinary pace, with BloombergNEF's 2024 Battery Market Outlook projecting that global lithium-ion battery manufacturing capacity will reach over 6,000 GWh annually by 2030, more than six times the 2022 capacity. Every gigawatt-hour of battery production requires substantial investment in testing and inspection systems throughout the manufacturing process.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Battery testing and inspection systems are the specialized equipment, instruments, and software platforms used to verify the safety, quality, performance, and reliability of battery cells, modules, and packs at every stage from laboratory research through manufacturing production to field service and second-life assessment. A single lithium-ion battery cell destined for an electric vehicle must pass dozens of test steps before it is approved for assembly into a module: capacity measurement, internal resistance testing, formation cycling where the cell is charged and discharged to activate its electrochemical structure, X-ray inspection for internal defects, dimensional checking, and final end-of-line electrical verification before shipment. At module and pack level, additional tests verify that the individual cells are balanced, that the battery management system operates correctly, and that the completed assembly is electrically and thermally safe under a range of operating conditions including overcharge, over-discharge, and high temperature.

The market is growing rapidly because battery manufacturing is one of the fastest-scaling industrial sectors in the world. According to BloombergNEF and supporting market research, global lithium‑ion battery manufacturing capacity exceeded 2,500 GWh in 2025, with a pipeline under construction or planned in the several‑thousand‑gigawatt‑hour range, representing an extraordinary expansion of production infrastructure that each carries very significant testing‑equipment investment requirements. In parallel, global EV sales reached 21 million units in 2025 and are projected to reach around 22.7 million in 2026, further reinforcing demand for battery‑capacity and diagnostic‑test infrastructure. According to the IEA's Critical Minerals Market Review 2024, the cost of battery quality failures is a major driver of testing investment: a recalled EV battery pack carrying hundreds of cells can cost tens of thousands of dollars to replace, and a safety-critical battery failure in the field carries reputational, regulatory, and liability risks that dwarf the cost of the testing systems that could have prevented it. The combination of rapidly scaling production volumes, very high per-unit value, and severe consequences of quality failures creates a compelling investment case for comprehensive testing and inspection at every production step.

Two emerging opportunities are broadening the market beyond its primary gigafactory focus. The development of solid-state batteries, which offer potentially superior energy density and safety compared with liquid-electrolyte lithium-ion cells, requires fundamentally different testing approaches because conventional electrochemical characterization methods must be adapted for solid-state electrolytes, and new non-destructive inspection techniques are needed to detect the solid-solid interface defects that are the primary failure mode of these cells. The second-life battery market, where EV battery packs that have degraded below automotive performance thresholds are repurposed for stationary energy storage applications, is creating growing demand for battery diagnostic and grading systems that can rapidly assess the remaining capacity, power capability, and health of a used battery pack.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 12.4 Billion |

|

Market Size in 2026 |

USD 4.8 Billion |

|

Market Size in 2025 |

USD 3.9 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 9.9% |

|

Dominating System Type |

Battery Test Systems |

|

Fastest Growing System Type |

Inline Inspection Systems (EOL Testing) |

|

Dominating Testing Method |

Electrical Testing |

|

Fastest Growing Testing Method |

Non-Destructive Testing (NDT) |

|

Dominating Battery Type |

Lithium-Ion Batteries |

|

Fastest Growing Battery Type |

Solid-State Batteries |

|

Dominating Application |

Automotive |

|

Fastest Growing Application |

Energy Storage Systems (ESS) |

|

Dominating End User |

Battery Manufacturers |

|

Fastest Growing End User |

Automotive OEMs |

|

Dominating Automation Level |

Semi-Automated Systems |

|

Fastest Growing Automation Level |

Fully Automated Systems |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Gigafactory Construction Wave Generating Multi-Billion Dollar Testing Equipment Programs

The global battery gigafactory construction boom is the primary driver of testing and inspection systems market growth, as each new large-scale manufacturing facility requires a complete complement of testing equipment covering every production step from cell formation to pack end-of-line. According to BloombergNEF’s 2024 Battery Market Outlook, more than 300 lithium‑ion battery‑gigafactory projects have been announced globally, with combined capacity projected to reach several thousand gigawatt‑hours by 2030, representing a roughly six‑fold expansion from 2022 levels. While not all of these announced projects will be built on schedule, even a fraction of this pipeline represents an enormous procurement opportunity for testing equipment suppliers.

The testing equipment investment per gigawatt-hour of battery production capacity is substantial. Industry estimates suggest that testing and inspection equipment accounts for approximately 5 to 8% of total gigafactory capital expenditure, meaning that a 50 GWh battery gigafactory might invest USD 200 to USD 400 million or more in testing systems alone across formation cycling equipment, X-ray inspection, electrical characterization, and end-of-line validation systems. The major gigafactory development programs in Europe, including Northvolt's facilities in Sweden and Germany, ACC's facilities in France and Germany backed by Stellantis, TotalEnergies, and Mercedes-Benz, and the CATL and BYD European plants under development, represent very large individual testing equipment procurement programs. In North America, the cell manufacturing facilities being built by Panasonic, LG Energy Solution, Samsung SDI, and SK On in partnership with GM, Ford, and Stellantis under the U.S. Inflation Reduction Act's domestic manufacturing incentives represent another large procurement wave currently underway.

X-ray and CT Inspection Becoming Standard for Battery Quality Assurance

Industrial X-ray and computed tomography inspection systems have evolved from specialized research tools to essential inline quality assurance equipment in battery manufacturing over the past five years, driven by the discovery that internal battery defects including electrode misalignment, metallic particle contamination, and lithium plating that are invisible from external visual inspection can cause thermal runaway safety incidents months or years after manufacture. According to a 2024 review published in the Journal of Power Sources, lithium plating on graphite anodes, which occurs when cells are charged too rapidly or at low temperatures, can result in lithium dendrite growth that eventually penetrates the separator and causes an internal short circuit. This failure mode, which has been identified as a contributing factor in several high-profile EV battery fire incidents, can only be detected non-destructively through X-ray or CT imaging that reveals the internal electrode structure.

Companies including Zeiss, Nikon Metrology, and Baker Hughes have developed industrial CT systems specifically for battery cell inspection that can scan individual cells at production line speeds, detecting particle contamination, electrode edge defects, and winding irregularities that are the precursors of cell failure. Chroma ATE and Hioki have integrated X-ray inspection capabilities into their battery testing platforms. According to the German Association of the Automotive Industry (VDA), battery quality standards for automotive applications now typically require 100% inline X-ray inspection of cells destined for EV battery packs, meaning every cell in a production run must pass through X-ray inspection before it is accepted for module assembly, driving very large installed equipment requirements at scale production facilities.

EU Battery Regulation Mandating Comprehensive Testing and Data Transparency

The European Union's Battery Regulation, which entered into force in August 2023 and is being implemented in stages through to 2027 and beyond, is the world's most comprehensive legislative framework for battery safety, sustainability, and traceability, and its requirements are directly driving significant investment in testing and inspection systems across the entire battery supply chain. The regulation requires battery manufacturers to provide a battery passport documenting the performance and safety parameters of every EV battery placed on the EU market, including capacity, power capability, state of health, and carbon footprint data. This battery passport requirement creates a mandatory data infrastructure that requires comprehensive testing and data logging at every production step.

According to the European Battery Alliance, the EU Battery Regulation's minimum performance threshold requirements for EV batteries and the requirement for third-party verification of compliance are driving investment in standardized testing protocols and accredited testing laboratory capacity across Europe. The regulation also introduces due diligence requirements for battery raw materials and end-of-life collection and recycling obligations that will drive investment in used battery assessment systems for sorting, grading, and repurposing end-of-life batteries. TUV Rheinland, Intertek, and Bureau Veritas have all reported growing demand for battery certification and testing services in response to the EU Battery Regulation requirements, indicating that the regulatory framework is already generating measurable commercial activity in the testing and inspection services market.

Expansion of Battery Manufacturing Capacity (Gigafactories)

The global battery manufacturing scale-up is the single most powerful demand driver for battery testing and inspection systems, as each new production facility represents a defined and large procurement program for testing equipment. According to BloombergNEF’s Battery Market Outlook 2024, global announced battery manufacturing capacity reached the multi‑thousand‑gigawatt‑hour range by 2024, driven by EV demand growth and government incentives for domestic battery production in the U.S. under the IRA, in Europe under the EU’s Net Zero Industry Act, and in China under its national energy‑security and NEV‑development programs. The U.S. Inflation Reduction Act's Section 45X advanced manufacturing tax credits for battery cells and modules manufactured domestically have triggered a wave of cell manufacturing investment in the U.S., with Panasonic, LG Energy Solution, Samsung SDI, and others building or expanding U.S. facilities that each require substantial formation cycling, electrical testing, and inspection system investments. Formation cycling equipment alone, which is used to charge and discharge newly assembled battery cells through their first activation cycles and accounts for a very large share of total gigafactory floor space and capital investment, represents a major procurement category within the testing systems market.

Increasing Focus on Battery Safety, Performance, and Reliability

Battery safety failures in electric vehicles and consumer electronics have been high-profile, costly, and commercially damaging events that have created very strong financial and regulatory motivation across the entire battery supply chain to invest in comprehensive testing that prevents defective batteries from reaching consumers. Multiple EV battery fire incidents and recalls have reinforced the industry's awareness that battery safety testing investment is not optional. According to the National Highway Traffic Safety Administration's recall database, battery-related EV recalls have been among the most costly in the automotive industry in recent years, with individual recall programs affecting hundreds of thousands of vehicles and costing hundreds of millions of dollars in replacement and remediation costs that in every case significantly exceeded the testing investment that could have prevented the underlying defect from entering production.

Automation and AI in Testing and Inspection

The integration of automation and artificial intelligence into battery testing and inspection systems is creating a new generation of highly productive, data-rich testing platforms that can significantly improve both the speed and sensitivity of quality assurance in high-volume battery manufacturing. A fully automated inline inspection system that combines machine vision, X-ray imaging, and AI-based defect classification can inspect hundreds of cells per minute with defect detection sensitivity that exceeds manual inspection while generating structured data from every inspected cell that feeds into process control and quality management systems. AI models trained on large datasets of cell images and their subsequent field performance outcomes can identify subtle visual or structural features that are precursors of future failure, enabling earlier detection of quality issues that become apparent only as batteries age in the field. Keysight Technologies has been developing AI-enhanced battery testing platforms, and Chroma ATE's automated battery testing systems incorporate intelligent data analysis capabilities that provide real-time feedback to the manufacturing process as well as comprehensive traceability data for each tested cell.

Expansion in Second-Life Battery Testing

The growing population of EV batteries reaching end-of-automotive-life is creating a new and commercially significant market for battery assessment and grading systems that can efficiently evaluate the remaining performance characteristics of used battery packs and classify them for second-life energy storage applications. EV battery packs typically retain approximately 70–80% of their original capacity after 8–10 years of use or ~150,000–200,000 kilometers, making them suitable for less demanding applications such as grid storage, residential energy systems, and industrial backup power. This residual value is driving the emergence of structured second-life battery ecosystems. According to Circular Energy Storage (2024), the global second-life EV battery market is expected to reach approximately 150–200 GWh of annual volume by 2030, supported by the rapid growth of EV adoption and the increasing number of batteries retiring from first-life applications.

This trend is creating strong demand for high-throughput battery testing, diagnostics, and grading systems capable of assessing state-of-health (SoH), safety, and remaining useful life at scale. Efficient batch testing technologies are becoming critical to enabling economically viable second-life deployment, as cost, speed, and accuracy of battery evaluation directly determine the commercial feasibility of repurposing used EV batteries.

By System Type: In 2026, Battery Test Systems to Dominate

Based on system type, the global battery testing and inspection systems market is segmented into battery test systems (cell, module, and pack), inspection systems (visual, X-ray/CT, and ultrasonic), formation and aging test systems, and end-of-line testing systems. In 2026, the battery test systems segment is expected to account for the largest share of the global battery testing and inspection systems market. Electrical characterization systems for capacity measurement, internal resistance testing, and charge-discharge cycling are required at every level of battery assembly from individual cells through to complete packs, and the very large installed base of these systems at battery manufacturers, automotive OEMs, and research institutions makes this the dominant segment by revenue. Arbin Instruments, Bitrode, and Maccor are leading suppliers of cell and module level test systems, while Keysight Technologies and Chroma ATE serve both R&D and production testing markets with high-performance electrical characterization systems.

However, the end-of-line testing systems segment is projected to register the highest CAGR during the forecast period. The scaling of gigafactory production volumes to millions of cells per day is creating strong demand for high-throughput EOL testing systems that can verify every completed cell or pack against final quality specifications at production line speeds. The requirement for 100% EOL testing of EV battery cells in automotive-grade production, combined with the scale of production at new gigafactories, is generating large procurement programs for EOL testing infrastructure that is growing faster than the broader testing systems market.

By Testing Method: In 2026, Electrical Testing to Hold the Largest Share

Based on testing method, the global battery testing and inspection systems market is segmented into electrical testing (capacity, internal resistance, and charge-discharge cycling), thermal testing, mechanical testing, safety testing, and non-destructive testing. In 2026, the electrical testing segment is expected to account for the largest share of the global battery testing and inspection systems market. Electrical characterization tests are the most fundamental and universally applied battery test category, required from early cell development through to production end-of-line and field service assessment. Every battery cell and pack must pass electrical performance tests as the primary verification of its fitness for use, making electrical testing the core revenue category in the market.

However, the non-destructive testing segment is projected to register the highest CAGR during the forecast period. The growing adoption of X-ray, CT, and ultrasonic inspection for 100% inline inspection of automotive-grade battery cells, driven by both regulatory requirements and the industry's experience with internal defect-related safety incidents, is creating rapidly growing demand for NDT equipment in gigafactory production lines. The German automotive industry's VDA standard requiring 100% X-ray inspection of EV battery cells represents an important adoption trigger that is pulling NDT investment into mainstream battery production.

By Application: In 2026, Automotive to Hold the Largest Share

Based on application, the global battery testing and inspection systems market is segmented into automotive (EV and HEV), energy storage systems (grid and residential), consumer electronics, industrial applications, aerospace and defense, and other applications. In 2026, the automotive segment is expected to account for the largest share of the global battery testing and inspection systems market. EV battery manufacturing for passenger cars and commercial vehicles is by far the largest single driver of battery testing equipment investment, reflecting the very high per-pack value of automotive batteries, the very stringent safety and performance requirements of automotive applications, and the enormous scale of EV battery production ramp-up currently underway globally. According to the IEA, global EV sales reached 17-18 million in 2024 and are projected to grow substantially, with each vehicle requiring a thoroughly tested battery pack.

However, the energy storage systems segment is projected to register the highest CAGR during the forecast period. Grid-scale and residential battery storage is growing very rapidly as the cost of battery systems falls and as renewable energy penetration creates growing demand for energy storage to manage supply variability. According to BloombergNEF's Energy Storage Market Outlook 2024, global energy storage installations are expected to grow sixfold from 2023 to 2030. Each storage system deployment requires battery testing for commissioning, performance verification, and ongoing health monitoring, creating growing demand for energy storage-specific testing systems alongside the large automotive testing market.

Battery Testing & Inspection Systems Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global battery testing and inspection systems market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global battery testing and inspection systems market. The region's dominance reflects the extraordinary concentration of global battery cell manufacturing in China, South Korea, and Japan. China's State Grid and BYD are also leading developers of grid-scale energy storage, adding further battery testing equipment demand from the storage sector. South Korea's LG Energy Solution, Samsung SDI, and SK On are the world's third, fourth, and fifth-largest EV battery manufacturers respectively according to SNE Research, with major manufacturing facilities in South Korea and internationally that represent significant ongoing testing equipment investment programs. Japan hosts Panasonic and the Panasonic-Tesla collaborative battery manufacturing, alongside leading precision testing equipment manufacturers including Hioki E.E. Corporation and Advantest Corporation, which serve both domestic and global battery manufacturing customers.

However, the European battery testing and inspection systems market is expected to grow at the fastest CAGR during the forecast period. Europe's battery testing market growth is being driven by two powerful converging forces: the very large wave of gigafactory construction underway across the continent, and the EU Battery Regulation's comprehensive testing and data transparency requirements that mandate systematic testing documentation across the entire battery lifecycle. Northvolt's gigafactory in Sweden, CATL's plant under construction in Hungary, ACC's facilities in France and Germany, and the anticipated Volkswagen and Mercedes-Benz in-house cell manufacturing facilities collectively represent billions of euros of capital investment that each requires substantial testing equipment procurement programs. The EU Battery Regulation's battery passport requirement, which mandates comprehensive performance and safety data for every EV battery placed on the EU market, is creating additional systematic testing infrastructure investment beyond what pure production quality assurance would require. TUV Rheinland, headquartered in Germany, and Intertek have both cited growing battery certification demand in their recent financial communications as the EU Battery Regulation creates new mandatory third-party verification requirements.

North America is a rapidly growing battery testing market, accelerating significantly following the Inflation Reduction Act's domestic battery manufacturing incentives that have triggered a wave of U.S. cell manufacturing investments. Keysight Technologies and Arbin Instruments, both headquartered in the United States, are leading global battery testing equipment suppliers with strong domestic and international customer bases. The U.S. Department of Energy's national laboratory network, including Argonne National Laboratory and the National Renewable Energy Laboratory, maintains significant battery testing infrastructure for research and development that generates ongoing equipment procurement. Latin America and the Middle East and Africa are earlier-stage markets for battery testing equipment, primarily driven by the testing requirements of imported EV batteries and growing energy storage deployments rather than domestic cell manufacturing.

The battery testing and inspection systems market is served by precision instrument companies with deep electrochemical characterization expertise, industrial testing equipment companies serving the broader electronics and automotive manufacturing sectors, and specialist battery testing system developers focused specifically on this growing market. Competition is based on testing throughput and accuracy specifications, system integration capability with production line automation, software data management and analytics capabilities, ability to support multiple battery chemistries and form factors, and the depth of applications engineering support for customer-specific testing program development.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' testing system portfolios, gigafactory customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global battery testing and inspection systems market include Keysight Technologies Inc. (U.S.), Chroma ATE Inc. (Taiwan), Hioki E.E. Corporation (Japan), HORIBA Ltd. (Japan), AVL List GmbH (Austria), Arbin Instruments (U.S.), Bitrode Corporation (U.S.), National Instruments/NI (U.S.), AMETEK Inc. (U.S.), Maccor Inc. (U.S.), TUV Rheinland Group (Germany), Intertek Group plc (UK), FEV Group GmbH (Germany), Advantest Corporation (Japan), and Kistler Group (Switzerland), among others.

The global battery testing and inspection systems market is expected to reach USD 12.4 billion by 2036 from an estimated USD 4.8 billion in 2026, at a CAGR of 9.9% during the forecast period 2026-2036.

In 2026, the battery test systems segment is expected to hold the largest share of the global battery testing and inspection systems market.

The end-of-line testing systems segment is projected to register the highest CAGR during the forecast period.

The EU Battery Regulation, which entered into force in August 2023 and is being implemented through to 2027, mandates battery passports with comprehensive performance and safety data for every EV battery placed on the EU market, and requires third-party verification of compliance. According to TUV Rheinland and Intertek's recent financial communications, this is already generating measurable growth in battery certification and testing services demand, creating systematic testing infrastructure investment across Europe beyond what production quality assurance alone would require.

The market is primarily driven by the global gigafactory construction wave, each requiring comprehensive testing equipment investment. The commercial and safety consequences of battery failures, illustrated by recalls costing billions of dollars, make testing system investment highly compelling for manufacturers, and the EU Battery Regulation is creating additional mandatory testing and documentation requirements across the European market.

Key players are Keysight Technologies Inc. (U.S.), Chroma ATE Inc. (Taiwan), Hioki E.E. Corporation (Japan), HORIBA Ltd. (Japan), AVL List GmbH (Austria), Arbin Instruments (U.S.), Bitrode Corporation (U.S.), National Instruments/NI (U.S.), AMETEK Inc. (U.S.), Maccor Inc. (U.S.), TUV Rheinland Group (Germany), Intertek Group plc (UK), FEV Group GmbH (Germany), Advantest Corporation (Japan), and Kistler Group (Switzerland), among others.

Europe is expected to register the highest growth rate in the global battery testing and inspection systems market during the forecast period 2026-2036. The combination of the large wave of gigafactory construction underway in Sweden, Hungary, France, Germany, and other European countries, and the EU Battery Regulation's mandatory testing and battery passport requirements, creates a uniquely powerful dual demand driver for battery testing investment that is expected to sustain Europe's above-average market growth throughout the forecast period.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rapid Growth of Electric Vehicles (EVs) and Energy Storage Systems

4.2.1.2 Increasing Focus on Battery Safety, Performance, and Reliability

4.2.1.3 Expansion of Battery Manufacturing Capacity (Gigafactories)

4.2.1.4 Stringent Regulatory Standards for Battery Testing

4.2.2 Restraints

4.2.2.1 High Cost of Advanced Testing Equipment

4.2.2.2 Complexity in Testing Next-Generation Batteries

4.2.2.3 Long Testing Cycles for Lifecycle Validation

4.2.3 Opportunities

4.2.3.1 Growth in Solid-State and Advanced Battery Technologies

4.2.3.2 Automation and AI in Testing and Inspection

4.2.3.3 Expansion in Second-Life Battery Testing

4.2.3.4 Increasing Demand for Inline Inspection Systems

4.2.4 Challenges

4.2.4.1 Standardization Across Battery Chemistries

4.2.4.2 Data Management and Analysis Complexity

4.3 Technology Landscape

4.3.1 Electrical Testing Systems

4.3.2 Thermal Testing and Environmental Chambers

4.3.3 Non-Destructive Testing (NDT) Technologies

4.3.4 Machine Vision and AI-Based Inspection

4.3.5 Battery Management System (BMS) Testing

4.4 Battery Testing Ecosystem

4.4.1 Battery Cell and Pack Manufacturers

4.4.2 Testing Equipment Providers

4.4.3 System Integrators

4.4.4 Automotive OEMs and Energy Companies

4.4.5 Certification and Regulatory Bodies

4.5 Value Chain Analysis

4.5.1 Raw Material Suppliers

4.5.2 Battery Manufacturers

4.5.3 Testing Equipment Providers

4.5.4 Integrators and Service Providers

4.5.5 End Users

4.6 Regulatory and Standards Landscape

4.6.1 Battery Safety Standards (UN 38.3, IEC, UL)

4.6.2 Automotive and EV Regulations

4.6.3 Environmental and Recycling Regulations

4.7 Porter’s Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Expansion of Gigafactories

4.8.2 Growth in EV Ecosystem Investments

4.8.3 Increasing Automation in Battery Production

5. Battery Testing & Inspection Systems Market, by System Type

5.1 Introduction

5.2 Battery Test Systems

5.2.1 Cell Testing Systems

5.2.2 Module Testing Systems

5.2.3 Pack Testing Systems

5.3 Inspection Systems

5.3.1 Visual Inspection Systems

5.3.2 X-ray and CT Inspection Systems

5.3.3 Ultrasonic Inspection Systems

5.4 Formation and Aging Test Systems

5.5 End-of-Line (EOL) Testing Systems

6. Battery Testing & Inspection Systems Market, by Testing Method

6.1 Introduction

6.2 Electrical Testing

6.2.1 Capacity Testing

6.2.2 Internal Resistance Testing

6.2.3 Charge/Discharge Cycling

6.3 Thermal Testing

6.4 Mechanical Testing

6.5 Safety Testing

6.6 Non-Destructive Testing (NDT)

7. Battery Testing & Inspection Systems Market, by Battery Type

7.1 Introduction

7.2 Lithium-Ion Batteries

7.3 Solid-State Batteries

7.4 Lead-Acid Batteries

7.5 Nickel-Based Batteries

7.6 Other Battery Types

8. Battery Testing & Inspection Systems Market, by Application

8.1 Introduction

8.2 Automotive

8.2.1 Electric Vehicles (EVs)

8.2.2 Hybrid Electric Vehicles (HEVs)

8.3 Energy Storage Systems (ESS)

8.3.1 Grid Storage

8.3.2 Residential Storage

8.4 Consumer Electronics

8.5 Industrial Applications

8.6 Aerospace and Defense

8.7 Other Applications

9. Battery Testing & Inspection Systems Market, by End User

9.1 Introduction

9.2 Battery Manufacturers

9.3 Automotive OEMs

9.4 Electronics Manufacturers

9.5 Research and Testing Laboratories

10. Battery Testing & Inspection Systems Market, by Automation Level

10.1 Introduction

10.2 Manual Systems

10.3 Semi-Automated Systems

10.4 Fully Automated Systems

11. Battery Testing & Inspection Systems Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Australia

11.4.6 Indonesia

11.4.7 Thailand

11.4.8 Vietnam

11.4.9 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Egypt

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Keysight Technologies, Inc.

13.2 Chroma ATE Inc.

13.3 Hioki E.E. Corporation

13.4 HORIBA, Ltd.

13.5 AVL List GmbH

13.6 Arbin Instruments

13.7 Bitrode Corporation

13.8 National Instruments (NI)

13.9 AMETEK, Inc.

13.10 Maccor, Inc.

13.11 TÜV Rheinland Group

13.12 Intertek Group plc

13.13 FEV Group GmbH

13.14 Advantest Corporation

13.15 Kistler Group

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Feb-2024

Subscribe to get the latest industry updates