Resources

About Us

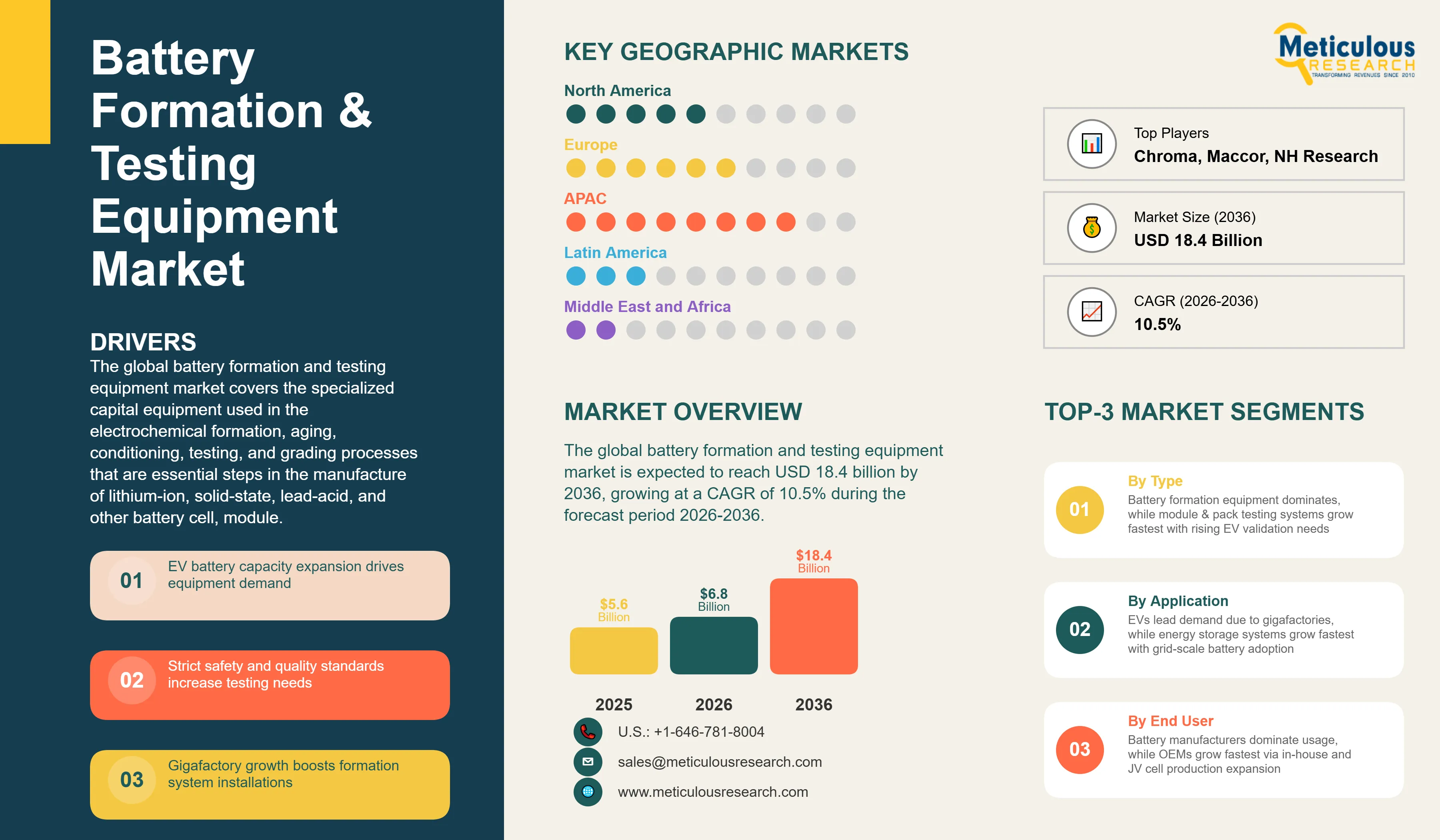

The global battery formation and testing equipment market was valued at USD 5.6 billion in 2025. This market is expected to reach USD 18.4 billion by 2036 from an estimated USD 6.8 billion in 2026, growing at a CAGR of 10.5% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

The global battery formation and testing equipment market covers the specialized capital equipment used in the electrochemical formation, aging, conditioning, testing, and grading processes that are essential steps in the manufacture of lithium-ion, solid-state, lead-acid, and other battery cell, module, and pack products. This encompasses battery formation chargers and dischargers that apply controlled charge-discharge cycling to activate the solid-electrolyte interphase layer in newly assembled cells, aging and conditioning chambers, electrical and safety testing systems that verify capacity, cycle life, internal resistance, and safety performance, environmental testing equipment, and the module and pack-level testing platforms required for battery management system validation and complete pack performance verification.

The growth of the global battery formation and testing equipment market is primarily driven by the extraordinary global expansion of EV battery manufacturing capacity, with hundreds of gigawatt-hours of new cell production capacity being commissioned at gigafactories across China, Europe, and North America that each require large-scale formation and testing equipment installations to commission and operate their production lines. The increasingly stringent quality, safety, and performance standards being applied to automotive-grade lithium-ion batteries by OEM customers and regulatory bodies are intensifying the testing and quality assurance requirements per manufactured cell, driving higher investment in both the quantity and capability of testing equipment per unit of production capacity.

Two significant opportunities are shaping the market's long-term trajectory. The development and commercialization of fast formation technologies that can reduce the formation cycle time from the current 6 to 24 hours required by conventional formation protocols to 1 to 4 hours through advanced charging algorithms and formation chamber optimization represents the highest-value efficiency opportunity in battery manufacturing, as formation currently accounts for 30 to 40% of total battery cell production time and is therefore a critical bottleneck in gigafactory throughput capacity. The integration of AI-based battery testing and diagnostics platforms that apply machine learning to formation and testing data to predict cell-level capacity, cycle life, and safety performance with greater accuracy and speed than conventional test protocols represents a transformative quality improvement opportunity that leading battery manufacturers are actively adopting to reduce testing time and improve end-of-line quality assurance.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 18.4 Billion |

|

Market Size in 2026 |

USD 6.8 Billion |

|

Market Size in 2025 |

USD 5.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.5% |

|

Dominating Equipment Type |

Battery Formation Equipment |

|

Fastest Growing Equipment Type |

Module & Pack Testing Equipment |

|

Dominating Battery Chemistry |

Lithium-Ion Batteries |

|

Fastest Growing Battery Chemistry |

Solid-State Batteries |

|

Dominating Battery Format |

Prismatic Cells |

|

Fastest Growing Battery Format |

Cylindrical Cells |

|

Dominating Application |

Electric Vehicles (EVs) |

|

Fastest Growing Application |

Energy Storage Systems (ESS) |

|

Dominating Automation Level |

Semi-Automated Systems |

|

Fastest Growing Automation Level |

Fully Automated Systems |

|

Dominating End User |

Battery Manufacturers (Cell Manufacturers) |

|

Fastest Growing End User |

OEMs (Automotive, Electronics) |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Transition Toward Fast Formation Technologies

The development and commercial adoption of fast formation protocols that dramatically reduce the electrochemical formation cycle time for lithium-ion cells is the highest-impact process innovation trend in the battery manufacturing equipment market. Conventional formation cycling requires 6 to 24 hours of controlled charge-discharge at moderate C-rates to properly develop the solid-electrolyte interphase layer on graphite anode surfaces, and this extended cycle time makes formation the single largest bottleneck in high-volume battery cell production, requiring the largest equipment floor space investment and representing the greatest constraint on gigafactory throughput capacity relative to capital invested. Fast formation approaches including high-temperature formation that accelerates SEI development kinetics, multi-step current profile optimization that achieves equivalent SEI quality in 1 to 4 hours, and advanced electrolyte formulations engineered for rapid SEI formation are all being pursued by equipment developers and battery manufacturers as pathways to reducing formation cycle time by 70 to 90% relative to conventional protocols.

Equipment vendors including Chroma ATE, PEC Group, and Digatron are developing next-generation formation systems specifically engineered to support fast formation protocols with precision temperature control, higher-accuracy current delivery, and advanced data acquisition capabilities that enable the detailed formation process monitoring required to validate fast formation SEI quality equivalence to conventional protocols. The commercial value of fast formation equipment is very high for gigafactory operators, as reducing formation time from 12 hours to 2 hours on a 40 GWh annual production line can eliminate hundreds of millions of dollars in working capital tied up in in-process inventory and free formation chamber floor space for additional production capacity without proportional capital expansion.

Integration of AI and Data Analytics in Battery Testing

The integration of artificial intelligence and machine learning into battery formation and testing workflows represents a transformative capability upgrade that is enabling battery manufacturers to extract far greater quality, performance, and predictive insight from the large volumes of electrochemical data generated during formation and testing processes than conventional statistical analysis methods can provide. AI models trained on large datasets of formation process data and long-term cycle life test results can predict individual cell capacity retention and cycle life from the pattern of voltage, current, and temperature signatures observed during the first few formation cycles with accuracy that reduces the need for time-consuming long-duration cycle life testing, enabling production quality screening decisions to be made earlier in the manufacturing process and reducing the time between cell production and quality release for shipment.

Machine learning-based anomaly detection applied to real-time formation process data can identify cells with incipient defects including lithium plating, separator damage, and electrode coating non-uniformity from formation curve deviations that are imperceptible to conventional threshold-based monitoring, enabling earlier identification and removal of defective cells before they progress to safety-relevant failure modes. Keysight Technologies, AVL List GmbH, and National Instruments are among the established test and measurement companies incorporating AI analytics capabilities into their battery test platform offerings, while a growing ecosystem of battery analytics software companies including Voltaiq and Battery Intelligence are providing cloud-based AI analytics platforms that can be integrated with formation and testing equipment data outputs from multiple equipment vendors.

Scaling of Module and Pack Testing for Automotive Qualification

The rapid growth of automotive-grade battery pack manufacturing for electric vehicles is driving a significant expansion of the module and pack testing equipment market, as OEM qualification and homologation requirements mandate comprehensive electrical, thermal, mechanical, and safety testing of complete battery packs to the most demanding test standards including UN38.3, IEC 62660, and automotive OEM-specific qualification protocols before any battery pack design can be approved for vehicle production. Module and pack-level testing requires significantly larger and more powerful test equipment than cell-level testing, including high-current cyclers capable of 400 to 1,000 ampere charge-discharge, large thermal management chambers able to temperature-cycle complete battery packs, vibration and mechanical shock test systems, and battery management system test platforms that simulate vehicle BMS communication and control environments.

The increasing number of new EV battery pack designs entering automotive qualification testing as the global EV model lineup expands and battery chemistry and format transitions occur is generating growing demand for high-capability module and pack test equipment. AVL List GmbH, Keysight Technologies, NH Research, and Bitrode Corporation are among the established players serving the automotive battery pack testing market with high-power, highly configurable pack test systems. The transition of battery pack testing from purely safety and regulatory compliance verification toward comprehensive performance characterization that informs vehicle range, charging curve, and thermal management system design is extending the scope and duration of pack test programs and expanding the test equipment market per battery pack design program.

Rapid Expansion of EV Battery Manufacturing

The primary driver of the global battery formation and testing equipment market is the unprecedented global expansion of electric vehicle battery cell manufacturing capacity, with the International Energy Agency projecting that global EV battery manufacturing capacity will need to reach approximately 9,000 GWh per year by 2030 to support the EV adoption trajectories required for net-zero emission scenarios, representing a roughly tenfold increase from the approximately 900 GWh of capacity operational in 2024. Each gigawatt-hour of new lithium-ion cell production capacity requires the installation of battery formation and testing equipment estimated at USD 5 to 12 million per GWh depending on chemistry, format, and automation level, translating the projected capacity expansion into several tens of billions of dollars in formation and testing equipment procurement over the forecast period. The geographic distribution of this capacity expansion across CATL, BYD, LG Energy Solution, Samsung SDI, SK On, Panasonic, and numerous emerging battery manufacturers in China, South Korea, Europe, and North America creates a diversified and sustained formation and testing equipment procurement market that benefits both established equipment suppliers and new market entrants.

Stringent Quality and Safety Requirements

The increasingly stringent quality and safety requirements imposed on automotive-grade lithium-ion battery cells by vehicle OEM customers, government safety regulators, and the EU Battery Regulation's battery performance and durability standards are driving battery manufacturers to invest in more comprehensive, more accurate, and more automated formation and testing equipment capable of detecting the subtle cell-level defects and performance deviations that can lead to field failures, warranty claims, and safety incidents in vehicle battery packs. Automotive OEM battery qualification requirements have progressively tightened to include 100% end-of-line testing of every cell against expanding test parameter sets including capacity, internal resistance, self-discharge rate, and formation curve quality metrics, replacing the statistical sampling approaches that were previously accepted for non-automotive battery applications. The EU Battery Regulation's mandatory battery performance class labeling, minimum capacity retention and cycle life requirements for EV batteries, and digital battery passport provisions requiring traceability of battery performance data throughout the battery lifecycle are creating additional requirements for comprehensive testing data capture and retention that is driving investment in more capable and better-connected testing platforms.

Development of Fast Formation Technologies

The commercial development of fast formation equipment and processes that can reduce battery cell formation cycle time by 70 to 90% compared with conventional protocols represents the highest-value efficiency improvement opportunity available in battery manufacturing and the most compelling near-term market opportunity for formation equipment developers. The economic value of reducing formation time from 12 to 24 hours to 1 to 4 hours is very large for gigafactory operators, as formation represents 30 to 40% of total cell production cycle time and is typically the single largest constraint on production throughput per unit of factory floor area. Equipment vendors that can deliver formation systems validated to achieve equivalent or superior cell quality metrics compared with conventional formation protocols at 5 to 10 times the throughput will be able to command significant premium pricing reflecting the substantial manufacturing productivity improvement their equipment enables. The competitive race among formation equipment suppliers including Chroma ATE, PEC NV, and Digatron to commercialize fast formation solutions is creating significant R&D investment and differentiation opportunity in this equipment category through the forecast period.

Integration of AI-Based Testing and Diagnostics

The integration of artificial intelligence and machine learning into battery testing platforms creates a compelling opportunity for equipment suppliers to deliver higher-value AI-enhanced testing solutions that command premium pricing while enabling their battery manufacturer customers to achieve faster quality release, earlier defect detection, and more accurate end-of-line performance grading than conventional test approaches permit. AI-based early cycle life prediction models that can accurately predict a cell's 500-cycle or 1,000-cycle capacity retention from the electrochemical signatures of the first 3 to 10 formation cycles represent a transformative testing efficiency improvement that could enable battery manufacturers to release cells to shipment without the weeks-long long-duration cycle life test programs currently required for product qualification, potentially compressing time-to-market for new battery product launches while reducing test equipment floor space requirements per unit of production capacity. The integration of cloud-based AI analytics with formation and testing equipment data platforms creates a sustainable and high-value software and data service revenue model for equipment companies that successfully develop AI testing intelligence capabilities validated by battery manufacturer customers.

By Equipment Type: In 2026, Battery Formation Equipment to Dominate

Based on equipment type, the global battery formation and testing equipment market is segmented into battery formation equipment, battery testing equipment, battery aging and grading systems, module and pack testing equipment, and other equipment. In 2026, the battery formation equipment segment is expected to account for the largest share of the global market. The large share of this segment is attributed to formation equipment representing the single largest capital equipment investment in the battery cell manufacturing process on a cost-per-GWh basis, with formation chargers, dischargers, and formation rack systems required in very large quantities to match the throughput requirements of high-volume cell production lines. The capital cost concentration in formation equipment reflects both the high quantity of formation channels required per GWh of annual production capacity and the high precision power electronics specifications required for the accurate current delivery and voltage measurement that quality formation protocols demand.

However, the module and pack testing equipment segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the rapid expansion of automotive battery pack production requiring comprehensive OEM qualification and homologation testing, the increasing complexity of battery pack designs incorporating more cells, more sophisticated battery management systems, and higher voltage architectures that require more extensive pack-level testing, and the EU Battery Regulation's performance class labeling and traceability requirements creating new pack-level testing data capture obligations across European battery manufacturers.

By Battery Chemistry: In 2026, Lithium-Ion Batteries to Hold the Largest Share

Based on battery chemistry, the global battery formation and testing equipment market is segmented into lithium-ion batteries (LFP, NMC, NCA), solid-state batteries, lead-acid batteries, nickel-based batteries, and other chemistries. In 2026, the lithium-ion batteries segment is expected to account for the largest share of the market. Lithium-ion cells represent the dominant chemistry across the EV, energy storage, and consumer electronics application segments that together constitute the large majority of global battery production volume, and the formation and testing protocols for lithium-ion cells have been extensively optimized over decades of high-volume manufacturing to represent the commercial standard for the industry. The concentration of gigafactory investment globally in lithium-ion production across LFP for cost-sensitive applications and NMC and NCA for energy-density-prioritized applications sustains the lithium-ion segment's market dominance through the forecast period.

However, the solid-state batteries segment is projected to register the highest CAGR during the forecast period. This growth is driven by the commercial development programs of Toyota, Samsung SDI, QuantumScape, and Solid Power advancing solid-state battery production timelines that will require entirely new formation and testing equipment platforms engineered for the different electrochemical characteristics, temperature requirements, and stack pressure management needs of solid-state cell architectures. Solid-state formation processes differ fundamentally from liquid electrolyte lithium-ion formation in requiring controlled stack pressure management during SEI formation on lithium metal anodes, higher formation temperatures in some solid electrolyte systems, and specialized testing approaches for the different impedance profiles and failure modes of solid-state cells, creating a new and premium-valued equipment market segment that leading formation equipment companies are investing to address.

By Battery Format: In 2026, Prismatic Cells to Hold the Largest Share

Based on battery format, the global battery formation and testing equipment market is segmented into cylindrical cells, prismatic cells, and pouch cells. In 2026, the prismatic cells segment is expected to account for the largest share of the market. The dominance of prismatic cells reflects their extensive adoption in Chinese EV battery manufacturing, where CATL and BYD produce very large volumes of prismatic LFP and NMC cells for domestic and international EV customers, and the prismatic format's mechanical stability and efficient pack integration characteristics that have made it the preferred format for the majority of current automotive battery pack designs. Formation and testing equipment for prismatic cells must accommodate the specific dimensions and terminal configurations of prismatic cell formats and the stack pressure management requirements that prismatic cell formation best practices specify.

However, the cylindrical cells segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapid expansion of cylindrical cell production capacity for the larger-format 4680 cells being produced by Tesla, Panasonic, and multiple new entrants that represent a new generation of cylindrical cells with higher energy capacity and lower production cost per kilowatt-hour than the established 18650 and 21700 cylindrical cell formats, and by the strong adoption of cylindrical cells in emerging battery applications including e-bikes, power tools, and industrial applications alongside their established consumer electronics use.

By Application: In 2026, Electric Vehicles to Hold the Largest Share

Based on application, the global battery formation and testing equipment market is segmented into electric vehicles, energy storage systems, consumer electronics, industrial applications, and aerospace and defense. In 2026, the electric vehicles segment is expected to account for the largest share of the global battery formation and testing equipment market. EV battery production accounts for the large majority of new gigafactory capacity investment globally, and the high quality, safety, and performance standards of automotive-grade battery cells require more comprehensive and more capable formation and testing equipment per unit of production capacity than non-automotive applications, generating very high formation and testing equipment capital intensity per GWh of EV battery production. The global EV battery cell production plans of CATL, BYD, LG Energy Solution, Samsung SDI, SK On, Panasonic, and the wave of new entrant gigafactories in Europe and North America collectively represent the largest formation and testing equipment procurement pipeline in the industry.

However, the energy storage systems segment is projected to register the highest CAGR during the forecast period. This growth is driven by the accelerating global deployment of grid-scale and distributed battery storage requiring large-volume production of ESS-optimized battery cells at formation and testing quality standards that are progressively approaching automotive-grade requirements as ESS battery reliability and warranty expectations increase, and the growing manufacturing volume of residential storage systems from BYD, CATL's ESS division, Tesla Energy, and LG Energy Solution that is expanding the ESS battery production base requiring dedicated formation and testing equipment.

By Automation Level: In 2026, Semi-Automated Systems to Hold the Largest Share

Based on automation level, the global battery formation and testing equipment market is segmented into manual systems, semi-automated systems, and fully automated systems. In 2026, the semi-automated systems segment is expected to account for the largest share of the global battery formation and testing equipment market. Semi-automated formation and testing systems that automate the core electrical cycling and data acquisition processes while requiring manual cell loading, connection, and grading operations represent the dominant configuration across the current global battery manufacturing installed base, reflecting the balance between automation investment cost and labor availability that has characterized the majority of battery cell manufacturing operations, particularly in China where the combination of relatively lower labor costs and very high production volumes has made semi-automated formation and testing economically competitive with fully automated alternatives.

However, the fully automated systems segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing priority of labor cost reduction, consistent product quality, and production line integration in new gigafactory designs, the higher labor cost environments of European and North American battery manufacturing locations that make automation ROI more compelling, and the OEM customer preference for fully automated formation and testing documentation that provides complete cell-level traceability records without manual data entry errors. New gigafactory designs by CATL in Europe, LG Energy Solution in the U.S. and Poland, and Samsung SDI in Hungary and the United States are specifying fully automated formation and testing lines as standard, establishing full automation as the preferred configuration for new capacity additions.

By End User: In 2026, Battery Manufacturers to Hold the Largest Share

Based on end user, the global battery formation and testing equipment market is segmented into battery manufacturers (cell manufacturers), module and pack manufacturers, OEMs (automotive and electronics), and R&D laboratories. In 2026, the battery manufacturers segment is expected to account for the largest share of the global battery formation and testing equipment market. Cell manufacturers including CATL, BYD, LG Energy Solution, Samsung SDI, SK On, Panasonic, and AESC represent the primary procurers of battery formation and testing equipment globally, as cell manufacturing requires the largest formation and testing equipment investment per unit of production capacity and the cell manufacturing operations of the leading battery companies represent the highest-volume and highest-value equipment procurement programs in the market. CATL alone, with over 250 GWh of annual production capacity and aggressive expansion plans, represents the single largest battery formation and testing equipment customer in the world.

However, the OEMs segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing number of automotive OEMs including Volkswagen Group through its PowerCo subsidiary, General Motors through Ultium Cells joint ventures, Stellantis through its ACC joint venture, and Toyota through its Prime Planet and Prime Earth JVs that are investing in battery cell manufacturing joint ventures and captive production capabilities requiring formation and testing equipment procurement. The shift from pure battery cell procurement to joint venture cell production is expanding the formation and testing equipment customer base beyond the established tier-1 battery manufacturers to include automotive OEM-controlled production facilities with significant equipment procurement budgets.

Battery Formation & Testing Equipment Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global battery formation and testing equipment market is segmented into Asia-Pacific, Europe, North America, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global battery formation and testing equipment market. The largest share of this region is mainly due to China's dominant position as the world's largest battery cell manufacturing location, with CATL, BYD, CALB, Gotion, EVE Energy, and numerous other Chinese cell manufacturers collectively operating several hundred GWh of annual production capacity that requires proportional formation and testing equipment installation and generates the largest aggregate annual formation and testing equipment procurement volumes globally. South Korea's three major battery manufacturers, LG Energy Solution, Samsung SDI, and SK On, represent the next-largest Asia-Pacific equipment procurement base, operating large domestic manufacturing capacities and rapidly expanding international manufacturing programs in Europe and North America that are fueling equipment orders placed through their Korean headquarters procurement organizations. Japan's Panasonic, in partnership with Toyota for automotive battery production and with Tesla for Nevada gigafactory cell production, represents an important premium equipment procurement market particularly for advanced formation and testing capabilities in cylindrical cell and solid-state battery development programs.

However, the European battery formation and testing equipment market is expected to grow at the fastest CAGR during the forecast period. Europe's rapid growth is driven by the largest wave of new battery gigafactory construction in the region's history, encompassing Northvolt's Swedish gigafactory expansion, ACC's plants in France and Germany, AESC's Sunderland expansion, CATL's Erfurt and Hungary facilities, Samsung SDI's Hungary plants, LG Energy Solution's Polish expansion, and the Volkswagen PowerCo Tesla-scale gigafactory program, collectively adding hundreds of GWh of new battery production capacity to the European manufacturing landscape through the forecast period. Each of these new facilities represents a major formation and testing equipment procurement program, and the European manufacturing context with its higher automation requirements, stricter environmental and safety standards, and EU Battery Regulation quality documentation obligations is driving specification of more comprehensive and more automated formation and testing equipment per GWh of production capacity than the Asian market average.

North America is establishing a rapidly growing battery formation and testing equipment market anchored by the Ultium Cells joint ventures between General Motors and LG Energy Solution in Ohio, Michigan, and Tennessee, the Panasonic Kansas gigafactory, the AESC Tennessee facility, and the growing pipeline of U.S. battery manufacturing investments motivated by the IRA's domestic manufacturing incentives. The Canadian battery manufacturing market is developing through Volkswagen's St. Thomas Ontario gigafactory, Stellantis and LG Energy Solution's Windsor Ontario joint venture, and the growing Canadian battery supply chain investment program supported by federal manufacturing incentives.

The global battery formation and testing equipment market is moderately concentrated among a tier of established specialized equipment companies, alongside larger test and measurement companies that have expanded into the battery testing segment. Competition is focused on formation throughput and energy efficiency, current delivery accuracy, channel count per floor area, fast formation protocol capability, data management and AI analytics integration, and the application engineering support required to qualify formation and testing equipment for specific cell chemistries and formats at major battery manufacturer customers.

Chroma ATE leads the formation and testing equipment market with a comprehensive product portfolio spanning cell-level formation chargers and dischargers, automated formation and testing systems, and battery module and pack testing platforms, with strong market positions at major Asian and international battery manufacturers. PEC Group and Digatron Power Electronics are leading European formation equipment specialists with strong automotive-grade qualification credentials and growing fast formation technology development programs. Arbin Instruments, Maccor, and Bitrode Corporation are established U.S.-based battery testing equipment suppliers serving both production and R&D test applications. Keysight Technologies, National Instruments, and Hioki E.E. Corporation bring precision measurement and advanced analytics capabilities to the battery testing segment from their broader test and measurement equipment businesses.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, technology capabilities, geographic presence, and key strategic developments. Some of the key players operating in the global battery formation and testing equipment market include Chroma ATE Inc. (Taiwan), Arbin Instruments (U.S.), Neware Technology Limited (China), Bitrode Corporation (U.S.), PEC Group/PEC NV (Belgium), Digatron Power Electronics GmbH (Germany), Maccor Inc. (U.S.), Keysight Technologies (U.S.), NH Research Inc. (U.S.), Hokuto Denko Corporation (Japan), AVL List GmbH (Austria), National Instruments/NI (U.S.), Hioki E.E. Corporation (Japan), Shenzhen Bonad Instrument Co. Ltd. (China), and Kikusui Electronics Corporation (Japan), among others.

The global battery formation and testing equipment market is expected to reach USD 18.4 billion by 2036 from an estimated USD 6.8 billion in 2026, at a CAGR of 10.5% during the forecast period 2026-2036.

In 2026, the battery formation equipment segment is expected to hold the largest share of the global battery formation and testing equipment market, driven by formation equipment representing the single largest capital equipment investment in battery cell manufacturing per GWh of production capacity.

The module and pack testing equipment segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the rapid expansion of automotive battery pack production requiring comprehensive OEM qualification testing and the EU Battery Regulation's performance class labeling requirements creating new pack-level testing data obligations.

In 2026, the lithium-ion batteries segment is expected to hold the largest share of the global battery formation and testing equipment market, reflecting lithium-ion's dominant position across EV, energy storage, and consumer electronics production that represents the majority of global battery manufacturing volume.

In 2026, the electric vehicles segment is expected to hold the largest share of the global battery formation and testing equipment market, driven by EV battery production accounting for the large majority of new gigafactory capacity investment globally and the high formation and testing equipment capital intensity of automotive-grade cell production.

The growth of this market is primarily driven by the unprecedented global expansion of EV battery cell manufacturing capacity requiring large-scale formation and testing equipment installations at new and expanded gigafactories across Asia, Europe, and North America, and the increasingly stringent quality, safety, and performance standards imposed by automotive OEMs and regulators on battery cells that are intensifying testing requirements and driving investment in more capable and more comprehensive formation and testing equipment per unit of production capacity.

Key players are Chroma ATE Inc. (Taiwan), Arbin Instruments (U.S.), Neware Technology Limited (China), Bitrode Corporation (U.S.), PEC Group/PEC NV (Belgium), Digatron Power Electronics GmbH (Germany), Maccor Inc. (U.S.), Keysight Technologies (U.S.), NH Research Inc. (U.S.), Hokuto Denko Corporation (Japan), AVL List GmbH (Austria), National Instruments/NI (U.S.), Hioki E.E. Corporation (Japan), Shenzhen Bonad Instrument Co. Ltd. (China), and Kikusui Electronics Corporation (Japan), among others.

Europe is expected to register the highest growth rate in the global battery formation and testing equipment market during the forecast period 2026-2036, driven by the largest wave of new battery gigafactory construction in the region's history encompassing Northvolt, ACC, AESC, CATL, Samsung SDI, LG Energy Solution, and Volkswagen PowerCo facilities collectively adding hundreds of GWh of new battery production capacity requiring formation and testing equipment procurement.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rapid Expansion of EV Battery Manufacturing

4.2.1.2. Increasing Demand for High-Performance Batteries

4.2.1.3. Stringent Quality and Safety Requirements

4.2.1.4. Growth of Gigafactories Globally

4.2.2. Restraints

4.2.2.1. High Capital Cost of Formation Equipment

4.2.2.2. Energy-Intensive Formation Processes

4.2.2.3. Long Cycle Time in Battery Formation

4.2.3. Opportunities

4.2.3.1. Development of Fast Formation Technologies

4.2.3.2. Integration of AI-Based Testing and Diagnostics

4.2.3.3. Growth in Solid-State Battery Manufacturing

4.2.3.4. Expansion in Emerging Battery Manufacturing Regions

4.2.4. Challenges

4.2.4.1. Thermal Management During Formation

4.2.4.2. Standardization and Calibration Issues

4.3. Technology Landscape

4.3.1. Battery Formation Technologies (Conventional vs Fast Formation)

4.3.2. Battery Testing Technologies (Electrical, Thermal, Safety Testing)

4.3.3. Automation and Digitalization in Battery Manufacturing

4.3.4. AI-Based Battery Diagnostics and Predictive Analytics

4.4. Battery Manufacturing Process Integration

4.4.1. Cell Assembly Stage

4.4.2. Formation Stage

4.4.3. Aging & Conditioning Stage

4.4.4. Testing & Grading Stage

4.4.5. Module & Pack Testing

4.5. Value Chain Analysis

4.5.1. Component Suppliers (Power Electronics, Sensors)

4.5.2. Equipment Manufacturers

4.5.3. Battery Manufacturers (Cell/Module/Pack)

4.5.4. Integrators and Automation Providers

4.5.5. End Users (EV, Energy Storage, Electronics OEMs)

4.6. Regulatory and Standards Landscape

4.6.1. Battery Safety Standards (UL, IEC, ISO)

4.6.2. EV Battery Regulations

4.6.3. Environmental and Recycling Regulations

4.7. Porter's Five Forces Analysis

4.8. Investment and Capacity Expansion Analysis

4.8.1. Gigafactory Expansion Trends

4.8.2. Regional Battery Manufacturing Investments

4.8.3. Strategic Partnerships and JV Activities

4.9. Cost and Pricing Analysis

4.9.1. Equipment Cost Breakdown

4.9.2. Cost Contribution of Formation vs Testing

4.9.3. Pricing by Automation Level

5. Battery Formation & Testing Equipment Market, by Equipment Type

5.1. Introduction

5.2. Battery Formation Equipment

5.2.1. Formation Chargers/Dischargers

5.2.2. Formation Racks and Systems

5.2.3. High-Temperature/Controlled Environment Formation Systems

5.3. Battery Testing Equipment

5.3.1. Electrical Testing Equipment

5.3.1.1. Capacity Testing

5.3.1.2. Cycle Life Testing

5.3.1.3. Internal Resistance Testing

5.3.2. Safety Testing Equipment

5.3.2.1. Overcharge/Overdischarge Testing

5.3.2.2. Short Circuit Testing

5.3.2.3. Thermal Runaway Testing

5.3.3. Environmental Testing Equipment

5.3.3.1. Temperature Cycling

5.3.3.2. Humidity Testing

5.3.4. Performance Testing Equipment

5.4. Battery Aging & Grading Systems

5.4.1. Aging Chambers

5.4.2. Sorting and Grading Systems

5.5. Module & Pack Testing Equipment

5.5.1. Battery Management System (BMS) Testing

5.5.2. Pack-Level Performance Testing

5.6. Other Equipment

6. Battery Formation & Testing Equipment Market, by Battery Chemistry

6.1. Introduction

6.2. Lithium-Ion Batteries

6.2.1. LFP

6.2.2. NMC

6.2.3. NCA

6.3. Solid-State Batteries

6.4. Lead-Acid Batteries

6.5. Nickel-Based Batteries

6.6. Other Chemistries

7. Battery Formation & Testing Equipment Market, by Battery Format

7.1. Introduction

7.2. Cylindrical Cells

7.3. Prismatic Cells

7.4. Pouch Cells

8. Battery Formation & Testing Equipment Market, by Application

8.1. Introduction

8.2. Electric Vehicles (EVs)

8.3. Energy Storage Systems (ESS)

8.4. Consumer Electronics

8.5. Industrial Applications

8.6. Aerospace & Defense

9. Battery Formation & Testing Equipment Market, by Automation Level

9.1. Introduction

9.2. Manual Systems

9.3. Semi-Automated Systems

9.4. Fully Automated Systems

10. Battery Formation & Testing Equipment Market, by End User

10.1. Introduction

10.2. Battery Manufacturers (Cell Manufacturers)

10.3. Module & Pack Manufacturers

10.4. OEMs (Automotive, Electronics)

10.5. R&D Laboratories

11. Battery Formation & Testing Equipment Market, by Geography

11.1. Introduction

11.2. Asia-Pacific

11.2.1. China

11.2.2. South Korea

11.2.3. Japan

11.2.4. India

11.2.5. Taiwan

11.2.6. Singapore

11.2.7. Malaysia

11.2.8. Thailand

11.2.9. Vietnam

11.2.10. Indonesia

11.2.11. Rest of Asia-Pacific

11.3. Europe

11.3.1. Germany

11.3.2. France

11.3.3. U.K.

11.3.4. Sweden

11.3.5. Norway

11.3.6. Italy

11.3.7. Spain

11.3.8. Netherlands

11.3.9. Poland

11.3.10. Rest of Europe

11.4. North America

11.4.1. U.S.

11.4.2. Canada

11.4.3. Mexico

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Colombia

11.5.6. Rest of Latin America

11.6. Middle East & Africa

11.6.1. UAE

11.6.2. Saudi Arabia

11.6.3. South Africa

11.6.4. Turkey

11.6.5. Israel

11.6.6. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1. Chroma ATE Inc.

13.2. Arbin Instruments

13.3. Neware Technology Limited

13.4. Bitrode Corporation

13.5. PEC Group (PEC NV)

13.6. Digatron Power Electronics GmbH

13.7. Maccor, Inc.

13.8. Keysight Technologies

13.9. NH Research, Inc.

13.10. Hokuto Denko Corporation

13.11. AVL List GmbH

13.12. National Instruments (NI)

13.13. Hioki E.E. Corporation

13.14. Shenzhen Bonad Instrument Co., Ltd.

13.15. Kikusui Electronics Corporation

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Dec-2024

Subscribe to get the latest industry updates