Resources

About Us

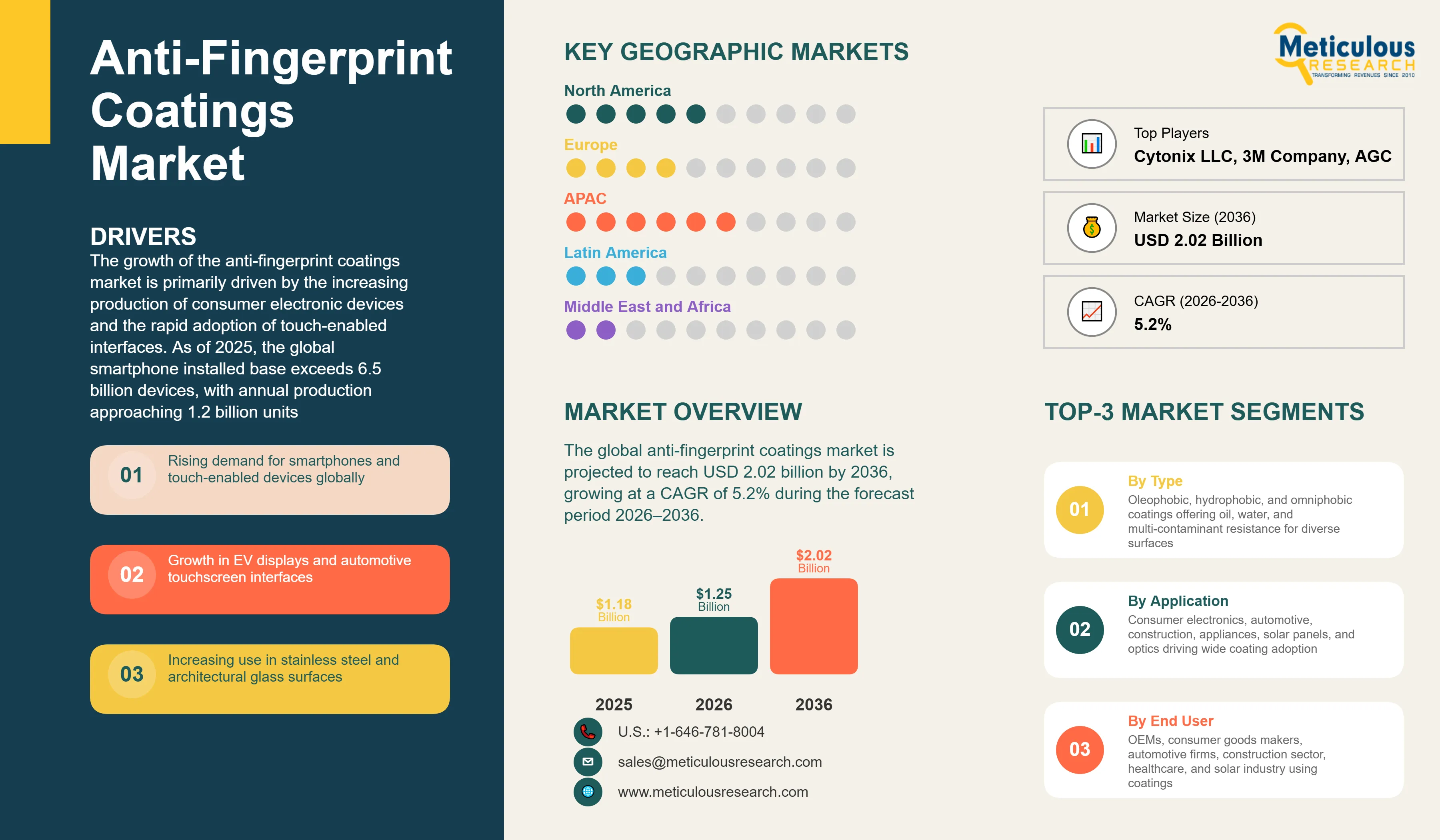

The global anti-fingerprint coatings market was valued at USD 1.18 billion in 2025. The market is projected to reach USD 2.02 billion by 2036 from an estimated USD 1.25 billion in 2026, growing at a CAGR of 5.2% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global anti-fingerprint coatings market comprises specialized coating formulations applied to surface substrates to reduce the visibility of fingerprints, smudges, sebum deposits, and oily contaminants. These coatings are widely used to maintain the aesthetic appearance, optical clarity, and tactile performance of high-touch surfaces across applications such as consumer electronics, automotive interiors, architectural glass, stainless steel appliances, optical products, and solar panels. Anti-fingerprint coatings function by modifying surface energy characteristics to create oleophobic (oil-repellent), hydrophobic (water-repellent), or omniphobic interfaces, thereby minimizing the adhesion of oily substances such as skin lipids and enabling easy removal of residues.

The market includes multiple coating chemistries, such as fluoropolymer-based formulations, silicone-based organosiloxane coatings, UV-curable acrylates, and inorganic sol-gel systems. Among these, fluoropolymer-based coatings, mainly those based on perfluoropolyether (PFPE) and polytetrafluoroethylene (PTFE) have accounted for a significant share of the market due to their superior oleophobic and hydrophobic performance, smooth tactile properties, and compatibility with high-volume manufacturing processes. These coatings are typically applied as ultra-thin films of approximately 10–15 nanometers on chemically strengthened glass substrates using vacuum deposition or spray techniques. For instance, the OPTOOL series developed by Daikin Industries represents a widely adopted commercial platform for oleophobic coatings in consumer electronics and automotive applications.

The growth of the anti-fingerprint coatings market is primarily driven by the increasing production of consumer electronic devices and the rapid adoption of touch-enabled interfaces. As of 2025, the global smartphone installed base exceeds 6.5 billion devices, with annual production approaching 1.2 billion units. Most smartphones, tablets, laptops, and wearable devices incorporate anti-fingerprint coatings as a standard component of display assemblies. In addition, the increasing size and number of display panels in both consumer electronics and automotive applications are expanding the total addressable surface area for these coatings. In the automotive sector, modern vehicles are increasingly equipped with multiple touchscreen interfaces, often exceeding a combined display area of 15 inches, further driving market growth.

The market is undergoing a transition due to increasing regulatory scrutiny of per- and polyfluoroalkyl substances (PFAS), which are commonly used in fluoropolymer-based coatings. A 2025 study published in Environmental Chemistry Letters reported that fluoropolymers used in touchscreen coatings, including PFPE, can transfer to users through dermal contact and may enter the human body through indirect exposure pathways. The study also highlighted that these coatings, typically applied as thin films of 10–15 nanometers, degrade over time with regular usage. Regulatory developments, such as the European Union’s REACH proposal targeting around 4,700 PFAS substances and the expansion of the U.S. Environmental Protection Agency’s Toxics Release Inventory to include 205 PFAS chemicals, are increasing compliance requirements for manufacturers.

In response, the key players are focusing on the development of PFAS-free coating technologies. In April 2026, Henkel introduced Loctite AF 8810 and AF 8812, which are fluorine-free anti-fingerprint coatings developed using silicone-based technologies. These products are designed for plastic and glass substrates and offer high durability, including resistance to abrasion and UV exposure. Similarly, companies such as Momentive are expanding PFAS-free product portfolios. Other industry participants, including LG Chem and BASF Coatings, are developing advanced coating solutions with additional functionalities, such as antimicrobial properties and improved durability.

The increasing adoption of electric vehicles (EVs) and advanced automotive display systems is expected to create significant growth opportunities for the market. EVs typically incorporate larger and more numerous display interfaces compared to conventional vehicles, increasing the demand for high-performance anti-fingerprint coatings. In addition, manufacturers are focusing on multifunctional coatings that combine fingerprint resistance with other performance attributes. For example, LG Chem has developed coatings with both anti-fingerprint and antimicrobial properties, while Nippon Paint Holdings has introduced UV-curable, water-based coatings for display panels and appliance applications.

Despite the positive outlook, the market faces challenges related to high production costs and durability limitations. The use of vacuum deposition equipment and premium raw materials increases manufacturing costs, limiting adoption in price-sensitive applications. In addition, the durability of existing oleophobic coatings remains a concern, as studies indicate that these coatings may degrade within a relatively short period under intensive usage conditions. Furthermore, increasing regulatory pressure on fluoropolymer-based materials is expected to impact supply chains and require continuous innovation in alternative coating technologies.

PFAS Regulatory Pressure Accelerating the Shift to Non-Fluorinated Anti-Fingerprint Chemistries

The tightening regulatory landscape surrounding per- and polyfluoroalkyl substances (PFAS), including fluoropolymers that form the foundation of most oleophobic anti-fingerprint coatings, is a key trend driving the anti-fingerprint coatings market. Increasing regulatory convergence across major regions is creating significant compliance challenges for manufacturers of fluoropolymer-based coatings and their OEM customers.

In the U.S., the Environmental Protection Agency (EPA) expanded its 2025 Toxics Release Inventory (TRI) reporting requirements to include 205 PFAS substances, classifying them as chemicals of special concern and eliminating low-concentration exemptions. As a result, coating manufacturers and electronics OEMs are required to report PFAS usage even in small quantities used in display coatings and surface treatments. In addition, the Significant New Use Rule (SNUR) mandates regulatory review prior to the reintroduction of inactive PFAS formulations. State-level regulations, such as California’s AB-1817, are further restricting the use of PFAS in relevant product categories. In Europe, the proposed REACH restriction covering up to 4,700 PFAS substances is expected to significantly impact non-essential applications, including electronics coatings and surface treatment technologies.

In response to these regulatory developments, coating manufacturers are increasingly focusing on the development and commercialization of PFAS-free alternatives. In April 2026, Henkel introduced Loctite AF 8810 and AF 8812, which are automotive-grade anti-fingerprint coatings developed using silicone-based, low-surface-energy chemistry without fluorinated components. These coatings are designed to meet performance requirements while addressing regulatory compliance concerns. Similarly, Momentive offers PFAS-free coating solutions for glass, metal, and plastic substrates with hydrophobic and oleophobic properties across automotive, industrial, and consumer applications.

Overall, the increasing regulatory pressure on PFAS is increasing the transition toward non-fluorinated coating technologies, including silicone-based, organosiloxane, and UV-curable systems. This shift is expected to create growth opportunities for manufacturers of alternative chemistries, while posing challenges for suppliers of PFPE-based coatings that are required to reformulate products to comply with evolving regulations.

Automotive EV Interior Display Proliferation Driving High-Growth Demand for Durable, UV-Stable Anti-Fingerprint Coatings

The rapid transition toward electric vehicles (EVs), along with the increasing integration of large-format touchscreen interfaces in vehicle interiors, is emerging as a key trend driving demand for anti-fingerprint coatings. Modern vehicles are increasingly replacing conventional physical controls with touch-sensitive glass or plastic display surfaces for infotainment, climate control, seating functions, and vehicle settings. This shift is significantly increasing the total surface area within vehicles that requires anti-fingerprint treatment, positioning the automotive segment as one of the fastest-growing application areas in the market.

Compared to consumer electronics, automotive applications require coatings with significantly higher performance standards. These include resistance to prolonged ultraviolet (UV) exposure through windshields and windows, stability under elevated cabin temperatures that may exceed 80°C, compatibility with automotive cleaning agents, and long-term durability aligned with vehicle lifecycles of 10 to 15 years. Conventional fluoropolymer-based coatings used in smartphones are typically not designed for such conditions, prompting the development of advanced formulations tailored for automotive use. For example, Daikin Industries developed the OPTOOL UD120 coating with enhanced UV durability to address these limitations.

These performance requirements are contributing to the emergence of a specialized, high-value segment within the anti-fingerprint coatings market, where suppliers are focusing on differentiated technologies and premium-grade formulations. In April 2026, Henkel introduced Loctite AF 8810 and AF 8812, designed for plastic and glass substrates used in automotive display systems, with features such as high hardness and improved durability. In addition, BASF Coatings entered into a co-development agreement with Hyundai Mobis in November 2024 to develop anti-smudge coatings for automotive dashboards, highlighting the increasing involvement of major coatings manufacturers in this segment.

Overall, the increasing adoption of digital interfaces in vehicles, particularly in EVs, is driving demand for durable and high-performance anti-fingerprint coatings. This trend is expected to drive the growth of automotive-specific coating solutions and create opportunities for manufacturers offering advanced, application-specific technologies.

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 2.02 Billion |

|

Market Size in 2026 |

USD 1.25 Billion |

|

Market Size in 2025 |

USD 1.18 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.2% |

|

Dominating Coating Type |

Oleophobic Coatings |

|

Fastest Growing Coating Type |

Hydrophobic Coatings |

|

Dominating Technology |

Vacuum Deposition |

|

Fastest Growing Technology |

Plasma-Enhanced CVD (PECVD) / UV-Curable |

|

Dominating Substrate |

Glass |

|

Fastest Growing Substrate |

Metal / Stainless Steel |

|

Dominating Application |

Consumer Electronics |

|

Fastest Growing Application |

Automotive |

|

Dominating End Use |

Consumer Goods Manufacturers |

|

Fastest Growing End Use |

Automotive OEMs |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on coating type, the global anti-fingerprint coatings market is segmented into oleophobic coatings, hydrophobic coatings, and omniphobic and multifunctional coatings.

In 2026, the oleophobic coatings segment is expected to account for the largest share of the global anti-fingerprint coatings market. The dominance of this segment is primarily attributed to its critical role as a standard surface treatment in consumer electronics manufacturing. Nearly all commercially produced smartphones, tablets, laptops, smartwatches, and smart display devices with glass interfaces incorporate oleophobic coatings as part of the display assembly process to enhance smudge resistance, maintain optical clarity, and improve tactile performance.

Oleophobic coatings are predominantly based on fluoropolymer chemistries, particularly perfluoropolyether (PFPE)-based nanocoatings, which are applied as ultra-thin films of approximately 10 to 15 nanometers using vacuum deposition techniques. These coatings typically achieve water contact angles above 100 degrees and provide strong oil repellency, preventing sebum deposits from adhering to glass surfaces. Commercial coating platforms such as the OPTOOL series developed by Daikin Industries are widely used in high-volume electronics manufacturing.

In addition, advanced glass products such as Gorilla Glass Armor 2, introduced in January 2025 and deployed on flagship smartphones, and Gorilla Glass Ceramic 2, introduced in May 2025, incorporate oleophobic surface coatings as standard features. Similarly, Dragontrail glass developed by AGC Inc. integrates oleophobic anti-fingerprint treatment as a standard specification across mid-range devices.

However, the hydrophobic coatings segment is projected to register the highest CAGR during the forecast period. The growth of this segment is primarily driven by increasing adoption across automotive interiors, stainless steel appliances, and architectural applications, where ease of cleaning and resistance to water and contaminants are key performance requirements. These applications typically prioritize durability and environmental resistance over the high-precision oleophobic performance required in touch-enabled consumer electronics.

In addition, the ongoing regulatory transition away from per- and polyfluoroalkyl substances (PFAS) is driving the adoption of non-fluorinated coating chemistries. Silicone-based hydrophobic coatings are emerging as a key alternative, particularly for automotive and industrial applications. In April 2026, Henkel introduced Loctite AF 8810 and AF 8812, PFAS-free coatings designed for plastic and glass substrates used in display applications. Similarly, Momentive offers PFAS-free coating solutions for glass, metal, and plastic substrates. These developments are expected to support the growth of hydrophobic coatings during the forecast period.

Based on technology, the global anti-fingerprint coatings market is segmented into vacuum deposition (including physical vapor deposition and chemical vapor deposition), sol-gel, plasma-enhanced chemical vapor deposition (PECVD), UV-curable coatings, and other application technologies.

In 2026, the vacuum deposition segment is expected to account for the largest share of the global anti-fingerprint coatings market. This dominance is primarily attributed to its established position as the standard industrial process for applying perfluoropolyether (PFPE)-based oleophobic coatings on glass substrates used in consumer electronics. Vacuum deposition is widely adopted across smartphone, tablet, and display manufacturing due to its ability to deliver consistent, high-quality thin-film coatings at scale.

In this process, glass substrates are placed within a vacuum chamber, where the coating material, typically PFPE or similar fluoropolymer formulations, is vaporized and deposited onto the substrate surface as a uniform nanometre-scale film. These coatings are typically applied in thicknesses of approximately 10 to 15 nanometers, ensuring high optical clarity, strong adhesion, and minimal impact on the tactile properties of the substrate. The process enables precise control over film uniformity and surface performance, making it suitable for high-performance display applications.

The large installed base of vacuum deposition equipment across major consumer electronics manufacturing hubs, including China, South Korea, Taiwan, and Japan, further supports the dominance of this segment. The integration of vacuum deposition processes into high-volume display manufacturing lines has created significant entry barriers for alternative technologies, reinforcing its continued adoption.

However, plasma-enhanced chemical vapor deposition (PECVD) and UV-curable coatings are projected to register the highest CAGR during the forecast period. PECVD enables the deposition of highly uniform and durable coatings from gas-phase precursors at relatively lower processing temperatures compared to conventional deposition methods. This makes it suitable for applications involving temperature-sensitive substrates and larger surface areas, particularly in automotive and architectural glass.

Similarly, UV-curable coating technologies enable rapid curing at ambient or low temperatures using ultraviolet light, supporting high-throughput processing of large-area substrates. These systems are increasingly adopted in applications such as automotive display panels, architectural glass, and appliance surfaces, where processing speed, scalability, and cost efficiency are critical. As a result, PECVD and UV-curable technologies are expected to gain traction over the forecast period, driven by expanding application scope beyond consumer electronics.

Based on substrate, the global anti-fingerprint coatings market is segmented into glass, metal and stainless steel, plastic and polymer, ceramic, and other substrates.

In 2026, the glass substrate segment is expected to account for the largest share of the global anti-fingerprint coatings market. This is primarily attributed to the wide use of glass as the primary surface material across key application areas, including consumer electronics displays, automotive infotainment systems, optical lenses, architectural glazing, and solar panel covers. These applications collectively represent major demand verticals for anti-fingerprint coatings, as glass surfaces require surface treatment to maintain visual clarity and usability.

The large share of this segment also reflects the inherent properties of glass that necessitate the use of anti-fingerprint coatings. Glass surfaces exhibit high visibility of fingerprints and smudges due to the contrast between transparent substrates and oily residues. While glass offers high scratch resistance and optical clarity, it lacks inherent oil-repellent properties, making coatings essential for performance enhancement. In addition, the extensive use of glass in high-value, touch-enabled consumer devices creates strong economic justification for the adoption of anti-fingerprint coatings.

Leading glass manufacturers incorporate anti-fingerprint coatings as a standard feature in advanced glass products. For instance, Corning Inc. offers Gorilla Glass solutions, including Gorilla Armor 2 (introduced in January 2025 and used in flagship smartphones) and Gorilla Glass Ceramic 2 (introduced in May 2025), both of which integrate oleophobic surface coatings. Similarly, Ceramic Shield 2, introduced in 2025 for premium smartphones, includes anti-fingerprint coating as part of the surface treatment stack. These developments highlight the widespread and standardized adoption of anti-fingerprint coatings across premium glass substrates.

However, the metal and stainless steel segment is projected to register the highest CAGR during the forecast period. The growth of this segment is driven by the increasing use of anti-fingerprint coatings on stainless steel appliances, including refrigerators, ovens, dishwashers, and washing machines, where fingerprints and water stains are highly visible on polished or brushed surfaces. In 2025, NANOKOTE introduced an advanced anti-fingerprint coating solution for kitchen appliances, focusing on improved resistance to fingerprints and water stains and enabling easier maintenance.

In addition, the growing use of premium metallic surfaces in automotive interiors, hospitality environments, and commercial architectural applications is further supporting demand for anti-fingerprint coatings on metal substrates. As a result, the metal and stainless steel segment is expected to witness strong growth over the forecast period.

Based on application, the global anti-fingerprint coatings market is segmented into consumer electronics (smartphones, tablets, laptops, wearables, and displays), building and construction (architectural glass, stainless steel fittings, and elevator panels), automotive (infotainment displays, dashboard and interior trim, and exterior glass), stainless steel appliances, solar panels and PV modules, eyewear and optics, and other applications.

In 2026, the consumer electronics segment is expected to account for the largest share of the global anti-fingerprint coatings market. This dominance is primarily attributed to the widespread and standardized use of anti-fingerprint coatings across smartphones, tablets, laptops, smartwatches, and other touch-enabled consumer devices. These coatings are an integral component of display assemblies, ensuring smudge resistance, improved tactile experience, and enhanced visual clarity.

The large share of this segment is driven by the scale of global smartphone production, which is approaching 1.2 billion units annually, along with the near-universal specification of oleophobic anti-fingerprint coatings on glass cover displays across all price segments. In addition to smartphones, the increasing adoption of tablets, touchscreen-enabled laptops, wearable devices, and smart home products with glass interfaces is expanding the total addressable surface area for anti-fingerprint coatings. Furthermore, advancements in coating technologies and performance optimization tools, such as the smart surface analytics system introduced by PPG Industries in 2025, reflect the growing level of innovation and product development in this segment.

However, the automotive segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing integration of large-format touchscreen interfaces in modern vehicles, particularly in electric vehicles, and the ongoing shift from physical controls to digital touch-based systems. Vehicles are increasingly equipped with multiple display surfaces, including center console screens, digital instrument clusters, rear-seat entertainment systems, and touch-enabled control panels. As a result, the total coated surface area per vehicle is significantly higher, often equivalent to five to ten smartphone display surfaces, leading to higher per-unit coating demand.

In the building and construction segment, anti-fingerprint coatings are used on architectural glass facades, glass railings, balustrades, stainless steel elevator panels, commercial kitchen surfaces, sanitary fittings, and decorative metal structures. The growth of this segment is supported by the increasing use of glass and stainless steel in modern architectural designs, where maintaining surface cleanliness and reducing maintenance requirements are key considerations. As a result, anti-fingerprint coatings are gaining traction as a value-added surface treatment in both commercial and residential construction projects.

Based on geography, the global anti-fingerprint coatings market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

In 2026, the Asia-Pacific is expected to account for the largest share of the global anti-fingerprint coatings market. The large share of this region is primarily attributed to its position as the global hub for consumer electronics manufacturing. China, in particular, is the world’s largest producer of smartphones, tablets, and laptops, which represent the largest application segment for anti-fingerprint coatings. In addition, China is a major exporter of architectural glass, supporting demand from both consumer electronics and building & construction applications.

The presence of leading coating material suppliers and technology providers further strengthens the regional market. Japan is home to key companies such as Daikin Industries, Natoco Co., Ltd., and NAGASE & Co., Ltd., which are major suppliers of oleophobic coating materials and specialty chemicals. In South Korea, companies such as Samsung Electronics and LG Electronics represent significant demand centers through their large-scale production of smartphones, display panels, and home appliances. In addition, LG Chem is actively involved in the development of coating technologies for automotive and EV display applications.

North America is expected to account for the second-largest share of the global anti-fingerprint coatings market. The U.S. commands around 80-85% of the North American market in 2026, driven by high adoption of consumer electronics, premium appliances, and advanced automotive interiors. The presence of major players, including PPG Industries, Cytonix Corporation, and Corning Inc., along with strong research and development capabilities, supports regional market growth. In addition, increasing regulatory pressure on PFAS in North America is driving investments in alternative coating chemistries.

The Asia-Pacific anti-fingerprint coatings market is also projected to grow at the fastest CAGR during the forecast period. This growth is driven by continued expansion in consumer electronics manufacturing across Southeast Asia and India, increasing domestic consumption of premium electronics and appliances in China, and rising investments in solar photovoltaic manufacturing in countries such as China and India. The expansion of solar PV capacity is creating additional demand for anti-fingerprint and anti-soiling coatings on photovoltaic glass modules.

The global anti-fingerprint coatings market is moderately fragmented, comprising global specialty chemical companies, materials science companies, glass and substrate manufacturers with integrated coating capabilities, and surface treatment technology providers. The competitive landscape is driven by companies with strong expertise in fluoropolymer and silicone-based chemistries, thin-film deposition technologies, and large-scale manufacturing integration. High entry barriers, including the need for precision coating application, established relationships with consumer electronics and automotive OEMs, and increasing regulatory compliance requirements, particularly related to PFAS, continue to shape competition.

The companies are focusing on the development of PFAS-free coating solutions, enhanced durability, and multifunctional performance to meet evolving requirements across consumer electronics, automotive, and industrial applications.

Key players operating in the global anti-fingerprint coatings market include Daikin Industries, PPG Industries, Henkel, Momentive, AGC Inc., Corning Inc., LG Chem, Nippon Paint Holdings, Natoco Co., Ltd., Sumitomo Chemical, NAGASE & CO., Ltd., Plasmatreat, Cytonix LLC, BASF Coatings, and 3M, among others.

This report provides market size estimates and forecasts for each segment and sub-segment at the global, regional, and country levels. The report further offers an in-depth analysis of the latest industry trends, market dynamics, technological advancements, regulatory developments, and key strategic initiatives across each sub-segment for the forecast period 2026–2036.

For the purpose of this study, the global Anti-Fingerprint Coatings Market has been segmented based on coating type, technology, substrate, application, end use, and geography.

|

Segment |

Sub-Segments |

|---|---|

|

By Coating Type |

Oleophobic Coatings, Hydrophobic Coatings, Omniphobic / Multifunctional Coatings |

|

By Technology |

Vacuum Deposition (PVD/CVD), Sol-Gel, Plasma-Enhanced CVD (PECVD), UV-Curable Coatings, Other Technologies |

|

By Substrate |

Glass, Metal / Stainless Steel, Plastic / Polymer, Ceramic, Other Substrates |

|

By Application |

Consumer Electronics (Smartphones, Tablets, Laptops, Wearables, Displays), Building & Construction (Architectural Glass, Stainless Steel Fittings, Elevator Panels), Automotive (Infotainment Displays, Dashboard & Interior Trim, Exterior), Stainless Steel Appliances, Solar Panels / PV Modules, Eyewear & Optics, Other Applications |

|

By End Use |

Consumer Goods Manufacturers, Architectural / Construction, Automotive OEMs, Appliance Manufacturers, Solar / PV Industry, Healthcare & Medical Devices, Other End Uses |

|

By Geography |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

By Coating Type (Revenue, USD Billion, 2026–2036)

By Technology (Revenue, USD Billion, 2026–2036)

By Substrate (Revenue, USD Billion, 2026–2036)

By Application (Revenue, USD Billion, 2026–2036)

By End Use (Revenue, USD Billion, 2026–2036)

By Geography (Revenue, USD Billion, 2026–2036)

The global anti-fingerprint coatings market is expected to reach USD 2.02 billion by 2036 from an estimated USD 1.25 billion in 2026, at a CAGR of 5.2% during the forecast period 2026–2036.

In 2026, oleophobic coatings are expected to hold the largest market share of global revenue, driven by their universal adoption in consumer electronics manufacturing as the standard anti-fingerprint treatment on smartphone, tablet, and display glass surfaces.

Hydrophobic coatings are expected to register the highest CAGR during the forecast period 2026–2036, driven by expanding adoption in automotive interiors, stainless steel appliances, and architectural applications, as well as by the shift toward non-fluorinated silicone-based hydrophobic formulations as PFAS regulations tighten globally, exemplified by Henkel’s April 2026 launch of Loctite AF 8810 and AF 8812.

In 2026, consumer electronics is expected to hold the largest market share, reflecting the near-universal specification of oleophobic anti-fingerprint coatings on global smartphone, tablet, laptop, and wearable device glass cover production approaching 1.2 billion units annually.

The automotive segment is expected to register the highest CAGR during the forecast period, driven by the rapid proliferation of large-format glass and plastic touchscreen control surfaces in electric vehicles and the associated demand for durable, UV-stable anti-fingerprint coatings meeting automotive-grade specifications for coating lifetime and performance under harsh conditions.

The growth of this market is primarily driven by the sustained global expansion of consumer electronics production and touch-enabled device proliferation; the rapid adoption of large-format touchscreen displays in electric vehicle interiors; the expansion of stainless steel appliance and architectural glass applications requiring low-maintenance anti-fingerprint surfaces; the growing adoption of premium multifunctional coatings combining anti-fingerprint with antimicrobial, anti-glare, and anti-reflective performance; and the market opportunities created by PFAS regulatory pressure accelerating reformulation toward non-fluorinated alternatives such as Henkel’s Loctite AF 8810/8812 (April 2026) and Momentive’s PFAS-free coating portfolio.

Key players in the global anti-fingerprint coatings market include Daikin Industries (Japan), PPG Industries (U.S.), Henkel (Germany), Momentive (U.S.), AGC Inc. (Japan), Corning Inc. (U.S.), LG Chem (South Korea), Nippon Paint Holdings (Japan), Natoco Co., Ltd. (Japan), Sumitomo Chemical (Japan), NAGASE & CO., Ltd. (Japan), Plasmatreat (Germany), Cytonix LLC (U.S.), BASF Coatings (Germany), and 3M (U.S.).

Asia Pacific is expected to register the highest growth rate in the global anti-fingerprint coatings market during the forecast period 2026–2036, sustained by its dominant position in consumer electronics manufacturing, China’s leadership in glass production and solar PV module manufacturing, growing domestic consumer electronics and premium appliance demand, and Japan’s leadership in fluoropolymer and specialty coating chemical technology.

1. INTRODUCTION

1.1. Market Definition & Scope

1.2. Market Ecosystem

1.3. Currency & Pricing Assumptions

1.4. Key Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Process

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research / Interviews with Key Opinion Leaders from the Industry

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.1.1. Bottom-up Approach

2.3.1.2. Top-down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

2.4. Limitations of the Study

3. EXECUTIVE SUMMARY

3.1. Overview

3.2. Market by Coating Type

3.3. Market by Technology

3.4. Market by Substrate

3.5. Market by Application

3.6. Market by End Use

3.7. Market by Geography

3.8. Competitive Landscape Snapshot

3.9. Key Strategic Insights

3.10. Analyst Recommendations

4. MARKET INSIGHTS

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Global Consumer Electronics Production and Touch-Screen Device Proliferation

4.2.1.2. Rapid Proliferation of Large-Format Touchscreen Displays in Electric Vehicles

4.2.1.3. Growing Demand for Low-Maintenance Stainless Steel and Architectural Glass Surfaces

4.2.1.4. Increasing Adoption of Multifunctional Coatings Combining Anti-Fingerprint, Antimicrobial, and Optical Properties

4.2.1.5. Solar PV Module Production Expansion Creating Demand for Anti-Soiling and Anti-Fingerprint Glass Coatings

4.2.2. Restraints

4.2.2.1. High Production Cost of Vacuum Deposition Equipment and Fluoropolymer Raw Materials

4.2.2.2. Limited Durability of Current Commercial Oleophobic Coatings in Harsh Environments

4.2.2.3. PFAS Regulatory Pressure on Incumbent Fluoropolymer-Based Oleophobic Formulations

4.2.3. Opportunities

4.2.3.1. Non-Fluorinated PFAS-Free Anti-Fingerprint Coating Development for Automotive and Electronics OEMs

4.2.3.2. Augmented Reality and Flexible Display Substrates Requiring Next-Generation Coating Architectures

4.2.3.3. Healthcare and Medical Device Surface Coatings with Integrated Anti-Fingerprint and Antimicrobial Properties

4.2.4. Challenges

4.2.4.1. Balancing Oleophobicity, Optical Clarity, Haptic Performance, and Durability in Single Coating Systems

4.2.4.2. Lack of Universally Accepted Testing and Certification Standards for Anti-Fingerprint Performance

4.2.4.3. Raw Material Volatility and Supply Chain Risks for Specialty Fluorochemicals

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of Substitutes

4.3.4. Threat of New Entrants

4.3.5. Degree of Competition

4.4. Regulatory Landscape

4.4.1. U.S. — EPA PFAS TRI Reporting (205 Substances, 2025), TSCA SNUR, State-Level Restrictions

4.4.2. Europe — REACH PFAS Broad Restriction Proposal, EU VOC Regulations

4.4.3. Asia Pacific — China, Japan, South Korea Environmental and Chemical Safety Frameworks

4.4.4. Other Key Regulatory Jurisdictions

4.5. Value Chain Analysis

4.6. Impact of Macroeconomic Factors

5. ANTI-FINGERPRINT COATINGS MARKET, BY COATING TYPE

5.1. Overview

5.2. Oleophobic Coatings

5.3. Hydrophobic Coatings

5.4. Omniphobic / Multifunctional Coatings

6. ANTI-FINGERPRINT COATINGS MARKET, BY TECHNOLOGY

6.1. Overview

6.2. Vacuum Deposition (PVD / CVD)

6.3. Sol-Gel

6.4. Plasma-Enhanced CVD (PECVD)

6.5. UV-Curable Coatings

6.6. Other Technologies

7. ANTI-FINGERPRINT COATINGS MARKET, BY SUBSTRATE

7.1. Overview

7.2. Glass

7.3. Metal / Stainless Steel

7.4. Plastic / Polymer

7.5. Ceramic

7.6. Other Substrates

8. ANTI-FINGERPRINT COATINGS MARKET, BY APPLICATION

8.1. Overview

8.2. Consumer Electronics

8.2.1. Smartphones

8.2.2. Tablets

8.2.3. Laptops & Monitors

8.2.4. Wearables & Smartwatches

8.2.5. Other Consumer Electronics

8.3. Building & Construction

8.3.1. Architectural Glass & Facades

8.3.2. Stainless Steel Fittings & Sanitary Ware

8.3.3. Elevator Panels & Interior Surfaces

8.4. Automotive

8.4.1. Infotainment Displays & Touchscreens

8.4.2. Dashboard & Interior Trim

8.4.3. Exterior Glass

8.5. Stainless Steel Appliances

8.6. Solar Panels / PV Modules

8.7. Eyewear & Optics

8.8. Other Applications

9. ANTI-FINGERPRINT COATINGS MARKET, BY END USE

9.1. Overview

9.2. Consumer Goods Manufacturers

9.3. Architectural / Construction

9.4. Automotive OEMs

9.5. Appliance Manufacturers

9.6. Solar / PV Industry

9.7. Healthcare & Medical Devices

9.8. Other End Uses

10. ANTI-FINGERPRINT COATINGS MARKET, BY GEOGRAPHY

10.1. Overview

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. France

10.3.3. U.K.

10.3.4. Italy

10.3.5. Spain

10.3.6. Rest of Europe

10.4. Asia Pacific

10.4.1. China

10.4.2. Japan

10.4.3. South Korea

10.4.4. India

10.4.5. Australia

10.4.6. Rest of Asia Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East & Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Rest of Middle East & Africa

11. COMPETITIVE LANDSCAPE

11.1. Overview

11.2. Key Growth Strategies

11.2.1. Market Differentiators

11.2.2. Synergy Analysis: Major Deals and Strategic Alliances

11.3. Competitive Dashboard

11.3.1. Industry Leaders

11.3.2. Market Differentiators

11.3.3. Vanguards

11.3.4. Emerging Companies

11.4. Competitive Benchmarking

11.5. Market Share / Ranking Analysis (2025)

12. COMPANY PROFILES

Business Overview, Financial Overview, Product Portfolio, Strategic Developments, and SWOT Analysis

12.1. Daikin Industries, Ltd. (Japan)

12.2. PPG Industries, Inc. (U.S.)

12.3. Henkel AG & Co. KGaA (Germany)

12.4. Momentive Performance Materials Inc. (U.S.)

12.5. AGC Inc. (Japan)

12.6. Corning Incorporated (U.S.)

12.7. LG Chem Ltd. (South Korea)

12.8. Nippon Paint Surf Chemicals Co., Ltd. (Japan)

12.9. Natoco Co., Ltd. (Japan)

12.10. Sumitomo Chemical Co., Ltd. (Japan)

12.11. NAGASE & CO., Ltd. (Japan)

12.12. Plasmatreat GmbH (Germany)

12.13. Cytonix LLC (U.S.)

12.14. BASF Coatings (Germany)

12.15. 3M Company (U.S.)

12.16. Others

13. APPENDIX

13.1. Questionnaire

13.2. Customization Options

13.3. Abbreviations

13.4. List of Data Sources

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates