Resources

About Us

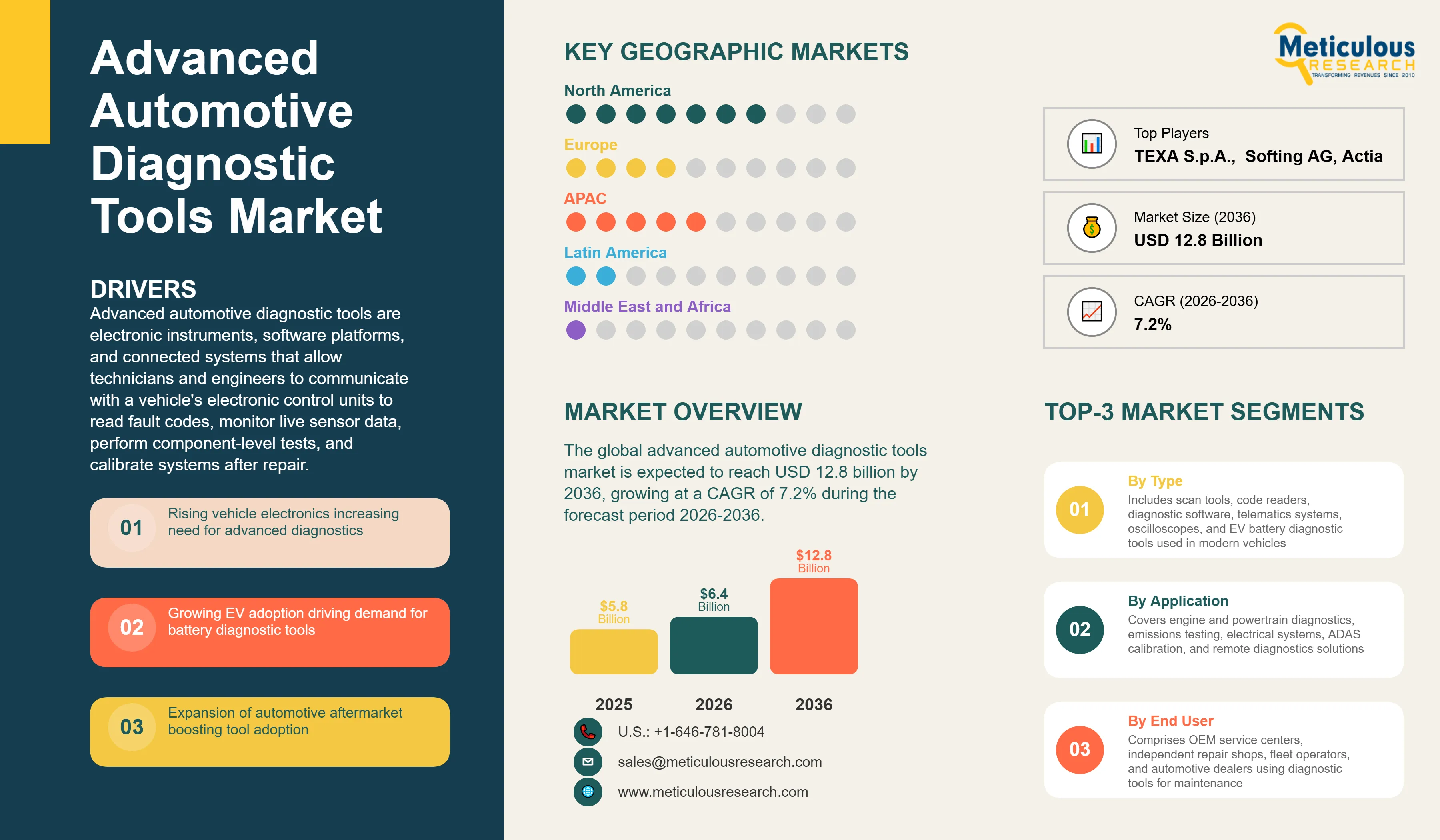

The global advanced automotive diagnostic tools market was valued at USD 5.8 billion in 2025. This market is expected to reach USD 12.8 billion by 2036 from an estimated USD 6.4 billion in 2026, growing at a CAGR of 7.2% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Advanced automotive diagnostic tools are electronic instruments, software platforms, and connected systems that allow technicians and engineers to communicate with a vehicle's electronic control units to read fault codes, monitor live sensor data, perform component-level tests, and calibrate systems after repair. A modern vehicle is effectively a rolling network of dozens to over one hundred ECUs controlling everything from the engine and transmission to the braking system, airbags, infotainment, advanced driver assistance systems, and the high-voltage battery management system in an EV. When any of these systems malfunctions or needs service, a technician requires a diagnostic tool that can establish communication with the relevant ECU over the vehicle's CAN bus or Ethernet network, retrieve and interpret the fault codes stored in its memory, and often command the system through active tests to isolate the faulty component. Without the right diagnostic tool, a modern vehicle is essentially a black box to the workshop.

The market is growing because every major trend in automotive technology is increasing the complexity of vehicles that need to be diagnosed. According to the IEA's Global EV Outlook 2025, global EV sales reached around 17-18 million in 2024, and the growing EV fleet requires specialized high-voltage battery diagnostic tools and BMS communication capabilities that conventional diagnostic equipment does not provide. According to the Auto Care Association’s 2026 Auto Care FactBook, the U.S. automotive aftermarket generated approximately USD 414 billion in total sales in 2024, with repair and maintenance representing a large share, and the profitability of that repair business increasingly depends on technicians having the right diagnostic tools to identify and fix faults efficiently without guesswork. The right-to-repair movement, which in the U.S. has resulted in a memorandum of understanding between automakers and independent repairers and in Europe has seen legislative developments supporting independent access to vehicle diagnostic data, is expanding the addressable market for third-party diagnostic tool providers.

Two particularly powerful growth drivers are converging. The proliferation of ADAS features including automatic emergency braking, lane keeping assist, and adaptive cruise control requires calibration after any repair that affects camera, radar, or lidar sensor alignment, and this calibration must be performed with the OEM or equivalent ADAS calibration equipment, creating a new and growing diagnostic tool procurement category in workshops that was essentially nonexistent five years ago. Simultaneously, the shift toward software-defined vehicles, where vehicle features and capabilities are delivered and updated through software rather than hardware, is transforming OTA diagnostics from a convenience into a core vehicle architecture feature that generates ongoing diagnostic data streams and remote service opportunities.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 12.8 Billion |

|

Market Size in 2026 |

USD 6.4 Billion |

|

Market Size in 2025 |

USD 5.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 7.2% |

|

Dominating Tool Type |

Scan Tools |

|

Fastest Growing Tool Type |

Battery and EV Diagnostic Tools |

|

Dominating Connectivity Type |

Wired Diagnostics |

|

Fastest Growing Connectivity Type |

Cellular/Cloud Connectivity |

|

Dominating Vehicle Type |

Passenger Cars |

|

Fastest Growing Vehicle Type |

Electric Vehicles (EVs) |

|

Dominating Application |

Engine and Powertrain Diagnostics |

|

Fastest Growing Application |

Safety Systems Diagnostics (ADAS) |

|

Dominating End User |

Independent Repair Shops |

|

Fastest Growing End User |

Fleet Operators |

|

Dominating Deployment Model |

On-Premises Diagnostics |

|

Fastest Growing Deployment Model |

Cloud-Based Diagnostics |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

EV Diagnostic Complexity Driving Specialist Tool Investment

The rapid growth of the electric vehicle fleet is creating one of the most commercially significant new product requirements in the diagnostic tools market, because EVs have fundamentally different diagnostic needs from internal combustion engine vehicles. An EV's most critical and expensive component, the high-voltage battery pack, requires dedicated battery diagnostic tools capable of measuring individual cell voltages across hundreds of cells in a battery module, assessing state of health and state of charge, communicating with the battery management system over vehicle-specific protocols, and safely managing the high-voltage isolation required when working near battery systems that may carry 400 to 800 volts. Conventional OBD-II scan tools designed for ICE vehicles typically cannot access EV battery systems at the cell level.

According to the IEA's Global EV Outlook 2025, global EV sales reached around 17-18 million in 2024 and the global EV stock exceeded 55 million vehicles, creating a rapidly growing population of EVs in service that need battery health assessment, warranty claim support, and eventual battery replacement service. Autel, Launch Tech, Bosch, and Snap-on have all introduced dedicated EV diagnostic product lines addressing high-voltage battery testing, electric drive system diagnostics, and charging system fault analysis. According to Autel's product announcements in 2024, its EV-specific MaxiBAS BT608EV battery and starter service system and its ADAS calibration platforms have been among its fastest-growing product categories, reflecting the strong workshop demand for tools that address the new diagnostic requirements of the growing EV fleet.

ADAS Calibration Becoming a Mandatory Workshop Capability

Advanced driver assistance systems have moved from premium vehicle options to standard equipment across a wide range of new vehicle models following regulatory mandates. The European Union's General Safety Regulation, which came into force for all new vehicle types from July 2022 and all new vehicles from July 2024, mandates automatic emergency braking, lane keeping, intelligent speed assistance, and driver drowsiness monitoring as standard equipment on new passenger cars and commercial vehicles. The U.S. National Highway Traffic Safety Administration has similarly advanced automatic emergency braking requirements. According to the European New Car Assessment Programme, majority of new vehicles tested in 2024 were equipped with the full set of mandated ADAS features.

The commercial implication for the diagnostic tools market is that every workshop performing a windscreen replacement, front-end collision repair, wheel alignment, or any other work that might disturb the mounting angle of a camera, radar, or lidar sensor must perform an ADAS calibration using approved calibration equipment before returning the vehicle to service. This calibration requires a flat calibration area of typically 8 to 10 meters in length, a target board positioned at specified distances and angles from the vehicle, and a diagnostic tool or dedicated calibration system that commands the ADAS system through its calibration routine and verifies that the sensor is aligned within specification. According to Autel's 2024 market communications, the ADAS calibration tool segment was growing at a significantly above-average rate in its product portfolio, and Bosch, Continental, and TEXA have all invested in expanding their ADAS calibration product ranges to serve this growing workshop requirement.

Software-Defined Vehicles Transforming Diagnostics from Hardware to Platform Business

The emerging software-defined vehicle architecture, exemplified by Tesla's OTA update capability that can add new vehicle features and performance characteristics remotely, and increasingly adopted by Volkswagen, BMW, Mercedes-Benz, and other traditional automakers through their vehicle platform software architectures, is transforming automotive diagnostics from a hardware-centric product business toward a software platform and data services business. In a software-defined vehicle, the vehicle itself continuously generates diagnostic data that is transmitted to the cloud, where OEMs and authorized service providers can monitor vehicle health, identify developing faults before they cause a breakdown, and push software remediation without requiring a workshop visit.

This transformation creates both threats and opportunities for the diagnostic tools market. Traditional hardware scan tool revenue is partially displaced as OTA diagnostics reduce the frequency of workshop diagnostic scans for software-related faults that can be resolved remotely. At the same time, the data generated by software-defined vehicles creates opportunities for cloud-based diagnostic platform businesses that can aggregate, analyze, and act on fleet-wide diagnostic data streams. Companies including Delphi Technologies through its Delphi Connect platform, KPIT Technologies with its automotive software and diagnostics services, and Vector Informatik with its cloud-based vehicle data analysis tools are all developing cloud diagnostic capabilities that position them to participate in the software-defined vehicle diagnostics opportunity.

Increasing Vehicle Electrification and Electronic Complexity

Every major automotive technology trend is adding electronic control units, sensors, and communication buses to vehicles, and each additional system requires diagnostic capability in the service workflow. Modern premium vehicles contain over 100 ECUs communicating over multiple CAN, LIN, MOST, and Automotive Ethernet networks, and diagnosing an intermittent fault in such a system requires tools capable of monitoring live data from multiple ECUs simultaneously, correlating signals across different networks, and performing guided fault isolation tests that conventional multimeters cannot provide. According to Bosch's Automotive Handbook, the most recent edition of which documents that the average semiconductor content per vehicle has been doubling approximately every eight years, this electronics proliferation trend shows no sign of slowing. The transition to electric vehicles adds another layer of diagnostic complexity through high-voltage battery systems, power electronics, and electric drive systems that require specialized insulation testing, cell-level battery analysis, and high-voltage safety protocols that represent entirely new diagnostic skill sets and tool requirements.

Expansion of Automotive Aftermarket Services

The global automotive aftermarket is large, growing, and increasingly dependent on advanced diagnostic tools for both the identification of vehicle faults and the calibration of repaired systems to specification. According to the Auto Care Association's 2024 Fact Book, the U.S. automotive aftermarket generated approximately USD 475 billion in 2023 across parts, service labor, and related categories. The average age of vehicles on U.S. roads reached a record 12.6 years in 2024 according to S&P Global Mobility, and older vehicles that are out of manufacturer warranty are serviced predominantly by the independent aftermarket, which requires diagnostic tools that can work across the full range of vehicle brands and model years rather than being limited to OEM-proprietary systems. The growth of the independent aftermarket is creating sustained demand for multi-brand diagnostic platforms that cover the broadest possible vehicle range, which is the core product positioning of Autel, Launch Tech, TEXA, and Snap-on's professional aftermarket diagnostic lines.

Remote and Cloud-Based Diagnostics

Cloud-based diagnostic platforms that allow vehicle diagnostic data to be accessed, analyzed, and acted on remotely represent a commercially transformative opportunity for the diagnostic tools industry, enabling service models that go far beyond the traditional workshop-visit fault diagnosis model. A fleet operator with hundreds of trucks can monitor the diagnostic health status of every vehicle in its fleet from a central dashboard, receive alerts when any vehicle develops a fault code indicating an imminent component failure, and route the vehicle for preventive service before a roadside breakdown occurs. According to a 2024 analysis citing the American Transportation Research Institute (ATRI), unplanned truck breakdowns cost commercial carriers on the order of USD 450–750 per day in direct and indirect costs per truck, making the preventive‑maintenance and remote‑diagnostics case financially compelling for large‑scale fleet operators. For the diagnostic tool providers, cloud-based diagnostics represent an opportunity to transition from one-time hardware sales toward recurring subscription revenue from diagnostic data analysis services, improving revenue quality and customer retention.

Integration with AI and Data Analytics

The integration of artificial intelligence into diagnostic tools is enabling a new category of predictive and guided diagnostics that can significantly improve the speed and accuracy of fault diagnosis in increasingly complex vehicles. A diagnostic tool with AI-assisted fault analysis can cross-reference a specific combination of fault codes, live data readings, and vehicle history against a database of millions of previous repair cases to identify the most probable root cause and suggest the most efficient repair path, reducing the diagnostic time that technicians spend on complex intermittent faults from hours to minutes. Bosch's automotive service business has been investing in AI-assisted repair guidance, and Snap-on has developed its iD Repair function that provides technician guidance based on vehicle-specific diagnostic data. According to a 2024 survey by the National Institute for Automotive Service Excellence, technician diagnostic proficiency has become the leading factor in workshop profitability, as diagnostic accuracy directly determines whether the correct part is ordered and fitted on the first visit or whether multiple return visits are required to resolve the fault, and AI-assisted diagnosis is the most commercially impactful technology for improving this proficiency at scale.

By Tool Type: In 2026, Scan Tools to Dominate

Based on tool type, the global advanced automotive diagnostic tools market is segmented into scan tools (handheld and PC-based), code readers, diagnostic software platforms, telematics-based diagnostic systems, oscilloscopes and multimeters, and battery and EV diagnostic tools. In 2026, the scan tools segment is expected to account for the largest share of the global advanced automotive diagnostic tools market. Scan tools that communicate with vehicle ECUs over the OBD-II diagnostic port to read fault codes, access live data, and perform active tests are the most universally required diagnostic instrument in automotive service, used in virtually every service interaction across passenger cars, commercial vehicles, and light trucks. Professional multi-brand scan tools from Bosch, Snap-on, Autel, and Launch Tech are standard workshop equipment for both dealer and independent workshops globally.

However, the battery and EV diagnostic tools segment is projected to register the highest CAGR during the forecast period. The rapidly growing global EV fleet, which surpassed 55 million vehicles in 2024 per the IEA, is creating urgent workshop demand for tools capable of assessing EV battery state of health, diagnosing BMS faults, testing charging system components, and safely handling high-voltage battery systems. This is a new product category that is growing rapidly from a small current base as EV service volumes increase and as workshops invest in the specialized equipment required to service EVs competently.

By Vehicle Type: In 2026, Passenger Cars to Hold the Largest Share

Based on vehicle type, the global advanced automotive diagnostic tools market is segmented into passenger cars, commercial vehicles, electric vehicles, and off-highway vehicles. In 2026, the passenger cars segment is expected to account for the largest share of the global advanced automotive diagnostic tools market. Passenger cars represent by far the largest component of the global vehicle parc by unit count, and the aftermarket diagnostic tool market is sized proportionally to the vehicle population. The high average electronic complexity of modern passenger cars, with over 100 ECUs in premium models, combined with the mandatory OBD-II diagnostic port requirement across all markets, makes passenger car diagnostic tooling the core of the market.

However, the electric vehicles segment is projected to register the highest CAGR during the forecast period. With global EV sales growing at above-average rates and the EV parc expanding rapidly toward tens of millions of vehicles requiring service, the EV-specific diagnostic tool segment is growing significantly faster than the overall market. Battery health assessment tools, BMS diagnostic platforms, and charging system analyzers for EVs represent an entirely new tool category that every EV-servicing workshop needs to acquire as the EV fleet in their market grows.

By Application: In 2026, Engine and Powertrain Diagnostics to Hold the Largest Share

Based on application, the global advanced automotive diagnostic tools market is segmented into engine and powertrain diagnostics, emission diagnostics, electrical and electronic systems diagnostics, safety systems diagnostics, telematics and remote diagnostics, and other applications. In 2026, the engine and powertrain diagnostics segment is expected to account for the largest share of the global advanced automotive diagnostic tools market. Engine and transmission faults are the most common diagnostic requirements across the global vehicle fleet, and engine diagnostic capability is a fundamental requirement of every professional scan tool. The very large ICE vehicle parc of over 1.5 billion vehicles generates the majority of diagnostic tool demand through engine and drivetrain service.

However, the safety systems diagnostics segment, particularly ADAS calibration, is projected to register the highest CAGR during the forecast period. As ADAS systems become standard equipment on new vehicles following regulatory mandates in Europe and North America, and as these vehicles progressively enter the service cycle, the demand for ADAS calibration equipment and software is growing very rapidly. Every workshop repairing ADAS-equipped vehicles needs calibration capability, and the European General Safety Regulation's requirements affecting all new vehicles from July 2024 are creating a particularly sharp and immediate increase in ADAS calibration tool demand across European workshops.

Advanced Automotive Diagnostic Tools Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global advanced automotive diagnostic tools market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global advanced automotive diagnostic tools market. The United States has the world's most developed automotive aftermarket, and one of the world's highest rates of diagnostic tool investment per workshop. The U.S. mandatory OBD-II requirement for all vehicles sold since 1996 established a standardized diagnostic architecture that has supported widespread diagnostic tool deployment across the independent repair sector. The U.S. vehicle parc is heavily dominated by trucks, SUVs, and premium vehicles with high electronic content that require advanced diagnostic tools for service. The Right-to-Repair memorandum of understanding signed between the Automotive Service Association and automakers in 2023 provides independent repairers with access to telematics data and remote diagnostic capabilities that were previously restricted to dealer networks, expanding the addressable market for advanced diagnostic tool providers in the U.S. independent channel. Snap-on Incorporated is the world's leading professional automotive diagnostic tool brand and generates the majority of its revenues from the North American professional workshop market.

However, the Asia-Pacific advanced automotive diagnostic tools market is expected to grow at the fastest CAGR during the forecast period. The region contains the world's two largest automotive markets by new vehicle sales, China and India, and has the world's fastest-growing EV adoption concentrated in China. China's domestic automotive diagnostic tool industry has grown very rapidly, with Autel Intelligent Technology and Launch Tech having grown from small domestic players to global competitors with millions of diagnostic tool users worldwide. India's record vehicle sales of over 20 million units in fiscal year 2024 per SIAM data are expanding the Indian vehicle parc and its associated service industry, driving growing diagnostic tool procurement across both dealer networks and the large independent repair sector. Japan, South Korea, and Australia are technologically sophisticated automotive markets with advanced diagnostic tool adoption, and Southeast Asian markets including Thailand, Indonesia, and Vietnam are growing rapidly as their automotive industries develop.

Europe is a technically advanced and regulatory-driven automotive diagnostic tools market, where the EU General Safety Regulation's ADAS mandates are creating particularly strong near-term demand for ADAS calibration tools and where the progressive transition to electric vehicles across European automotive markets is driving EV diagnostic tool investment. Germany, as the home of the European automotive industry and the headquarters of Bosch, Continental, and Hella, is both the largest European diagnostic tool market by revenue and the location of significant diagnostic tool R&D. The UK's right-to-repair regulations and the established independent aftermarket culture in France, Italy, and Spain sustain strong diagnostic tool demand across European independent workshops.

The advanced automotive diagnostic tools market is served by large Tier-1 automotive technology companies with comprehensive diagnostic portfolios, professional tool specialists focused exclusively on workshop diagnostic equipment, software and platform companies serving OEM and independent service networks, and a growing cohort of Chinese tool manufacturers that have rapidly expanded from domestic to global markets. Competition is based on vehicle coverage breadth, diagnostic depth for complex systems, update frequency and quality, EV and ADAS diagnostic capability, ease of use and technician training, and price positioning across professional, mid-tier, and entry-level product ranges.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, vehicle coverage, EV and ADAS capabilities, geographic presence, and recent strategic developments. Some of the key players operating in the global advanced automotive diagnostic tools market include Robert Bosch GmbH (Germany), Snap-on Incorporated (U.S.), Continental AG (Germany), Delphi Technologies/BorgWarner Inc. (U.S.), DENSO Corporation (Japan), Autel Intelligent Technology Corp. Ltd. (China), Launch Tech Co. Ltd. (China), Actia Group (France), AVL List GmbH (Austria), TEXA S.p.A. (Italy), Softing AG (Germany), KPIT Technologies Ltd. (India), Vector Informatik GmbH (Germany), Hickok Incorporated (U.S.), and Hella GmbH & Co. KGaA (Germany), among others.

The global advanced automotive diagnostic tools market is expected to reach USD 12.8 billion by 2036 from an estimated USD 6.4 billion in 2026, at a CAGR of 7.2% during the forecast period 2026-2036.

In 2026, the scan tools segment is expected to hold the largest share of the global advanced automotive diagnostic tools market.

The battery and EV diagnostic tools segment is projected to register the highest CAGR during the forecast period 2026-2036.

The EU General Safety Regulation mandating ADAS as standard equipment on all new vehicles from July 2024, and equivalent regulatory requirements in North America, means every windscreen replacement, front-end repair, or wheel alignment on a modern vehicle requires ADAS camera and sensor calibration. This is creating very rapid growth in ADAS calibration tool demand across European and North American workshops, with Autel, Bosch, Continental, and TEXA all reporting ADAS calibration as among their fastest-growing product categories in 2024.

The market is primarily driven by increasing vehicle electronic complexity, with modern vehicles containing over 100 ECUs requiring specialized diagnostic access, combined with the rapid growth of the EV fleet requiring new high-voltage battery diagnostic capabilities and the mandatory ADAS systems in new vehicles requiring calibration equipment after any relevant repair work.

Key players are Robert Bosch GmbH (Germany), Snap-on Incorporated (U.S.), Continental AG (Germany), Delphi Technologies/BorgWarner Inc. (U.S.), DENSO Corporation (Japan), Autel Intelligent Technology Corp. Ltd. (China), Launch Tech Co. Ltd. (China), Actia Group (France), AVL List GmbH (Austria), TEXA S.p.A. (Italy), Softing AG (Germany), KPIT Technologies Ltd. (India), Vector Informatik GmbH (Germany), Hickok Incorporated (U.S.), and Hella GmbH & Co. KGaA (Germany), among others.

Asia-Pacific is expected to register the highest growth rate in the global advanced automotive diagnostic tools market during the forecast period 2026-2036.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Vehicle Electrification and Electronic Complexity

4.2.1.2. Growth in Connected and Software-Defined Vehicles

4.2.1.3. Rising Demand for Predictive Maintenance and Diagnostics

4.2.1.4. Expansion of Automotive Aftermarket Services

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Diagnostic Equipment

4.2.2.2. Proprietary OEM Software Restrictions

4.2.2.3. Lack of Skilled Technicians

4.2.3. Opportunities

4.2.3.1. Remote and Cloud-Based Diagnostics

4.2.3.2. Integration with AI and Data Analytics

4.2.3.3. Growth in Electric and Autonomous Vehicles

4.2.3.4. Expansion in Emerging Automotive Markets

4.2.4. Challenges

4.2.4.1. Cybersecurity Risks in Connected Diagnostics

4.2.4.2. Rapid Technological Evolution

4.3. Technology Landscape

4.3.1. On-Board Diagnostics (OBD-II and Beyond)

4.3.2. Telematics and Remote Diagnostics

4.3.3. AI-Based Fault Detection

4.3.4. Cloud and Edge Diagnostics Platforms

4.3.5. Over-the-Air (OTA) Diagnostics and Updates

4.4. Automotive Diagnostics Ecosystem

4.4.1. OEMs and Tier-1 Suppliers

4.4.2. Diagnostic Tool Manufacturers

4.4.3. Software and Platform Providers

4.4.4. Service Centers and Workshops

4.4.5. Fleet Operators and End Users

4.5. Value Chain Analysis

4.5.1. Component and Hardware Suppliers

4.5.2. Software Developers

4.5.3. Tool Manufacturers

4.5.4. Distributors and Service Providers

4.5.5. End Users

4.6. Regulatory and Standards Landscape

4.6.1. OBD Regulations and Emission Standards

4.6.2. Right-to-Repair Regulations

4.6.3. Data Privacy and Cybersecurity Standards

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Growth in EV Diagnostics Tools

4.8.2. Increasing M&A and Strategic Partnerships

4.8.3. Digitalization of Automotive Service Industry

4.9. Cost and Pricing Analysis

4.9.1. Cost by Tool Type

4.9.2. Subscription-Based Software Models

4.9.3. Lifecycle Cost of Diagnostic Systems

5. Advanced Automotive Diagnostic Tools Market, by Tool Type

5.1. Introduction

5.2. Scan Tools

5.2.1. Handheld Scanners

5.2.2. PC-Based Scanners

5.3. Code Readers

5.4. Diagnostic Software Platforms

5.5. Telematics-Based Diagnostic Systems

5.6. Oscilloscopes and Multimeters

5.7. Battery and EV Diagnostic Tools

6. Advanced Automotive Diagnostic Tools Market, by Connectivity Type

6.1. Introduction

6.2. Wired Diagnostics

6.3. Wireless Diagnostics

6.3.1. Bluetooth

6.3.2. Wi-Fi

6.3.3. Cellular/Cloud Connectivity

7. Advanced Automotive Diagnostic Tools Market, by Vehicle Type

7.1. Introduction

7.2. Passenger Cars

7.3. Commercial Vehicles

7.4. Electric Vehicles (EVs)

7.5. Off-Highway Vehicles

8. Advanced Automotive Diagnostic Tools Market, by Application

8.1. Introduction

8.2. Engine and Powertrain Diagnostics

8.2.1. Engine Control Systems

8.2.2. Transmission Systems

8.3. Emission Diagnostics

8.4. Electrical and Electronic Systems Diagnostics

8.4.1. Battery Management Systems (BMS)

8.4.2. Infotainment and Connectivity Systems

8.5. Safety Systems Diagnostics

8.5.1. ADAS Systems

8.5.2. Airbag and Brake Systems

8.6. Telematics and Remote Diagnostics

8.7. Other Applications

9. Advanced Automotive Diagnostic Tools Market, by End User

9.1. Introduction

9.2. OEM Service Centers

9.3. Independent Repair Shops

9.4. Fleet Operators

9.5. Automotive Dealers

10. Advanced Automotive Diagnostic Tools Market, by Deployment Model

10.1. Introduction

10.2. On-Premises Diagnostics

10.3. Cloud-Based Diagnostics

11. Advanced Automotive Diagnostic Tools Market, by Geography

11.1. Introduction

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. U.K.

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Netherlands

11.3.7. Sweden

11.3.8. Switzerland

11.3.9. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. India

11.4.3. Japan

11.4.4. South Korea

11.4.5. Australia

11.4.6. Indonesia

11.4.7. Thailand

11.4.8. Vietnam

11.4.9. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Colombia

11.5.6. Rest of Latin America

11.6. Middle East & Africa

11.6.1. UAE

11.6.2. Saudi Arabia

11.6.3. South Africa

11.6.4. Turkey

11.6.5. Egypt

11.6.6. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1. Robert Bosch GmbH

13.2. Snap-on Incorporated

13.3. Continental AG

13.4. Delphi Technologies (BorgWarner Inc.)

13.5. DENSO Corporation

13.6. Autel Intelligent Technology Corp., Ltd.

13.7. Launch Tech Co., Ltd.

13.8. Actia Group

13.9. AVL List GmbH

13.10. TEXA S.p.A.

13.11. Softing AG

13.12. KPIT Technologies Ltd.

13.13. Vector Informatik GmbH

13.14. Hickok Incorporated

13.15. Hella GmbH & Co. KGaA

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Nov-2024

Published Date: Sep-2024

Published Date: Jun-2024

Subscribe to get the latest industry updates