Resources

About Us

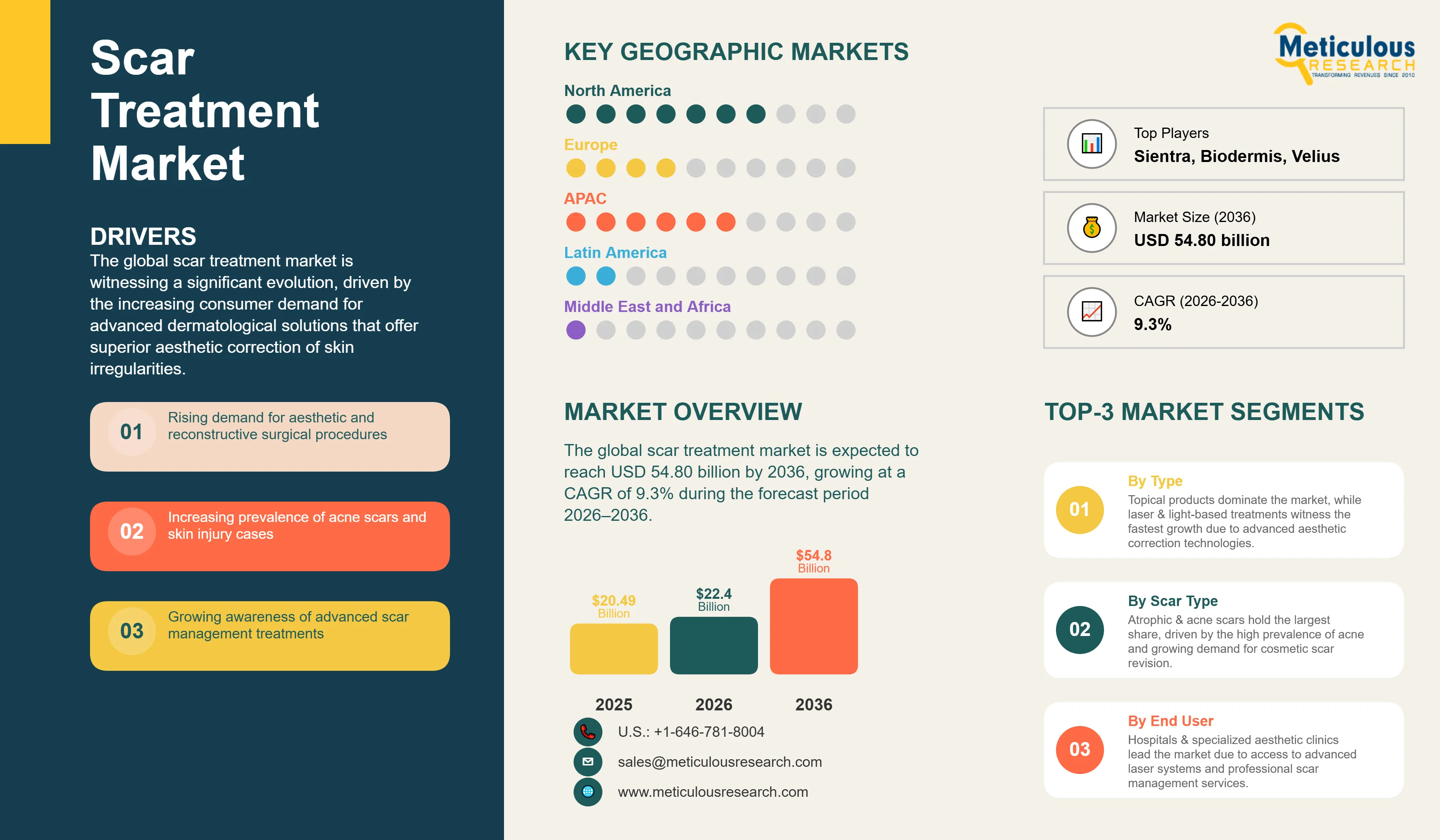

The global scar treatment market is estimated to be USD 22.40 billion in 2026. This market is expected to reach USD 54.80 billion by 2036, growing at a CAGR of 9.3% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global scar treatment market is witnessing a significant evolution, driven by the increasing consumer demand for advanced dermatological solutions that offer superior aesthetic correction of skin irregularities. As a critical component of post-procedural and corrective skincare, scar treatment involves the use of specialized topical, injectable, and light-based therapies to minimize the appearance of atrophic, hypertrophic, and keloid scars. The market is primarily propelled by the rising global volume of surgical procedures and the increasing prevalence of acne-related scarring among younger demographics. Furthermore, the growing social emphasis on aesthetic perfection and the rising availability of specialized aesthetic clinics are broadening the clinical application of these treatments beyond traditional medical necessity. Technological advancements, such as fractional CO2 lasers and high-efficacy silicone-based topical gels, are significantly improving patient outcomes and reducing treatment durations. Clinical guidelines from the American Academy of Dermatology (AAD) and the International Society of Aesthetic Plastic Surgery (ISAPS) continue to emphasize the importance of early and multi-modal scar management protocols. As the industry focuses on developing non-invasive, user-friendly, and cost-effective solutions for home-based and clinical use, the market is expected to witness sustained growth, particularly in emerging economies where the aesthetic medicine infrastructure is rapidly modernizing, ensuring consistent market expansion through 2036.

The growth of the global scar treatment market is primarily driven by the rising volume of surgical procedures and the increasing consumer focus on aesthetic correction in both developed and emerging economies.

Rising Global Volume of Aesthetic and General Surgical Procedures

A major driver for the market is the rising global volume of both aesthetic and general surgical procedures. According to International Society of Aesthetic Plastic Surgery, more than 34.9 million aesthetic procedures were performed globally in 2023, including approximately 15.8 million surgical procedures and 19.1 million non-surgical procedures, reflecting the continued growth of the cosmetic treatment market. Furthermore, the World Health Organization estimates that approximately 1.19 million people die annually from road traffic accidents, while tens of millions sustain non-fatal injuries, many of which require surgical intervention and subsequent scar management. Every surgical procedure, whether performed for medical or aesthetic purposes, carries the risk of post-procedural scarring, creating sustained demand for scar prevention and treatment solutions. The increasing popularity of elective cosmetic procedures, combined with the growing number of trauma-related and general surgeries, is driving demand for topical scar therapies, silicone-based products, injectables, and laser-based treatments. This trend is particularly evident in developed healthcare markets and rapidly expanding healthcare systems across emerging economies.

Growing Social Stigma Associated with Facial Scarring and the Resulting High Demand for Aesthetic Correction

The market is significantly driven by the growing social stigma associated with facial scarring, particularly atrophic and acne scars, which affects a large segment of the adolescent and young adult population. The high psychological impact of visible scarring is encouraging individuals to seek effective aesthetic corrections through both over-the-counter topical solutions and specialized clinical treatments. This patient-driven demand is further bolstered by the increasing influence of social media and the growing availability of specialized aesthetic clinics that offer fractional laser and chemical peel treatments. This focus on aesthetic perfection is making scar treatment a priority for consumers, reinforcing its position as a high-growth segment within the broader dermatological market.

Despite their aesthetic benefits, the scar treatment market faces challenges related to the high cost of advanced laser-based therapies and the lack of comprehensive reimbursement for procedures deemed cosmetic.

Prohibitive Cost of Advanced Fractional Laser and Light-Based Corrective Treatments

A major restraint for the market is the high cost of advanced fractional laser and light-based corrective treatments, which can be prohibitive for a significant segment of the population, particularly in resource-limited settings. While these therapies offer superior aesthetic outcomes for complex and deep scarring, the requirement for multiple sessions and specialized clinical expertise leads to a high overall treatment valuation. This cost barrier often limits the broader adoption of advanced clinical treatments, encouraging a reliance on less expensive, albeit sometimes less effective, topical OTC solutions. The persistent challenge of demonstrating the value of these premium treatments to cost-conscious consumers remains a significant hurdle for manufacturers of high-end aesthetic devices.

Lack of Standardized Reimbursement Policies for Scar Revision Procedures Deemed Cosmetic

The market is also impacted by the lack of standardized reimbursement policies for scar revision procedures that are often deemed cosmetic rather than medically necessary. Many healthcare payers do not provide comprehensive coverage for advanced laser therapies or specialized topical gels unless the scarring results from severe trauma or burns. This lack of financial support increases the out-of-pocket burden for patients, potentially restraining the market's growth among middle-income demographics. Manufacturers and clinicians continue to face challenges in securing broader insurance recognition for scar management as a critical component of post-surgical recovery and psychological well-being, which is essential for unlocking the full market potential.

Future growth opportunities in the scar treatment market are centered on the development of personalized multi-modal treatment protocols and the rapid expansion of specialized aesthetic care in emerging economies.

Integration of Advanced Topical and Energy-Based Therapies for Personalized Scar Management

There is a significant opportunity for market growth driven by the integration of advanced topical treatments with energy-based therapies to create personalized, multi-modal scar management protocols. Clinical research is increasingly demonstrating that combining silicone-based gels with fractional laser treatments or microneedling can lead to superior aesthetic outcomes compared to single-modality therapy. Manufacturers that can provide integrated treatment kits or specialized training for clinicians on how to combine these modalities effectively are well-positioned to lead the premium market segment. This trend toward 'holistic scar revision' represents a high-growth opportunity for industry leaders looking to differentiate their offerings and provide comprehensive clinical solutions.

Rapid Proliferation of Specialized Aesthetic and Dermatology Clinics in the Asia-Pacific Region

The rapid proliferation of specialized aesthetic and dermatology clinics in the Asia-Pacific region represents a major opportunity. Countries like China, India, and South Korea are witnessing a significant increase in the number of private clinics that offer advanced laser-based scar revision and professional-grade topical treatments. Growing awareness of aesthetic procedures among the rising middle-class population is accelerating the demand for both post-procedural and corrective scar solutions. Manufacturers that can provide durable, cost-effective, and high-performance devices and products tailored for these rapidly expanding markets are likely to lead the next phase of global market expansion, capitalizing on the high volume of aesthetic consumers in these populous regions.

Growing Clinical Preference for High-Efficacy Silicone-Based Topical Gels and Sheets

A prominent trend in 2026 is the increasing clinical and consumer preference for high-efficacy silicone-based topical gels and sheets. Silicone has become the undisputed first-line recommendation for preventing and treating hypertrophic and keloid scars due to its non-invasive nature and proven ability to hydrate and flatten scar tissue. Manufacturers are focusing on developing more comfortable, transparent, and long-lasting silicone formulations that enhance patient compliance. This trend is particularly evident in the post-surgical market, where clinicians are increasingly prescribing silicone-based products as a standard part of the recovery protocol, aligning with the global clinical emphasis on improving aesthetic outcomes and patient quality of life.

Increasing Adoption of Non-Invasive Fractional Laser Resurfacing for Complex Scar Revision

The market is witnessing an increasing trend toward the adoption of non-invasive fractional laser resurfacing for the revision of complex and deep scarring. Fractional CO2 and erbium-glass lasers are becoming the preferred choice for clinicians due to their ability to precisely target scar tissue while minimizing damage to the surrounding healthy skin. This trend is driving the demand for advanced aesthetic platforms that offer multiple wavelengths and customizable treatment parameters. The shift toward less invasive clinical procedures with shorter downtime is encouraging more individuals to seek professional scar revision, particularly for atrophic and acne scars, making energy-based therapies a critical driver of the broader corrective dermatology market.

Analysis by Product Type

Based on product type, the topical products segment is expected to hold the largest share of the global scar treatment market in 2026. This leadership is substantiated by its status as the primary first-line treatment recommended by clinical guidelines for post-surgical and minor wound scarring. The high availability of silicone gels and sheets as over-the-counter solutions ensures its dominant market position. However, the laser & light-based treatments segment is projected to register the highest CAGR during the forecast period. The rapid technological advancements in fractional CO2 lasers and the increasing consumer focus on achieving superior aesthetic outcomes for complex scars are driving the rapid adoption of these clinical interventions.

Analysis by Scar Type

By scar type, the atrophic & acne scars segment is expected to hold the largest share in 2026, due to the high global prevalence of acne vulgaris and the resulting high patient demand for aesthetic correction. However, the keloid scars segment is projected to register the highest CAGR during the forecast period. The increasing clinical emphasis on managing these difficult-to-treat lesions through multi-modal therapies and growing awareness of specialized keloid management techniques are significantly boosting demand in this segment.

Analysis by End User

By end user, the hospitals & specialized aesthetic clinics segment is expected to hold the largest share in 2026, as they provide advanced surgical and laser-based revisions that require professional expertise and specialized equipment. However, the home care settings segment is projected to register the highest CAGR during the forecast period. The increasing adoption of professional-grade topical silicone treatments and the growing availability of high-efficacy OTC scar treatment kits are facilitating rapid growth in this segment.

Largest Share: North America

North America is expected to dominate the global scar treatment market in 2026. This leading position is attributed to its advanced aesthetic medicine infrastructure, high consumer spending on personal care, and the presence of major industry players. Data from the ASPS and AAD indicates a high level of consumer awareness regarding scar revision and high adoption rates of both topical and laser-based therapies in the U.S., which is a major factor driving the high regional market valuation and the consistent demand for premium dermatological products in the U.S. and Canada.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global scar treatment market, with a CAGR of 10-12% during the forecast period. This rapid expansion is driven by the rapidly expanding aesthetic medicine market, improving healthcare access, and rising disposable income. Reports from the ISAPS highlight a significant increase in the volume of aesthetic procedures across APAC, directly translating into higher demand for both post-procedural and corrective scar treatment solutions in countries like China, India, and South Korea.

The global scar treatment market is characterized by a high degree of fragmentation, with a diverse range of pharmaceutical companies and aesthetic device manufacturers competing across the topical and clinical segments. Competition is primarily focused on improving the efficacy, aesthetic outcomes, and patient comfort of treatments to capture a larger share of the growing aesthetic correction market. Key players are investing heavily in R&D to develop advanced fractional laser platforms and high-performance silicone formulations that enhance scar maturation. Strategic developments often involve acquisitions of specialized dermatological firms and partnerships with aesthetic medical societies like ISAPS to validate new multi-modal treatment protocols. Furthermore, there is a growing focus on providing comprehensive scar management kits that combine professional-grade topicals with clinical interventions. Manufacturers are also increasingly focusing on robust clinician training programs and direct-to-consumer marketing to build brand awareness and ensure the successful implementation of their systems in specialized clinics and hospital settings, which is critical for maintaining market leadership in this highly competitive field.

Smith & Nephew plc (UK), Bausch Health Companies Inc. (Canada), Lumenis Be Ltd. (Israel), Mölnlycke Health Care AB (Sweden), Perrigo Company plc (Ireland), Hologic, Inc. (Cynosure) (US), Suneva Medical, Inc. (US), Encore Dermatology, Inc. (US), Alliance Pharma plc (UK), Sonoma Pharmaceuticals, Inc. (US), Sientra, Inc. (US), Candela Corporation (US), Merz Pharma GmbH & Co. KGaA (Germany), Scarguard Labs LLC (US), Revitol Corporation (US), Quantum Health (US), Pacific World Corporation (US), Biodermis (US), Velius, LLC (US), AVITA Medical (US)

The global market is estimated at USD 22.40 billion in 2026, with a projected growth to USD 54.80 billion by 2036, at a CAGR of 9.3%.

Primary drivers include the rising volume of surgical procedures and the growing social emphasis on aesthetic perfection.

Major restraints include the high cost of advanced laser treatments and the lack of standardized reimbursement for procedures deemed cosmetic.

Opportunities lie in the development of personalized multi-modal therapies and the proliferation of specialized aesthetic centers in emerging markets.

Topical products are expected to hold the largest share as the primary first-line treatment for post-surgical scarring.

Laser & light-based treatments are projected to grow at the fastest CAGR, driven by rapid technological advancements in aesthetic correction.

Atrophic & acne scars are expected to hold the largest share due to the high global prevalence of acne vulgaris.

North America is expected to dominate the market due to its advanced aesthetic infrastructure and high consumer spending.

Asia-Pacific is projected to witness the fastest growth, fueled by the rapidly expanding aesthetic medicine market and rising disposable income.

Key trends include the increasing adoption of silicone-based topical gels and the rise of non-invasive fractional resurfacing.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholder

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumption

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Global Volume of Aesthetic and General Surgical Procedures

4.2.1.2. Growing Social Stigma Associated with Facial Scarring and the Resulting High Demand for Aesthetic Correction

4.2.2. Restraints

4.2.2.1. Prohibitive Cost of Advanced Fractional Laser and Light-Based Corrective Treatments

4.2.2.2. Lack of Standardized Reimbursement Policies for Scar Revision Procedures Deemed Cosmetic

4.2.3. Opportunities

4.2.3.1. Integration of Advanced Topical and Energy-Based Therapies for Personalized Scar Management

4.2.3.2. Rapid Proliferation of Specialized Aesthetic and Dermatology Clinics in the Asia-Pacific Region

4.2.4. Trends

4.2.4.1. Growing Clinical Preference for High-Efficacy Silicone-Based Topical Gels and Sheets

4.2.4.2. Increasing Adoption of Non-Invasive Fractional Laser Resurfacing for Complex Scar Revision

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Scar Treatment Market, by Product Type

5.1. Topical Products

5.1.1. Silicone Gels & Sheets

5.1.2. Scar Creams & Ointments

5.1.3. Scar Sprays & Oils

5.2. Laser & Light-Based Treatments

5.2.1. Fractional Laser Treatments

5.2.2. Pulsed Dye Laser (PDL) Treatments

5.2.3. Intense Pulsed Light (IPL) Treatments

5.3. Surface Treatments

5.3.1. Chemical Peels

5.3.2. Dermabrasion & Microdermabrasion

5.3.3. Microneedling Treatments

5.4. Injectable Therapies

5.4.1. Corticosteroid Injections

5.4.2. Dermal Fillers

5.4.3. Other Injectable Therapies

6. Global Scar Treatment Market, by Scar Type

6.1. Atrophic & Acne Scars

6.2. Hypertrophic Scars

6.3. Keloid Scars

6.4. Contracture Scars

7. Global Scar Treatment Market, by End User

7.1. Hospitals & Specialized Aesthetic Clinics

7.2. Home Care Settings

8. Global Scar Treatment Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia-Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia-Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Share/Ranking Analysis, By Key Player (2025)

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Smith & Nephew plc

10.2. Bausch Health Companies Inc.

10.3. Lumenis Be Ltd.

10.4. Mölnlycke Health Care AB

10.5. Perrigo Company plc

10.6. Hologic, Inc. (Cynosure)

10.7. Suneva Medical, Inc.

10.8. Encore Dermatology, Inc.

10.9. Alliance Pharma plc

10.10. Sonoma Pharmaceuticals, Inc.

10.11. Sientra, Inc.

10.12. Candela Corporation

10.13. Merz Pharma GmbH & Co. KGaA

10.14. Scarguard Labs LLC

10.15. Revitol Corporation

10.16. Quantum Health

10.17. Pacific World Corporation

10.18. Biodermis

10.19. Velius, LLC

10.20. AVITA Medical

11. Appendix

11.1. Disclaimer

12. Key Questions Answered

Published Date: Jun-2026

Published Date: Jun-2024

Published Date: Jun-2026

Published Date: Jan-2025

Subscribe to get the latest industry updates