Resources

About Us

Dry Eye Treatment Devices Market Size, Share & Trends Analysis by Technology, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

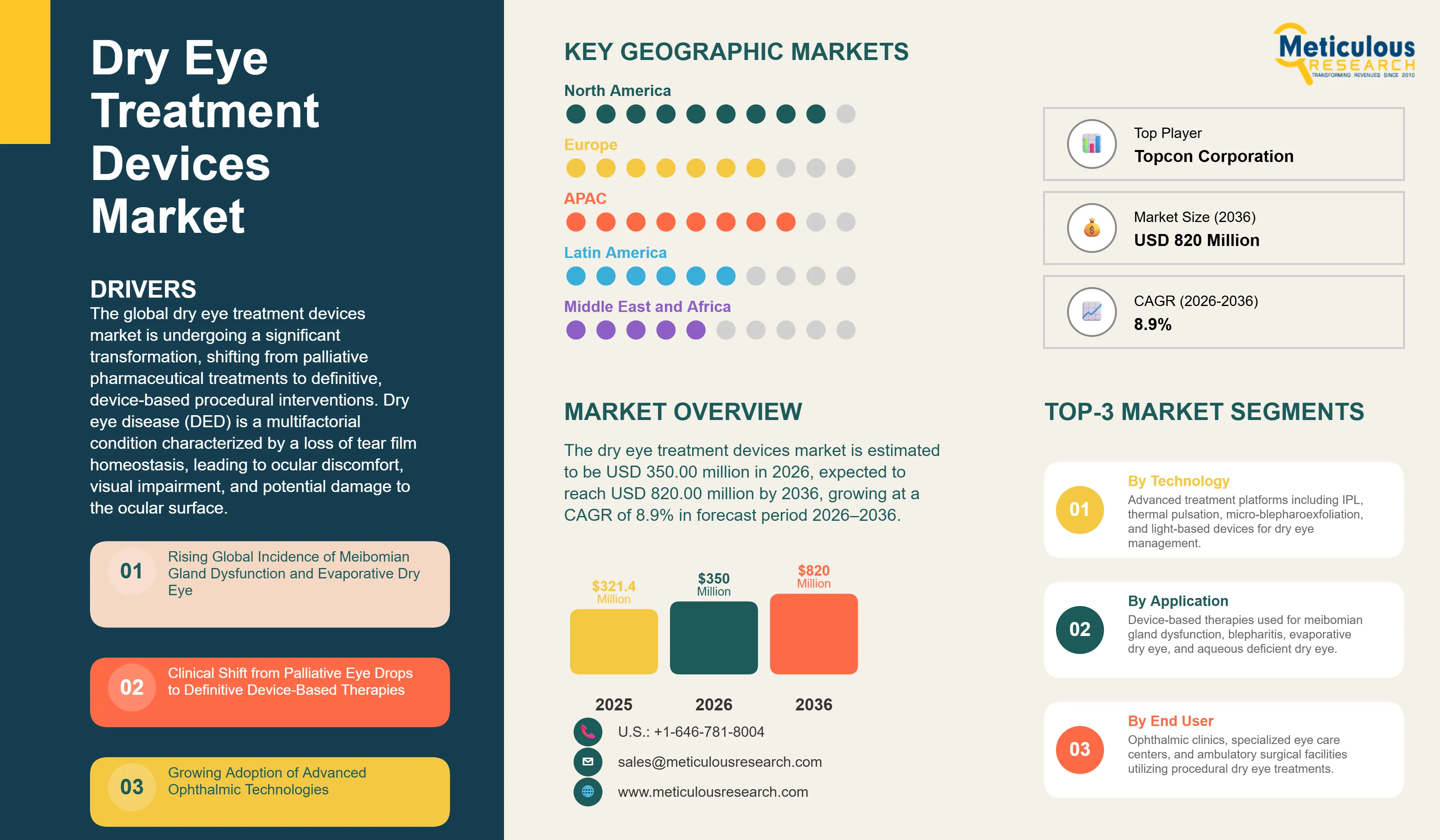

Report ID: MRHC - 1042085 Pages: 285 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global dry eye treatment devices market is estimated to be USD 350.00 million in 2026. This market is expected to reach USD 820.00 million by 2036, growing at a CAGR of 8.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global dry eye treatment devices market is undergoing a significant transformation, shifting from palliative pharmaceutical treatments to definitive, device-based procedural interventions. Dry eye disease (DED) is a multifactorial condition characterized by a loss of tear film homeostasis, leading to ocular discomfort, visual impairment, and potential damage to the ocular surface. This market is primarily driven by the increasing global prevalence of meibomian gland dysfunction (MGD), which is the leading cause of evaporative dry eye. Technological advancements in intense pulsed light (IPL) therapy, thermal pulsation systems, and micro-blepharoexfoliation are providing clinicians with more effective tools to address the root causes of DED rather than just managing symptoms. Clinical guidelines from the Tear Film & Ocular Surface Society (TFOS) and the American Academy of Ophthalmology (AAO) increasingly emphasize the role of in-office procedural treatments for moderate to severe cases. As the global population ages and digital device usage continues to rise, the demand for long-lasting, effective dry eye relief is expected to drive substantial market expansion, particularly in specialized ophthalmic settings.

Drivers: Increasing Prevalence of MGD and the Shift toward Definitive In-Office Procedures

The growth of the global dry eye treatment devices market is primarily driven by the rising incidence of evaporative dry eye and the clinical shift toward procedural interventions that offer sustained symptom relief.

Rising Global Incidence of Meibomian Gland Dysfunction and Evaporative Dry Eye

A major driver for the market is the increasing global prevalence of meibomian gland dysfunction (MGD), one of the leading causes of evaporative dry eye disease. According to the Tear Film & Ocular Surface Society, meibomian gland dysfunction is responsible for approximately 60–86% of dry eye disease cases, making it the most common cause of evaporative dry eye. Furthermore, the National Eye Institute estimates that more than 16 million adults in the United States have been diagnosed with dry eye disease, while global epidemiological studies estimate that dry eye disease affects between 5% and 50% of the world's population, depending on age and diagnostic criteria. Factors such as aging, prolonged digital screen use, environmental stressors, and the increasing prevalence of metabolic disorders are contributing to the growing burden of MGD. As patients increasingly seek effective treatments for chronic ocular discomfort and blurred vision, demand for specialized devices that restore meibomian gland function and improve tear film stability continues to rise, particularly in developed healthcare markets.

Clinical Shift from Palliative Eye Drops to Definitive Device-Based Therapies

The ophthalmic community is witnessing a significant shift in the treatment paradigm for dry eye, moving away from temporary relief provided by artificial tears toward definitive, device-based therapies. Procedural treatments such as thermal pulsation and IPL therapy offer the advantage of addressing the underlying pathophysiology of DED, providing relief that can last for several months. This shift is supported by growing clinical evidence and the inclusion of device-based therapies in professional treatment algorithms. As clinicians and patients alike prioritize long-term outcomes and improved quality of life, the adoption of specialized dry eye treatment devices is expected to accelerate.

Restraints: High Out-of-Pocket Costs and Limited Global Insurance Coverage

Despite their clinical benefits, the adoption of dry eye treatment devices is hindered by high procedure costs and the lack of widespread reimbursement for in-office ocular surface therapies.

Significant Out-of-Pocket Costs for Advanced Procedural Treatments

A major restraint for the market is the high cost associated with advanced device-based dry eye treatments. Many of these procedures, such as thermal pulsation and IPL, require multiple sessions and are often not covered by standard health insurance plans. The resulting high out-of-pocket costs can be a significant barrier for many patients, particularly those in lower-income brackets or regions with limited private insurance coverage. This economic barrier limits the potential patient pool and can slow the overall market penetration of innovative technologies in price-sensitive markets.

Lack of Standardized Reimbursement and Variable Global Regulatory Landscapes

The global dry eye treatment devices market is impacted by the lack of standardized reimbursement codes for many in-office procedural treatments. While some progress has been made in North America, many international markets still categorize these treatments as elective or cosmetic, leading to variable adoption rates. Furthermore, the rigorous regulatory requirements for medical device approval can delay the introduction of new technologies in certain regions. These regulatory and reimbursement challenges create an uneven playing field for manufacturers and can impact the long-term investment in new product development.

Opportunities: Integrating Pre-Operative Ocular Surface Optimization and At-Home Device Expansion

Future growth opportunities in the dry eye treatment devices market are centered on the integration of ocular surface management into surgical workflows and the development of professional-grade at-home devices.

Integration of Dry Eye Management into Pre-Operative Surgical Workflows

There is a massive opportunity for market growth by integrating dry eye management into the pre-operative workflows for cataract and refractive surgeries. It is increasingly recognized that an unstable tear film can lead to inaccurate pre-operative measurements and suboptimal surgical outcomes. By utilizing specialized treatment devices to optimize the ocular surface before surgery, clinicians can improve patient satisfaction and surgical precision. Manufacturers that can successfully position their devices as essential tools for surgical success are likely to see significant adoption in high-volume ophthalmic surgical centers.

Development of Professional-Grade At-Home Dry Eye Treatment Devices

The development of safe and effective professional-grade devices for at-home dry eye management represents a significant opportunity. As patients seek more convenient ways to manage their chronic condition between office visits, there is a growing demand for devices that can provide consistent lid hygiene and thermal therapy. Manufacturers that can bridge the gap between simple warm compresses and complex in-office systems by offering validated at-home devices could tap into a large and growing consumer healthcare segment, supported by professional recommendations from eye care providers.

Growing Adoption of Multimodal and Combination Treatment Platforms

A prominent trend in 2026 is the rise of multimodal treatment platforms that combine different technologies, such as IPL and Low-Level Light Therapy (LLLT), into a single device. These combination systems allow clinicians to address multiple aspects of dry eye pathophysiology—such as inflammation and gland obstruction—simultaneously, leading to improved clinical outcomes and greater procedural efficiency. This trend reflects a broader move toward more comprehensive and integrated ocular surface management solutions.

Increasing Focus on Personalized and Data-Driven Ocular Surface Care

The market is witnessing an increasing focus on personalized care, driven by advanced diagnostic imaging that allows for a more detailed assessment of individual tear film and gland health. This data-driven approach enables clinicians to tailor device-based treatments to the specific needs of each patient, improving the efficacy and safety of interventions. The integration of diagnostic data with treatment parameters is fostering a more precise and effective approach to dry eye management, aligning with the broader trend of precision medicine in ophthalmology.

Analysis by Technology

Based on technology, the intense pulsed light (IPL) technology segment is expected to hold the largest share of the global dry eye treatment devices market in 2026. This dominant position is substantiated by its proven efficacy in managing meibomian gland dysfunction and its widespread adoption by eye care professionals as a versatile clinical tool. Its ability to address both inflammation and gland obstruction ensures its market leadership. However, the thermal pulsation systems segment is projected to register the highest CAGR during the forecast period. The increasing clinical preference for automated, targeted therapies that offer consistent and long-lasting relief from evaporative dry eye symptoms is driving the rapid growth of this segment.

Analysis by Application

By application, the meibomian gland dysfunction (MGD) segment is expected to hold the largest share in 2026. This leadership is driven by the fact that MGD is the primary cause of evaporative dry eye, affecting the majority of the dry eye patient population. The high effectiveness of specialized devices in restoring gland function makes them essential for MGD management. However, the blepharitis segment is projected to grow at the fastest CAGR during the forecast period. The rising clinical awareness of the link between chronic lid inflammation and ocular surface disease, combined with the development of specialized micro-exfoliation devices, is accelerating growth in this application area.

Analysis by End User

By end user, the ophthalmic clinics & specialized centers segment is expected to hold the largest share in 2026. These facilities are the primary setting for advanced dry eye management, offering the specialized diagnostic and treatment infrastructure required for device-based therapies. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing trend toward performing more ocular surface procedures in outpatient settings and the integration of dry eye treatments into surgical workflows are driving the rapid adoption of advanced devices in ASCs.

Geographic Analysis: North American Market Dominance and Asia-Pacific's Rapid Ophthalmic Modernization

Largest Share: North America

North America is expected to dominate the global dry eye treatment devices market in 2026. This leading position is attributed to the high prevalence of dry eye disease, a well-established network of specialized clinics, and the early adoption of innovative procedural treatments. The region benefits from strong patient awareness and a favorable reimbursement environment for certain device-based procedures. Key companies operating in the North America market are Alcon Inc., Johnson & Johnson Vision, Bausch + Lomb Corporation, and Sight Sciences, Inc.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global dry eye treatment devices market, with a CAGR of 10.5% during the forecast period. This rapid expansion is driven by the increasing aging population, rising screen time, and the rapid modernization of ophthalmic care infrastructure in countries like China, Japan, and India. Expanding healthcare access and a growing focus on early ocular surface management are accelerating market adoption. Key companies operating in the Asia Pacific market are Alcon Inc., Johnson & Johnson Vision, Topcon Corporation, and Lumenis Be Ltd.

The global dry eye treatment devices market is characterized by a mix of major global ophthalmic corporations and specialized innovative players focusing on ocular surface health. Competition is primarily focused on improving the efficacy, safety, and ease of use of procedural treatments, with a significant emphasis on developing multimodal platforms that combine different technologies. Key players are investing in clinical validation studies to support the inclusion of device-based therapies in professional treatment algorithms and to secure favorable reimbursement. Strategic developments often involve acquisitions of specialized technology companies by larger ophthalmic firms to expand their ocular surface portfolios. Furthermore, there is a growing focus on developing integrated diagnostic and treatment systems that allow for more personalized and data-driven patient care. Manufacturers are also increasingly focusing on educational initiatives to raise awareness among eye care professionals and patients about the benefits of in-office procedural treatments, which is critical for maintaining market leadership in an increasingly competitive and specialized field.

Alcon Inc. (Switzerland/US), Johnson & Johnson Vision (US), Bausch + Lomb Corporation (Canada/US), Lumenis Be Ltd. (Israel/US), Sight Sciences, Inc. (US), TearScience (Johnson & Johnson) (US), MiBo Medical Group (US), ESW-Vision (France), Quantel Medical (Lumibird Group) (France), BlephEx, LLC (US), Sondermed (Germany), Topcon Corporation (Japan), Oasis Medical, Inc. (US), EssilorLuxottica (TearCheck) (France), SBM Sistemi (Italy), Eye-Light (Espansione Group) (Italy), Lacrimera (Chroma Pharma) (Austria), Bruder Healthcare Company (US), Ocusoft, Inc. (US), Tarsus Pharmaceuticals (US).

The global market is estimated at USD 350.00 million in 2026, with a projected growth to USD 820.00 million by 2036, at a CAGR of 8.9%.

Primary drivers include the rising prevalence of MGD and the clinical shift toward definitive in-office procedural treatments.

Major restraints include high out-of-pocket costs for patients and limited global insurance coverage for procedural treatments.

Opportunities lie in integrating dry eye management into surgical workflows and the development of professional-grade at-home devices.

Intense pulsed light (IPL) technology is expected to hold the largest share due to its proven efficacy and widespread clinical adoption.

The blepharitis segment is projected to grow at the fastest CAGR, driven by rising clinical awareness and specialized treatment devices.

Ophthalmic clinics & specialized centers are expected to hold the largest share as the primary setting for advanced device-based therapies.

North America is expected to dominate the market due to high disease prevalence and early adoption of innovative treatments.

Asia Pacific is projected to witness the fastest growth, fueled by an aging population and rapid modernization of ophthalmic care.

Key trends include the rise of multimodal treatment platforms and the focus on personalized, data-driven ocular surface care.

Published Date: Jun-2026

Published Date: Jun-2024

Published Date: Jan-2025

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates