Resources

About Us

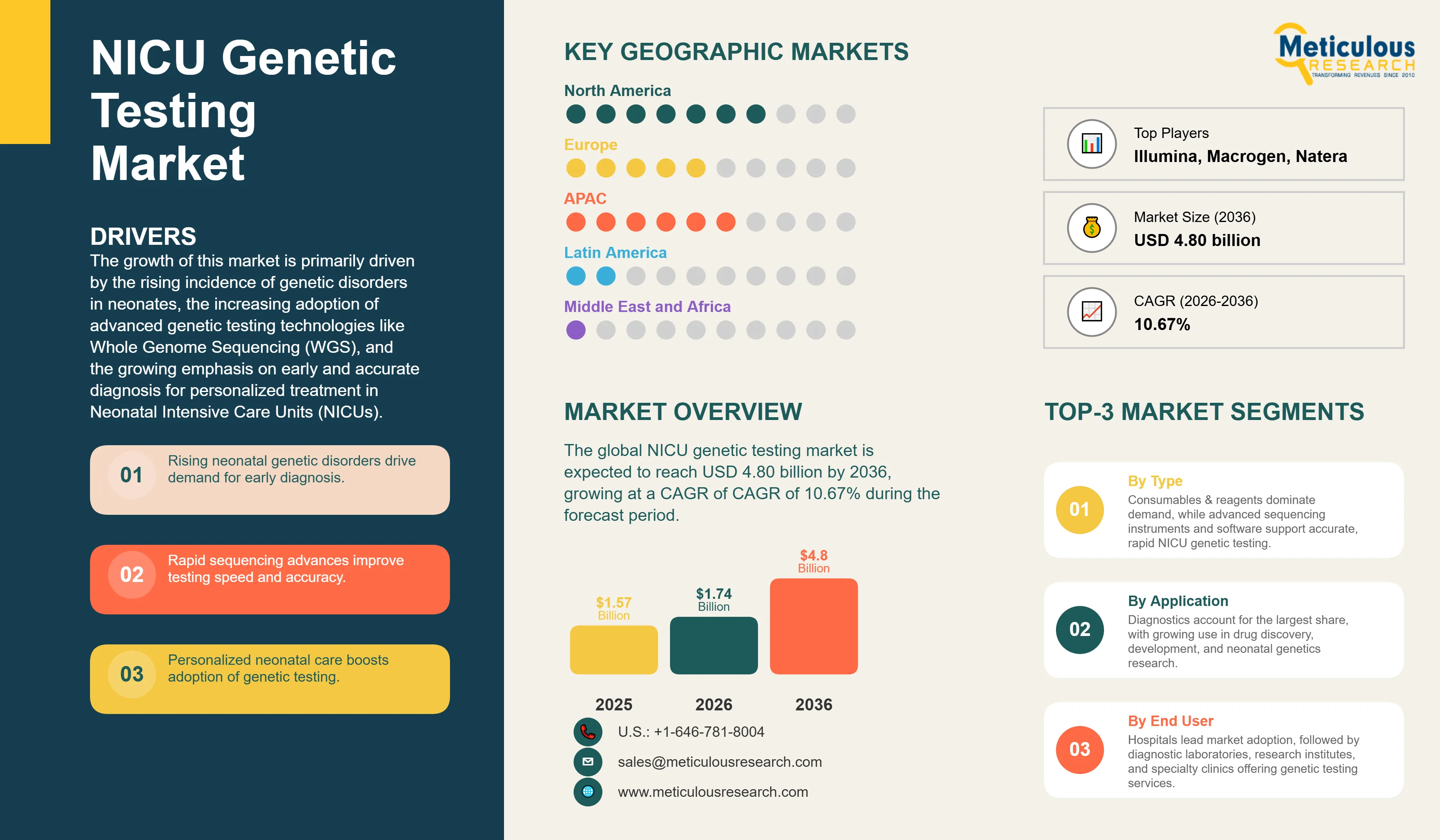

NICU Genetic Testing Market Size, Share & Trends Analysis by Product Type, Scar Type, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

Report ID: MRHC - 1042089 Pages: 265 Jun-2026 Formats*: Excel Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global NICU genetic testing market is estimated to be USD 1.74 billion in 2026. The market is expected to reach USD 4.80 billion by 2036, growing at a CAGR of CAGR of 10.67% during the forecast period. The growth of this market is primarily driven by the rising incidence of genetic disorders in neonates, the increasing adoption of advanced genetic testing technologies like Whole Genome Sequencing (WGS), and the growing emphasis on early and accurate diagnosis for personalized treatment in Neonatal Intensive Care Units (NICUs).

Click here to: Get Free Sample Pages of this Report

NICU genetic testing involves the application of advanced molecular and cytogenetic techniques to diagnose genetic conditions in critically ill newborns. These tests provide crucial information for guiding clinical management, predicting disease progression, and offering prognostic insights for infants in the Neonatal Intensive Care Unit (NICU). According to the World Health Organization, an estimated 240,000 newborns die within the first 28 days of life each year due to congenital disorders, while congenital anomalies account for a significant proportion of neonatal morbidity and mortality worldwide. Early and precise genetic diagnosis can significantly impact treatment decisions, reduce diagnostic odysseys, and improve long-term outcomes for neonates with suspected genetic disorders.

The market encompasses a range of genetic testing modalities, including chromosomal microarray (CMA), next-generation sequencing (NGS) panels, whole exome sequencing (WES), and whole genome sequencing (WGS). According to the Centers for Disease Control and Prevention, birth defects affect approximately 1 in every 33 babies born in the United States, underscoring the importance of early genetic evaluation in neonatal care. The increasing understanding of the genetic basis of neonatal diseases, coupled with technological advancements that enable rapid and comprehensive genetic analysis, is propelling the adoption of these tests. Rapid whole genome and whole exome sequencing are increasingly being integrated into NICU workflows because they enable diagnosis within days rather than weeks, facilitating timely interventions for critically ill newborns. NICU genetic testing plays a vital role in identifying congenital anomalies, metabolic disorders, neurological conditions, and other rare genetic diseases, thereby supporting personalized treatment decisions and improving clinical outcomes.

Drivers

Restraints

Opportunities

Challenges

The global NICU genetic testing market is characterized by several pivotal trends. A significant trend is the increasing adoption of rapid Whole Genome Sequencing (rWGS), which offers the fastest turnaround times for comprehensive genetic diagnosis in critically ill neonates, enabling timely interventions. Another key trend is the growing integration of bioinformatics and artificial intelligence (AI) for automated data analysis and interpretation, improving diagnostic efficiency and accuracy. The market is also witnessing a rise in the development of targeted gene panels for specific neonatal conditions, offering cost-effective and focused diagnostic solutions. Furthermore, there is an increasing emphasis on non-invasive genetic testing (NIPT) approaches, though primarily used prenatally, its advancements are influencing the broader genetic testing landscape. Finally, the expansion of telemedicine and remote genetic counseling services is a notable trend, improving access to expert genetic advice for families in diverse geographic locations.

Analysis by Product Type: Consumables and Reagents Driving Test Volume

Based on product type, the consumables and reagents segment is expected to hold the largest share of the global NICU genetic testing market. This dominance is attributed to the recurring demand for kits, reagents, and other disposables required for each genetic test performed, directly correlating with the increasing volume of tests. The sequencing instruments segment is anticipated to witness the fastest CAGR, driven by the continuous technological advancements in next-generation sequencing platforms, leading to higher throughput, faster turnaround times, and decreasing per-test costs, thereby expanding their adoption in NICU settings.

Analysis by Technology: Next-Generation Sequencing (NGS) at the Forefront

Based on technology, Next-Generation Sequencing (NGS) is expected to command the largest share of the global NICU genetic testing market. NGS platforms, including WES and WGS, offer comprehensive genetic analysis capabilities, enabling the detection of a wide range of genetic variations with high accuracy and speed, making them indispensable for diagnosing complex neonatal conditions. The chromosomal microarray (CMA) segment is anticipated to exhibit a significant CAGR, as it remains a crucial first-line test for detecting chromosomal abnormalities and copy number variations in neonates.

Analysis by Application: Diagnostics Dominating the Market

Based on application, the diagnostics segment is projected to account for the largest share of the NICU genetic testing market. This is due to the primary role of genetic testing in identifying the underlying genetic causes of diseases in critically ill newborns, guiding clinical management, and providing prognostic information. The drug discovery and development segment is expected to grow at the fastest CAGR, fueled by the increasing use of genetic information from NICU patients to understand disease mechanisms and develop targeted therapeutic interventions.

Analysis by End User: Hospitals and Diagnostic Laboratories as Key Adopters

Based on end user, hospitals are expected to command the largest share of the global NICU genetic testing market. NICUs within hospitals are the primary points of care for critically ill newborns, where genetic testing is initiated and managed. The diagnostic laboratories segment is anticipated to exhibit the fastest CAGR, driven by the increasing outsourcing of complex genetic testing to specialized laboratories that possess the necessary infrastructure, expertise, and accreditation for high-throughput analysis.

North America: A Leader in Advanced Neonatal Care and Genetic Diagnostics

North America is expected to hold the largest share of the global NICU Genetic Testing market. This dominance is attributed to a highly developed healthcare infrastructure, significant investments in genetic research and technology, the presence of numerous key market players and specialized diagnostic laboratories, and a robust reimbursement landscape for genetic testing. The United States, in particular, is a major contributor due to its large birth cohort, high prevalence of genetic disorders, and strong adoption of advanced genetic testing modalities in NICUs.

Europe: Advancing Neonatal Genetic Screening with Strong Healthcare Systems

Europe is expected to hold a significant share of the global NICU Genetic Testing market, driven by well-established healthcare systems, increasing government funding for rare disease research, and a growing focus on early diagnosis and intervention for genetic conditions in newborns. Countries like Germany, the U.K., and France are key contributors due to their advanced medical facilities and the presence of leading genetic testing providers. The key companies operating in the European market are Illumina, Inc., Thermo Fisher Scientific Inc., and F. Hoffmann-La Roche AG.

Asia-Pacific: Rapid Growth Fueled by Improving Healthcare Infrastructure and Awareness

Asia-Pacific is projected to witness the fastest CAGR during the forecast period. This rapid growth is driven by improving healthcare infrastructure, increasing birth rates, a rising awareness of genetic disorders, and growing investments in genetic testing technologies in countries like China, India, and Japan. Government initiatives to enhance maternal and child health, coupled with the expanding presence of international genetic testing companies, also contribute to the region's market expansion. The key companies operating in the Asia-Pacific market are BGI Genomics Co., Ltd., Macrogen Inc., and PerkinElmer Inc.

Latin America: Emerging Opportunities in Neonatal Genetic Diagnostics

Latin America is anticipated to witness steady growth in the NICU Genetic Testing market, primarily due to increasing investments in healthcare infrastructure, a rising focus on improving neonatal care outcomes, and growing awareness about genetic disorders in countries like Brazil and Mexico. The modernization of medical facilities and the adoption of international guidelines for genetic screening also contribute to the demand for NICU genetic testing services. The key companies operating in the Latin American market are Thermo Fisher Scientific Inc. (with regional presence) and Illumina, Inc. (with regional presence).

Middle East & Africa: Gradual Expansion with Developing Healthcare Sectors

The Middle East & Africa region is expected to experience gradual growth in the NICU Genetic Testing market, driven by increasing healthcare investments, government initiatives to develop local medical capabilities, and a growing focus on adopting advanced diagnostic technologies. Countries like UAE and Saudi Arabia are investing in genetic research and neonatal care, leading to a gradual increase in demand for NICU genetic testing services. The key companies operating in the Middle East & Africa market are Thermo Fisher Scientific Inc. (with regional presence) and F. Hoffmann-La Roche AG (with regional presence).

The global NICU Genetic Testing market is characterized by a dynamic and highly competitive landscape. It features a mix of large, diversified diagnostic companies, specialized genetic testing providers, and biotechnology firms. Key players are focusing on expanding their test menus, investing in R&D for faster and more comprehensive sequencing technologies, offering integrated bioinformatics solutions, and forming strategic collaborations or acquisitions to strengthen their market positions. The competitive strategy often revolves around demonstrating clinical utility, ensuring rapid turnaround times, providing accurate and reliable results, and offering comprehensive genetic counseling support to healthcare providers and families. Companies are also investing heavily in developing user-friendly platforms and expanding their geographic reach to cater to the growing demand for NICU genetic testing.

The global NICU Genetic Testing market is estimated at USD 1.74 billion in 2026 and is projected to reach USD 4.80 billion by 2036, growing at a CAGR of 10.67%.

The market is driven by the rising incidence of genetic disorders in neonates, technological advancements in genetic sequencing, growing emphasis on personalized medicine, and increasing awareness and acceptance of genetic testing.

Key restraints include the high cost of genetic testing, ethical, legal, and social implications (ELSI), lack of reimbursement policies in some regions, and shortage of skilled professionals.

Opportunities include the integration of Artificial Intelligence (AI) for data interpretation, development of rapid and point-of-care genetic testing, expansion into underserved geographic regions, and strategic collaborations and partnerships.

Challenges include data management and interpretation complexity, standardization and quality control, educating healthcare professionals and families, and regulatory landscape evolution.

Consumables and reagents hold the largest share, while sequencing instruments are expected to grow the fastest.

Next-Generation Sequencing (NGS) commands the largest share, and chromosomal microarray (CMA) is projected to have a significant CAGR.

Diagnostics accounts for the largest share, and drug discovery and development is anticipated to grow the fastest.

Which end-user segment accounts for the largest share, and which is anticipated to grow the fastest?

Hospitals hold the largest share, and diagnostic laboratories are expected to grow the fastest.

North America leads the market, and Asia-Pacific is projected to exhibit the fastest growth.

Key players include Illumina, Inc., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche AG, BGI Genomics Co., Ltd., Macrogen Inc., PerkinElmer Inc., Natera, Inc., Invitae Corporation, Quest Diagnostics, and Laboratory Corporation of America Holdings (LabCorp).

• Illumina, Inc.

• Thermo Fisher Scientific Inc.

• F. Hoffmann-La Roche AG

• BGI Genomics Co., Ltd.

• Macrogen Inc.

• PerkinElmer Inc.

• Natera, Inc.

• Invitae Corporation

• Quest Diagnostics

• Laboratory Corporation of America Holdings (LabCorp)

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: May-2024

Published Date: Apr-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates