Resources

About Us

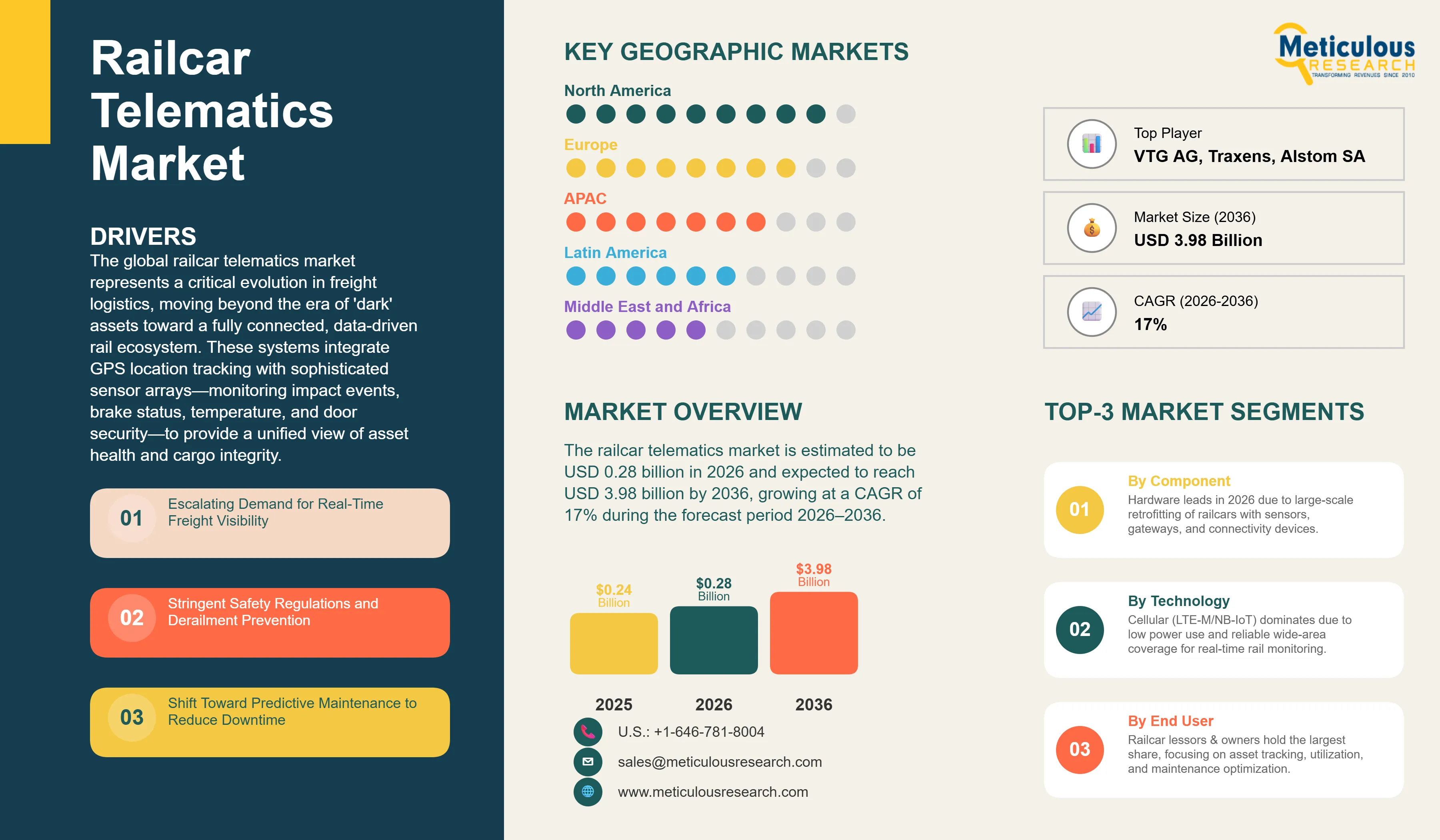

The global railcar telematics market is estimated to be USD 0.28 billion in 2026. This market is expected to reach USD 3.98 billion by 2036, growing at a CAGR of 17% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global railcar telematics market represents a critical evolution in freight logistics, moving beyond the era of 'dark' assets toward a fully connected, data-driven rail ecosystem. These systems integrate GPS location tracking with sophisticated sensor arrays—monitoring impact events, brake status, temperature, and door security—to provide a unified view of asset health and cargo integrity. According to the International Union of Railways, digitalization is essential for improving freight rail reliability, operational efficiency, and customer visibility. Rail transport already plays a vital role in global freight movement, carrying approximately 8% of the world's passengers and 7% of global freight transport activity while accounting for less than 2% of transport-related energy demand, according to the International Energy Agency. As freight operators seek greater asset utilization and supply chain transparency, telematics solutions are becoming increasingly critical. By providing real-time situational awareness, telematics enable rail operators and owners to shift from reactive maintenance to predictive maintenance strategies, reducing unplanned downtime, improving asset availability, and fundamentally transforming the operational dynamics of modern rail networks.

Drivers: Addressing the Global Supply Chain Visibility and Safety Crisis

The growth of the global railcar telematics market is propelled by the urgent need for end-to-end supply chain visibility and the increasing regulatory pressure to enhance rail safety. Shippers today demand the same level of tracking precision for rail freight as they do for road or parcel delivery. Furthermore, high-profile derailments have intensified the focus on monitoring critical components like wheel bearings and braking systems. Telematics solutions provide the continuous data streams necessary to address both operational inefficiencies and safety vulnerabilities, making them an indispensable investment for modern rail operators.

Escalating Demand for Real-Time Asset Visibility and Cargo Integrity

In an era of highly optimized, just-in-time supply chains, the lack of visibility into rail freight movements is a significant operational bottleneck. Shippers require precise estimated times of arrival (ETAs) to manage inventory and coordinate intermodal transfers. Rail asset monitoring systems address this by providing continuous, real-time location data, eliminating the 'black holes' in transit. This enhanced visibility allows shippers and operators to proactively manage delays, optimize yard operations, and significantly improve overall customer satisfaction, driving widespread adoption across the industry.

Stringent Safety Regulations and Proactive Derailment Prevention

Safety remains paramount in the rail industry, particularly concerning the transport of hazardous materials. Regulatory bodies and industry associations like the AAR are increasingly emphasizing the need for proactive safety measures. Railcar telematics play a crucial role by continuously monitoring the health of critical components. Sensors that detect abnormal impacts, excessive vibration, or failing handbrakes can trigger immediate alerts, allowing operators to intervene before a catastrophic failure or derailment occurs. This capability to shift from reactive repairs to proactive safety management is a powerful driver for market growth.

Strategic Shift Toward Predictive Maintenance and Asset Lifecycle Optimization

Unplanned maintenance and out-of-service railcars represent significant revenue losses for owners and operators. Telematics data, when combined with advanced analytics, enables a shift toward predictive maintenance. By analyzing historical performance and real-time sensor data, operators can predict when a component is likely to fail and schedule maintenance during planned downtime. This approach maximizes asset availability, extends the lifespan of the railcars, and optimizes maintenance budgets, providing a clear and compelling return on investment for telematics deployments.

Restraints: Overcoming Capital Expenditure and Interoperability Hurdles

Despite the clear operational benefits, market growth is constrained by high capital requirements and the significant organizational change management needed for enterprise-wide deployment. The global railcar fleet consists of millions of wagons, many of which are decades old and require complex retrofitting. Additionally, the rail industry has historically operated in silos, making the seamless exchange of telematics data between different operators, lessors, and national networks a persistent challenge.

High Initial Capital Investment for Retrofitting Legacy Fleets

The upfront cost of equipping a large fleet of legacy railcars with telematics gateways, sensors, and power management systems is substantial. Beyond the hardware costs, the installation process requires taking assets out of service, resulting in temporary revenue loss. For smaller operators or those with older fleets nearing the end of their lifecycle, justifying this high initial capital expenditure (CAPEX) can be difficult. This financial barrier often leads to phased or delayed rollouts, restraining the overall pace of market growth.

Data Interoperability and Standardization Challenges Across Fragmented Networks

Freight rail operations frequently involve the interchange of cars between different national networks and private operators. However, the lack of universal standards for telematics data formats and communication protocols creates significant interoperability issues. A telematics system installed by one lessor may not seamlessly integrate with the IT infrastructure of the operating railroad. While initiatives by the UIC and UNIFE aim to establish common data models, the current fragmented landscape complicates data sharing and limits the full potential of network-wide visibility.

Opportunities: Leveraging AI and Intermodal Synergy for Market Expansion

The future of the railcar telematics market lies in leveraging advanced technologies to create truly autonomous and highly efficient freight networks. The integration of Artificial Intelligence (AI) with telematics data opens up vast opportunities for automated decision-making and dynamic routing. Furthermore, as global trade increasingly relies on seamless intermodal transport, telematics solutions that provide end-to-end visibility across rail, maritime, and road segments will see massive demand.

Integration of AI and Machine Learning for Autonomous Fleet Orchestration

The massive volume of data generated by connected railcars provides the perfect foundation for AI and machine learning applications. AI algorithms can analyze complex patterns in transit times, yard congestion, and maintenance needs to autonomously orchestrate fleet movements. This could involve dynamically rerouting cars to avoid bottlenecks or automatically dispatching maintenance crews based on predictive alerts. The development of these AI-driven 'smart yards' and autonomous logistics platforms represents a highly lucrative opportunity for telematics vendors.

Growth in Seamless, Multi-Modal Intermodal Transport Solutions

As supply chains become more integrated, the demand for telematics solutions that transcend single modes of transport is growing. Railcar telematics providers have a significant opportunity to develop hybrid systems that seamlessly track assets as they move from rail networks to ports and onto trucks. By offering unified dashboards that provide true end-to-end visibility, vendors can capture a larger share of the broader supply chain digitalization market, appealing to major global shippers and logistics integrators.

Industry-Wide Collaborative Data Initiatives (e.g., RailPulse)

A defining trend in 2026 is the rise of collaborative initiatives like RailPulse. This coalition of railcar owners, builders, and operators aims to accelerate the adoption of telematics by establishing a neutral, open-architecture infrastructure for data sharing. By pooling resources and standardizing data access, such initiatives overcome interoperability hurdles and create a unified ecosystem for rail asset monitoring. This collaborative approach is expected to significantly accelerate market penetration and set a precedent for other regions.

Advancements in Energy-Harvesting and Autonomous Power Solutions

Powering telematics devices on unpowered rail freight wagons has always been a challenge. A major trend is the rapid advancement in energy-harvesting technologies, particularly robust solar panels and kinetic energy recovery systems. These innovations allow telematics gateways and sensors to operate autonomously for years without battery replacements. This 'install and forget' capability drastically reduces the total cost of ownership and makes fleet-wide deployments much more economically viable.

Analysis by Component

Based on component, the hardware segmentis expected to hold the largest share in 2026. This dominance is driven by the fundamental necessity of equipping millions of 'dark' railcars with physical devices, such as gateways, impact sensors, brake monitors, and solar power units, to initiate data collection. Hardware remains the primary revenue generator during the initial massive retrofitting phase of legacy fleets. However, the software/platform segment is projected to register the highest CAGR during the forecast period. As the installed base of hardware matures, the value shifts toward the software platforms that analyze this data. Advanced fleet management dashboards, predictive maintenance algorithms, and AI-driven orchestration services are becoming the primary differentiators, offering recurring revenue and higher margins for vendors.

Analysis by Technology

By technology, the cellular (LTE-M/NB-IoT) segment is expected to hold the largest share in 2026. These low-power wide-area networks provide the ideal balance of broad regional coverage, low data transmission costs, and minimal power consumption, making them perfectly suited for continuous rail asset monitoring across national networks. However, the satellite & hybrid connectivity segment is projected to grow at the fastest CAGR during the forecast period. The expansion of LEO satellite constellations and the increasing need for seamless global intermodal tracking, especially for remote cross-border transit and deep-sea visibility, are driving the adoption of hybrid devices that can switch between networks to ensure uninterrupted connectivity.

Analysis by End User

By end user, the railcar lessors & owners segment is expected to hold the largest share in 2026. Companies that own and lease large fleets of railcars (e.g., GATX, VTG) are the primary investors in telematics, using the technology to monitor asset health, ensure lease compliance, and offer value-added data services to their clients. However, the shippers & industrial manufacturers segment is projected to register the highest CAGR during the forecast period. Direct demand from shippers in industries such as Chemicals, Energy, and Agriculture for end-to-end visibility and cargo integrity is skyrocketing. Shippers are increasingly bypassing traditional carriers to manage their own digital supply chain visibility, driving rapid adoption of telematics solutions.

Geographic Analysis: Regional Growth Dynamics and Market Dominance

North America

North America is expected to dominate the global railcar telematics market in 2026, holding the largest market share of approximately 36%. This dominance is underpinned by the massive scale of its freight rail network and the high proportion of privately owned railcars requiring advanced monitoring. Initiatives like RailPulse are rapidly accelerating the standardization and adoption of telematics across the continent. The focus on improving network velocity and the stringent safety standards enforced by the AAR further drive the demand for advanced asset monitoring. The key companies operating in the North America market are Wabtec Corporation, Orbcomm Inc., Amsted Digital Solutions, and The Greenbrier Companies.

Europe

Europe is expected to hold a significant share of the global market in 2026. The European market is heavily influenced by the push for interoperability and modernization led by organizations like the UIC and UNIFE. The transition toward Digital Automatic Coupling (DAC) is a major catalyst, as it inherently requires advanced telematics and power distribution across freight trains. The region's strong environmental policies also favor the optimization of rail freight to reduce carbon emissions. The key companies operating in the Europe market are Nexxiot AG, Siemens Mobility, Knorr-Bremse AG, and VTG AG.

Asia Pacific

The Asia Pacific region is projected to witness the fastest growth during the forecast period, with a CAGR of approximately 10.2%. This rapid expansion is driven by massive investments in rail infrastructure, particularly in China and India, where dedicated freight corridors are being developed. The modernization of these vast networks includes the integration of digital tracking and predictive maintenance technologies to handle increasing freight volumes efficiently. The key companies operating in the Asia Pacific market are Advantech Co., Ltd., Dot Telematics, and various regional technology integrators.

Latin America

Latin America is anticipated to experience steady growth, supported by the modernization of rail networks dedicated to the export of agricultural products and mining commodities. The inclusion of Mexico in this region highlights the importance of cross-border rail logistics and the need for secure, trackable freight movements. The key companies operating in the Latin America market are Orbcomm Inc. and regional telematics providers.

Middle East & Africa

The Middle East & Africa region will see gradual adoption, primarily driven by investments in new rail corridors designed to connect mining operations and ports, where asset security and operational efficiency are critical. The key companies operating in the Middle East & Africa market are Nexxiot AG and global integrators.

The global railcar telematics market is highly competitive, featuring a mix of specialized rail technology providers, global IoT companies, and major railcar manufacturers. Key players are focusing on developing comprehensive, end-to-end solutions that combine ruggedized hardware with sophisticated, AI-driven analytics platforms. Strategic partnerships and acquisitions are common as companies seek to expand their technological capabilities and geographic reach. Furthermore, collaboration with industry consortia like RailPulse is becoming a crucial strategy for vendors to ensure their solutions align with emerging data standards and interoperability requirements, thereby securing long-term market relevance.

The global Railcar Telematics market is estimated to be approximately USD 0.82 billion in 2026, with a projected growth to USD 3.98 billion by 2036, at a CAGR of 17%.

Key drivers include the escalating demand for real-time freight visibility, stringent safety regulations and derailment prevention, and the shift toward predictive maintenance to reduce downtime.

Restraints include the high capital expenditure required for retrofitting legacy fleets and ongoing data interoperability and standardization issues across fragmented rail networks.

Opportunities lie in the integration of AI for autonomous railcar orchestration and the growth in seamless, end-to-end intermodal transport solutions.

The hardware segment is expected to hold the largest share due to the foundational need for physical sensors and gateways, while the software/platform segment is projected for the fastest growth.

Cellular technologies (LTE-M/NB-IoT) are expected to grow at the fastest CAGR, providing cost-effective, low-power connectivity for continuous regional tracking.

The railcar lessors & owners segment is expected to hold the largest share, as they invest heavily to monitor asset health and offer data-enriched leasing services.

North America is expected to dominate the market due to its massive freight rail network, high private railcar ownership, and industry initiatives like RailPulse.

Asia Pacific is projected to witness the fastest growth, fueled by massive investments in rail infrastructure and dedicated freight corridors in China and India.

Key trends include industry-wide collaborative data-sharing initiatives and rapid advancements in energy-harvesting sensor technology for unpowered wagons.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Escalating Demand for Real-Time Freight Visibility

4.2.1.2. Stringent Safety Regulations and Derailment Prevention

4.2.1.3. Shift Toward Predictive Maintenance to Reduce Downtime

4.2.2. Restraints

4.2.2.1. High Capital Expenditure for Retrofitting Legacy Fleets

4.2.2.2. Data Interoperability and Standardization Issues

4.2.3. Opportunities

4.2.3.1. Integration of AI for Autonomous Railcar Orchestration

4.2.3.2. Growth in Seamless Intermodal Transport Solutions

4.2.4. Trends

4.2.4.1. Industry-Wide Collaborative Initiatives (e.g., RailPulse)

4.2.4.2. Advancements in Energy-Harvesting Sensor Technology

4.3. Porter's Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Railcar Telematics Market, by Component

5.1. Hardware

5.1.1. Telematics Gateways/Communication Units

5.1.2. Sensors

5.1.2.1. Impact/Shock Sensors

5.1.2.2. Door/Hatch Sensors

5.1.2.3. Brake Status Sensors

5.1.2.4. Temperature Sensors

5.1.2.5. Load/Empty Sensors

5.1.3. Power Management Units

5.2. Software/Platform

5.2.1. Fleet Management Platforms

5.2.2. Predictive Maintenance Analytics

5.2.3. API & Integration Services

6. Global Railcar Telematics Market, by Technology

6.1. Cellular (LTE-M/NB-IoT)

6.2. Satellite Tracking

6.3. Short-Range Wireless (BLE/RFID/NFC)

6.4. Hybrid Connectivity

7. Global Railcar Telematics Market, by End User

7.1. Railcar Lessors & Owners

7.2. Rail Operators/Carriers

7.3. Shippers & Industrial Manufacturers

8. Global Railcar Telematics Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Key Players Strategies

9.2. Market Share Analysis

9.3. Strategic Developments

9.4. Competitive Benchmarking

10. Company Profiles

10.1. Wabtec Corporation

10.2. Nexxiot AG

10.3. Orbcomm Inc.

10.4. Intermodal Telematics (IMT)

10.5. Amsted Digital Solutions

10.6. Siemens Mobility

10.7. Knorr-Bremse AG

10.8. Trinity Industries

10.9. The Greenbrier Companies

10.10. GATX Corporation

10.11. VTG AG

10.12. Savvy Telematic Systems

10.13. Traxens

10.14. Globe Tracker

10.15. Dot Telematics

10.16. ZF Friedrichshafen AG

10.17. Advantech Co., Ltd.

10.18. Aptiv PLC (Ireland/Global)

10.19. Alstom SA (France)

10.20. Sensata Technologies (US)

11. Appendix

11.1. References

11.2. Disclaimer

12. Key Questions Answered

Published Date: Jun-2026

Published Date: Feb-2024

Published Date: Feb-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates