Resources

About Us

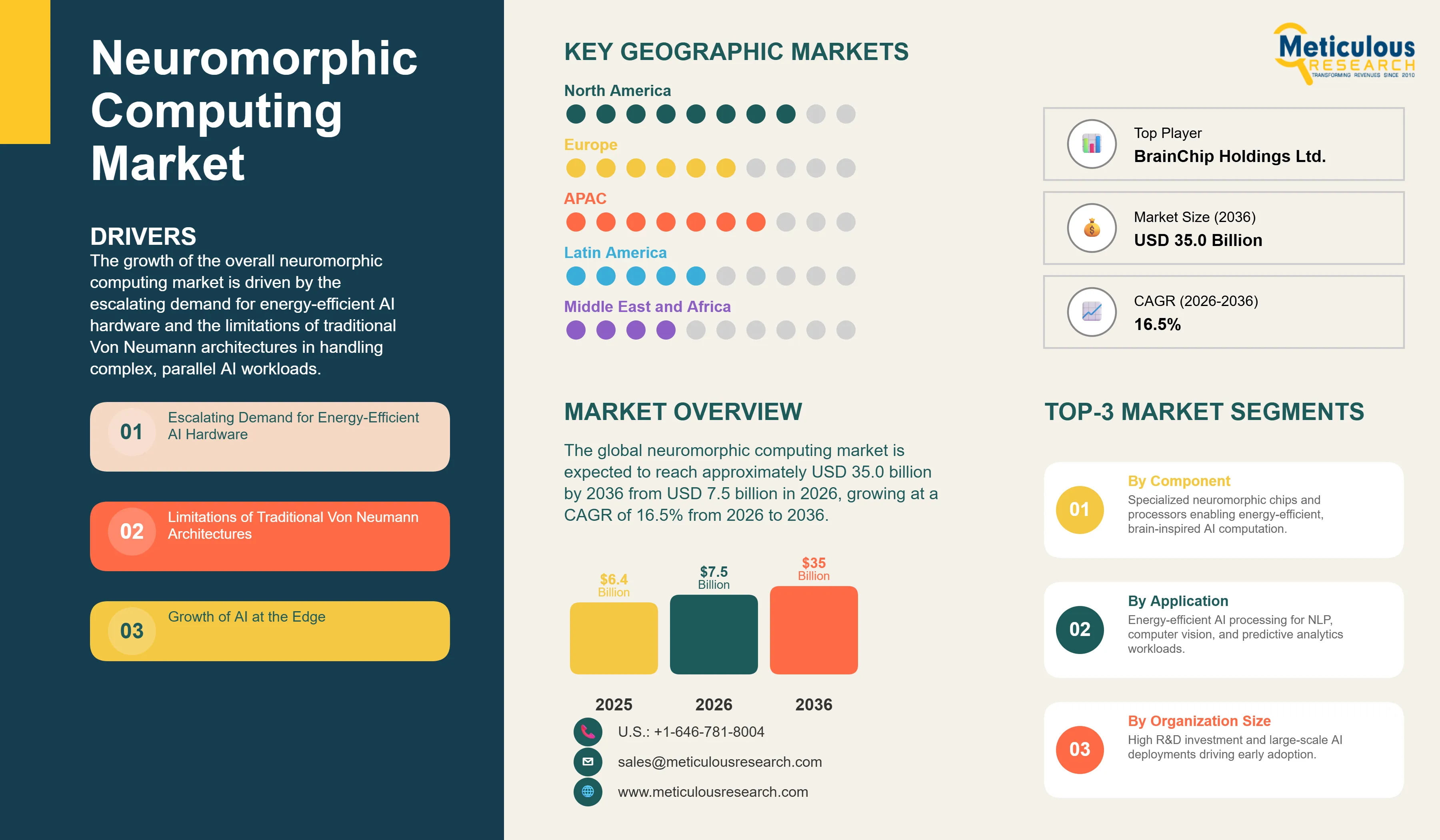

The global neuromorphic computing market was valued at USD 6.4 billion in 2025. The market is expected to reach approximately USD 35.0 billion by 2036 from USD 7.5 billion in 2026, growing at a CAGR of 16.5% from 2026 to 2036.

The growth of the overall neuromorphic computing market is driven by the escalating demand for energy-efficient AI hardware and the limitations of traditional Von Neumann architectures in handling complex, parallel AI workloads. As organizations increasingly deploy AI at the edge, the need for brain-inspired architectures that deliver high performance with minimal power consumption has become critical. The expansion of IoT ecosystems, the rise of autonomous systems, and the pursuit of more biologically plausible AI models are further compelling enterprises and research institutions to transition toward neuromorphic platforms. At the same time, the rapid development of spiking neural networks (SNNs) and event-driven processing is reinforcing the need for hardware that can natively support these advanced computational paradigms—a capability that neuromorphic chips are uniquely positioned to provide.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Neuromorphic computing is a cloud-to-edge architecture that converges brain-inspired hardware and specialized software frameworks into a single, highly efficient computational platform. These platforms integrate core capabilities such as spiking neural networks (SNNs), event-driven processing, and massive parallelism into a unified engine that mimics the neural structure and operation of the biological brain. The market is defined by a decisive shift from traditional, power-hungry CPUs and GPUs toward neuromorphic chips capable of delivering consistent performance and optimal energy efficiency across robotics, autonomous systems, and distributed IoT environments simultaneously.

The market encompasses a diverse range of solution architectures, from specialized neuromorphic processors serving research and academic institutions to fully integrated edge AI platforms that replace legacy computing stacks in industrial and automotive applications. These platforms are increasingly embedded with autonomous learning and adaptive capabilities that automate pattern recognition, dynamically adjust neural weights, and provide proactive decision-making across complex environments. The ability to deliver real-time threat detection, granular sensory processing, and continuous cognitive monitoring from a single, low-power platform has made neuromorphic technology the architecture of choice for organizations that require both operational agility and computational resilience.

The global computing environment is undergoing fundamental transformation, driven by the intersection of AI-first application strategies, edge computing permanence, and escalating data processing requirements. This transformation has dramatically accelerated the retirement of traditional, linear processing models, with organizations prioritizing unified neuromorphic platforms that can enforce energy-efficient execution, automate complex tasks, and maintain performance across geographically dispersed operations. The rapid growth in autonomous systems development, edge-native application deployment, and AI-driven workloads is further reinforcing neuromorphic computing as the foundational architecture for the modern digital enterprise.

The neuromorphic landscape is undergoing a significant shift as leading vendors embed autonomous learning and adaptive capabilities directly into their core chip architectures rather than offering them as static hardware components. Intel’s Loihi 2, for instance, integrates programmable neurons that allow researchers to implement diverse spiking neural network models, automatically identifying and optimizing neural connections based on real-time data input. Similarly, IBM’s TrueNorth architecture enables real-time analysis of sensory data and behavior patterns, generating precise cognitive responses that trigger automated actions without external intervention. This intelligence-led approach is transforming neuromorphic computing from a passive processing layer into an active, self-optimizing fabric capable of learning and adapting before new data materializes. As adaptive capabilities become a primary differentiation factor, vendors that embed autonomous learning and response workflows into their neuromorphic stacks are gaining a measurable competitive edge over those offering traditional fixed-function solutions.

Enterprise and research buyers are rapidly abandoning fragmented, multi-chip approaches in favor of fully integrated neuromorphic ecosystems that deliver hardware, development tools, and pre-trained models through one unified framework. The complexity, programming overhead, and integration costs associated with stitching together separate neuromorphic components from different vendors have become untenable as AI environments grow more complex and dynamic. BrainChip has pioneered this approach with its Akida neuromorphic platform, offering edge devices, industrial sensors, and automotive systems a consistent AI experience managed from a single development environment. SynSense has reinforced this trend by consolidating its Speck and Xylo offerings under a unified software-hardware stack, delivering event-driven vision, low-power audio processing, and AI-powered threat protection through a single platform and licensing framework. According to industry analysis, by 2030, 60% of neuromorphic hardware purchases are expected to be part of an integrated ecosystem offering, up from approximately 20% in 2025—a trajectory that is fundamentally reshaping vendor competitive dynamics and buyer procurement strategies across the market.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 35.0 Billion |

|

Market Size in 2026 |

USD 7.5 Billion |

|

Market Size in 2025 |

USD 6.4 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 16.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Application, End-use Vertical, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

A fundamental driver of the neuromorphic computing market is the broad organizational move away from legacy, power-intensive computing architectures toward energy-efficient frameworks that enable AI at the network edge. The normalization of distributed AI has made traditional cloud-dependent and GPU-heavy infrastructure structurally inadequate, as organizations now require secure, low-latency access to AI capabilities for devices spread across factories, vehicles, hospitals, and remote mobile environments. The increasing focus on sustainability and the European Union’s Green Deal mandates are accelerating this transition significantly in Europe, while similar initiatives are gaining traction across North America and Asia-Pacific. These factors are establishing neuromorphic computing not as an optional modernization initiative but as a necessity for the next generation of AI, driving research timelines and budget allocations across automotive, healthcare, and industrial sectors.

The explosive growth of autonomous systems and the rapid proliferation of brain-computer interfaces (BCIs) and neuroprosthetics present a substantial growth opportunity for the neuromorphic computing market. Autonomous navigation requires ultra-low-latency, high-bandwidth connectivity between sensory nodes and processing units—an environment where legacy computing architectures introduce unacceptable performance bottlenecks. Neuromorphic platforms, with their event-driven processing and biologically inspired efficiency, are uniquely suited to deliver the performance, responsiveness, and reliability required for autonomous operations. Furthermore, the increasing deployment of connected neuroprosthetic devices in healthcare creates new frontiers for direct brain-machine interaction that require real-time signal processing and continuous adaptation—capabilities that modern neuromorphic platforms deliver through high-density neural architectures and unified learning models.

The hardware segment accounts for the largest share of the overall neuromorphic computing market in 2026. This dominance is primarily driven by the urgent enterprise and research need to replace traditional processors with specialized neuromorphic chips that can natively execute brain-inspired algorithms. The hardware bundle—combining neuromorphic processors, specialized memory architectures, and high-speed interconnects—addresses the most pressing computational challenges of the AI-first enterprise, including excessive power consumption, high latency, and data movement bottlenecks. Large-scale hardware deployments by automotive manufacturers, defense agencies, and research institutions are reinforcing this segment’s leadership position, with vendors like Intel, IBM, and BrainChip continuing to expand their hardware capability sets through higher neuron densities and broader integration features.

The Software segment, which encompasses development tools, programming frameworks, and pre-trained models, is expected to grow at the fastest rate during the forecast period. As enterprises consolidate their neuromorphic procurement, the role of software in enabling the effective use of specialized hardware is becoming more critical, with vendors increasingly bundling robust development environments and SNN libraries into their platform tiers rather than selling hardware in isolation.

The artificial intelligence segment holds the largest market share in 2026, driven by the growing enterprise recognition that traditional computing architectures are reaching their physical limits in handling the scale and complexity of modern AI models. A unified neuromorphic platform allows AI developers to manage all functions—from pattern recognition and NLP to computer vision and predictive analytics—with consistent energy efficiency and a single point of accountability for performance outcomes. Vendors such as Intel, IBM, and BrainChip have continued to invest heavily in deepening the integration of their hardware with popular AI frameworks, reinforcing this segment’s appeal.

The Robotics segment continues to serve enterprises with specific real-time processing requirements that make traditional computing impractical. However, as neuromorphic platforms mature and their ability to handle complex sensory-motor tasks becomes more proven, the robotics approach is expected to witness significant growth, gradually becoming a primary application for neuromorphic technology across most industrial segments during the forecast period.

The Large Enterprises and Research Institutions segment commands the largest share of the global neuromorphic computing market in 2026. This dominance is primarily driven by the significant capital investment required for neuromorphic hardware development and deployment, coupled with the extensive R&D capabilities and complex AI workloads inherent to these organizations. Large enterprises, particularly in automotive, aerospace, and industrial manufacturing, are investing heavily in neuromorphic solutions for advanced robotics, autonomous systems, and real-time data processing. Similarly, leading research institutions and universities are at the forefront of neuromorphic algorithm development and application exploration, often in collaboration with industry players. Their ability to fund long-term projects, attract top talent, and leverage existing infrastructure positions them as early adopters and key drivers of market growth.

The Small and Medium Enterprises (SMEs) segment is expected to witness steady growth during the forecast period. While SMEs may face challenges in initial investment and technical expertise, the increasing availability of cloud-based neuromorphic platforms and more accessible development kits is lowering the barrier to entry. As neuromorphic technology matures and becomes more standardized, SMEs are anticipated to adopt these solutions for specialized edge AI applications, smart sensor integration, and optimized industrial automation processes, particularly in niche markets where energy efficiency and real-time processing are critical competitive advantages.

The automotive vertical commands the largest share of the global neuromorphic computing market in 2026. This leadership stems from the sector’s combination of stringent performance requirements—including real-time perception, low power consumption, and high reliability—and the rapid move toward autonomous driving. Automotive manufacturers manage vast volumes of sensory data from cameras, lidar, and radar across globally distributed vehicle fleets, making consistent, low-latency processing and real-time decision-making a non-negotiable operational requirement. Neuromorphic platforms that deliver continuous environmental monitoring, granular object detection, and automated incident response are particularly compelling for automotive firms seeking to meet safety mandates without compromising vehicle range or battery life.

The IT and telecom vertical is poised for steady growth through 2036, fueled by the sector’s role as both a primary neuromorphic consumer and a major delivery channel for edge AI services. The healthcare vertical is also emerging as a high-growth segment, driven by the rapid expansion of neuroprosthetics, connected medical device deployments, and the stringent data protection requirements of modern medical regulations.

North America holds the largest share of the global neuromorphic computing market in 2026. This dominance is primarily attributable to the region’s high concentration of leading neuromorphic solution providers, mature AI research ecosystem, and strong government impetus driving advanced computing adoption across both public and private sectors. The United States alone accounts for the majority of regional revenue, with federal initiatives like the National AI Research Resource and DARPA’s advanced computing programs accelerating research timelines across government and defense. The presence of established vendors including Intel, IBM, Qualcomm, and Hewlett Packard Enterprise, alongside a well-developed ecosystem of research institutions and systems integrators, provides North American enterprises with robust access to mature, fully supported neuromorphic deployments.

Asia-Pacific is the fastest-growing regional market for neuromorphic computing during the forecast period, driven by rapid industrial automation investment across China, India, Japan, and South Korea. The region’s large and rapidly digitizing manufacturing base, combined with growing awareness of energy-efficient AI and evolving smart city regulations, is creating strong demand for neuromorphic platforms that can scale with the pace of digital transformation. Governments across the region are also actively promoting advanced semiconductor frameworks aligned with AI principles, further accelerating enterprise adoption.

Europe represents a substantial and steadily growing share of the global neuromorphic computing market, shaped by the continent’s stringent sustainability and privacy regulations, including the European AI Act and the Green Deal. The requirement for energy-efficient processing and secure, local data handling is driving European enterprises to prioritize neuromorphic vendors with a focus on low-power architectures and transparent AI operations. Germany, the United Kingdom, France, and Switzerland are among the most active adoption markets, supported by a mature research landscape and a well-developed ecosystem of regional technology providers.

Companies such as Intel Corporation, IBM Corporation, BrainChip Holdings Ltd., Qualcomm Technologies, Inc., and GrAI Matter Labs lead the global neuromorphic computing market with comprehensive, integrated platforms that combine hardware, software, and development tools. Meanwhile, players including SynSense AG, Vicarious AI, Samsung Electronics Co., Ltd., and Hewlett Packard Enterprise Company focus on specific architectural niches—such as event-driven vision, biologically inspired learning, and high-performance edge computing—targeting enterprises with particular performance preferences or existing research relationships. Emerging and expanding providers such as Applied Brain Research Inc., General Vision Inc., Koniku Inc., and Prophesee SA are strengthening their market positions through innovations in SNN algorithms, neuro-inspired sensing, and purpose-built offerings for industrial and medical applications.

The global neuromorphic computing market is expected to grow from USD 7.5 billion in 2026 to USD 35.0 billion by 2036.

The global neuromorphic computing market is projected to grow at a CAGR of 16.5% from 2026 to 2036.

The hardware segment is expected to dominate the market in 2026 due to its foundational role in enabling brain-inspired computation through specialized chips. The software segment is projected to accelerate its growth as enterprises demand more robust development tools and SNN frameworks to utilize neuromorphic hardware effectively.

AI is transforming neuromorphic computing by enabling platforms to move beyond traditional processing toward autonomous learning, real-time adaptation, and predictive cognitive management. Leading vendors are embedding spiking neural network models, adaptive learning algorithms, and event-driven processing directly into their core chip architectures, enabling enterprises to significantly reduce power consumption and latency while minimizing reliance on traditional computing paradigms.

North America holds the largest share of the global neuromorphic computing market in 2026. The region’s dominance is primarily driven by the high concentration of leading solution providers, strong government research funding, and mature enterprise adoption of advanced AI architectures.

The leading companies include Intel Corporation, IBM Corporation, BrainChip Holdings Ltd., Qualcomm Technologies, Inc., GrAI Matter Labs, and SynSense AG.

1. Introduction

1.1 Market Definition

1.2 Market Scope

1.3 Research Methodology

1.4 Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3 Impact of Brain-Inspired Architectures and AI on Neuromorphic Adoption

3.4 Regulatory Landscape and Compliance Requirements

3.5 Porter’s Five Forces Analysis

4. Global Neuromorphic Computing Market, by Component

4.1 Introduction

4.2 Hardware

4.2.1 Neuromorphic Processors/Chips

4.2.2 Neuromorphic Memory

4.2.3 Interconnects and Sensors

4.3 Software

4.3.1 Development Tools and SDKs

4.3.2 Programming Frameworks

4.3.3 SNN Libraries and Models

4.4 Services

4.4.1 Consulting and Design Services

4.4.2 Integration and Support Services

5. Global Neuromorphic Computing Market, by Application

5.1 Introduction

5.2 Artificial Intelligence

5.2.1 Pattern Recognition

5.2.2 Natural Language Processing

5.2.3 Computer Vision

5.2.4 Predictive Analytics

5.3 Robotics

5.3.1 Industrial Robots

5.3.2 Service Robots

5.4 Autonomous Systems

5.4.1 Autonomous Vehicles

5.4.2 Unmanned Aerial Vehicles (UAVs)

5.5 Data Analytics and Signal Processing

6. Global Neuromorphic Computing Market, by Organization Size

6.1 Introduction

6.2 Large Enterprises and Research Institutions

6.3 Small and Medium Enterprises (SMEs)

7. Global Neuromorphic Computing Market, by End-use Vertical

7.1 Introduction

7.2 Automotive

7.3 Aerospace and Defense

7.4 Healthcare and Life Sciences

7.5 Industrial Automation and Manufacturing

7.6 IT and Telecommunications

7.7 Consumer Electronics

7.8 Other End-use Verticals (Research & Academia, Energy)

8. Global Neuromorphic Computing Market, by Region

8.1 Introduction

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.2.3 Mexico

8.3 Europe

8.3.1 Germany

8.3.2 France

8.3.3 U.K.

8.3.4 Italy

8.3.5 Spain

8.3.6 Netherlands

8.3.7 Rest of Europe

8.4 Asia-Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 South Korea

8.4.5 Southeast Asia

8.4.6 Australia

8.4.7 Rest of Asia-Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.5.4 Rest of Latin America

8.6 Middle East & Africa

8.6.1 Saudi Arabia

8.6.2 UAE

8.6.3 South Africa

8.6.4 Rest of Middle East & Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Ranking / Positioning Analysis of Key Players, 2025

10. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1 Intel Corporation

10.2 IBM Corporation

10.3 BrainChip Holdings Ltd.

10.4 Qualcomm Technologies, Inc.

10.5 GrAI Matter Labs

10.6 SynSense AG

10.7 Vicarious AI

10.8 Samsung Electronics Co., Ltd.

10.9 Hewlett Packard Enterprise Company

10.10 Applied Brain Research Inc.

10.11 General Vision Inc.

10.12 Koniku Inc.

10.13 Prophesee SA

11. Appendix

11.1 Questionnaire

11.2 Related Reports

Published Date: Feb-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates