Resources

About Us

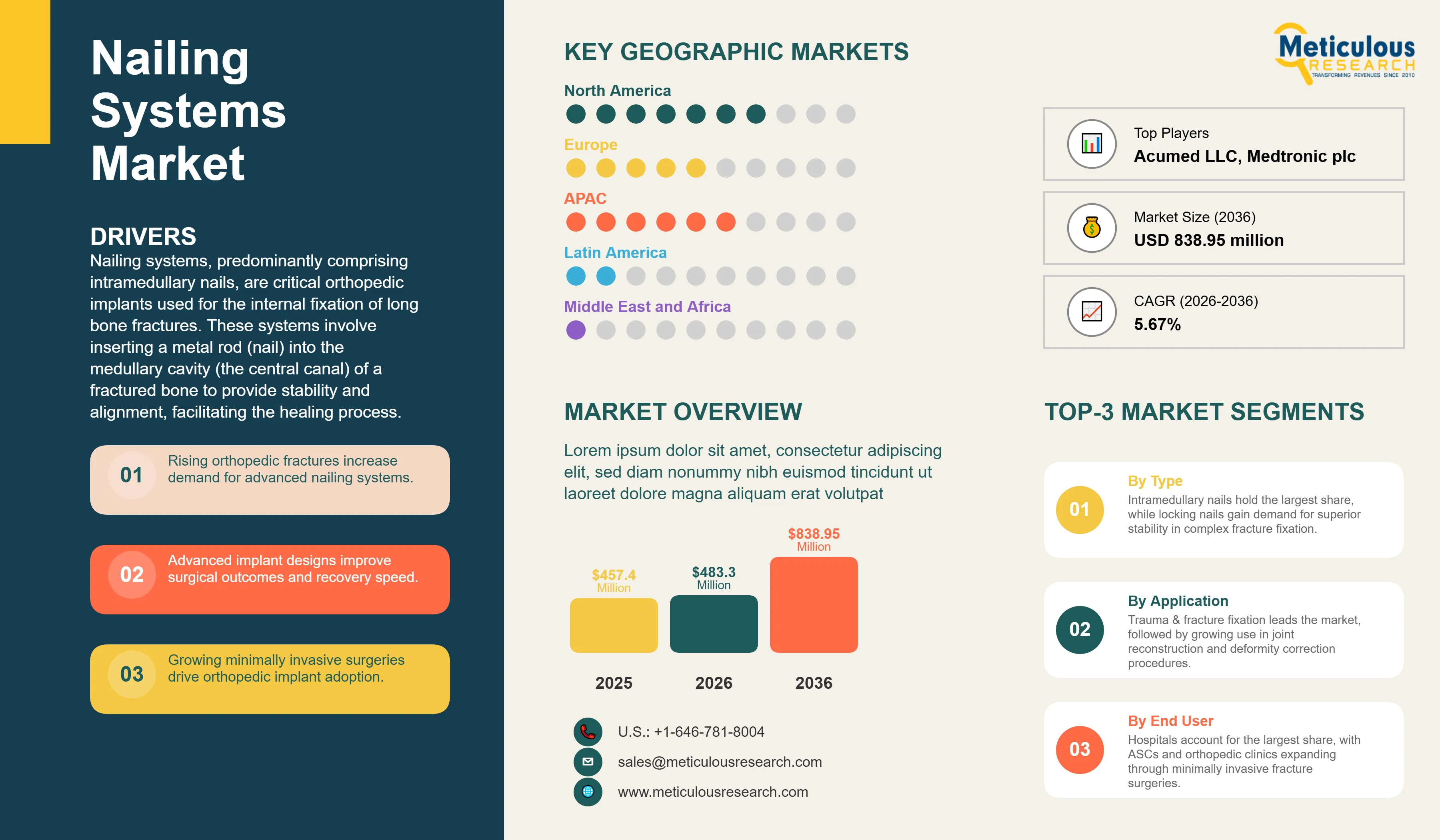

The global nailing systems market is estimated to be USD 483.3 million in 2026. This market is reach USD 838.95 million by 2036, growing at CAGR of 5.67% during the forecast period. The growth of this market is primarily driven by the increasing incidence of orthopedic fractures, a rapidly aging global population prone to bone fragility, and continuous advancements in surgical techniques and implant materials.

Click here to: Get Free Sample Pages of this Report

Nailing systems, predominantly comprising intramedullary nails, are critical orthopedic implants used for the internal fixation of long bone fractures. These systems involve inserting a metal rod (nail) into the medullary cavity (the central canal) of a fractured bone to provide stability and alignment, facilitating the healing process. Intramedullary nailing is considered the gold standard for treating various long bone fractures, including those of the femur (thigh bone), tibia (shin bone), and humerus (upper arm bone), offering advantages such as reduced soft tissue damage, improved blood supply to the fracture site, and early mobilization of the patient. According to the World Health Organization, road traffic crashes result in approximately 1.19 million deaths annually and 20–50 million non-fatal injuries worldwide each year, many of which involve long bone fractures requiring surgical fixation. In addition, the International Osteoporosis Foundation estimates that approximately 8.9 million osteoporotic fractures occur globally each year—equivalent to one fracture every 3 seconds, further driving the demand for orthopedic fixation devices.

The evolution of nailing systems has been marked by innovations in implant design, material science, and surgical instrumentation, leading to more biomechanically stable constructs and better patient outcomes. The market is continuously adapting to address the complexities of different fracture patterns, patient demographics, and the growing demand for minimally invasive surgical approaches. According to the latest Global Burden of Disease (GBD) 2021 study, approximately 607 million people worldwide were living with osteoarthritis in 2021, contributing to the rising volume of orthopedic procedures among aging populations. The emphasis on faster recovery times, reduced hospital stays, and improved functional restoration following surgery further underscores the indispensable role of advanced nailing systems in modern orthopedic trauma management.

Drivers

Restraints

Opportunities

Challenges

The global nailing systems market is witnessing several transformative trends. A prominent trend is the increasing adoption of locking plate and nail systems, which provide enhanced angular stability and improved fixation, particularly in osteoporotic bone. Another key trend is the growing focus on minimally invasive surgical (MIS) techniques for fracture fixation, driving the development of specialized instruments and implant designs that facilitate less invasive approaches. The market is also characterized by continuous innovation in biomaterials, with a shift towards advanced titanium alloys and the exploration of bioresorbable materials to reduce complications and the need for secondary surgeries. Furthermore, there is a rising emphasis on pre-operative planning software and 3D printing for patient-specific guides and implants, enhancing surgical precision and customization. Finally, the integration of surgical navigation and robotic assistance with nailing procedures is an emerging trend, promising to revolutionize accuracy and efficiency in orthopedic trauma surgery.

Analysis by Product Type: Intramedullary Nails Leading the Charge

Based on product type, intramedullary nails are expected to hold the largest share of the global nailing systems market. Their proven efficacy, biomechanical advantages, and widespread application in long bone fracture fixation solidify their dominance. The locking nails segment is anticipated to witness the fastest CAGR, driven by the superior stability they offer, particularly in complex and comminuted fractures, and their increasing adoption in challenging orthopedic cases.

Analysis by Material: Titanium Alloys at the Forefront

Based on material, titanium alloys are expected to command the largest share of the global nailing systems market. Their excellent biocompatibility, high strength-to-weight ratio, and corrosion resistance make them the preferred material for orthopedic implants. The bioresorbable materials segment is anticipated to exhibit the fastest CAGR, driven by ongoing research and development into implants that gradually resorb into the body, eliminating the need for removal surgeries and reducing long-term complications.

Analysis by Application: Trauma & Fracture Fixation Dominating

The trauma & fracture fixation segment is projected to account for the largest share of the nailing systems market. This is directly attributable to the primary purpose of nailing systems in stabilizing various types of fractures, from simple to complex. The joint reconstruction segment is expected to grow at the fastest CAGR, propelled by the increasing prevalence of degenerative joint diseases and the use of nailing systems in conjunction with arthroplasty procedures for peri-prosthetic fractures.

Analysis by End User: Hospitals as Primary Adopters

Based on end user, hospitals are expected to command the largest share of the global nailing systems market. Hospitals serve as the primary centers for orthopedic trauma care, performing a high volume of fracture fixation surgeries. The ambulatory surgical centers (ASCs) segment is anticipated to exhibit the fastest CAGR, driven by the increasing shift of less complex orthopedic procedures to outpatient settings due to cost-effectiveness and patient convenience.

North America: A Hub for Orthopedic Innovation and Adoption

North America is expected to hold the largest share of the global Nailing Systems market. This dominance is attributed to a highly developed healthcare infrastructure, a high prevalence of orthopedic injuries, significant investments in research and development of advanced orthopedic implants, and favorable reimbursement policies. The United States, in particular, is a major contributor due to its large patient population and the presence of key market players.

Europe: Advancing Fracture Care with Established Healthcare Systems

Europe is expected to hold a significant share of the global Nailing Systems market, driven by well-established healthcare systems, a growing geriatric population, and a strong focus on improving orthopedic care outcomes. Countries like Germany, the U.K., and France are key contributors due to their high surgical volumes and the adoption of advanced fracture fixation techniques. The key companies operating in the European market are DePuy Synthes (Johnson & Johnson), Stryker Corporation, and Zimmer Biomet.

Asia-Pacific: Rapid Growth Fueled by Expanding Healthcare Access

Asia-Pacific is projected to witness the fastest CAGR during the forecast period. This rapid growth is driven by improving healthcare infrastructure, increasing healthcare expenditure, a large and aging population, and a rising awareness of advanced orthopedic treatments in countries like China, India, and Japan. The growing medical tourism sector and government initiatives to enhance healthcare access also contribute to the region's market expansion. The key companies operating in the Asia-Pacific market are DePuy Synthes (Johnson & Johnson) and Stryker Corporation.

Latin America: Emerging Opportunities in Orthopedic Trauma

Latin America is anticipated to witness steady growth in the Nailing Systems market, primarily due to increasing investments in healthcare infrastructure, a rising incidence of trauma cases, and growing awareness about advanced orthopedic surgical options in countries like Brazil and Mexico. The modernization of healthcare facilities and the adoption of international surgical standards also contribute to the demand for nailing systems. The key companies operating in the Latin American market are DePuy Synthes (Johnson & Johnson) and Stryker Corporation.

Middle East & Africa: Gradual Expansion with Healthcare Development

The Middle East & Africa region is expected to experience gradual growth in the Nailing Systems market, driven by increasing healthcare investments, government initiatives to improve healthcare quality, and a growing focus on adopting advanced medical technologies for trauma care. Countries like UAE and Saudi Arabia are leading the adoption of modern orthopedic practices and equipment in the region. The key companies operating in the Middle East & Africa market are DePuy Synthes (Johnson & Johnson) and Stryker Corporation.

The global Nailing Systems market is characterized by a dynamic and highly competitive landscape. It features a mix of large multinational medical device corporations and specialized orthopedic implant manufacturers. Key players are focusing on product innovation, strategic acquisitions, collaborations with orthopedic surgeons, and geographic expansion to strengthen their market positions. The competitive strategy often revolves around developing biomechanically superior implants, offering comprehensive surgical solutions, and providing extensive surgeon training and support. Companies are also investing heavily in clinical research to demonstrate the efficacy and safety of their products and gain a competitive edge.

The global Nailing Systems market is estimated at USD 483.3 million in 2026 and is projected to reach USD 838.95 million by 2036, growing at a CAGR of 5.67%.

The market is driven by increasing incidence of orthopedic fractures, aging global population, advancements in surgical techniques, and growing demand for minimally invasive procedures.

Key restraints include high cost of advanced systems, risk of complications, stringent regulatory approvals, and lack of skilled surgeons in underserved regions.

Opportunities include development of bioresorbable and smart implants, personalized solutions, expansion in emerging markets, and integration with surgical navigation and robotics.

Challenges include supply chain vulnerabilities, surgeon training, reimbursement policies, and competitive pressure.

Intramedullary nails hold the largest share, while locking nails are expected to grow the fastest.

Titanium alloys command the largest share, and bioresorbable materials are projected to have the fastest CAGR.

Trauma & fracture fixation accounts for the largest share, and joint reconstruction is anticipated to grow the fastest.

Which end-user segment accounts for the largest share, and which is anticipated to grow the fastest?

Hospitals hold the largest share, and ambulatory surgical centers (ASCs) are expected to grow the fastest.

North America leads the market, and Asia-Pacific is projected to exhibit the fastest growth.

Key players include DePuy Synthes (Johnson & Johnson), Stryker Corporation, Zimmer Biomet, Smith & Nephew plc, and Medtronic plc.

1. Introduction

1.1. Market Definition & Scope

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product Type

3.2.2. Market Analysis, by Material

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Increasing Incidence of Orthopedic Fractures

4.2.1.2. Aging Global Population and Osteoporosis

4.2.1.3. Advancements in Surgical Techniques and Implant Design

4.2.1.4. Growing Demand for Minimally Invasive Procedures

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Nailing Systems

4.2.2.2. Risk of Complications and Revision Surgeries

4.2.2.3. Stringent Regulatory Approval Processes

4.2.2.4. Lack of Skilled Orthopedic Surgeons in Underserved Regions

4.2.3. Opportunities

4.2.3.1. Development of Bioresorbable and Smart Implants

4.2.3.2. Personalized and Patient-Specific Nailing Solutions

4.2.3.3. Expansion in Emerging Markets

4.2.3.4. Integration with Surgical Navigation and Robotics

4.2.4. Challenges

4.2.4.1. Supply Chain Vulnerabilities

4.2.4.2. Surgeon Training and Education

4.2.4.3. Reimbursement Policies and Healthcare Economics

4.2.4.4. Competitive Pressure and Price Sensitivity

4.2.5. Key Trends

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Nailing Systems Market, by Product Type

5.1. Overview

5.2. Intramedullary Nails

5.2.1. Locking Nails

5.2.2. Non-Locking Nails

5.3. External Fixation Systems

5.4. Accessories

6. Global Nailing Systems Market, by Material

6.1. Overview

6.2. Titanium Alloys

6.3. Stainless Steel

6.4. Bioresorbable Materials

6.5. Other Materials

7. Global Nailing Systems Market, by Application

7.1. Overview

7.2. Trauma & Fracture Fixation

7.2.1. Femur Fractures

7.2.2. Tibia Fractures

7.2.3. Humerus Fractures

7.2.4. Other Fractures

7.3. Joint Reconstruction

7.4. Deformity Correction

8. Global Nailing Systems Market, by End User

8.1. Overview

8.2. Hospitals

8.3. Ambulatory Surgical Centers (ASCs)

8.4. Orthopedic Clinics

9. Global Nailing Systems Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. UAE

9.6.2. Saudi Arabia

9.6.3. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share/Ranking Analysis, By Key Player (2025)

11. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

11.1. DePuy Synthes (Johnson & Johnson)

11.2. Stryker Corporation

11.3. Zimmer Biomet

11.4. Smith & Nephew plc

11.5. Medtronic plc

11.6. Orthofix Medical Inc.

11.7. Acumed LLC

11.8. B. Braun Melsungen AG

11.9. Wright Medical Group N.V. (now part of Stryker)

11.10. Globus Medical Inc.

12. Appendix

12.1. Abbreviations

12.2. Bibliography

12.3. Disclaimer

Published Date: Jul-2024

Published Date: Feb-2023

Subscribe to get the latest industry updates