Resources

About Us

Myopia Management Devices Market Size, Share & Trends Analysis by Product Type, Modality, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

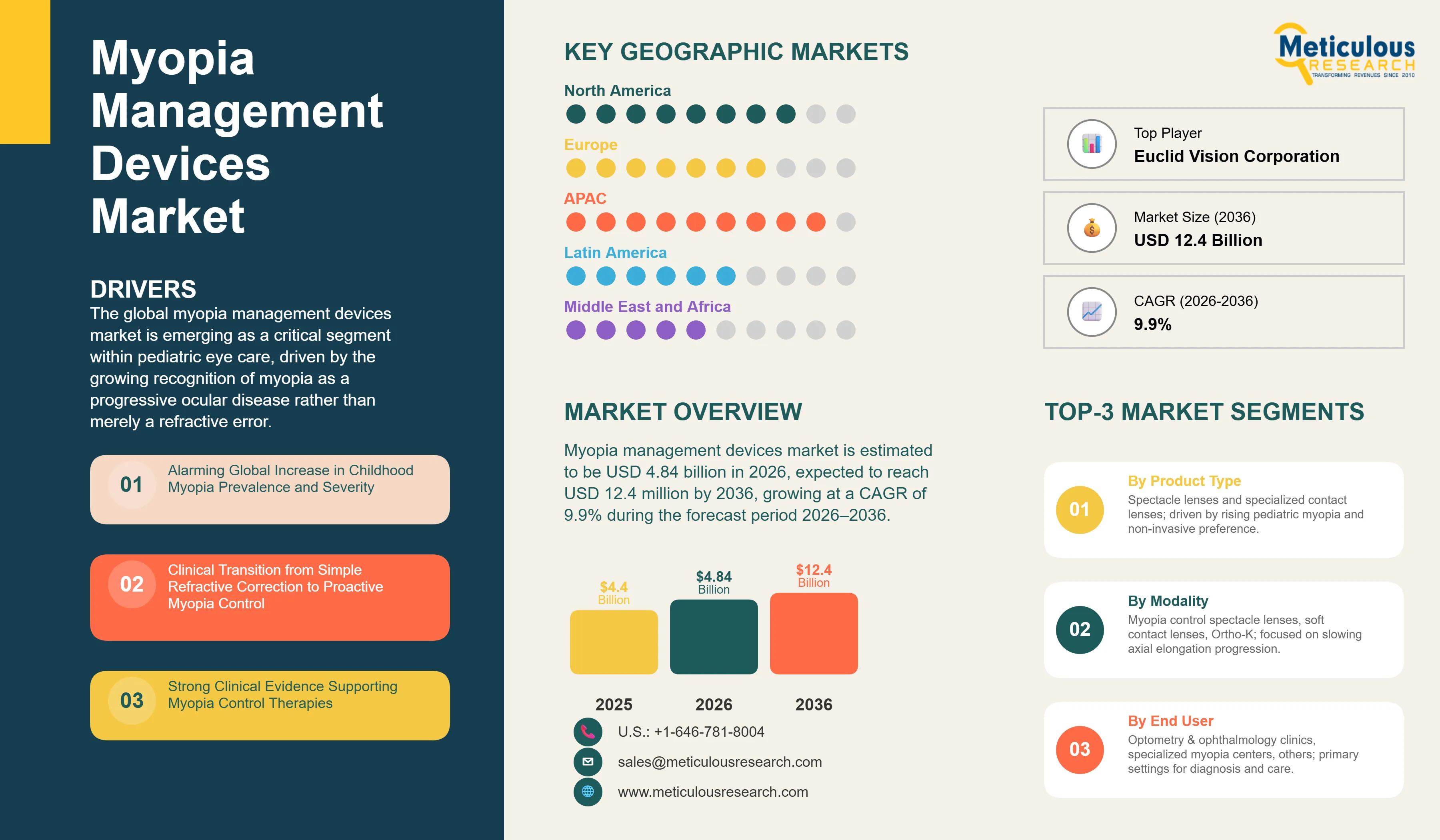

Report ID: MRHC - 1042077 Pages: 285 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global myopia management devices market is estimated to be USD 4.84 billion in 2026. This market is expected to reach USD 12.4 million by 2036, growing at a CAGR of 9.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global myopia management devices market is emerging as a critical segment within pediatric eye care, driven by the growing recognition of myopia as a progressive ocular disease rather than merely a refractive error. High and progressive myopia are associated with an increased lifetime risk of serious ocular complications, including retinal detachment, glaucoma, myopic macular degeneration, and cataracts. According to the World Society of Paediatric Ophthalmology and Strabismus (WSPOS), myopia prevalence has reached epidemic levels in several East Asian countries, affecting 80–90% of young adults in some urban populations, while prevalence among school-age children continues to rise globally. Furthermore, projections from the International Myopia Institute indicate that nearly 50% of the world's population—approximately 5 billion people—could be myopic by 2050, with almost 1 billion people affected by high myopia.

The increasing prevalence of childhood myopia is being linked to environmental and lifestyle factors, including intensive near-work activities, prolonged digital device usage, and reduced outdoor exposure. WSPOS consensus guidelines highlight that increased time spent outdoors has demonstrated a protective effect against the onset of myopia, while sustained near-work activities are associated with a greater risk of myopia development and progression. These trends have intensified demand for early intervention strategies aimed at slowing axial elongation, the primary structural driver of progressive myopia.

Technological innovation has significantly expanded the range of evidence-based optical interventions available to clinicians. Myopia control spectacle lenses, dual-focus and multifocal soft contact lenses, and orthokeratology (Ortho-K) lenses have demonstrated meaningful reductions in myopia progression and axial length growth in children. Commercial adoption has accelerated following the introduction of specialized products such as peripheral-defocus spectacle lenses and dual-focus contact lenses designed specifically for myopia control.

Professional organizations including the International Myopia Institute (IMI) and WSPOS increasingly advocate proactive monitoring and early treatment of pediatric myopia rather than conventional vision correction alone. As clinical guidelines continue to evolve and awareness among eye-care professionals and parents increases, myopia management is becoming an established standard of care in pediatric optometry and ophthalmology. This shift is expected to drive sustained demand for specialized myopia management devices across both developed and emerging markets throughout the forecast period.

Drivers: Rising Pediatric Myopia Prevalence and the Shift toward Proactive Management Protocols

The growth of the global myopia management devices market is primarily driven by the alarming rise in childhood myopia cases and the clinical shift from simple correction to proactive progression control.

Alarming Global Increase in Childhood Myopia Prevalence and Severity

A major driver for the market is the rapid increase in the prevalence and severity of myopia among children and adolescents worldwide. Modern lifestyles, characterized by intensive near-work and limited outdoor activity, are significantly accelerating the onset and progression of myopia. As more children are diagnosed with myopia at younger ages, the window for effective intervention expands, driving the demand for specialized management devices. This trend is particularly pronounced in urban environments where the prevalence of high myopia is also on the rise, creating an urgent need for effective control strategies.

Clinical Transition from Simple Refractive Correction to Proactive Myopia Control

The global eye care community is witnessing a fundamental shift in how myopia is managed, moving away from simple refractive correction with standard single-vision lenses toward proactive progression control. This shift is supported by a growing body of clinical evidence demonstrating that slowing myopia progression can significantly reduce the long-term risk of ocular pathologies. As professional associations increasingly advocate for myopia management as the standard of care, practitioners are rapidly adopting specialized optical devices. This clinical consensus, combined with rising parental awareness, is fueling the widespread adoption of myopia management protocols in primary eye care practices.

Restraints: High Treatment Costs and the Lack of Standardized Global Reimbursement

Despite their clinical benefits, the adoption of myopia management devices is hindered by high out-of-pocket costs and the technical complexities of implementing comprehensive management programs.

Significant Out-of-Pocket Costs and Long-Term Financial Commitment for Parents

A major restraint for the market is the high cost associated with specialized myopia management devices and the ongoing clinical monitoring they require. Unlike standard corrective lenses, myopia management often involves a long-term financial commitment that can span several years. In many regions, these treatments are not covered by standard vision insurance or government health plans, placing the full financial burden on parents. This economic barrier can limit the accessibility of advanced myopia control options, particularly for lower-income families, and may slow the overall market penetration in price-sensitive regions.

Lack of Standardized Global Reimbursement and Variable Professional Adoption Rates

The global myopia management devices market is impacted by the lack of standardized reimbursement codes and varying levels of professional adoption across different regions. While some markets have established clear pathways for myopia management, others still lack the necessary regulatory and financial frameworks to support widespread implementation. Furthermore, the specialized training and equipment required to fit and monitor advanced devices like Ortho-K lenses can be a barrier for some practitioners. These variable adoption rates and reimbursement challenges create an uneven global market landscape and can impact the consistent delivery of myopia care.

Opportunities: Expanding into Emerging Markets and Integrating Digital Health Monitoring

Future growth opportunities in the myopia management devices market are centered on the expansion into rapidly developing eye care markets and the integration of digital tools for enhanced patient monitoring.

Massive Expansion Opportunity in Rapidly Developing Eye Care Markets

There is a massive opportunity for market growth in emerging economies where the prevalence of myopia is rising and the healthcare infrastructure is modernizing. Countries in Southeast Asia, Latin America, and parts of the Middle East are seeing a surge in demand for pediatric eye care services. Manufacturers that can provide a range of myopia management options—from premium specialized lenses to more accessible control strategies—are well-positioned to tap into these high-growth regions. Strategic partnerships with regional eye care networks and educational initiatives for local practitioners can further accelerate market penetration.

Integration of Digital Health Tools and Wearable Sensors for Enhanced Monitoring

The integration of digital health tools and wearable sensors for real-time monitoring of visual habits represents a significant opportunity. Wearable devices that can track outdoor time, near-work duration, and viewing distance can provide invaluable data to both clinicians and parents, facilitating more personalized and effective myopia management. Furthermore, the use of tele-ophthalmology for remote monitoring and follow-up can improve patient compliance and accessibility. Manufacturers that can successfully integrate these digital tools with their optical devices are likely to offer a more comprehensive and appealing management solution.

Growing Proliferation of Dedicated and Specialized Myopia Management Centers

A prominent trend in 2026 is the rapid expansion of dedicated myopia management centers focused on pediatric eye care and myopia progression control. This trend is supported by the growing global burden of myopia, with the International Myopia Institute (IMI) projecting that nearly 50% of the world's population could be myopic by 2050, including almost 1 billion individuals with high myopia. Specialized centers provide comprehensive services including myopia risk assessment, axial length monitoring, orthokeratology fitting, myopia-control spectacle lenses, and dual-focus contact lens therapies. Increasing parental awareness and professional recommendations for early intervention are driving patient volumes at these facilities. Many centers also participate in clinical research, practitioner training, and treatment outcome monitoring, accelerating adoption of evidence-based myopia management and contributing to the establishment of dedicated myopia care as a standard component of pediatric eye health services.

Increasing Clinical Focus on Combination and Multimodal Management Strategies

The market is witnessing a growing shift toward combination and multimodal treatment strategies aimed at enhancing myopia control outcomes. Clinical evidence published by the International Myopia Institute and World Society of Paediatric Ophthalmology and Strabismus (WSPOS) indicates that optical interventions such as orthokeratology, dual-focus soft contact lenses, and peripheral-defocus spectacle lenses can reduce myopia progression by approximately 30–60% compared with conventional correction methods. As a result, clinicians are increasingly exploring combinations of optical devices with low-dose atropine therapy to achieve additive treatment benefits, particularly for children exhibiting rapid axial elongation or high-risk progression profiles. This personalized treatment approach is gaining traction as eye-care professionals increasingly utilize axial length measurements, family history assessments, and lifestyle risk factors to tailor management plans, supporting improved long-term visual outcomes and further advancing the sophistication of modern myopia care.

Analysis by Product Type

Based on product type, the spectacle lenses segment is expected to hold the largest share of the global myopia management devices market in 2026. This dominant position is substantiated by its non-invasive nature, high parental acceptance, and ease of use in pediatric populations. Advanced lens designs like DIMS and HAL have shown significant efficacy, making them the primary choice for initial management. However, the specialized contact lenses segment is projected to register the highest CAGR during the forecast period. The increasing demand for lifestyle-friendly options for active children and the growing clinical evidence supporting the superior peripheral defocus control of dual-focus soft lenses are driving the rapid growth of this segment.

Analysis by Modality

By modality, the myopia control spectacle lenses segment is expected to hold the largest share in 2026. This leadership is driven by the fact that spectacle lenses are the most accessible and cost-effective entry point for myopia management, providing a foundational modality for primary eye care practices. However, the orthokeratology (Ortho-K) segment is projected to grow at the fastest CAGR during the forecast period. The unique benefit of providing clear daytime vision without the need for correction, combined with its strong myopia control effect, is making Ortho-K an increasingly popular choice for parents and active children, fueling its rapid expansion.

Analysis by End User

By end user, the optometry & ophthalmology clinics segment is expected to hold the largest share in 2026. These facilities are the primary setting for professional myopia management, offering the specialized diagnostic and monitoring infrastructure required for effective care. However, the specialized myopia management centers segment is projected to register the highest CAGR during the forecast period. The rise of dedicated facilities that focus exclusively on childhood myopia and offer a comprehensive range of advanced management options is attracting a growing number of patients, driving the rapid expansion of this specialized segment.

Geographic Analysis: Asia-Pacific's Market Dominance and North America's Rapid Clinical Adoption

Largest Share: Asia-Pacific

Asia-Pacific is expected to dominate the global myopia management devices market in 2026, holding a market share of around 55%. This leading position is attributed to the exceptionally high prevalence of myopia in East and Southeast Asian countries, strong government initiatives to address the myopia epidemic, and high parental awareness. The region benefits from being a hub for clinical research and the presence of leading manufacturers. Key companies operating in the Asia Pacific market are Hoya Corporation, EssilorLuxottica, Menicon Co., Ltd., and CooperVision.

Fastest Growing: North America

The North America region is projected to witness the fastest growth in the global myopia management devices market, with a CAGR of 10.8% during the forecast period. This rapid expansion is driven by the increasing awareness of high myopia risks, the recent FDA approvals for specialized myopia control lenses, and the rapid expansion of management services in private practices. Growing professional consensus on the need for early intervention is accelerating market adoption. Key companies operating in the North America market are CooperVision, Johnson & Johnson Vision, EssilorLuxottica, and Visioneering Technologies, Inc. (VTI).

The global myopia management devices market is characterized by intense competition among major global vision care corporations and specialized innovative players focusing on pediatric eye care. Competition is primarily focused on improving the efficacy of optical defocus designs, enhancing the safety and comfort of contact lenses, and developing comprehensive digital management platforms. Key players are investing heavily in long-term clinical trials to substantiate the sustained myopia control effects of their devices and to secure regulatory approvals in new markets. Strategic developments often involve acquisitions of specialized technology firms and partnerships with research institutions to stay at the forefront of myopia research. Furthermore, there is a growing focus on providing comprehensive professional education and training programs to support practitioners in implementing effective myopia management protocols. Manufacturers are also increasingly focusing on direct-to-parent educational initiatives to raise awareness about the importance of proactive myopia control, which is critical for maintaining market leadership in this rapidly evolving and clinically-driven field.

CooperVision, EssilorLuxottica SA, Hoya Corporation, Menicon Co., Ltd., Johnson & Johnson Vision, Carl Zeiss Vision, Bausch + Lomb Corporation, Alcon Inc., SightGlass Vision, Inc., Visioneering Technologies, Inc., Euclid Vision Corporation, Paragon Vision Sciences, Mark'ennovy Personalized Care S.L., SwissLens SA, X-Cel Specialty Contacts, Alpha Corporation, Brighten Optix Corporation, Art Most

The global market is estimated at USD 4.85 billion in 2026, with a projected growth to USD 12.4 billion by 2036, at a CAGR of 9.9%.

Primary drivers include the rising global prevalence of childhood myopia and the clinical shift toward proactive progression control.

Major restraints include high out-of-pocket costs for parents and the lack of standardized global reimbursement for management programs.

Opportunities lie in expanding into rapidly developing eye care markets and the integration of digital health tools for enhanced monitoring.

Spectacle lenses are expected to hold the largest share due to their non-invasive nature and high parental acceptance.

Orthokeratology (Ortho-K) is projected to grow at the fastest CAGR, driven by its unique benefit of daytime vision without correction.

Optometry & ophthalmology clinics are expected to hold the largest share as the primary setting for professional myopia management.

Asia-Pacific is expected to dominate the market due to the exceptionally high prevalence of myopia and strong government initiatives.

North America is projected to witness the fastest growth, fueled by increasing awareness of high myopia risks and rapid clinical adoption.

Key trends include the rise of specialized myopia management centers and the focus on combination management strategies.

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jun-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates