Resources

About Us

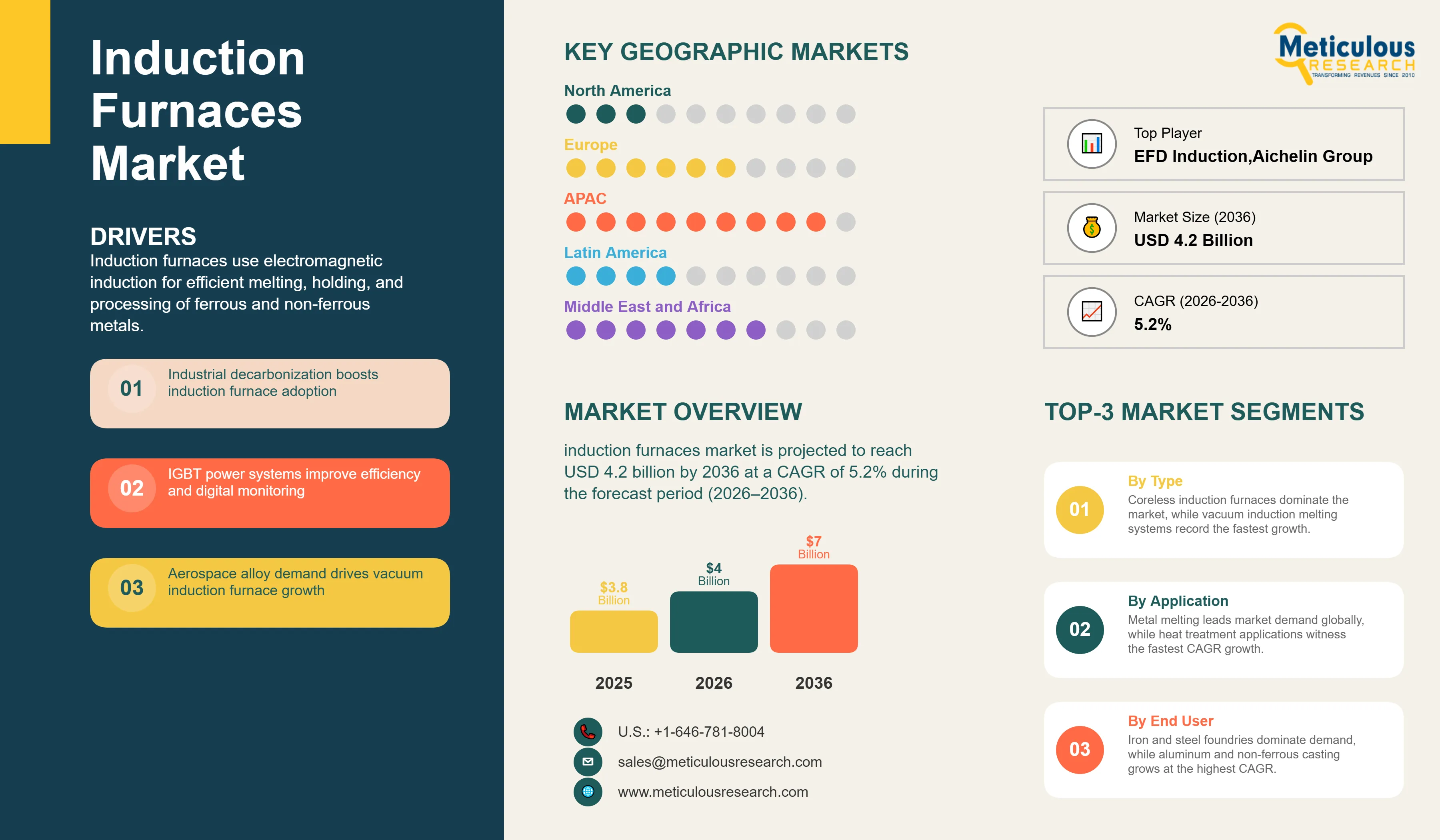

The global induction furnaces market was valued at USD 2.4 billion in 2025. The market is projected to reach USD 4.2 billion by 2036, growing from USD 2.5 billion in 2026 at a CAGR of 5.2% during the forecast period (2026–2036).

Market Overview and Insights

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global induction furnaces industry encompasses the full range of industrial equipment that uses electromagnetic induction to generate heat directly within electrically conductive materials, enabling the melting, holding, and thermal processing of ferrous and non-ferrous metals without direct contact between the energy source and the workpiece. The market includes coreless induction furnaces used for the melting of iron, steel, copper, aluminum, and specialty alloys in foundry and secondary steelmaking operations; channel induction furnaces used for holding and continuous pouring of molten non-ferrous metals; vacuum induction melting furnaces used for producing high-purity superalloys and reactive metals under controlled atmospheric conditions; and induction heating systems deployed across heat treatment operations including hardening, tempering, annealing, normalizing, and stress relieving, as well as for preheating billets and bars ahead of hot forming operations such as forging and rolling.

These systems serve a broad range of end-use industries including iron and steel foundries, aluminum and non-ferrous metal casting operations, precious metals and specialty alloy production, automotive components manufacturing, aerospace and defense manufacturing, and mining and mineral processing. Induction furnaces operate across a wide capacity range, from sub-100 kilogram units used in precious metal refining and laboratory-scale alloy development to large-format installations serving continuous melting and holding operations at industrial-scale foundries and steelmaking facilities.

The growth of the induction furnaces market is primarily driven by the global industrial push toward electrification of thermal processes as part of carbon reduction commitments and energy efficiency mandates. According to the International Energy Agency, the iron and steel sector accounts for approximately 7% of global energy system CO2 emissions, making it one of the largest industrial contributors to greenhouse gas output and a primary focus of electrification efforts under national and regional net-zero programs. The transition from fossil fuel-based melting equipment, including coke-fired cupola furnaces and gas-fired reverberatory furnaces, toward induction-based electric systems is being accelerated by carbon pricing mechanisms, tightening industrial emission standards, and government incentives tied to energy-efficient manufacturing modernization. According to the World Steel Association, global crude steel production reached approximately 1,888 million tonnes in 2023, with China accounting for roughly 54% of total global output. India, the world's second-largest crude steel producer, produced approximately 140 million tonnes in 2023 and is targeting a national steelmaking capacity of 300 million tonnes by 2030 under its National Steel Policy, an ambition expected to drive sustained new investment in induction furnace-based secondary steel production over the forecast period.

In addition to the direct melting market, the growing adoption of induction heating technology for heat treatment and hot forming applications across automotive, aerospace, and precision manufacturing sectors is creating a structurally expanding market segment distinct from traditional foundry applications. The increasing complexity of automotive drivetrain systems, particularly in electric vehicles where precision-hardened gears, shafts, and rotor components require tight metallurgical specifications, is reinforcing demand for dedicated induction hardening and tempering systems. Simultaneously, the transition of the global automotive industry toward battery electric vehicle platforms is creating new demand for aluminum and non-ferrous metal induction melting equipment as automakers scale production of lightweight structural castings to reduce vehicle mass and extend driving range.

Despite strong growth drivers, the market faces challenges related to the higher upfront capital cost of induction melting systems compared with fuel-fired alternatives in markets where natural gas prices remain low and carbon pricing mechanisms are not yet in force. The requirement for stable, high-quality electrical power supply creates infrastructure dependencies that can complicate induction furnace adoption in regions with less reliable grid infrastructure. Harmonic distortion generated by induction furnace power supplies can create power quality issues that necessitate investment in reactive power compensation and harmonic filtering equipment, adding to the total installed cost of induction melting systems in foundry environments. Refractory lining management also presents ongoing operational complexity, as lining wear rates and replacement costs constitute a significant portion of total cost of ownership for coreless induction melting systems operating at high utilization rates.

Significant market opportunities exist for manufacturers offering digitally integrated induction furnace platforms that combine precise process control, real-time energy monitoring, and predictive maintenance capabilities with compliance documentation features aligned with industrial energy management standards such as ISO 50001. The rapid expansion of aerospace and defense manufacturing capacity in response to global aircraft production backlogs and defense spending increases is creating a structurally attractive growth segment for vacuum induction melting furnaces, where demand for nickel-based superalloys and titanium alloys processed under controlled atmospheric conditions is expanding faster than overall market growth rates. In addition, the emergence of new industrial applications including induction processing of battery cell materials, selective induction heating for advanced composite manufacturing, and specialty melting systems for semiconductor-grade crystal growth represents a nascent but expanding addressable market for induction technology suppliers over the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 7.0 Billion |

|

Market Size in 2026 |

USD 4.0 Billion |

|

Market Size in 2025 |

USD 3.8 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.8% |

|

Dominating Furnace Type |

Coreless Induction Furnaces |

|

Fastest Growing Furnace Type |

Vacuum Induction Melting Furnaces |

|

Dominating Application |

Metal Melting |

|

Fastest Growing Application |

Heat Treatment |

|

Dominating Capacity |

1 to 10 Tons |

|

Fastest Growing Capacity |

10 to 50 Tons |

|

Dominating End-use Industry |

Iron and Steel Foundry |

|

Fastest Growing End-use Industry |

Aluminum and Non-ferrous Metal Casting |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Industrial Decarbonization Mandates and Carbon Pricing Mechanisms Compelling Replacement of Fossil Fuel-Based Furnaces with Induction Systems Across Steel and Foundry Operations

Industrial decarbonization is transforming investment decisions across the steel and foundry sectors, with induction furnaces emerging as a key electrification pathway for facilities that still depend on coke-fired cupolas or other fossil-fuel-based melting systems. In Europe, the Carbon Border Adjustment Mechanism (CBAM) advanced from its transitional reporting phase in October 2023 to full implementation in January 2026, intensifying carbon-cost pressures on imported iron and steel products. Together with the revised Industrial Emissions Directive and Ambient Air Quality Directive, these measures reinforce the economic rationale for adopting lower-emission melting technologies, including induction systems where they are technically and financially viable.

In the United States, the Department of Energy’s Industrial Decarbonization Roadmap, published in September 2022, identifies iron and steel as one of five priority energy-intensive industries for deep decarbonization and provides a strategic framework that can support federal funding priorities for industrial electrification projects while influencing capital allocation decisions by large foundry and steelmaking operators. The Inflation Reduction Act’s industrial tax incentives, especially those linked to advanced energy projects and manufacturing investments, are also strengthening the case for electric melting technologies by helping offset part of the high upfront cost of induction furnace installations in retrofit applications. In India, the Bureau of Energy Efficiency’s Perform, Achieve and Trade scheme, which covers energy-intensive industries including iron and steel, is creating compliance-driven incentives for foundry and steel operators to improve energy efficiency and monitor performance more systematically. India’s Production Linked Incentive Scheme for Specialty Steel, approved with a total outlay of INR 6,322 crore over five years, is further directing investment toward specialty steel grades and higher-value production capabilities, which can support demand for precise and controlled melting technologies, including induction systems where technically suitable. Taken together, these policy developments across major industrial economies are steadily shifting induction furnace investment from a purely commercial decision toward one that is increasingly shaped by compliance, efficiency, and decarbonization objectives, thereby expanding the addressable market for equipment suppliers.

IGBT Solid-State Power Supply Technology Displacing Thyristor-Based Systems and Enabling Connected Furnace Monitoring Platforms

The shift from conventional thyristor-based (SCR) power supplies to insulated gate bipolar transistor (IGBT) solid-state platforms represents one of the most significant product-level trends shaping the competitive landscape for induction furnace manufacturers in new installations. While thyristor-based medium-frequency systems have historically dominated induction melting applications, they typically provide less precise control, lower power factor, and higher harmonic distortion compared with modern IGBT-based technologies. In contrast, IGBT systems enable more accurate power modulation, reduced harmonic content, improved power factor, and, in many cases, substantial reductions in energy consumption and reactive power-related infrastructure costs. For foundry operators, where electricity frequently represents the largest share of operating expenses, these efficiency improvements can enhance operating economics and improve the return on investment for both retrofit and greenfield projects.

Inductotherm Group, the world's leading manufacturer of induction melting equipment, has integrated IGBT technology across its medium-frequency power supply product lines, enabling the company to offer solid-state systems that combine high energy efficiency with digital process control interfaces that record power consumption, heat cycle data, and operational parameters for reporting and process optimization. EFD Induction, the leading European and global supplier of induction heating systems, similarly deploys IGBT-based solid-state technology across its heating product range, enabling the integration of programmable process controllers and real-time monitoring capabilities that support lean manufacturing and traceability requirements in automotive and aerospace supply chains. Ajax Tocco Magnethermic, a major North American supplier of induction heating and melting systems, has similarly updated its power supply platform to IGBT-based architectures that support remote diagnostics and connectivity integration.

The commercial availability of connected induction furnace systems built on IGBT power supply platforms is enabling a transition toward service-based business models for equipment manufacturers, where aftermarket support, remote performance monitoring, process optimization consulting, and energy benchmarking services create recurring revenue streams alongside capital equipment sales. For large industrial operators managing multiple furnace installations across distributed facilities, the ability to monitor furnace performance remotely, track energy consumption per heat, and receive predictive maintenance alerts based on real-time operational data represents a meaningful operational advantage that is influencing procurement preferences toward manufacturers capable of delivering integrated digital platforms alongside furnace hardware.

Vacuum Induction Melting Furnace Demand Expanding from Aerospace Superalloy Manufacturing, Defense Production, and Advanced Energy Applications

The vacuum induction melting furnace segment is experiencing structural demand growth driven by the intersection of three reinforcing forces: the production ramp-up of commercial and military aircraft requiring nickel-based superalloy components, rising defense procurement budgets directing investment toward advanced materials supply chains, and the expanding use of specialty alloys in next-generation energy infrastructure including advanced nuclear reactors and large-scale industrial gas turbines. Vacuum induction melting is the foundational processing step for producing nickel-based superalloys such as Inconel, Waspaloy, and René alloy families, as well as for titanium and titanium aluminide alloys, cobalt-based alloys, and high-strength specialty steels that cannot be melted in open-air induction systems without unacceptable oxidation and contamination. The quality and compositional control achievable in VIM processing is a prerequisite for the mechanical and fatigue performance specifications demanded in rotating turbine components, airframe structural members, and propulsion system hardware across both commercial and defense aerospace applications.

Consarc Corporation, a subsidiary of Inductotherm Group, is a leading supplier of vacuum induction melting (VIM) systems, offering solutions that range from laboratory-scale equipment to large production furnaces designed for diverse alloy development and manufacturing applications. ALD Vacuum Technologies, a Germany-based specialist in vacuum and controlled-atmosphere metallurgical systems, also provides an extensive VIM portfolio widely used by superalloy manufacturers and aerospace suppliers for first-melt and specialty alloy production. Retech Systems similarly serves the specialty vacuum melting segment, including applications involving reactive and high-purity metals such as titanium and zirconium that may require skull melting or other contamination-controlled processes.

Demand for VIM furnaces is also being reinforced by the expanding use of high-performance alloys in advanced energy infrastructure. Nickel-based superalloys continue to play a critical role in industrial gas turbines for power generation, where ongoing efficiency improvements are driving higher temperature and performance requirements. In addition, emerging small modular reactor (SMR) programs across the United States, United Kingdom, Canada, and parts of Asia are expected to support long-term demand for corrosion-resistant nickel alloy components and related specialty materials, although the specific melting technologies used will vary depending on the component and supply chain requirements.

By Furnace Type: In 2026, the Coreless Induction Furnaces Segment to Dominate the Global Induction Furnaces Market

Based on furnace type, the induction furnaces industry is segmented into coreless induction furnaces, channel induction furnaces, vacuum induction melting furnaces, and induction skull melting furnaces. In 2026, the coreless induction furnaces segment is expected to account for the largest share of this market. The leading position of this segment is attributed to its function as the foundational melting technology across the global iron and steel foundry industry, where coreless systems enable batch melting of scrap and pig iron charges to produce cast iron, ductile iron, and steel castings for automotive, infrastructure, and general engineering applications. Coreless induction furnaces operate using an alternating magnetic field generated by a water-cooled copper coil surrounding a refractory crucible, which induces eddy currents and resistive heating directly within the metal charge, delivering high melting rates, precise temperature control, and metallurgical flexibility that no alternative technology can match at comparable scale and cost for batch foundry operations. Inductotherm Group, the global market leader in induction melting systems, and OTTO JUNKER GmbH, a leading European manufacturer of both coreless and channel systems, exemplify the depth of product development investment that continues to sustain this segment's dominant commercial position.

However, the vacuum induction melting furnaces segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating demand for nickel-based superalloys and titanium alloys in commercial and military aerospace programs, the structural expansion of advanced manufacturing supply chains requiring VIM-processed specialty materials, and the growing use of high-performance alloys in industrial gas turbines and advanced energy infrastructure. The high per-unit value of vacuum induction melting systems and the premium placed on processing capability and metallurgical quality assurance features in aerospace and defense procurement are additionally supporting revenue growth rates in this segment that significantly outpace those of conventional melting equipment categories.

By Application: In 2026, the Metal Melting Segment to Hold the Largest Share

Based on application, the induction furnaces industry is segmented into metal melting, metal holding and pouring, heat treatment, and hot forming. In 2026, the metal melting segment is expected to account for the largest share of this market. The dominant position of the metal melting application reflects the primary commercial purpose for which induction furnace technology was developed and continues to be most widely deployed, encompassing the melting of iron, steel, aluminum, copper, and specialty metal charges in foundry and steelmaking operations that collectively represent the broadest and highest-volume category of induction furnace use globally. The metal melting segment is characterized by large-scale capital investment cycles tied to foundry capacity expansion, facility modernization, and the replacement of aging fuel-fired melting equipment with energy-efficient induction alternatives, particularly across Asia Pacific where new foundry capacity additions are occurring at a pace that has no equivalent in mature market regions.

However, the heat treatment segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the expanding adoption of induction hardening, tempering, annealing, and normalizing systems in automotive drivetrain and chassis component manufacturing, where the precision and repeatability of induction heat treatment methods deliver superior dimensional control and metallurgical consistency compared with conventional batch furnace alternatives. The rapid growth of electric vehicle production globally is creating particularly strong demand for induction heat treatment systems capable of processing precision-hardened components including electric motor shafts, reduction gear assemblies, and bearing races to tight case depth and hardness specifications. EMAG eldec, EFD Induction, and Ajax Tocco Magnethermic are among the leading manufacturers investing in application-specific induction hardening and heat treatment system development for automotive and precision engineering customers, underscoring the strong commercial momentum in this application segment.

By Capacity: In 2026, the 1 to 10 Tons Segment to Account for the Largest Share

Based on capacity, the induction furnaces industry is segmented into below 1 ton, 1 to 10 tons, 10 to 50 tons, and above 50 tons. In 2026, the 1 to 10 tons segment is expected to account for the largest share of this market. This growth is primarily driven by the widespread deployment of systems in this capacity range across the global iron and steel foundry industry, where the majority of independent foundries producing castings for automotive, agricultural equipment, and general engineering applications operate melting systems within this capacity band as the optimal balance between production flexibility, energy efficiency, and capital investment scale. The 1 to 10 ton capacity range also aligns closely with the standard charge weight requirements of the Indian induction furnace-based secondary steel sector, which represents one of the largest concentrations of induction melting equipment in the world and constitutes a structurally important demand base for manufacturers active in the Asia Pacific region.

However, the 10 to 50 tons segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the scaling of induction-based steelmaking capacity in India and Southeast Asia, where operators are investing in higher-capacity systems to improve throughput and reduce per-tonne energy consumption as they expand production to serve growing domestic demand for structural steel, reinforcing bar, and engineering steel products. The progressive shift of larger foundries and mini-mill operators from electric arc furnace technology to medium-frequency induction melting systems for specific product grades, driven by the superior metallurgical control and lower electrode consumption costs of induction technology in these applications, is additionally contributing to revenue growth in the higher capacity range over the forecast period.

By End-use Industry: In 2026, the Iron and Steel Foundry Segment to Hold the Largest Share

Based on end-use industry, the induction furnaces industry is segmented into iron and steel foundry, aluminum and non-ferrous metal casting, precious metals and specialty alloys, automotive components manufacturing, aerospace and defense, mining and mineral processing, and other end-use industries. In 2026, the iron and steel foundry segment is expected to account for the largest share of this market, reflecting the status of induction melting as the foundational process technology for the production of cast iron and steel castings consumed in automotive, agricultural, construction, and industrial machinery applications globally. The iron and steel foundry sector represents the largest and most geographically distributed end-user base for induction melting equipment, with tens of thousands of independent and captive foundries operating globally across varying scales of production, the majority of which rely on coreless induction melting systems as their primary thermal processing infrastructure. In India, the Joint Plant Committee under the Ministry of Steel recognizes the induction furnace route as a critical component of the country's secondary steelmaking infrastructure, highlighting the unique significance of this technology to the Indian industry structure at a scale that has no parallel among other major steel-producing economies.

However, the aluminum and non-ferrous metal casting segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the structural transformation of the global automotive industry toward battery electric vehicle platforms, where aluminum and aluminum alloy castings for battery enclosures, electric motor housings, structural frames, and thermal management components are consuming induction melting capacity at a rate that significantly exceeds historical growth patterns for non-ferrous foundry operations. The lightweighting imperative embedded in both regulatory fuel economy standards and competitive vehicle range targets is compelling automotive manufacturers and their Tier 1 casting suppliers to invest in expanded aluminum melting and holding capacity, creating sustained demand for coreless induction melting systems, channel holding furnaces, and associated ladle and degassing equipment optimized for high-purity aluminum alloy processing. In parallel, expanding copper and copper alloy casting operations in electrical infrastructure manufacturing, driven by grid modernization investments and growing demand for EV charging infrastructure components, are adding a secondary growth driver within this segment.

Based on geography, the induction furnaces market is commonly segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Asia Pacific is expected to hold the largest market share in 2026, supported by the region’s concentration of steelmaking and foundry activity, especially in China and India. China remains the world’s largest steel producer, while India is a major and fast-growing market for induction furnaces, particularly in the secondary steel and foundry segments. Japan and South Korea also contribute meaningful demand through advanced manufacturing, automotive casting, and precision metal processing applications.

However, the Middle East and Africa market is expected to be among the faster-growing regional markets for induction furnaces over 2026 to 2036, supported by greenfield and brownfield steel investments in the Gulf Cooperation Council countries. Economic diversification programs such as Saudi Vision 2030 and the UAE’s industrial strategy are encouraging investment in domestic metals and steel processing capacity, while Saudi Arabia’s expanding steel sector is likely to support additional demand for electric melting equipment. In Sub-Saharan Africa, growth in mining and mineral processing for copper, cobalt, gold, and other metals is creating demand for induction-based smelting and refining equipment, and the gradual expansion of foundry and engineering goods manufacturing in countries such as South Africa, Kenya, and Nigeria is adding early-stage demand for small and medium-capacity induction systems. Together, these trends suggest a positive long-term growth outlook for the region.

However, the Middle East and Africa market is expected to be among the faster-growing regional markets for induction furnaces over 2026 to 2036, supported by greenfield and brownfield steel investments in the Gulf Cooperation Council countries. Economic diversification programs such as Saudi Vision 2030 and the UAE’s industrial strategy are encouraging investment in domestic metals and steel processing capacity, while Saudi Arabia’s expanding steel sector is likely to support additional demand for electric melting equipment. In Sub-Saharan Africa, growth in mining and mineral processing for copper, cobalt, gold, and other metals is creating demand for induction-based smelting and refining equipment, and the gradual expansion of foundry and engineering goods manufacturing in countries such as South Africa, Kenya, and Nigeria is adding early-stage demand for small and medium-capacity induction systems. Together, these trends suggest a positive long-term growth outlook for the region.

The global induction furnaces market is moderately consolidated at the system level, with competition primarily driven by melting performance, energy efficiency, power supply technology, application-specific engineering capability, and the breadth and accessibility of aftermarket support for refractory, coil, and power supply components. Key competitive differentiators include the availability of IGBT-based solid-state power supply platforms with digital monitoring capabilities, expertise in designing systems for combustible or reactive metal processing, the provision of vacuum and controlled-atmosphere system configurations for specialty alloy applications, and the scale and geographic reach of field service and applications engineering networks.

Large integrated induction system manufacturers such as Inductotherm Group and EFD Induction compete through comprehensive product portfolios covering melting, holding, and heating applications across a full range of metals and capacity scales, with global service networks and deep application engineering resources that enable them to support complex, multi-furnace facility projects. Specialty system manufacturers including Consarc Corporation and ALD Vacuum Technologies compete through advanced vacuum and controlled-atmosphere melting capability, serving aerospace, defense, and specialty alloy customers where system performance and metallurgical process control are the primary procurement criteria. Regionally focused manufacturers including OTTO JUNKER GmbH, Aichelin Group, GH Electrotermia S.A., and EMAG eldec GmbH maintain strong competitive positions in European markets through customized engineering and proximity-based service capabilities, while Electrotherm (India) Limited competes effectively across South and Southeast Asia through cost-competitive system offerings and an extensive service network aligned with the requirements of the region's large and geographically dispersed foundry and secondary steel customer base.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global induction furnaces market include Inductotherm Group (U.S.), EFD Induction (Norway), OTTO JUNKER GmbH (Germany), Ajax Tocco Magnethermic Corporation (U.S.), Electrotherm (India) Limited (India), Consarc Corporation (U.S.), Pillar Induction (U.S.), ALD Vacuum Technologies GmbH (Germany), GH Electrotermia, S.A. (Spain), Aichelin Group (Austria), EMAG eldec GmbH (Germany), Retech Systems LLC (U.S.), Fuji Electric Co., Ltd. (Japan), SMS Group GmbH (Germany), and Tenova S.p.A. (Italy), among others.

The global induction furnaces market is expected to reach USD 4.2 billion by 2036 from an estimated USD 2.5 billion in 2026, at a CAGR of 5.2% during the forecast period 2026–2036.

In 2026, the coreless induction furnaces segment is expected to hold the largest share of this market, driven by its established position as the primary melting technology for iron, steel, and non-ferrous metals across the global foundry and secondary steelmaking industry.

The vacuum induction melting furnaces segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing demand for high-purity nickel-based superalloys, titanium alloys, and specialty materials in aerospace, defense, and advanced energy applications.

The vacuum induction melting furnaces segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing demand for high-purity nickel-based superalloys, titanium alloys, and specialty materials in aerospace, defense, and advanced energy applications.

In 2026, the metal melting segment is expected to hold the largest share of this market, reflecting the primary commercial use of induction furnaces in iron, steel, and non-ferrous foundry operations globally.

In 2026, the 1 to 10 tons capacity segment is expected to hold the largest share of this market, driven by its prevalence across the global iron and steel foundry industry and the Indian secondary steel sector.

In 2026, the iron and steel foundry segment is expected to hold the largest share of this market, reflecting the central role of induction melting across the global production of cast iron and steel castings for automotive, infrastructure, and industrial machinery applications.

The growth of this market is primarily driven by industrial decarbonization mandates and carbon pricing mechanisms including the EU Carbon Border Adjustment Mechanism compelling replacement of fossil fuel-based furnaces, India's expanding secondary steel production capacity and National Steel Policy targets, growing adoption of IGBT-based solid-state power supply technology that improves energy efficiency and enables digital monitoring, rising demand for vacuum induction melting systems from aerospace and defense superalloy manufacturing, and the structural shift in automotive manufacturing toward aluminum and non-ferrous castings driven by electric vehicle lightweighting requirements.

Key players in the global induction furnaces market include Inductotherm Group (U.S.), EFD Induction (Norway), OTTO JUNKER GmbH (Germany), Ajax Tocco Magnethermic Corporation (U.S.), Electrotherm (India) Limited (India), Consarc Corporation (U.S.), Pillar Induction (U.S.), ALD Vacuum Technologies GmbH (Germany), GH Electrotermia, S.A. (Spain), Aichelin Group (Austria), EMAG eldec GmbH (Germany), Retech Systems LLC (U.S.), Fuji Electric Co., Ltd. (Japan), SMS Group GmbH (Germany), and Tenova S.p.A. (Italy).

Middle East & Africa is expected to register the highest growth rate in the global induction furnaces market during the forecast period 2026–2036, driven by greenfield steel manufacturing investments aligned with Gulf Cooperation Council economic diversification programs, expanding mining and mineral processing capacity across Sub-Saharan Africa, and increasing industrial electrification investment across the region.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Furnace Type

3.3 Market Analysis by Application

3.4 Market Analysis by Capacity

3.5 Market Analysis by End-use Industry

3.6 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Industrial Decarbonization Mandates and Carbon Pricing Mechanisms Compelling Replacement of Fossil Fuel-Based Furnaces with Induction Systems

4.2.2 Rapid Expansion of Iron and Steel Production Capacity in Asia Pacific and the Middle East Driving Induction Furnace Procurement

4.2.3 Growing Demand for High-Performance Alloys in Aerospace, Defense, and Advanced Energy Applications Driving Vacuum Induction Melting System Adoption

4.2.4 IGBT Solid-State Power Supply Technology Improving Energy Efficiency and Enabling Connected Furnace Monitoring Platforms

4.3 Restraints

4.3.1 High Upfront Capital Cost of Induction Systems Relative to Fossil Fuel-Based Melting Alternatives in Low Carbon-Price Markets

4.3.2 Power Quality and Grid Infrastructure Dependencies Complicating Induction Furnace Adoption in Emerging Market Regions

4.4 Opportunities

4.4.1 India's National Steel Policy Capacity Targets and Secondary Steel Sector Modernization Creating Sustained Induction Furnace Demand

4.4.2 Electric Vehicle Production Ramp-Up Driving Aluminum and Non-ferrous Induction Melting Capacity Investment

4.4.3 Digitally Integrated Furnace Platforms Opening Service-Based Revenue Models for Equipment Manufacturers

4.5 Challenges

4.5.1 Refractory Lining Management Costs and Wear Variability Adding Operational Complexity to Total Cost of Ownership Calculations

4.5.2 Harmonic Distortion and Reactive Power Requirements Increasing Balance-of-Plant Infrastructure Costs for Foundry Operators

4.6 Porter's Five Forces Analysis

5. Induction Furnaces Market, by Furnace Type

5.1 Overview

5.2 Coreless Induction Furnaces

5.2.1 Medium-Frequency Coreless Induction Furnaces

5.2.2 Main-Frequency Coreless Induction Furnaces

5.3 Channel Induction Furnaces

5.3.1 Single-Channel Induction Furnaces

5.3.2 Multi-Channel Induction Furnaces

5.4 Vacuum Induction Melting Furnaces

5.4.1 Standard Vacuum Induction Melting Furnaces

5.4.2 Vacuum Induction Melting and Casting Furnaces

5.5 Induction Skull Melting Furnaces

6. Induction Furnaces Market, by Application

6.1 Overview

6.2 Metal Melting

6.3 Metal Holding and Pouring

6.4 Heat Treatment

6.4.1 Induction Hardening

6.4.2 Induction Tempering

6.4.3 Induction Annealing and Normalizing

6.5 Hot Forming

6.5.1 Forging and Rolling Preheating

6.5.2 Extrusion Preheating

6.6 Brazing and Soldering

7. Induction Furnaces Market, by Capacity

7.1 Overview

7.2 Below 1 Ton

7.3 1 to 10 Tons

7.4 10 to 50 Tons

7.5 Above 50 Tons

8. Induction Furnaces Market, by End-use Industry

8.1 Overview

8.2 Iron and Steel Foundry

8.3 Aluminum and Non-ferrous Metal Casting

8.4 Precious Metals and Specialty Alloys

8.5 Automotive Components Manufacturing

8.6 Aerospace and Defense

8.7 Mining and Mineral Processing

8.8 Other End-use Industries

9. Induction Furnaces Market, by Geography

9.1 Overview

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 Germany

9.3.2 U.K.

9.3.3 France

9.3.4 Italy

9.3.5 Spain

9.3.6 Sweden

9.3.7 Austria

9.3.8 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Japan

9.4.4 South Korea

9.4.5 Australia

9.4.6 Southeast Asia

9.4.7 Rest of Asia Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Argentina

9.5.3 Rest of Latin America

9.6 Middle East and Africa

9.6.1 Saudi Arabia

9.6.2 UAE

9.6.3 South Africa

9.6.4 Rest of Middle East and Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Share/Ranking Analysis (2025)

11. Company Profiles

11.1 Inductotherm Group

11.2 EFD Induction

11.3 OTTO JUNKER GmbH

11.4 Ajax Tocco Magnethermic Corporation

11.5 Electrotherm (India) Limited

11.6 Consarc Corporation

11.7 Pillar Induction

11.8 ALD Vacuum Technologies GmbH

11.9 GH Electrotermia, S.A.

11.10 Aichelin Group

11.11 EMAG eldec GmbH

11.12 Retech Systems LLC

11.13 Fuji Electric Co., Ltd.

11.14 SMS Group GmbH

11.15 Tenova S.p.A.

11.16 Others

12. Appendix

12.1 Questionnaire

12.2 Available Customization Options

12.3 Related Reports

Subscribe to get the latest industry updates