Resources

About Us

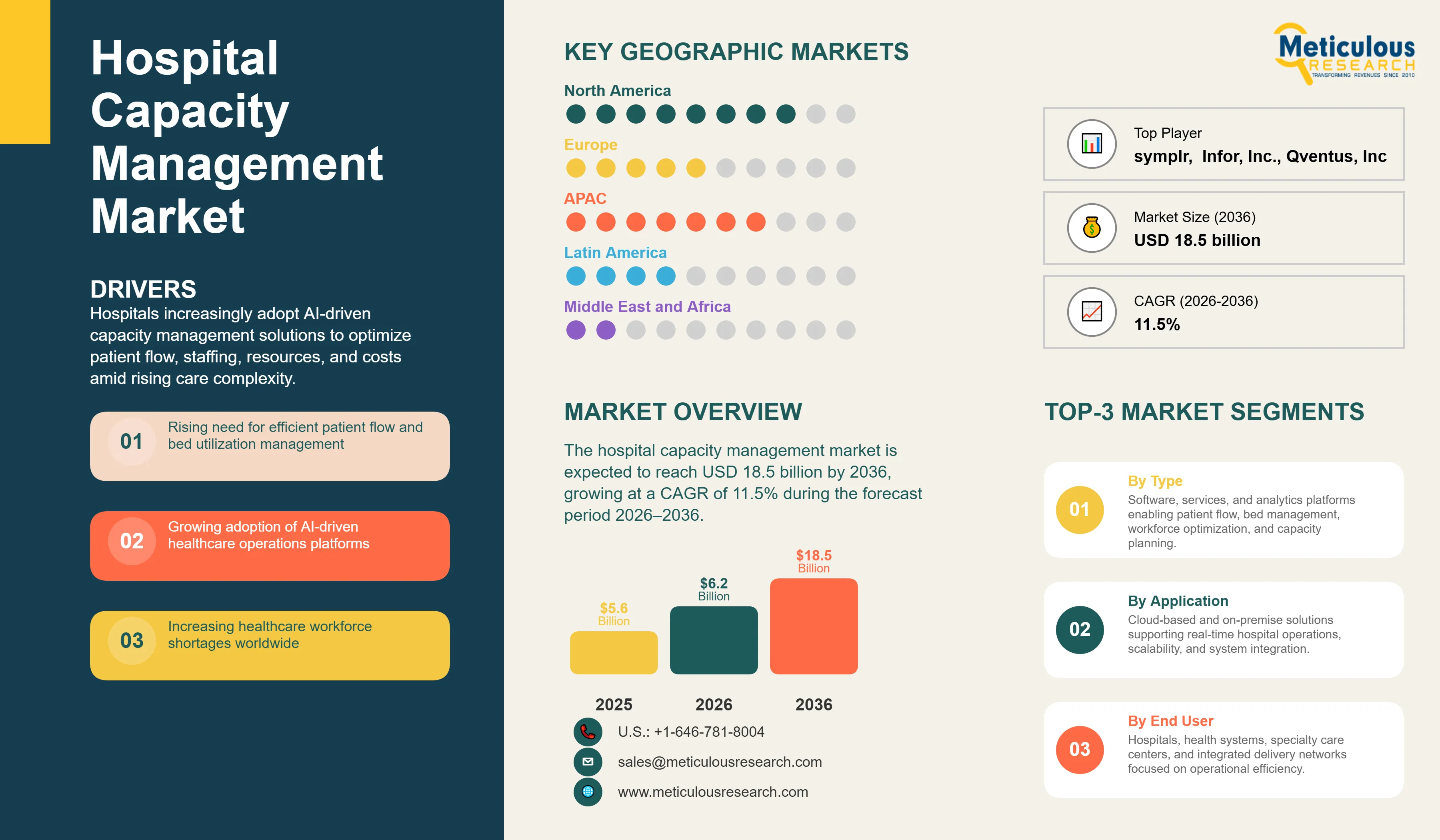

Hospital Capacity Management Market Size, Share & Trends Analysis by Component, Deployment Mode, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

Report ID: MRHC - 1042051 Pages: 316 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global hospital capacity management market is estimated to be USD 6.2 billion in 2026. This market is expected to reach USD 18.5 billion by 2036, growing at a CAGR of 11.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global hospital capacity management market reflects the increasing need for healthcare systems to manage growing operational complexity and rising patient acuity. These solutions integrate data from electronic health records (EHRs), real-time location systems (RTLS), clinical telemetry, and workforce management platforms to optimize patient flow, bed utilization, staffing, and resource allocation. According to the American Hospital Association's 2026 Costs of Caring report, hospital case-mix index—a standard measure of patient complexity—increased by approximately 5% between 2019 and 2024, indicating that a larger proportion of inpatient care is being devoted to higher-acuity patients with multiple conditions and greater clinical needs. The report further estimates that increasing patient severity contributed about 19% of total hospital expense growth over the same period. As hospitals face rising care complexity, workforce shortages, and financial pressures, healthcare providers are increasingly shifting from reactive operational reporting toward AI-enabled and predictive capacity management platforms that support proactive care orchestration and throughput optimization.

Drivers: Addressing the Global Healthcare Capacity Crisis

The growth of the overall market is being driven by the critical need to optimize patient throughput and the rising use of predictive analytics to manage chronic emergency department (ED) boarding. Recent industry data indicate that hospitals are caring for sicker, more complex patients, with inpatient volumes rising by about 5.3% in 2025 while total expenses increased by 7.5% (AHA, based on Strata Decision Technology benchmarks). At the same time, the WHO projects a global shortfall of up to 10 million health workers by 2030, pushing health systems to explore AI-enabled staffing and workforce optimization models. Hospital capacity management systems have shown measurable impact, with reported reductions in bed allocation delays and improved patient throughput (NHS/BMJ Informatics).

Restraints: Capital Expenditure and Change Management Barriers

Despite clear operational benefits, market growth is constrained by high capital requirements and the significant organizational change management needed for enterprise-wide deployment. Health system capacity management typically requires multi-million-dollar investments in software, integration, and dedicated staff, with case studies reporting implementation costs in the low single-digit millions of dollars for a large hospital. At the same time, analyses of healthcare data show that data quality remains a persistent challenge, which can undermine the performance and reliability of predictive analytics if not managed correctly.

Opportunities: Scaling Virtual Care and Digital Twin Simulation

Emerging opportunities in 'hospital-at-home' models and 'Digital Twin' technology are creating new growth avenues. By 2026, digital twin simulations are enabling health systems to forecast bed-request spikes with high accuracy, leading to a reduction in ambulance diversions. The expansion of virtual care hubs allows capacity management centers to monitor low-acuity patients remotely, preserving acute care beds for the most critically ill. This trend is particularly strong in North America, where hospitals are investing heavily in telehealth and remote monitoring integration to extend the reach of capacity management.

Transition to Autonomous and Self-Healing Operational Logistics

A defining trend in 2026 is the evolution of hospital capacity management from decision-support systems into autonomous orchestration platforms. AI-enabled solutions are increasingly automating bed assignment, discharge workflows, and housekeeping requests based on predicted patient volumes, reducing administrative burden and improving throughput. This shift is being driven by mounting workforce pressures; according to the U.S. Bureau of Labor Statistics, employment of registered nurses is projected to grow by 6% between 2023 and 2033, with approximately 194,500 openings annually due to retirements and workforce turnover. Meanwhile, the American Hospital Association's 2026 Costs of Caring report indicates that rising patient acuity contributed nearly 19% of hospital expense growth between 2019 and 2024. Consequently, hospitals are increasingly adopting AI- and generative AI-enabled platforms to automate operational tasks and provide real-time actionable insights.

Ambient Clinical Intelligence for Virtual Nursing and Patient Safety

The convergence of ambient intelligence, computer vision, and virtual nursing is expanding the scope of hospital capacity management beyond traditional patient flow. AI-enabled sensors and remote monitoring systems allow continuous observation of high-risk patients and support fall prevention, hand hygiene compliance, and early clinical intervention without requiring constant bedside presence. This trend is gaining momentum amid persistent staffing shortages; the World Health Organization estimates a global shortage of approximately 4.5 million nurses by 2030. In parallel, the U.S. Agency for Healthcare Research and Quality (AHRQ) reports that hospital-acquired conditions declined by 13% between 2014 and 2019, preventing an estimated 1.7 million patient harms and 87,000 deaths, demonstrating the clinical value of enhanced patient safety initiatives. As a result, virtual nursing and ambient clinical intelligence are becoming integral components of next-generation capacity management platforms.

Analysis by Component

Based on component, the software segment is expected to hold the largest share in 2026. This dominance is driven by the consolidation of hospitals into large integrated delivery networks (IDNs) that require a centralized 'source of truth' to manage regional patient flow. However, the services segment is projected to register a high CAGR during the forecast period. This growth is fueled by the expansion of consulting and implementation needs as health systems adopt more complex, AI-driven platforms.

Analysis by Deployment Mode

Based on deployment mode, the cloud-based segment is expected to account for the largest share in 2026. Cloud platforms are foundational to modern capacity management, enabling the prediction of patient census and discharge readiness across multiple facilities. The cloud-based segment is also projected to register the highest CAGR, as health systems increasingly adopt scalable, cost-effective solutions that support regional care coordination.

North America

North America is expected to dominate the global hospital capacity management market in 2026. The region's dominance is supported by a mature healthcare IT landscape and the widespread adoption of centralized operational models by large IDNs. These systems have reported serving thousands of additional patients annually through optimized bed orchestration. The presence of leading vendors and significant investment in digital health infrastructure continue to drive the market in the U.S. and Canada.

Asia Pacific

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This is driven by rapid healthcare infrastructure expansion and 'Smart Hospital' initiatives across China, India, and Australia. For example, major private healthcare providers in India are standardizing on centralized capacity management models to manage large patient volumes across multi-facility networks. The increasing adoption of cloud-based platforms and the digital transformation of public health agencies in the region are creating substantial opportunities.

The competitive landscape of the global hospital capacity management market is characterized by intense innovation and strategic acquisitions as vendors seek to provide end-to-end operational orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide demonstrated ROI in terms of length-of-stay reduction. Strategic moves, such as the integration of patient communication and throughput modules into unified ecosystems, are redefining vendor positioning in the June 2026 landscape.

TeleTracking Technologies, Oracle Health (Cerner), Epic Systems, GE HealthCare, Philips, Siemens Healthineers, McKesson, symplr, Health Catalyst, Infor, Stryker, LeanTaaS, Qventus, Care.ai, Artisight, Ascom Holding AG, Alcidion Group, Dedalus Group, WellSky, Central Logic.

The market is projected to reach USD 18.5 billion by 2036, growing at a CAGR of 11.5% from 2026 to 2036.

Hospitals implementing advanced capacity management platforms have reported reductions in length of stay and improvements in patient throughput, with some health systems achieving double-digit operational gains through optimized bed orchestration and discharge workflows.

The Artificial Intelligence & Machine Learning (AI/ML) segment is the fastest-growing, as predictive analytics becomes essential for forecasting demand.

Approximately 80% of new deployments are cloud-native, enabling regional coordination and rapid scalability.

North America holds the largest share, estimated at 52% in 2026, driven by a mature IT infrastructure and high demand for efficiency.

Digital twins allow for 95% accuracy in simulating bed-request spikes and staffing models, reducing ambulance diversions by 18%.

AI-driven staffing models reduce nurse overtime by 12% and improve clinician satisfaction scores by an average of 18%.

Tertiary Care Centers and multi-hospital Integrated Delivery Networks (IDNs) are the primary adopters of enterprise-wide capacity management platforms.

Integrated monitoring within capacity management platforms has been shown to improve clinical bundle compliance and reduce hospital-acquired conditions (HACs).

The top 5 players are TeleTracking Technologies, Inc., GE HealthCare, Philips, Siemens Healthineers, and Oracle Health (Cerner).

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Oct-2024

Published Date: Sep-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates