Resources

About Us

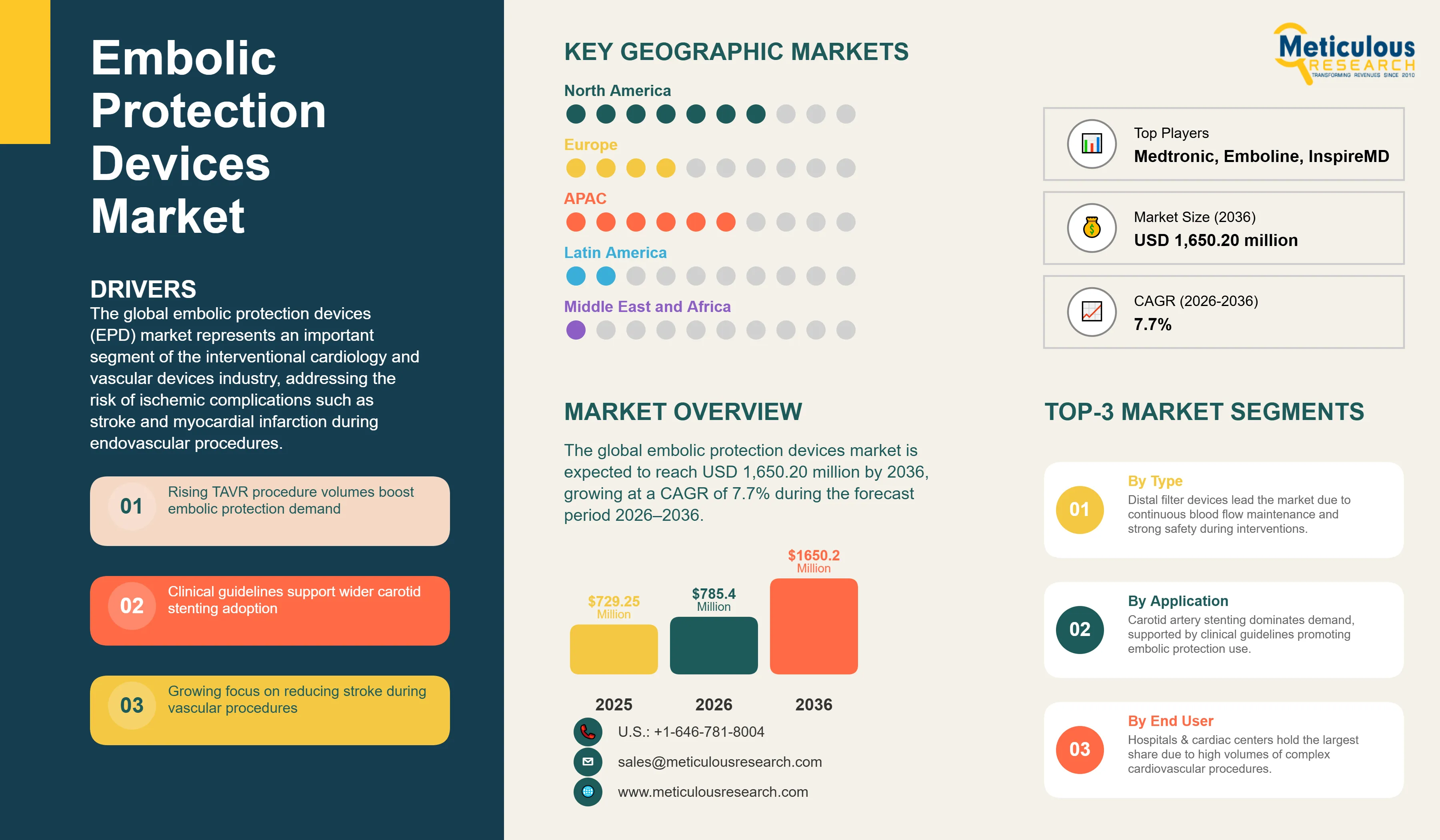

The global embolic protection devices market is estimated to be USD 785.40 million in 2026. This market is expected to reach USD 1,650.20 million by 2036, growing at a CAGR of 7.7% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global embolic protection devices (EPD) market represents an important segment of the interventional cardiology and vascular devices industry, addressing the risk of ischemic complications such as stroke and myocardial infarction during endovascular procedures. EPDs are specialized systems designed to capture or deflect embolic debris—including plaque, thrombus, and calcific material—that may become dislodged during interventions. Their use has become increasingly important as physicians treat older and higher-risk patient populations through minimally invasive approaches.

The growing burden of cardiovascular disease continues to support market expansion. According to the World Health Organization (WHO), cardiovascular diseases account for approximately 17.9 million deaths annually, representing nearly 32% of all global deaths, making them the leading cause of mortality worldwide. Furthermore, ischemic heart disease and stroke together account for more than 85% of cardiovascular deaths. These trends have contributed to rising volumes of catheter-based procedures and increased emphasis on minimizing procedural complications.

Clinical guidelines from the American College of Cardiology (ACC) and the Society for Cardiovascular Angiography and Interventions (SCAI) recommend the use of embolic protection during carotid artery stenting to reduce the risk of distal embolization and periprocedural stroke. Consequently, embolic protection has become a well-established component of carotid interventions. Meanwhile, cerebral protection technologies are gaining attention in transcatheter aortic valve replacement (TAVR) procedures as operators seek to further reduce neurological complications.

The rapid growth of structural heart interventions is also supporting demand. According to the Society of Thoracic Surgeons (STS) and ACC Transcatheter Valve Therapy (TVT) Registry, more than 276,000 TAVR procedures were performed in the United States between 2011 and 2019, with annual TAVR volumes reaching 72,991 procedures in 2019, surpassing surgical aortic valve replacement volumes for the first time. The registry also reported that 30-day mortality declined from 7.2% in 2011 to 2.5% in 2019, highlighting the continued advancement of minimally invasive cardiac therapies.

Continuous innovation in device design, including improvements in deliverability, pore size optimization, and debris capture efficiency, is further enhancing physician adoption. As healthcare systems increasingly focus on improving procedural outcomes and reducing the economic burden associated with stroke-related disability, embolic protection devices are expected to remain a strategic component of contemporary interventional cardiology and vascular procedures.

The growth of the global embolic protection devices market is primarily driven by the increasing procedural volumes in interventional cardiology and the rising clinical evidence supporting the efficacy of embolic protection in high-risk patients.

Rising Procedural Volumes in Transcatheter Aortic Valve Replacement (TAVR)

The rapid expansion of TAVR procedures globally is a major driver for the EPD market. As TAVR is increasingly performed on younger and lower-risk patients, the focus on reducing even minor procedural strokes has intensified. Cerebral embolic protection devices have shown significant promise in reducing the volume of new brain lesions during TAVR. This clinical benefit is driving a surge in adoption among structural heart specialists who seek to ensure the highest levels of safety for their patients, particularly as TAVR becomes a dominant therapy for aortic stenosis.

Established Clinical Guidelines and Favorable Reimbursement for Carotid Artery Stenting

Carotid artery stenting (CAS) remains a cornerstone application for EPDs, supported by robust clinical guidelines that mandate their use to prevent periprocedural stroke. Favorable reimbursement policies in major markets like the U.S. and Europe further support the consistent use of these devices. The ongoing shift from open surgery to minimally invasive endovascular techniques for carotid disease management ensures a steady demand for embolic protection, as interventionalists prioritize the reduction of neurological complications in high-risk surgical candidates.

Restraints: Addressing Technical Complexity and the High Cost of Advanced Protection Systems

Despite their life-saving potential, the adoption of EPDs is hindered by the technical challenges associated with device delivery and the significant cost burden on healthcare facilities. These factors can limit the routine use of embolic protection in certain clinical scenarios.

Technical Challenges and Potential for Vessel Injury During Device Manipulation

The deployment and retrieval of EPDs require a high degree of technical skill. In tortuous or heavily calcified vessels, the manipulation of these devices can sometimes lead to vessel injury, such as dissection or spasm. Furthermore, the presence of the device itself can sometimes interfere with the deliverability of stents or balloons. These technical complexities, coupled with the potential for device-related complications, can lead to clinical hesitancy, particularly among less experienced interventionalists, restraining the overall market penetration.

High Cost of Specialized EPDs and Budgetary Constraints in Healthcare

Embolic protection devices are sophisticated, single-use medical tools that carry a high price tag. In many healthcare systems, particularly in developing regions, the additional cost of an EPD can be a significant deterrent. Budgetary constraints in hospitals often lead to a risk-based approach where EPDs are only used in the most high-risk cases rather than as a routine procedural step. The lack of adequate incremental reimbursement for these devices in some markets further exacerbates this challenge, limiting their widespread adoption.

Opportunities: Expanding into Neurovascular Interventions and Developing Next-Gen Low-Profile Devices

The future of the EPD market lies in the expansion into emerging interventional areas and the development of next-generation devices that offer better deliverability and more comprehensive protection. These advancements offer significant potential for improving patient safety across a broader range of procedures.

Rising Demand for Embolic Protection in Neurovascular Thrombectomy

The rapid growth of mechanical thrombectomy for acute ischemic stroke is creating a significant opportunity for EPD manufacturers. Preventing 'embolization to new territories' during the retrieval of a thrombus is a major clinical goal. The development of specialized neurovascular EPDs that can safely navigate the delicate and tortuous vessels of the brain offers a high-growth opportunity. As thrombectomy procedures become more frequent and standardized globally, the integration of embolic protection into these workflows is expected to drive significant market expansion.

Development of Low-Profile and Bio-Compatible Next-Generation EPDs

There is a significant opportunity for the development of next-generation EPDs with lower profiles and enhanced bio-compatibility. Reducing the size of the delivery system would allow for the use of EPDs in smaller vessels and more complex anatomies. Furthermore, the use of advanced coatings to reduce the risk of thrombosis on the device itself could improve safety during long procedures. Innovation in device materials and design to provide more comprehensive 'proximal-to-distal' protection remains a key area for future market growth and differentiation.

Dominance of Cerebral Embolic Protection (CEP) in Structural Heart Procedures

A major trend in 2026 is the increasing adoption of cerebral embolic protection (CEP) devices in structural heart interventions, particularly transcatheter aortic valve replacement (TAVR). According to the American College of Cardiology (ACC) and Society of Thoracic Surgeons (STS) Transcatheter Valve Therapy Registry, annual TAVR procedures in the United States exceeded 100,000 cases by 2023, reflecting the continued expansion of minimally invasive valve therapies. Stroke remains one of the most feared complications following TAVR, with reported 30-day stroke rates ranging from 2–4% in contemporary practice. Growing awareness of post-procedural neurological and cognitive outcomes has accelerated interest in cerebral protection technologies. This trend is driving the development of next-generation CEP systems capable of protecting multiple cerebral vessels and improving debris capture efficiency, reflecting a broader emphasis on procedural safety and long-term patient quality of life. Furthermore, the U.S. FDA approved Boston Scientific's SENTINEL™ Cerebral Protection System in 2017, and by 2024 more than 175,000 patients worldwide had been treated with the device, underscoring the increasing clinical acceptance of cerebral embolic protection.

Increasing Use of Distal Filters in Complex Peripheral Vascular Interventions

Beyond carotid and coronary interventions, there is a growing trend toward the use of distal filter devices in complex peripheral vascular procedures. According to the U.S. Centers for Disease Control and Prevention (CDC), peripheral artery disease (PAD) affects approximately 6.5 million Americans aged 40 years and older, while the American Heart Association estimates that more than 230 million people globally are living with PAD. As physicians increasingly perform atherectomy and endovascular revascularization in heavily calcified lower-extremity lesions, concerns regarding distal embolization and limb-threatening complications have intensified. Studies from the Society for Cardiovascular Angiography and Interventions (SCAI) indicate that embolic debris is frequently generated during atherectomy procedures, supporting the selective use of embolic protection devices in high-risk cases. Consequently, the adoption of distal filters in peripheral vascular interventions is expanding, demonstrating the gradual extension of embolic protection technologies beyond traditional carotid applications into broader vascular care.

Analysis by Product Type

Based on product type, the distal filter devices segment is expected to hold the largest share of the global embolic protection devices market in 2026. This leading position is due to their established safety profile and the critical advantage of allowing continuous blood flow during interventional procedures. Distal filters are highly versatile and compatible with a wide range of guidewires and interventional tools, making them the preferred choice for the majority of carotid and coronary interventions. However, the proximal occlusion devices segment is projected to register the highest CAGR during the forecast period. Proximal occlusion is increasingly favored for high-risk procedures as it provides more comprehensive protection by stopping or reversing blood flow before any debris is dislodged. The rising complexity of neurovascular and high-risk cardiac interventions is driving the rapid adoption of these sophisticated protection systems.

Analysis by Application

By application, the carotid artery stenting (CAS) segment is expected to hold the largest share in 2026. CAS has long been the primary driver for the EPD market, with established clinical guidelines from major cardiovascular societies strongly recommending the use of embolic protection to prevent procedural stroke. The high procedural volume and mature clinical practice in CAS ensure its dominant revenue position. However, the transcatheter aortic valve replacement (TAVR) segment is projected to grow at the fastest CAGR during the forecast period. The rapid global expansion of TAVR procedures and the increasing clinical focus on reducing cerebral embolic events to improve long-term patient outcomes are creating a surge in demand for specialized cerebral protection devices, making this the most dynamic growth segment in the market.

Analysis by End User

By end user, the hospitals & cardiac centers segment is expected to hold the largest share in 2026. The vast majority of high-risk interventional procedures requiring EPDs, such as TAVR and complex carotid stenting, are performed in well-equipped hospital settings that have the necessary infrastructure and expert clinical teams. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. There is a growing global trend toward moving minimally invasive vascular procedures to outpatient settings to improve efficiency and reduce costs. As interventional techniques become more standardized and EPDs more user-friendly, ASCs are increasingly adopting these devices to ensure procedural safety in the outpatient environment.

Largest Share: North America

North America is expected to dominate the global embolic protection devices market in 2026, holding a market share of around 45%. This leading position is attributed to the high prevalence of cardiovascular diseases, an advanced healthcare infrastructure, and favorable reimbursement policies for interventional procedures. The region's strong focus on clinical innovation and the early adoption of advanced medical technologies drive significant demand. Key companies operating in the North America market are Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, and Edwards Lifesciences.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global embolic protection devices market, with a CAGR of 9.5% during the forecast period. This rapid expansion is fueled by the rapidly aging population, increasing healthcare expenditure, and the expansion of specialized cardiac care facilities in China and India. The rising awareness of stroke prevention and the adoption of minimally invasive interventional techniques are accelerating market penetration in this region. Key companies operating in the Asia Pacific market are Terumo Corporation, Asahi Intecc, and various regional distributors for global medical device leaders.

Competitive Landscape: Innovating for Precision and Safety in Vascular Care

The global embolic protection devices market is characterized by intense competition and a high degree of innovation among a group of well-established medical device leaders. Key players are focusing on developing lower-profile delivery systems and improving the capture efficiency of their devices. Strategic clinical trials are a major area of investment as companies seek to expand the indicated use of their EPDs into new procedural areas like TAVR and neurovascular thrombectomy. The market is also seeing strategic acquisitions as larger companies look to integrate specialized EPD technologies into their broader interventional portfolios. Furthermore, there is an increasing emphasis on providing 'procedural solutions' that combine EPDs with stents and delivery systems for optimized clinical workflows.

Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Cordis (Hellman & Friedman), Edwards Lifesciences Corporation, W. L. Gore & Associates, Inc., Terumo Corporation, Silk Road Medical, Inc., Teleflex Incorporated, Cook Medical, Contego Medical, Inc., Emboline, Inc., InspireMD, Inc., Keystone Heart Ltd., Innovative Cardiovascular Solutions LLC, Transverse Medical Inc., Penumbra, Inc., Becton Dickinson (BD), Stryker Corporation, Merit Medical Systems, Inc.

The global market is estimated at USD 785.40 million in 2026, with a projected growth to USD 1,650.20 million by 2036, at a CAGR of 7.7%.

Primary drivers include rising procedural volumes in TAVR and established clinical guidelines for stroke prevention in carotid artery stenting.

Major restraints include the technical complexity of device manipulation and the high cost of specialized protection systems.

Opportunities lie in expanding into neurovascular interventions and developing next-generation, low-profile devices.

The distal filter devices segment is expected to hold the largest share due to its established safety profile and versatility.

The transcatheter aortic valve replacement (TAVR) segment is projected to grow at the fastest CAGR, driven by the increasing focus on cerebral protection.

The hospitals & cardiac centers segment is expected to hold the largest share as the primary setting for complex vascular procedures.

North America is expected to dominate the market due to its advanced healthcare infrastructure and high procedural volumes.

Asia Pacific is projected to witness the fastest growth, fueled by an aging population and expanding cardiac care facilities.

Key trends include the shift toward specialized cerebral protection and the increasing use of EPDs in complex peripheral vascular interventions.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Procedural Volumes in Transcatheter Aortic Valve Replacement (TAVR)

4.2.1.2. Established Clinical Guidelines and Favorable Reimbursement for Carotid Artery Stenting

4.2.2. Restraints

4.2.2.1. Technical Challenges and Potential for Vessel Injury During Device Manipulation

4.2.2.2. High Cost of Specialized EPDs and Budgetary Constraints in Healthcare

4.2.3. Opportunities

4.2.3.1. Rising Demand for Embolic Protection in Neurovascular Thrombectomy

4.2.3.2. Development of Low-Profile and Bio-Compatible Next-Generation EPDs

4.2.4. Trends

4.2.4.1. Dominance of Cerebral Embolic Protection (CEP) in Structural Heart Procedures

4.2.4.2. Increasing Use of Distal Filters in Complex Peripheral Vascular Interventions

4.3. Porter's Five Forces Analysis

4.4. Clinical Trial Landscape and Regulatory Outlook

4.5. Value Chain Analysis

5. Global Embolic Protection Devices Market, by Product Type

5.1. Distal Filter Devices

5.2. Distal Occlusion Devices

5.3. Proximal Occlusion Devices

6. Global Embolic Protection Devices Market, by Application

6.1. Carotid Artery Stenting (CAS)

6.2. Transcatheter Aortic Valve Replacement (TAVR)

6.3. Coronary Interventions

6.4. Peripheral Vascular Interventions

6.5. Others

7. Global Embolic Protection Devices Market, by End User

7.1. Hospitals & Cardiac Centers

7.2. Ambulatory Surgical Centers (ASCs)

7.3. Specialty Clinics

8. Global Embolic Protection Devices Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Key Players Strategies

9.2. Market Share Analysis

9.3. Strategic Developments

9.4. Competitive Benchmarking

10. Company Profiles

10.1. Medtronic plc

10.2. Abbott Laboratories

10.3. Boston Scientific Corporation

10.4. Cordis (Hellman & Friedman)

10.5. Edwards Lifesciences Corporation

10.6. W. L. Gore & Associates, Inc.

10.7. Terumo Corporation

10.8. Silk Road Medical, Inc.

10.9. Teleflex Incorporated

10.10. Cook Medical

10.11. Contego Medical, Inc.

10.12. Emboline, Inc.

10.13. InspireMD, Inc.

10.14. Keystone Heart Ltd.

10.15. Innovative Cardiovascular Solutions LLC

10.16. Transverse Medical Inc.

10.17. Penumbra, Inc.

10.18. Becton, Dickinson and Company (BD)

10.19. Stryker Corporation

10.20. Merit Medical Systems, Inc.

11. Appendix

11.1. Abbreviations

11.2. Disclaimer

12. Key Questions Answered

Published Date: Aug-2024

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Jun-2024

Subscribe to get the latest industry updates