Resources

About Us

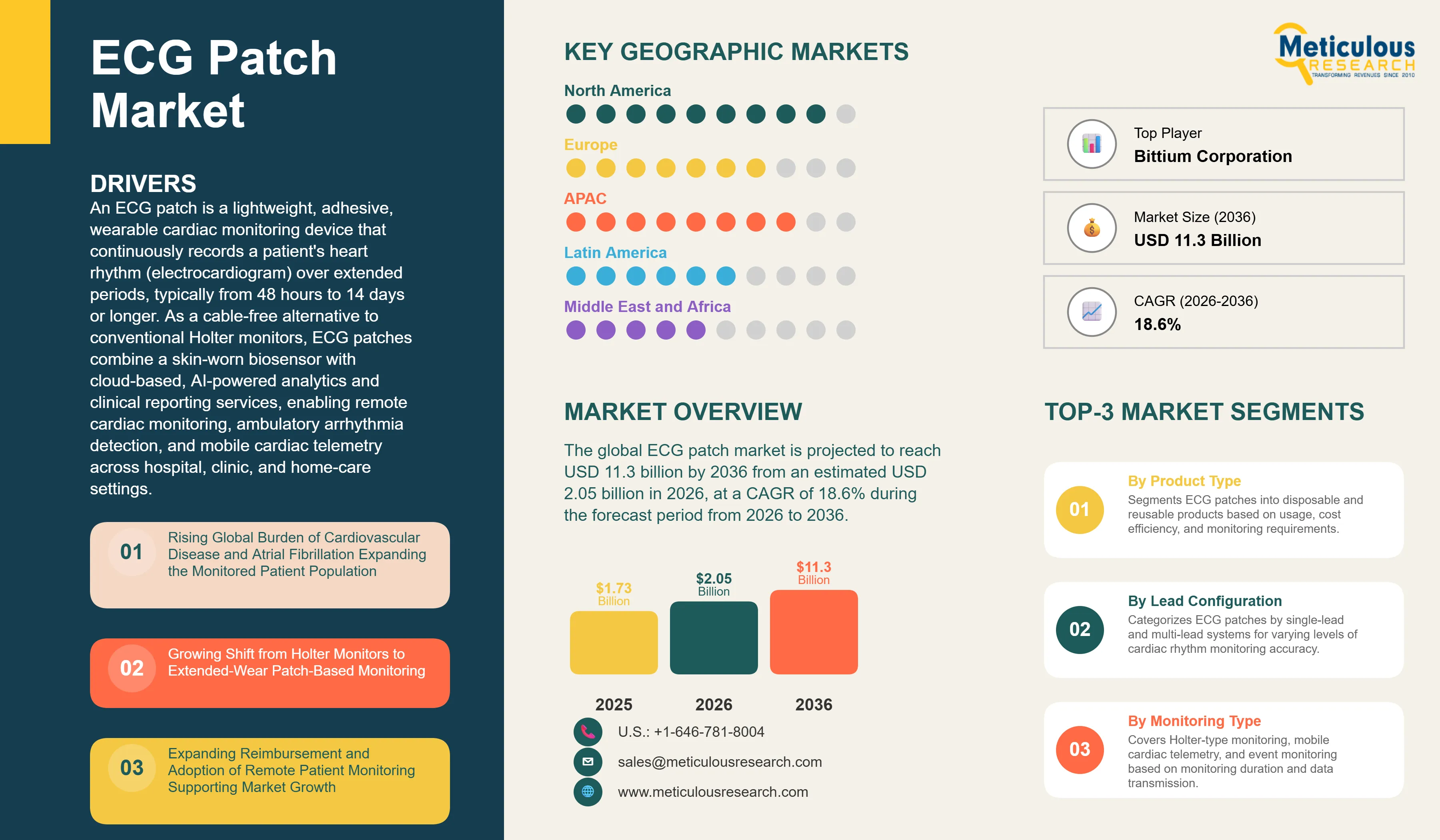

The global ECG patch market is projected to reach USD 11.3 billion by 2036 from an estimated USD 2.05 billion in 2026, at a CAGR of 18.6% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages

An ECG patch is a lightweight, adhesive, wearable cardiac monitoring device that continuously records a patient's heart rhythm (electrocardiogram) over extended periods, typically from 48 hours to 14 days or longer. As a cable-free alternative to conventional Holter monitors, ECG patches combine a skin-worn biosensor with cloud-based, AI-powered analytics and clinical reporting services, enabling remote cardiac monitoring, ambulatory arrhythmia detection, and mobile cardiac telemetry across hospital, clinic, and home-care settings. The ECG patch market spans single-use and reusable devices, single-lead and multi-lead configurations, and the software and monitoring services that convert raw ECG data into actionable diagnostic insight.

According to the World Health Organization, cardiovascular diseases account for approximately 17.9 million deaths each year, making them the leading cause of mortality worldwide. Atrial fibrillation (AFib) — the most common sustained cardiac arrhythmia and a major driver of ECG patch demand — affected an estimated 59 million people globally in 2019, up from 33.5 million in 2010, and the European Society of Cardiology projects the figure could rise by more than 60% by 2050. Because AFib is frequently paroxysmal and asymptomatic, long-term continuous monitoring with wearable ECG patches materially improves detection rates.

Clinical evidence has accelerated the transition from Holter monitors to extended-wear ECG patches. Wearable patch-based monitoring has demonstrated significantly higher diagnostic yield than short-duration Holter testing, alongside strong patient compliance owing to its discreet, water-resistant, cable-free design. This combination of better arrhythmia detection and improved adherence has made the ECG patch the preferred modality for ambulatory cardiac rhythm monitoring, particularly for atrial fibrillation screening, cryptogenic stroke evaluation, and post-ablation surveillance.

The market is further propelled by the expansion of remote patient monitoring and telehealth. Reimbursement frameworks, including remote monitoring and remote therapeutic monitoring codes, have made at-home cardiac monitoring economically viable, while the integration of ECG patch platforms with electronic health record (EHR) systems has streamlined clinical workflows. With continued advances in AI-powered arrhythmia detection, growing adoption of disposable wireless ECG patches, and rising demand across aging populations, the ECG patch market is positioned for sustained double-digit growth, driven by the need for early cardiac diagnosis, preventive care, and scalable remote monitoring.

Rising Global Burden of Cardiovascular Disease and Atrial Fibrillation

The escalating global prevalence of cardiovascular disease is the foremost driver of the ECG patch market. The World Health Organization estimates that cardiovascular diseases cause around 17.9 million deaths annually, representing the single largest cause of death worldwide. This large and growing disease base directly expands the population that requires cardiac rhythm monitoring.

Atrial fibrillation is the most consequential arrhythmia for the ECG patch market. Global AFib prevalence rose from 33.5 million cases in 2010 to approximately 59 million in 2019, and the European Society of Cardiology has warned that heart rhythm disorders represent a "silent epidemic," with roughly one in three people at lifetime risk. Because AFib is a leading cause of stroke and is often intermittent and asymptomatic, it frequently evades short-duration testing, creating strong clinical demand for the long-term continuous monitoring that ECG patches provide.

Demographic aging compounds this trend, as arrhythmia incidence rises sharply with age. As the global population over 60 expands and cardiovascular risk factors such as hypertension, obesity, and diabetes become more prevalent, the addressable patient population for wearable ECG monitoring continues to grow. This rising and recurring demand for arrhythmia detection underpins the sustained expansion of the ECG patch market.

Growing Shift from Holter Monitors to Extended-Wear ECG Patches

A structural shift from conventional Holter monitors to extended-wear ECG patches is a powerful growth driver, as healthcare providers increasingly favor longer-duration, patient-friendly monitoring. Traditional Holter monitors are typically limited to 24–48 hours and rely on cumbersome wires and electrodes, which constrain both diagnostic yield and patient comfort.

ECG patches address both limitations. Extended-wear patches record continuously for up to 14 days or longer, capturing intermittent arrhythmias that shorter tests miss, and their adhesive, cable-free, water-resistant form factor supports high patient adherence. Clinical studies have shown that patch-based long-term continuous monitoring delivers a substantially higher diagnostic yield than short-duration Holter testing — for example, landmark screening research demonstrated a roughly threefold improvement in atrial fibrillation detection with patch monitoring versus usual care.

This higher diagnostic yield translates into tangible health-system value, including fewer repeat tests and faster, more accurate diagnosis. As payers and providers recognize these benefits, extended-wear ECG patches are steadily displacing legacy Holter systems as the standard of care for ambulatory cardiac rhythm monitoring, directly expanding the ECG patch market.

Expanding Reimbursement and Adoption of Remote Patient Monitoring

The rapid expansion of remote patient monitoring (RPM) and telehealth is a key catalyst for ECG patch adoption, converting clinical demand into scalable, reimbursed care delivery. The shift toward value-based and preventive care has positioned wearable cardiac monitoring as a cornerstone of chronic disease management, particularly for atrial fibrillation, heart failure, and post-stroke surveillance.

Reimbursement has been decisive. In the United States, established codes for remote monitoring and remote therapeutic monitoring, together with specific coverage for extended ambulatory ECG monitoring following atrial fibrillation ablation, have made at-home cardiac monitoring financially sustainable for providers. Leading vendors have reinforced this shift through deep EHR integration; iRhythm, Philips, and Boston Scientific have all connected their cardiac monitoring platforms to major EHR systems such as Epic, streamlining ordering, reporting, and results delivery within clinical workflows.

This combination of reimbursement support, telehealth infrastructure, and workflow integration is expanding ECG patch use beyond the hospital into ambulatory diagnostic centers and the home. As remote cardiac monitoring becomes embedded in routine care pathways, the recurring, service-oriented revenue associated with ECG patches continues to grow, reinforcing the market's long-term expansion.

Expansion into Home-Based Care and Emerging Markets

The extension of ECG patch monitoring into home-based care and emerging markets represents one of the most significant growth opportunities, widening access far beyond the traditional hospital setting. As healthcare systems prioritize decentralized, patient-centric models, self-applied wearable ECG patches enable continuous cardiac monitoring at home, reducing hospital visits and supporting cardiac rehabilitation and chronic care management.

Home care is already the fastest-growing end-user setting for ECG patches, driven by the approval of prescription-grade, at-home cardiac monitoring, expanded remote monitoring reimbursement, and user-friendly patch kits designed for older adults. The disposable, cloud-connected nature of modern ECG patches makes them well suited to remote deployment, with data transmitted directly to clinicians for review.

Emerging markets offer a parallel opportunity. Rising cardiovascular disease burden across Asia-Pacific, Latin America, and the Middle East & Africa, combined with expanding telemedicine infrastructure and demand for affordable, accessible diagnostics, is opening large underserved populations to wearable cardiac monitoring. Manufacturers are responding with cost-efficient, battery-optimized ECG patch systems and regional distribution partnerships, positioning localization and home-based care as durable engines of ECG patch market growth.

By Product Type: The Single-use/Disposable Segment is Expected to Dominate the ECG Patch Market in 2026

Based on product type, the ECG patch market is segmented into single-use/disposable ECG patches and reusable ECG patches. In 2026, the single-use/disposable segment is expected to account for the largest share of 68.2% of the global ECG patch market. The large share of this segment is primarily attributed to infection-control advantages, elimination of reprocessing, and its established role in ambulatory diagnostic monitoring, where single-patient-use devices simplify logistics in clinical and outpatient settings.

Advances in flexible printed electronics have reduced manufacturing costs while improving patch adhesion and signal quality, further reinforcing the disposable segment's dominance across diagnostic ambulatory ECG applications.

However, the reusable ECG patch segment is projected to record the highest CAGR during the forecast period. Growth is driven by the expansion of continuous remote patient monitoring and home-based care, where reusable, multi-parameter patches offer favorable long-run economics for extended and repeated monitoring of chronic cardiac patients.

By Lead Configuration: The Single-Lead Segment Dominated the ECG Patch Market in 2025

Based on lead configuration, the market is segmented into single-lead and multi-lead ECG patches. In 2025, the single-lead segment accounted for the largest share of 61.5% of the global ECG patch market. Single-lead patches dominate because of their high clinical utility in ambulatory cardiac rhythm tracking — particularly for atrial fibrillation and post-operative arrhythmia monitoring — combined with their compact, low-cost, easy-to-apply design.

Their simplicity supports strong patient compliance and streamlined workflows, making single-lead patches the workhorse of extended-wear ambulatory ECG monitoring.

However, the multi-lead ECG patch segment is projected to grow fastest during the forecast period, driven by rising demand for richer diagnostic detail. Multi-lead and multi-channel patches enable more comprehensive arrhythmia characterization and morphology analysis, supporting adoption in more complex cardiac assessments as manufacturers commercialize higher-lead-count wearable systems.

By Monitoring Type: The Holter-Type/LTCM Segment is Expected to Dominate the ECG Patch Market in 2025

Based on monitoring type, the market is segmented into Holter-type/long-term continuous monitoring (LTCM), mobile cardiac telemetry (MCT), and cardiac event monitoring. In 2026, the Holter-type/LTCM segment is expected to account for the largest share of 47.8% of the global ECG patch market. The largest share of this segment is mainly due to its widespread use of extended-wear patches for continuous multi-day recording and retrospective analysis, which forms the core diagnostic use case for ambulatory ECG monitoring.

Established clinical validation, broad reimbursement, and the strong diagnostic yield of long-term continuous monitoring reinforce the segment's dominant position.

However, the mobile cardiac telemetry (MCT) segment is projected to grow fastest during the forecast period. MCT patches transmit ECG data in near real time, enabling faster clinical response for higher-risk patients, and typically command higher reimbursement, factors that are accelerating adoption as connectivity and cloud analytics mature.

By Application: The Atrial Fibrillation Detection Segment Dominates the ECG Patch Market in 2026

Based on application, the market is segmented into atrial fibrillation detection, post-operative & post-ablation monitoring, cryptogenic stroke evaluation, syncope & palpitation evaluation, and other applications. In 2026, the atrial fibrillation detection segment accounts for the largest share of 43.9% of the global ECG patch market. As the most common sustained arrhythmia and a leading cause of stroke, atrial fibrillation represents the primary clinical indication for ECG patch monitoring, and early AFib screening has become a public-health priority worldwide.

The high and rising prevalence of AFib, combined with the superior detection rates of long-term patch monitoring, sustains this segment's leading share.

However, the cryptogenic stroke evaluation segment is projected to grow fastest during the forecast period. Extended patch-based monitoring is increasingly used to identify occult atrial fibrillation in patients with unexplained (cryptogenic) stroke, where prolonged monitoring materially improves diagnosis and guides anticoagulation — driving rapid adoption in this high-value clinical pathway.

By End User: The Hospitals & Clinics Segment Dominated the ECG Patch Market in 2025

Based on end user, the market is segmented into hospitals & clinics, ambulatory & diagnostic testing centers, home care settings, and others. In 2026, the hospitals & clinics segment accounts for the largest share of 52.3% of the global ECG patch market. Hospitals and clinics dominate owing to high patient inflow, the availability of cardiologists and electrophysiologists, and their role as the primary point of prescription and diagnosis for ambulatory cardiac monitoring.

Their established clinical infrastructure and integration with diagnostic and reimbursement pathways reinforce the segment's leading position.

However, the home care settings segment is projected to grow fastest during the forecast period. The migration of cardiac monitoring into the home, enabled by self-applied disposable patches, expanded remote monitoring reimbursement, and telehealth adoption, is rapidly expanding at-home ECG monitoring, making home care the highest-growth end-user setting.

North America Dominates the Global ECG Patch Market in 2025

Based on geography, the global ECG patch market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2026, North America accounts for the largest share of 54.8% of the global ECG patch market.

The large share of North America is attributed to well-established remote patient monitoring reimbursement, high telehealth penetration, early integration of wearable cardiac monitoring into clinical pathways, and the presence of leading manufacturers including iRhythm Technologies, Boston Scientific, and Baxter. The United States represents the dominant national market, supported by expedited regulatory pathways for wearable cardiac devices and payer programs that incentivize extended ECG monitoring after atrial fibrillation ablation.

However, the Asia-Pacific is expected to register the fastest CAGR during the forecast period. Rapid demographic aging, a rising burden of cardiovascular disease across China, India, and Japan, expanding healthcare infrastructure, and growing telemedicine adoption are driving demand for affordable, accessible ECG patch monitoring. Europe remains a significant market, led by Germany, the United Kingdom, and France, where atrial fibrillation screening initiatives and established reimbursement support steady growth.

Major companies in the global ECG patch market have pursued strategies including product launches & enhancements, partnerships & collaborations, acquisitions, and geographic expansion to strengthen their market positions. Product launches and enhancements, together with EHR integrations and clinical evidence generation, have accounted for the majority of strategic activity, as established players defend share and emerging vendors differentiate through AI and connectivity.

Some of the prominent players operating in the global ECG patch market include iRhythm Technologies, Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Boston Scientific Corporation (U.S.), Baxter International Inc. (U.S.), GE HealthCare Technologies Inc. (U.S.), Medtronic plc (Ireland), VitalConnect, Inc. (U.S.), VivaLNK, Inc. (U.S.), Bittium Corporation (Finland), AliveCor, Inc. (U.S.), Cardiac Insight, Inc. (U.S.), LifeSignals, Inc. (U.S.), SmartCardia SA (Switzerland), Nuubo (Medical Wireless Sensing Ltd.) (Spain), and Isansys Lifecare Limited (U.K.).

|

Particulars |

Details |

|

Forecast Period |

2026–2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

18.6% |

|

Market Size (Value) in 2026 |

USD 2.05 Billion |

|

Market Size (Value) in 2036 |

USD 11.30 Billion |

|

Segments Covered |

By Product Type - Single-use/Disposable ECG Patches - Reusable ECG Patches By Lead Configuration - Single-lead ECG Patches - Multi-lead ECG Patches By Monitoring Type - Holter-type/Long-Term Continuous Monitoring (LTCM) - Mobile Cardiac Telemetry (MCT) - Cardiac Event Monitoring By Component - Hardware (Patch Devices, Gateways & Transmitters) - Software & Services (AI Analysis, Monitoring Services) By Application - Atrial Fibrillation Detection - Post-operative & Post-ablation Monitoring - Cryptogenic Stroke Evaluation - Syncope & Palpitation Evaluation - Other Applications By End User - Hospitals & Clinics - Ambulatory & Diagnostic Testing Centers - Home Care Settings - Others |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, Netherlands, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa) |

|

Key Companies |

iRhythm Technologies, Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Boston Scientific Corporation (U.S.), Baxter International Inc. (U.S.), GE HealthCare Technologies Inc. (U.S.), Medtronic plc (Ireland), VitalConnect, Inc. (U.S.), VivaLNK, Inc. (U.S.), Bittium Corporation (Finland), AliveCor, Inc. (U.S.), Cardiac Insight, Inc. (U.S.), LifeSignals, Inc. (U.S.), SmartCardia SA (Switzerland), Nuubo (Medical Wireless Sensing Ltd.) (Spain), and Isansys Lifecare Limited (U.K.). |

The global ECG patch market size is estimated at USD 2.05 billion in 2026.

The market is projected to grow from USD 2.05 billion in 2026 to USD 11.30 billion by 2036, at a CAGR of 18.6%.

The ECG patch market is projected to reach USD 11.30 billion by 2036, at a compound annual growth rate (CAGR) of 18.6% from 2026 to 2036.

Key companies operating in this market include iRhythm Technologies, Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Boston Scientific Corporation (U.S.), Baxter International Inc. (U.S.), GE HealthCare Technologies Inc. (U.S.), Medtronic plc (Ireland), VitalConnect, Inc. (U.S.), Bittium Corporation (Finland), AliveCor, Inc. (U.S.), and others.

Growing integration of AI-powered arrhythmia detection and cloud analytics, the shift from Holter monitors to extended-wear patches, and the convergence of consumer wearables with clinical-grade ECG patches are prominent trends in the market.

By product type, the single-use/disposable segment held the largest share; by lead configuration, the single-lead segment dominated; by monitoring type, the Holter-type/LTCM segment led while mobile cardiac telemetry is expected to grow fastest; by component, the hardware segment held the largest share; by application, atrial fibrillation detection dominated; by end user, the hospitals & clinics segment held the largest share; and by geography, North America commanded the largest share in 2026.

North America holds the largest share of the ECG patch market in 2026, supported by strong remote patient monitoring reimbursement and telehealth penetration. Asia-Pacific is expected to register the highest growth rate during the forecast period, driven by rising cardiovascular disease burden and healthcare digitization.

Key drivers include the rising global burden of cardiovascular disease and atrial fibrillation, the shift from Holter monitors to extended-wear patch-based monitoring, and expanding reimbursement and adoption of remote patient monitoring. These factors are collectively accelerating adoption of ECG patches across care settings.

1. Introduction

1.1. Market Definition

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Global Burden of Cardiovascular Disease and Atrial Fibrillation Expanding the Monitored Patient Population

4.2.1.2. Growing Shift from Holter Monitors to Extended-Wear Patch-Based Monitoring

4.2.1.3. Expanding Reimbursement and Adoption of Remote Patient Monitoring Supporting Market Growth

4.2.2. Restraints

4.2.2.1. Reimbursement Uncertainty and Pricing Pressure Limiting Market Growth

4.2.3. Opportunities

4.2.3.1. Expansion into Home-Based Care and Emerging Markets Generating Growth Opportunities

4.2.3.2. Rising Adoption of AI-Enabled Analysis and EHR Integration Accelerating Market Expansion

4.2.4. Challenges

4.2.4.1. Data Privacy, Security, and Regulatory Compliance Concerns Expected to Remain a Major Challenge

4.3. Key Trends

4.3.1. Growing Integration of AI-Powered Arrhythmia Detection and Cloud Analytics

4.3.2. Convergence of Consumer Wearables and Clinical-Grade ECG Patches

4.4. Vendor Selection Criteria/Factors Influencing Purchase Decisions

4.5. Use Cases

4.6. Porter's Five Forces Analysis

4.6.1. Bargaining Power of Buyers: Moderate to High

4.6.2. Bargaining Power of Suppliers: Moderate

4.6.3. Threat of Substitutes: Moderate

4.6.4. Threat of New Entrants: Moderate to High

4.6.5. Degree of Competition: High

4.7. Value Chain Analysis

4.8. Pricing Analysis

4.9. Technology Analysis

4.10. PESTEL Analysis

5. ECG Patch Market Assessment—By Product Type

5.1. Overview

5.2. Single-Use/Disposable ECG Patches

5.3. Reusable ECG Patches

6. ECG Patch Market Assessment—By Lead Configuration

6.1. Overview

6.2. Single-Lead ECG Patches

6.3. Multi-Lead ECG Patches

7. ECG Patch Market Assessment—By Monitoring Type

7.1. Overview

7.2. Holter-Type/Long-Term Continuous Monitoring (LTCM)

7.3. Mobile Cardiac Telemetry (MCT)

7.4. Cardiac Event Monitoring

8. ECG Patch Market Assessment—By Application

8.1. Overview

8.2. Atrial Fibrillation Detection

8.3. Post-operative & Post-ablation Monitoring

8.4. Cryptogenic Stroke Evaluation

8.5. Syncope & Palpitation Evaluation

8.6. Other Applications

9. ECG Patch Market Assessment—By End User

9.1. Overview

9.2. Hospitals & Clinics

9.3. Ambulatory & Diagnostic Testing Centers

9.4. Home Care Settings

9.5. Others

10. ECG Patch Market Assessment—By Geography

10.1. Overview

10.2. North America

10.2.1. United States

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. United Kingdom

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Netherlands

10.3.7. Switzerland

10.3.8. Rest of Europe

10.4. Asia Pacific

10.4.1. Japan

10.4.2. China

10.4.3. India

10.4.4. South Korea

10.4.5. Australia & New Zealand

10.4.6. Rest of Asia Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East & Africa

10.6.1. Saudi Arabia

10.6.2. United Arab Emirates

10.6.3. South Africa

10.6.4. Rest of Middle East & Africa

11. Competitive Landscape

11.1. Introduction

11.2. Key Growth Strategies

11.3. Competitive Benchmarking

11.4. Competitive Dashboard

11.4.1. Industry Leaders

11.4.2. Market Differentiators

11.4.3. Vanguards

11.4.4. Emerging Companies

11.5. Market Share/Position Analysis

12. Company Profiles (Company Overview, Financial Overview, Product Portfolio, Strategic Developments)

12.1. iRhythm Technologies, Inc. (U.S.)

12.2. Koninklijke Philips N.V. (Netherlands)

12.3. Boston Scientific Corporation (U.S.)

12.4. Baxter International Inc. (U.S.)

12.5. GE HealthCare Technologies Inc. (U.S.)

12.6. Medtronic plc (Ireland)

12.7. VitalConnect, Inc. (U.S.)

12.8. VivaLNK, Inc. (U.S.)

12.9. Bittium Corporation (Finland)

12.10. AliveCor, Inc. (U.S.)

12.11. Cardiac Insight, Inc. (U.S.)

12.12. LifeSignals, Inc. (U.S.)

12.13. SmartCardia SA (Switzerland)

12.14. Nuubo (Medical Wireless Sensing Ltd.) (Spain)

12.15. Isansys Lifecare Limited (U.K.)

13. Appendix

13.1. Available Customization

13.2. Related Reports

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jun-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates