Resources

About Us

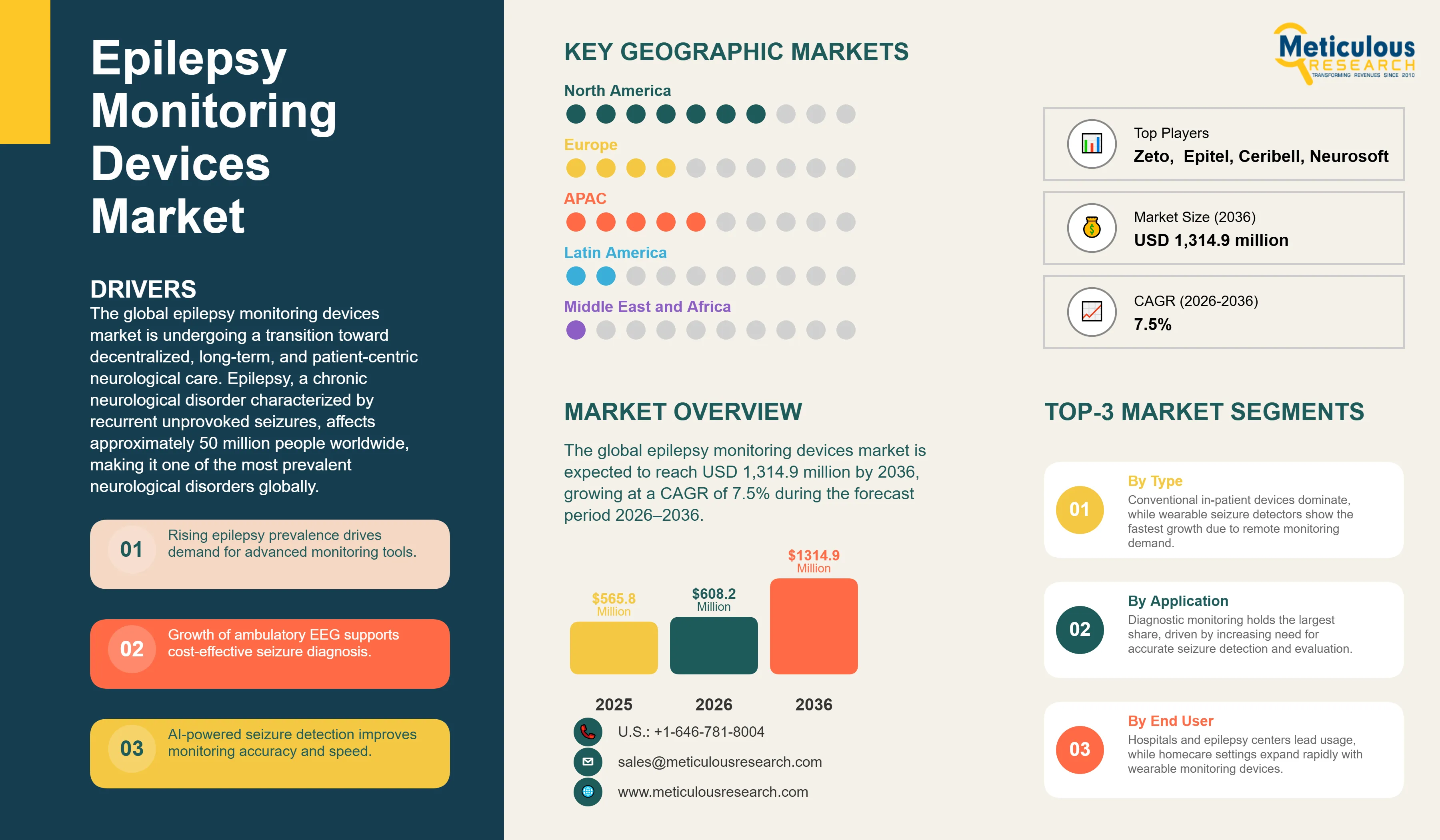

Epilepsy Monitoring Devices Market Size, Share & Trends Analysis by Product Type (Conventional, Ambulatory, Wearables, Implantable), Technology (EEG, sEMG, Multi-modal, AI), Application, End User, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

Report ID: MRHC - 1042014 Pages: 276 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global epilepsy monitoring devices market was valued at USD 608.2 million in 2026. This market is expected to reach USD 1,314.9 million by 2036, growing at a CAGR of 7.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global epilepsy monitoring devices market is undergoing a transition toward decentralized, long-term, and patient-centric neurological care. Epilepsy, a chronic neurological disorder characterized by recurrent unprovoked seizures, affects approximately 50 million people worldwide, making it one of the most prevalent neurological disorders globally. According to the World Health Organization (2024), nearly 5 million people are diagnosed with epilepsy annually. Despite the widespread use of anti-seizure medications, approximately one-third of patients experience inadequate seizure control, necessitating advanced diagnostic monitoring for presurgical evaluation, seizure characterization, and neurostimulation optimization. Market growth is further supported by increasing awareness of diagnostic delays and treatment gaps, particularly in low- and middle-income countries, which has accelerated demand for continuous EEG monitoring, ambulatory monitoring systems, and wearable seizure-detection technologies.

Modern epilepsy monitoring is increasingly characterized by the convergence of electroencephalography (EEG), wearable technologies, and artificial intelligence. Although conventional in-patient video-EEG monitoring remains the clinical gold standard for seizure characterization and presurgical evaluation, its high cost and limited availability have accelerated the adoption of ambulatory EEG solutions. Ambulatory EEG systems enable prolonged monitoring in the patient's home environment, allowing seizure activity to be recorded during routine daily activities and sleep while offering a more cost-effective alternative to hospital-based monitoring. This transition is particularly evident across developed healthcare systems, where healthcare providers are increasingly utilizing ambulatory monitoring to expand diagnostic capacity, improve patient convenience, and reduce pressure on specialized epilepsy monitoring units.

The rise of wearable seizure detection technologies is another key trend shaping the market. These devices employ multimodal sensors, including accelerometry, photoplethysmography (PPG), and other physiological measurements, to provide real-time alerts for convulsive seizures and enhance patient safety. SUDEP is estimated to occur in approximately one per 1,000 people with epilepsy annually, with elevated risk among individuals with poorly controlled seizures. In parallel, AI-driven cloud analytics are enabling automated review of large volumes of neurological data, reducing the interpretation burden on neurophysiologists and improving seizure documentation accuracy.

Geographically, North America is expected to account for approximately 42% of the global market in 2026, supported by a well-established network of accredited epilepsy centers and high adoption of advanced monitoring technologies. Meanwhile, Asia-Pacific is projected to register the fastest growth through 2036. With an estimated 9–10 million people living with epilepsy in China and increasing healthcare investments across countries such as India, demand for both premium diagnostic systems and cost-effective ambulatory monitoring solutions is expected to rise. As healthcare systems continue to embrace digital health and remote patient monitoring, epilepsy monitoring devices are poised to play an increasingly important role in personalized neurological care.

The primary driver for the epilepsy monitoring devices market is the substantial global burden of epilepsy and the growing need for accurate diagnosis and seizure characterization. According to the World Health Organization (2024), epilepsy is among the most common neurological disorders worldwide, with approximately 5 million new cases diagnosed annually. In addition, the increasing preference for cost-effective and patient-centric care models is accelerating the adoption of ambulatory monitoring technologies. Compared with hospital-based video-EEG monitoring, ambulatory EEG systems enable prolonged monitoring in home settings while reducing healthcare resource utilization and improving patient convenience. Growing acceptance of remote monitoring and favorable reimbursement coverage for long-term EEG procedures in several developed markets are further supporting the expansion of outpatient neurology services and home-based epilepsy care.

A major restraint for the epilepsy monitoring devices market is the technical and operational limitations associated with current seizure detection technologies. Although wearable devices have demonstrated significant potential for continuous monitoring, false alarms and inconsistent detection performance may contribute to alarm fatigue among caregivers and negatively affect patient adherence. In addition, the substantial capital investment required for advanced video-EEG systems and specialized monitoring infrastructure restricts their adoption among community hospitals and healthcare providers in resource-constrained settings. According to the World Health Organization, nearly 80% of people with epilepsy reside in low- and middle-income countries, where limited access to neurologists, EEG facilities, and specialized diagnostic services continues to hinder market penetration.

The growing emphasis on SUDEP prevention and remote patient management presents a significant opportunity for the epilepsy monitoring devices market. Sudden Unexpected Death in Epilepsy (SUDEP) is estimated to occur at a rate of approximately 1.16 cases per 1,000 person-years, driving the development of next-generation wearable devices equipped with automated seizure detection and real-time alert capabilities. In addition, the pediatric population represents a promising growth avenue, as a substantial proportion of epilepsy cases are diagnosed during childhood, creating demand for non-invasive, patient-friendly monitoring technologies. Furthermore, expanding healthcare infrastructure, improving access to neurological care, and increasing healthcare expenditures across Asia-Pacific countries, particularly China and India, are expected to create substantial opportunities for manufacturers of both conventional EEG systems and ambulatory monitoring solutions. The increasing affordability and accessibility of mobile and home-based monitoring technologies are further expected to support market growth during the forecast period.

Maintaining data privacy and cybersecurity in cloud-based monitoring platforms is a critical challenge, given the sensitive nature of neurological and video data. Manufacturers must also navigate complex regulatory pathways to secure clearance for AI-based detection modules across different global regions. Technical challenges also persist in developing sensors with high sensitivity for non-convulsive seizures in ambulatory settings. Furthermore, achieving seamless interoperability with diverse electronic health record (EHR) systems is essential for integrating long-term monitoring data into the broader clinical workflow, yet it remains a significant hurdle for many technology providers.

Artificial intelligence is increasingly transitioning from research settings to routine clinical practice, emerging as a key trend in the epilepsy monitoring devices market. According to the U.S. Food and Drug Administration (FDA), the number of AI-enabled medical devices receiving marketing authorization has increased significantly in recent years, reflecting the growing adoption of AI across healthcare. AI-assisted algorithms are enabling automated analysis of thousands of hours of EEG recordings, substantially reducing manual review time and supporting more efficient seizure identification by neurologists. In addition, FDA-cleared wearable solutions, such as Empatica's EpiMonitor platform, are accelerating the adoption of AI-enabled remote epilepsy monitoring technologies.

Another prominent trend shaping the market is the shift toward multi-modal and ultra-long-term monitoring technologies. Next-generation devices increasingly combine EEG with physiological signals such as motion, electrodermal activity, heart rate, and photoplethysmography to improve seizure detection accuracy. Furthermore, the development of minimally invasive subcutaneous and behind-the-ear EEG systems is expanding the duration of continuous monitoring from days to months and even years. For instance, Epiminder's FDA-authorized Minder® system is designed for up to three years of continuous monitoring, highlighting the growing emphasis on long-term, patient-centric epilepsy management.

Based on product type, the market is segmented into Conventional/In-patient Devices, Ambulatory Devices, Wearable Seizure Detectors, and Implantable Monitors. In 2026, the Conventional/In-patient Devices segment is expected to hold the largest share of the market. This is due to the high unit cost and the essential role of high-density video-EEG systems in the definitive diagnosis and presurgical evaluation of epilepsy.

The Wearable Seizure Detectors segment is projected to witness the fastest growth, with a CAGR of approximately 10.5%. This growth is driven by increasing safety concerns, the rising focus on SUDEP prevention, and the rapid innovation in consumer-oriented neurological health technology.

Based on end user, the market is segmented into Hospitals & Epilepsy Centers, Diagnostic Centers, and Homecare/Patients. In 2026, the Hospitals & Epilepsy Centers segment is expected to hold the largest share, accounting for nearly 65% of the market. These facilities remain the primary hubs for complex diagnostic and surgical planning procedures that require specialized equipment.

The Homecare/Patients segment is projected to witness the fastest growth, reflecting the broader healthcare trend toward decentralized care and the increasing availability of reliable, user-friendly seizure detection tools for personal use.

North America is expected to account for the largest share of the global epilepsy monitoring devices market in 2026, representing approximately 42% of total market revenue. The region's dominance is primarily attributed to the presence of a well-established network of accredited epilepsy centers, favorable reimbursement frameworks, and high adoption of advanced monitoring and wearable technologies. According to the U.S. Centers for Disease Control and Prevention (CDC), nearly 1 in 26 individuals in the U.S. are expected to develop epilepsy during their lifetime, creating sustained demand for diagnostic and long-term monitoring solutions.

Europe represents another significant market, supported by increasing adoption of ambulatory EEG systems and growing emphasis on reducing pressure on specialized epilepsy monitoring units. Meanwhile, Asia-Pacific is projected to register the highest growth during the forecast period, with an estimated CAGR of ~9.2%. According to the World Health Organization and the Chinese Association Against Epilepsy, nearly 10 million people in China are living with epilepsy, with approximately 400,000 new cases diagnosed annually. Rising healthcare expenditures, improving access to neurological care, and the presence of both global companies such as Natus Medical Incorporated and Nihon Kohden Corporation and an expanding base of regional manufacturers are expected to support strong market growth across the region.

The global epilepsy monitoring devices market is highly competitive, featuring established leaders in neurological diagnostics and innovative startups focusing on wearable and AI technology. Natus Medical, Nihon Kohden, and Medtronic maintain strong positions through their comprehensive portfolios of diagnostic and therapeutic tools. Competition is increasingly focused on sensor precision, battery life in ambulatory devices, and the clinical validation of automated detection algorithms.

Key players in the global market include Natus Medical Incorporated (U.S.), Nihon Kohden Corporation (Japan), Medtronic plc (Ireland), Koninklijke Philips N.V. (Netherlands), Compumedics Limited (Australia), Empatica Inc. (U.S.), Cadwell Industries, Inc. (U.S.), Bio-Signal Group Corp. (U.S.), Neurosoft (Russia), Lifelines Neuro (U.S.), Advanced Brain Monitoring, Inc. (U.S.), Drägerwerk AG & Co. KGaA (Germany), Micromed (Italy), Brain Scientific Inc. (U.S.), Zeto, Inc. (U.S.), Seer Medical (Australia), Epitel, Inc. (U.S.), and Ceribell, Inc. (U.S.).

The market is projected to reach USD 1,314.9 million by 2036, growing at a CAGR of 7.5% from 2026 to 2036.

Epilepsy affects approximately 50 million people worldwide, with 5 million new diagnoses annually according to the WHO.

Ambulatory EEG is significantly more cost-effective, averaging USD 970 per test in the U.S., compared to inpatient video-EEG which can cost up to USD 3,000 per day.

The Asia-Pacific region is projected to witness the fastest growth, with a CAGR of approximately 9.2% due to expanding healthcare infrastructure.

The risk of SUDEP is estimated at approximately 1.16 per 1,000 person-years among people with epilepsy.

The rising global prevalence of epilepsy, the shift toward cost-effective home-based monitoring, and advancements in AI-driven detection are the primary drivers.

The market is expected to grow at a CAGR of 7.5% during the forecast period 2026–2036.

Conventional/In-patient Devices hold the largest share due to their essential role in definitive diagnosis and presurgical evaluation.

High false-alarm rates (FAR), ranging from 0.1 to 2.0 per day, remain a significant technical challenge leading to alarm fatigue.

The market is led by Natus Medical Incorporated, Nihon Kohden Corporation, Compumedics Limited, Medtronic plc, and Cadwell Industries, Inc. Other notable participants include Philips, Masimo Corporation, Empatica Inc., NeuroPace, Inc., and GE HealthCare Technologies Inc.

Published Date: Jan-2024

Published Date: Dec-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates