Resources

About Us

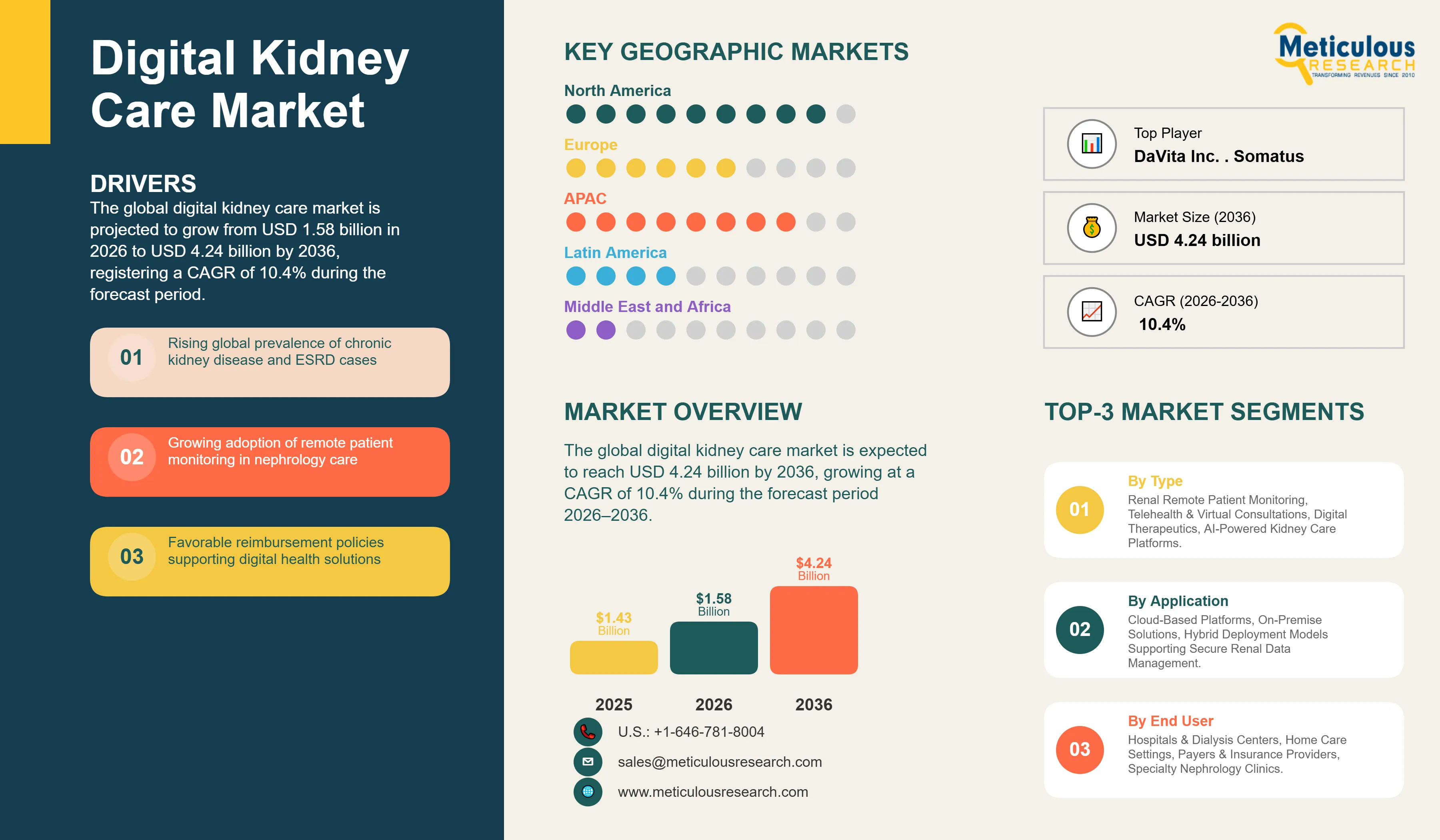

The global digital kidney care market was valued at USD 1.58 billion in 2026. This market is expected to reach USD 4.24 billion by 2036, growing at a CAGR of 10.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global digital kidney care market represents a paradigm shift in the management of chronic kidney disease (CKD) and end-stage renal disease (ESRD), moving from episodic, clinic-based care toward continuous, home-based monitoring and intervention. Digital nephrology solutions, including telehealth platforms, renal remote patient monitoring (RPM) systems, and digital therapeutics, leverage real-time data and AI-driven insights to optimize patient outcomes and reduce the overall cost of care. As of 2026, the market is undergoing rapid expansion, driven by the global imperative to address the rising prevalence of CKD, which currently affects an estimated 850 million people worldwide (Source: ISN). The transition to digital renal care is essential for managing the complex needs of this patient population, particularly in light of the global shortage of nephrologists.

The integration of digital health into the nephrology workflow is enabling more proactive and personalized care delivery. Remote patient monitoring systems allow clinicians to track vital signs, fluid balance, and laboratory results in real-time, facilitating early intervention and preventing acute complications. Furthermore, the rise of digital therapeutics for kidney disease is providing patients with tools for self-management, including AI-driven nutrition counseling and medication adherence support. As healthcare systems transition toward value-based care models, the demand for digital kidney care solutions that can demonstrate improved clinical outcomes and reduced hospitalizations is expected to surge. Modern digital renal care platforms are increasingly designed to provide a holistic view of the patient journey, integrating data from wearable devices, home dialysis machines, and electronic health records (EHRs).

Drivers: Addressing the Global CKD Burden with Digital Health and Remote Monitoring

The primary driver for the digital kidney care market is the escalating global burden of chronic kidney disease (CKD) and its associated comorbidities, such as diabetes and hypertension. According to the CDC, approximately 37 million adults in the U.S. are estimated to have CKD, with many remaining undiagnosed until the advanced stages. This massive patient population necessitates the adoption of digital health solutions to scale care delivery and improve early detection. Furthermore, favorable reimbursement policies for remote patient monitoring (RPM) and telehealth, particularly in North America and Europe, are significantly accelerating market growth. The shift toward value-based care models, which incentivize providers to reduce hospital readmissions and delay the progression to ESRD, is also a major driver for the adoption of digital nephrology platforms that can provide continuous, data-driven patient management.

Restraints: Data Privacy Concerns and Technical Integration Challenges

Market growth is restrained by concerns regarding data privacy and security, as digital kidney care platforms handle highly sensitive patient information. Compliance with stringent regulations such as HIPAA and GDPR is a significant operational burden for vendors. Additionally, the technical challenges of integrating digital health solutions with disparate legacy EHR and dialysis management systems can lead to implementation delays and data silos. The lack of standardized data protocols across different devices and platforms also complicates the achievement of a truly enterprise-wide view of renal care. Furthermore, the 'digital divide' among certain patient populations, particularly the elderly and those in rural areas, may limit the accessibility and effectiveness of home-based digital renal care solutions, acting as a deterrent to widespread adoption.

Opportunities: Scaling AI-Driven Digital Therapeutics and Home Dialysis Support

The development of AI-driven digital therapeutics and the expansion of home dialysis support offer substantial growth opportunities for the digital kidney care market. AI-powered platforms can analyze historical patient data to predict the risk of CKD progression and acute kidney injury (AKI), enabling early intervention and personalized care planning. By 2026, digital therapeutics are being integrated into standard nephrology care to provide patients with real-time support for dietary management and medication adherence. Furthermore, the global trend toward home dialysis is creating a high demand for remote monitoring and support solutions that can ensure the safety and efficacy of home-based treatments. This shift offers an opportunity for vendors to develop integrated platforms that coordinate care across the entire renal care continuum, from early-stage CKD to post-transplant management.

Evolution toward Holistic and AI-Powered Renal Care Orchestration

A defining trend in 2026 is the evolution of digital kidney care from siloed applications into holistic, AI-powered care orchestration hubs. These platforms aggregate data from various sources—including wearables, home dialysis machines, and clinical records—to provide a comprehensive view of the patient's health status. Advanced AI engines are increasingly capable of predicting complications and recommending personalized treatment adjustments, reducing the cognitive load on nephrologists and improving patient safety. This trend reflects a strategic shift toward proactive, enterprise-wide patient management, prioritizing early intervention and long-term health over reactive acute care.

Integration of Digital Therapeutics for Personalized CKD Management

The integration of digital therapeutics (DTx) into the standard nephrology workflow is gaining significant traction. These software-based interventions provide patients with personalized, evidence-based support for managing their condition, including AI-driven nutrition guidance and cognitive behavioral therapy for coping with chronic illness. In 2026, DTx solutions are increasingly being prescribed alongside traditional medications to improve adherence and slow disease progression. This trend is supported by clinical evidence demonstrating that patients who engage with digital kidney care platforms experience better blood pressure control and fewer hospitalizations, directly contributing to the goals of value-based care.

Analysis by Type

Based on type, the renal remote patient monitoring (RPM) segment is expected to hold the largest share in 2026. This dominance is driven by the critical role of RPM in managing high-risk CKD and ESRD patients in home settings, facilitating early detection of complications and reducing hospital readmissions. The digital therapeutics for kidney disease segment is projected to register the highest CAGR, as clinical evidence for the efficacy of these interventions grows and reimbursement pathways become more established. Telehealth and virtual consultation platforms remain a foundational segment, providing the essential infrastructure for remote nephrology care delivery.

Analysis by End User

Based on end user, the hospitals and dialysis centers segment is expected to account for the largest share in 2026. These facilities are increasingly adopting digital kidney care solutions to optimize their operations and meet the requirements of value-based care contracts. The patient/home care segment is projected to exhibit the highest CAGR, reflecting the global shift toward home-based renal care and the increasing empowerment of patients through digital health tools. Payers and insurance companies are also emerging as key end users, leveraging digital nephrology data to manage population health and reduce the total cost of renal care.

North America is expected to dominate the global digital kidney care market in 2026. The region's leadership is supported by a high prevalence of CKD, a mature digital health ecosystem, and favorable reimbursement for remote patient monitoring and telehealth. Significant investments in value-based care and the presence of leading market players, such as DaVita and Fresenius, continue to drive market growth in the U.S. and Canada. The Advancing American Kidney Health initiative also plays a pivotal role in promoting home-based care and digital health adoption.

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This growth is fueled by the rising burden of diabetes and hypertension, which are the leading causes of CKD, across China, India, and Southeast Asian nations. As these countries implement large-scale digital health initiatives and increase their focus on expanding access to specialized care, the demand for digital nephrology solutions is expected to rise significantly. The increasing adoption of cloud-based platforms and the modernization of public health agencies in the region are creating substantial opportunities for global and local digital kidney care vendors.

The competitive landscape of the global digital kidney care market is characterized by intense innovation and the formation of strategic partnerships between digital health vendors and large renal care providers. Leading players are focusing on the development of integrated platforms that provide end-to-end visibility into the patient journey, from early-stage CKD to ESRD management. Strategic moves, such as the acquisition of AI-driven predictive analytics companies and the expansion of home dialysis support services, are redefining vendor positioning in the 2026 landscape. The market is also seeing increased collaboration between digital kidney care vendors and payers to manage population health and demonstrate the ROI of digital interventions.

Key players operating in the global digital kidney care market include Fresenius Medical Care AG & Co. KGaA (Germany), DaVita Inc. (U.S.), Baxter International Inc. (U.S.), Strive Health (U.S.), Monogram Health (U.S.), Cricket Health (U.S.), Somatus (U.S.), Outset Medical, Inc. (U.S.), Renalytix plc (U.K.), Healthy.io (Israel), and various emerging technology providers specializing in AI-driven renal care and digital therapeutics.

The market is projected to reach USD 4.24 billion by 2036, growing at a CAGR of 10.4% from 2026 to 2036.

Providers report a significant reduction in hospital readmissions and an improvement in patient adherence to treatment plans.

The digital therapeutics for kidney disease segment is expected to grow the fastest as clinical evidence and reimbursement pathways expand.

RPM enables real-time tracking of vital signs and fluid balance, facilitating early intervention and preventing acute complications.

North America holds the largest share, estimated at 41.5% in 2026, driven by high CKD prevalence and favorable reimbursement.

AI enables the prediction of CKD progression and AKI risk, allowing for proactive care planning and personalized interventions.

The shortage is compelling health systems to adopt digital solutions to scale care delivery and improve early detection.

The patient/home care segment is the primary adopter, reflecting the global shift toward home dialysis and self-management.

These systems provide the continuous, data-driven patient management necessary to improve outcomes and reduce the total cost of care.

The top 5 players are Fresenius Medical Care, DaVita Inc., Baxter International, Strive Health, and Monogram Health.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Type

3.2.2. Market Analysis, by Component

3.2.3. Market Analysis, by Deployment Mode

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Addressing the Global CKD Burden with Digital Health and Remote Monitoring

4.2.1.2. Favorable Reimbursement Policies and Value-Based Care Incentives

4.2.1.3. Global Shortage of Nephrologists Compelling Scalable Digital Solutions

4.2.2. Restraints

4.2.2.1. Data Privacy Concerns and Stringent Regulatory Compliance

4.2.2.2. Technical Integration Challenges with Legacy Dialysis Systems

4.2.3. Opportunities

4.2.3.1. Scaling AI-Driven Digital Therapeutics and Home Dialysis Support

4.2.3.2. Expansion into Specialized Care Facilities and Outpatient Settings

4.2.3.3. Greenfield Smart Nephrology Projects in Emerging Markets

4.2.4. Challenges

4.2.4.1. Data Interoperability Across Fragmented Healthcare IT Systems

4.2.4.2. Addressing the Digital Divide in Elderly Patient Populations

4.2.4.3. Managing Alert Fatigue and Investigative Burden for Clinicians

4.2.5. Trends

4.2.5.1. Evolution toward Holistic and AI-Powered Renal Care Orchestration

4.2.5.2. Integration of Digital Therapeutics for Personalized CKD Management

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Digital Kidney Care Market, by Type

5.1. Overview

5.2. Renal Remote Patient Monitoring (RPM)

5.3. Digital Therapeutics for Kidney Disease

5.4. Telehealth and Virtual Consultation Platforms

5.5. Dialysis Management Software

6. Global Digital Kidney Care Market, by Component

6.1. Overview

6.2. Software

6.3. Services

6.4. Hardware

7. Global Digital Kidney Care Market, by Deployment Mode

7.1. Overview

7.2. Cloud-Based (SaaS) Deployment

7.3. On-Premises Deployment

8. Global Digital Kidney Care Market, by End User

8.1. Overview

8.2. Hospitals and Dialysis Centers

8.3. Patient/Home Care

8.4. Payers and Insurance Companies

8.5. Specialized Nephrology Clinics

9. Global Digital Kidney Care Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Australia

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. GCC Countries

9.6.2. South Africa

9.6.3. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share/Ranking Analysis

11. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

11.1. Fresenius Medical Care AG & Co. KGaA

11.2. DaVita Inc.

11.3. Baxter International Inc.

11.4. Strive Health

11.5. Monogram Health

11.6. Cricket Health

11.7. Somatus

11.8. Outset Medical, Inc.

11.9. Renalytix plc

11.10. Healthy.io

11.11. Medtronic plc

11.12. B. Braun Melsungen AG

11.13. Nipro Corporation

11.14. Terumo Corporation

11.15. Asahi Kasei Medical Co., Ltd.

11.16. CVS Health (Kidney Care)

11.17. Humana Inc. (Kindred at Home)

11.18. UnitedHealth Group (Optum)

11.19. Microsoft Corporation (Healthcare)

11.20. Salesforce, Inc. (Health Cloud)

12. Appendix

12.1. Available Customization

12.2. Related Reports

Published Date: Nov-2025

Published Date: Apr-2025

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Nov-2024

Subscribe to get the latest industry updates