Resources

About Us

CO₂-Derived Chemicals Market Size, Share & Trends Analysis by Product Type (Methanol, Formic Acid, Urea, Polycarbonates, Synthetic Fuels), Conversion Technology, End-Use Industry, Carbon Source, and Geography - Global Opportunity Analysis & Industry Forecast (2026–2036)

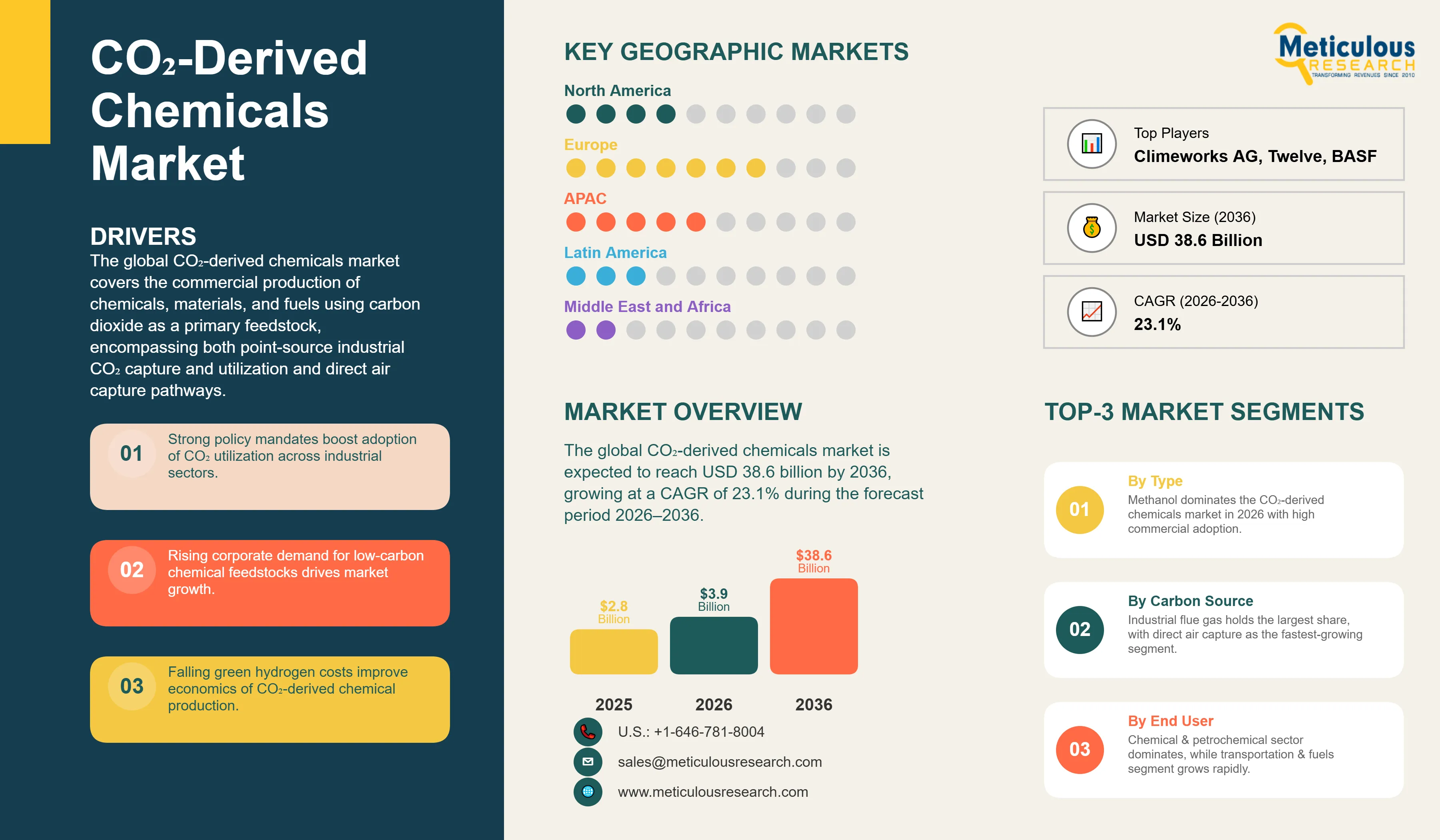

Report ID: MRCHM - 1041881 Pages: 288 Apr-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global CO₂-derived chemicals market was valued at USD 2.8 billion in 2025. This market is expected to reach USD 38.6 billion by 2036 from an estimated USD 3.9 billion in 2026, growing at a CAGR of 23.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global CO₂-derived chemicals market covers the commercial production of chemicals, materials, and fuels using carbon dioxide as a primary feedstock, encompassing both point-source industrial CO₂ capture and utilization and direct air capture pathways. The market spans the full spectrum of CO₂ conversion technologies, including catalytic hydrogenation, electrochemical reduction, biological fermentation, and mineralization, and the diverse portfolio of derivative products, including e-methanol, formic acid, urea and fertilizers, polycarbonates, synthetic aviation fuels, and construction aggregates, across the complete value chain from CO₂ capture and conditioning through synthesis, processing, and downstream end-use application.

The growth of the global CO₂-derived chemicals market is primarily driven by the accelerating policy imperative to decarbonize hard-to-abate industrial sectors, the escalating corporate demand for low-carbon chemical feedstocks and sustainable aviation fuel from major industrial offtakers, and the progressive cost reduction of green hydrogen as renewable electricity costs decline across major production regions. The European Union’s Carbon Border Adjustment Mechanism, the Inflation Reduction Act’s 45Q tax credit for carbon utilization in the United States, and the emerging carbon pricing frameworks in South Korea, Japan, and Canada are collectively creating the economic incentive structure required to commercialize CO₂ utilization at scale by improving the cost competitiveness of CO₂-derived products against their fossil-feedstock equivalents.

However, the market faces meaningful constraints. The production cost of CO₂-derived methanol, formic acid, and synthetic fuels remains substantially higher than fossil-derived equivalents in the absence of carbon pricing, creating a green premium that currently limits offtake to sustainability-committed industrial buyers and regulated applications such as sustainable aviation fuel blending mandates. The energy intensity of electrochemical CO₂ reduction processes and the efficiency losses inherent in CO₂ hydrogenation chemistry impose fundamental thermodynamic costs that must be offset by low-cost, low-carbon electricity and hydrogen to achieve commercially viable production economics.

Despite these challenges, the market outlook is strongly positive. The falling levelized cost of green hydrogen from renewable electrolysis, combined with the expanding commercial scale of direct air capture and the growing availability of concentrated industrial CO₂ streams from cement, steel, and fertilizer production, is progressively improving the production economics of the leading CO₂-derived chemicals. The strategic entry of major chemical companies including BASF, LanzaTech, Covestro, and Siemens Energy into CO₂ utilization technology platforms, combined with the landmark commercial projects being advanced by Carbon Recycling International, Haldor Topsøe, and Carbon Engineering, is driving rapid technology maturation and cost reduction across the CO₂ utilization value chain.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 38.6 Billion |

|

Market Size in 2026 |

USD 3.9 Billion |

|

Market Size in 2025 |

USD 2.8 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 23.1% |

|

Dominating Product Type |

Methanol |

|

Fastest Growing Product Type |

Synthetic Fuels (e-Fuels) |

|

Dominating Conversion Technology |

Catalytic Hydrogenation |

|

Fastest Growing Technology |

Electrochemical Reduction |

|

Dominating Carbon Source |

Industrial Flue Gas (Point-Source) |

|

Fastest Growing Carbon Source |

Direct Air Capture (DAC) |

|

Dominating End-Use Industry |

Chemical & Petrochemical |

|

Fastest Growing End-Use Industry |

Transportation & Fuels |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Commercialization of Green Methanol as the Lead CO₂-Derived Product

The emergence of e-methanol—produced by combining green hydrogen from renewable electrolysis with captured CO₂—as the commercially most advanced CO₂-derived chemical is the defining market development trend of the current period. Methanol’s established global commodity markets, its broad applicability as a chemical feedstock and fuel blendstock, and the technical maturity of methanol synthesis from CO₂ and hydrogen via reverse water-gas shift and methanol synthesis reactor technology are making e-methanol the primary commercial scale-up target for CO₂ utilization technology developers and project developers. Carbon Recycling International’s George Olah plant in Iceland, Haldor Topsøe’s eSMR Methanol technology, and the consortium projects advancing in the Netherlands, Germany, and South Korea represent an advancing commercial pipeline of green methanol production facilities targeting both chemical feedstock and maritime fuel applications.

The maritime shipping industry’s structural adoption of methanol as a primary alternative fuel pathway, driven by the International Maritime Organization’s 2050 net-zero shipping emissions ambition and the committed fleet of methanol-fueled vessels being deployed by Maersk, COSCO, and other major container shipping operators, is providing a large-volume offtake driver for green methanol that is accelerating project development timelines and enabling investment decisions at commercial scale. The landmark agreement between Maersk and European Energies for 730,000 tonnes per year of green methanol from wind-powered CO₂ hydrogenation capacity in Denmark represents a transaction scale that is redefining the commercial ambition of the CO₂-derived chemicals market.

Scaling of Electrochemical CO₂ Reduction for Formic Acid and Syngas

The progressive scale-up of electrochemical CO₂ reduction (eCO₂R) technology from laboratory and pilot scale toward industrial demonstration represents a strategically significant technology development trend that is expanding the addressable product portfolio of the CO₂ utilization market beyond the hydrogenation-dominated methanol pathway. Electrochemical reduction enables direct conversion of CO₂ to formic acid, carbon monoxide, ethylene, and multicarbon products using renewable electricity without requiring a separate green hydrogen production step, offering a potentially simpler production pathway with lower capital requirements for certain product applications. Twelve Benefit Corporation’s CO₂-to-syngas electrolyzer technology, Electrochaea’s biological methanation systems, and the eCO₂R platforms being developed by SUNFIRE, Haldor Topsøe, and Opus 12 are advancing the technology readiness level of electrochemical CO₂ conversion from TRL 4–6 toward the TRL 7–9 commercial demonstration stage.

Formic acid is emerging as a particularly attractive target product for electrochemical CO₂ reduction given the high selectivity achievable with tin and bismuth catalyst systems, the established industrial demand for formic acid in leather tanning, textile processing, and hydrogen storage applications, and the emerging market for formic acid as a liquid hydrogen carrier for fuel cell power systems. Several European electrochemical CO₂ reduction projects are advancing with formic acid as the primary target product, supported by EU Horizon funding and the strategic interest of major chemical companies in securing low-carbon formic acid supply.

Integration of CO₂ Utilization with Direct Air Capture Infrastructure

The increasing commercial deployment of direct air capture technology by companies including Climeworks, Carbon Engineering, and Global Thermostat is progressively expanding the CO₂ feedstock availability for CO₂-derived chemical production beyond the geographically constrained point-source industrial capture market, representing a fundamentally transformative development for the long-term growth trajectory of the CO₂-derived chemicals market. DAC-sourced CO₂ enables production of CO₂-derived chemicals with a net-negative or deeply negative carbon footprint that qualifies for the most demanding sustainability certification standards and commands the maximum green premium from sustainability-committed offtakers. The combination of Climeworks’ Orca and Mammoth DAC plants in Iceland with geothermal renewable electricity and green hydrogen infrastructure establishes the proof-of-concept for integrated DAC-to-chemicals production chains that are advancing toward commercial scale.

Expansion of Sustainable Aviation Fuel Programs via CO₂-to-e-Fuel Pathways

The emergence of power-to-liquid sustainable aviation fuel produced from green hydrogen and captured CO₂ via reverse water-gas shift synthesis and Fischer-Tropsch processing as a key pathway for meeting the escalating regulatory mandates for SAF blending in aviation represents one of the most commercially significant growth drivers for CO₂ utilization at scale. The European Union’s ReFuelEU Aviation regulation mandating 2% SAF blending by 2025 rising to 70% by 2050, the U.S. SAF Grand Challenge targeting 3 billion gallons per year of SAF by 2030, and the International Civil Aviation Organization’s global carbon offsetting and reduction scheme for international aviation are creating a mandated demand pull for SAF at volumes that cannot be met by biomass-based pathways alone, making CO₂-derived e-fuel an essential supply contribution. Norsk e-Fuel in Norway, Atmospheric Carbon Technologies, and the ARCADIA Efuels project in Germany are among the commercial-scale e-fuel projects advancing through development with announced offtake commitments from major European airlines.

Accelerating Policy Mandates for Carbon Utilization and Industrial Decarbonization

The primary structural driver of the global CO₂-derived chemicals market is the rapidly strengthening policy and regulatory environment across major economies that is creating binding demand for low-carbon chemicals, fuels, and materials and providing financial incentives for CO₂ capture and utilization technology deployment. The European Union’s Carbon Border Adjustment Mechanism, which entered its transitional phase in October 2023 and will impose full carbon costs on imports of cement, steel, aluminum, fertilizers, hydrogen, and electricity from 2026, is creating a powerful financial incentive for industrial operators in both European and non-European markets to reduce the embodied carbon content of their products through CO₂ utilization and other decarbonization measures. The U.S. Inflation Reduction Act’s Section 45Q tax credit provides USD 60 per tonne of CO₂ utilized in non-EOR applications, substantially improving the economics of commercial CO₂ utilization projects across the United States. Japan’s Green Innovation Fund, South Korea’s carbon neutrality roadmap, and the EU Innovation Fund are collectively mobilizing several billion euros of co-funding for CO₂ utilization technology demonstration and commercial deployment.

Growing Corporate Demand for Sustainable Chemical Feedstocks

The escalating corporate sustainability commitments and science-based emissions reduction targets adopted across major chemical, materials, and consumer goods companies are generating growing demand for low-carbon and CO₂-derived chemical feedstocks that is creating commercial offtake pull for CO₂ utilization projects at commercial scale. Major chemical companies including BASF, Covestro, and Borealis have announced product lines incorporating CO₂ as a feedstock, including Covestro’s cardyon polyol technology that uses CO₂ as a partial replacement for fossil-derived propylene oxide in polyurethane production. IKEA’s commitment to sourcing renewable and recycled materials, Unilever’s carbon footprint reduction targets for cleaning product surfactants, and the automotive industry’s demand for CO₂-derived polycarbonates and polymers for vehicle lightweighting are collectively expanding the addressable market for CO₂-derived chemicals across multiple downstream industrial verticals.

Establishment of CO₂ Utilization as a Carbon Credit-Generating Activity

The development of verifiable, high-quality carbon credit and carbon removal certificate methodologies for CO₂ utilization activities represents a significant near-term commercial opportunity that could substantially improve CO₂-derived chemicals project economics by providing an additional revenue stream on top of product sales. If CO₂-derived chemicals produced from DAC-sourced carbon and renewable energy are recognized as providing durable carbon removal equivalent to the tonne of CO₂ incorporated in long-lived products such as polycarbonates and construction materials, the carbon removal credit value at prevailing voluntary carbon market prices of USD 50 to 300 per tonne would significantly improve project returns. Several carbon accounting standards bodies including Verra and Gold Standard are developing CO₂ utilization methodologies, and the Science Based Targets initiative’s carbon removal guidance is progressively creating the corporate demand framework for high-quality CO₂ utilization credits.

Integration with Green Hydrogen Export Hubs

The strategic co-location of CO₂-derived chemicals production with the large-scale green hydrogen export hubs being developed in Australia, Chile, Namibia, Saudi Arabia, and Morocco creates a high-value opportunity to convert stranded or surplus renewable electricity and green hydrogen into energy-dense chemical commodities that can be economically shipped to demand centers in Europe, Japan, and South Korea. Unlike direct green hydrogen export, which requires expensive liquefaction or ammonia conversion infrastructure, e-methanol and other liquid CO₂-derived chemicals can be transported in conventional chemical tanker infrastructure, providing a cost-competitive export pathway that is attracting strategic investment from integrated energy companies and national development entities in potential export nations.

By Product Type: In 2026, Methanol to Dominate

Based on product type, the global CO₂-derived chemicals market is segmented into methanol, formic acid, urea and fertilizers, polycarbonates and polymers, synthetic fuels (e-fuels), and other CO₂-derived chemicals. In 2026, the methanol segment is expected to account for the largest share of the global CO₂-derived chemicals market. The large share of this segment is attributed to methanol’s status as the most technically mature and commercially advanced CO₂-derived chemical, the established global methanol market providing clear offtake pathways for green methanol production, the accelerating demand from the maritime shipping sector for methanol as a low-carbon marine fuel, and the multiple commercial and near-commercial e-methanol production projects operating or under construction in Iceland, Denmark, Germany, and South Korea that are establishing production reference points and commercial pricing benchmarks for the broader market.

However, the synthetic fuels (e-fuels) segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the binding SAF blending mandates being implemented across European Union member states and the anticipated expansion of global SAF regulations, the aviation industry’s structural inability to fully decarbonize through electrification or hydrogen fuel cells on medium and long-haul routes, and the committed investment programs by oil majors, aerospace companies, and independent e-fuel developers in power-to-liquid production infrastructure that is advancing commercial-scale synthesis capacity toward the end of the forecast period.

By Conversion Technology: In 2026, Catalytic Hydrogenation to Hold the Largest Share

Based on conversion technology, the global CO₂-derived chemicals market is segmented into catalytic hydrogenation, electrochemical reduction, biological/fermentation, mineralization and carbonation, and thermochemical conversion. In 2026, the catalytic hydrogenation segment is expected to account for the largest share of the global CO₂-derived chemicals market. This dominance reflects the technological maturity and commercial validation of CO₂ hydrogenation chemistry for methanol, formic acid, and synthetic fuel production, the substantial installed base of pilot and commercial catalytic hydrogenation reactors already generating revenue from CO₂-derived methanol sales, and the strong pipeline of commercial catalytic hydrogenation projects in advanced development across Europe, the Middle East, and Asia-Pacific.

However, the electrochemical reduction segment is projected to register the highest CAGR during the forecast period. This growth is driven by the potential of electrochemical reduction to produce a broader range of CO₂-derived chemicals with higher atom economy than hydrogenation pathways, the falling cost of renewable electricity that underpins electrochemical process economics, and the significant venture capital and corporate R&D investment in eCO₂R technology platforms that is accelerating technology readiness level advancement and reducing capital costs for electrolyzer stack manufacturing.

By Carbon Source: In 2026, Industrial Flue Gas to Hold the Largest Share

Based on carbon source, the global CO₂-derived chemicals market is segmented into industrial flue gas (point-source capture), direct air capture, and biogenic CO₂. In 2026, the industrial flue gas segment is expected to account for the largest share of the global CO₂-derived chemicals market. This dominance reflects the substantially lower cost of CO₂ capture from concentrated industrial point sources such as cement kilns, steel blast furnaces, and ammonia plants—where CO₂ capture costs range from USD 15 to 50 per tonne—relative to direct air capture costs of USD 200 to 600 per tonne that remain prohibitive for most commercial CO₂-derived chemicals applications at current scale. The geographic concentration of large industrial CO₂ emitters in regions with developing CO₂ utilization industries, including the Rhine-Ruhr industrial corridor, the Benelux chemical cluster, and the South Korean and Japanese industrial coastal zones, provides accessible CO₂ feedstock supply for the current generation of commercial CO₂-derived chemicals projects.

However, the direct air capture segment is projected to register the highest CAGR during the forecast period. This growth is driven by the accelerating commercial scale-up of DAC technology by Climeworks, Carbon Engineering, and emerging DAC developers, the strategic imperative to produce CO₂-derived chemicals with a net-negative carbon footprint for the most demanding sustainability certification standards, and the projected rapid reduction in DAC costs from current levels toward USD 100 to 150 per tonne by 2030 as technology matures and deployment scales.

CO₂-Derived Chemicals Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global CO₂-derived chemicals market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global CO₂-derived chemicals market. The largest share of this region is mainly due to Europe’s first-mover advantage in CO₂ utilization policy, technology development, and commercial deployment, anchored by the European Union’s comprehensive regulatory framework for carbon capture and utilization, the Carbon Border Adjustment Mechanism providing ongoing financial incentive for industrial decarbonization, and the strong pipeline of commercial CO₂ utilization projects in Germany, the Netherlands, Denmark, Norway, and Iceland. The European Commission’s Innovation Fund, which has committed over EUR 3.4 billion to large-scale innovative low-carbon technology projects across multiple rounds, has specifically supported CO₂ utilization projects including e-methanol synthesis, CO₂-to-chemicals electrochemical platforms, and power-to-liquid e-fuel production facilities. Germany’s Carbon Management Strategy, the Netherlands’ SDE++ subsidy program for CO₂ utilization, and the Nordic nations’ green hydrogen and e-fuel strategies collectively constitute the world’s most developed commercial CO₂-derived chemicals policy ecosystem.

However, the Asia-Pacific CO₂-derived chemicals market is expected to grow at the fastest CAGR during the forecast period. The region’s rapid growth is driven by Japan’s ambitious Green Innovation Fund commitment of JPY 2 trillion (approximately USD 15 billion) for hydrogen and carbon recycling technology scale-up, including commercial CO₂-derived methanol and synthetic fuels programs; South Korea’s Carbon Neutrality and Green Growth Strategy that establishes specific targets for CO₂ utilization technology deployment in the Korean petrochemical and steel industries; China’s national CO₂ capture, utilization, and storage roadmap that is advancing commercial CO₂-to-methanol projects at coal chemical and cement industrial clusters; and Australia’s strategic positioning as a low-cost green hydrogen production hub with CO₂ utilization as a value-added export pathway. The strong domestic chemical and refining industry presence in Japan, South Korea, and China provides both the CO₂ point-source feedstock and the downstream chemical offtake infrastructure required to support large-scale CO₂-derived chemicals manufacturing.

North America is establishing a growing CO₂-derived chemicals commercial pipeline, primarily concentrated in the United States where the Inflation Reduction Act’s 45Q tax credit for carbon utilization has materially improved project economics and stimulated significant developer interest. LanzaTech’s commercial ethanol and chemical production from industrial waste gas CO and CO₂ streams using proprietary gas fermentation technology represents the most commercially mature U.S. CO₂ utilization platform, with multiple operational plants supplying sustainable aviation fuel blendstock and chemical feedstocks to industrial offtakers. The U.S. Department of Energy’s Carbon Utilization Program and the Regional Direct Air Capture Hubs initiative are funding technology demonstration and scale-up projects across multiple CO₂ utilization pathways that are building the commercial reference base for the next generation of investment decisions.

The global CO₂-derived chemicals market is characterized by a diverse and rapidly evolving competitive ecosystem encompassing specialty chemical companies with proprietary CO₂ utilization technology platforms, industrial gas and engineering companies providing CO₂ capture and conversion process technology, independent green chemistry startup companies advancing novel electrochemical and biological CO₂ conversion approaches, and major integrated energy and chemical companies entering CO₂ utilization as a strategic component of their industrial decarbonization and green product portfolios. Competition is currently focused on technology cost reduction, process efficiency improvement, product certification for sustainability standards, and securing long-term offtake agreements with sustainability-committed industrial buyers rather than on commodity volume or market share in mature product categories.

Carbon Recycling International leads the market in CO₂-to-methanol technology commercialization with its operational George Olah renewable methanol plant in Iceland and multiple licensed projects in development globally. Haldor Topsøe advances eSMR Methanol and SOEC electrolysis-integrated methanol synthesis technology targeting commercial scale deployment in Europe and Asia. LanzaTech has commercialized gas fermentation technology for converting industrial CO and CO₂ waste streams to ethanol and chemical intermediates across multiple operational plants worldwide. Covestro has commercialized its cardyon technology for CO₂-based polyol production at commercial scale in Leverkusen, Germany. Siemens Energy advances CO₂ electrolysis and power-to-X system integration technology. BASF, Clariant, and Johnson Matthey provide heterogeneous catalyst systems for CO₂ hydrogenation reactions underpinning multiple technology platforms.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players’ technology platforms, product portfolios, geographic presence, and key strategic developments. Some of the key players operating in the global CO₂-derived chemicals market include Carbon Recycling International (Iceland), Haldor Topsøe A/S (Denmark), LanzaTech (U.S.), Covestro AG (Germany), Siemens Energy AG (Germany), BASF SE (Germany), Evonik Industries AG (Germany), Air Liquide S.A. (France), Linde plc (Ireland/U.S.), Johnson Matthey (U.K.), Climeworks AG (Switzerland), Carbon Engineering Ltd. (Canada), Twelve Benefit Corporation (U.S.), Electrochaea GmbH (Germany), Sunfire GmbH (Germany), Opus 12 Inc. (U.S.), CarbonCure Technologies (Canada), Verdox Inc. (U.S.), among others.

The global CO?-derived chemicals market is expected to reach USD 38.6 billion by 2036 from an estimated USD 3.9 billion in 2026, at a CAGR of 23.1% during the forecast period 2026–2036.

In 2026, the methanol segment is expected to hold the largest share of the global CO?-derived chemicals market, driven by methanol’s technical maturity as a CO?-derived product, the established global commodity market providing clear offtake pathways, and the accelerating demand from the maritime shipping sector for methanol as a low-carbon marine fuel.

The synthetic fuels (e-fuels) segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by binding SAF blending mandates across European Union member states, aviation’s structural inability to decarbonize long-haul routes through alternative electrification pathways, and committed commercial investment programs in power-to-liquid production infrastructure.

In 2026, the catalytic hydrogenation segment is expected to hold the largest share of the global CO?-derived chemicals market, reflecting the technological maturity and commercial validation of CO? hydrogenation chemistry and the substantial installed base of pilot and commercial hydrogenation reactors already generating revenue from CO?-derived product sales.

The growth of this market is primarily driven by accelerating policy mandates for carbon utilization including the EU Carbon Border Adjustment Mechanism and the U.S. IRA Section 45Q tax credit, the growing corporate demand for low-carbon chemical feedstocks and sustainable aviation fuel from sustainability-committed industrial offtakers, and the progressive reduction in green hydrogen production costs from renewable electrolysis that is improving the economics of CO? hydrogenation pathways.

Key players are Carbon Recycling International (Iceland), Haldor Topsøe A/S (Denmark), LanzaTech (U.S.), Covestro AG (Germany), Siemens Energy AG (Germany), BASF SE (Germany), Evonik Industries AG (Germany), Air Liquide S.A. (France), Linde plc (Ireland/U.S.), Johnson Matthey (U.K.), Climeworks AG (Switzerland), Carbon Engineering Ltd. (Canada), Twelve Benefit Corporation (U.S.), Electrochaea GmbH (Germany), and Sunfire GmbH (Germany), among others.

Asia-Pacific is expected to register the highest growth rate in the global CO?-derived chemicals market during the forecast period 2026–2036, driven by Japan’s substantial Green Innovation Fund commitments for carbon recycling technology, South Korea’s Carbon Neutrality Strategy targeting CO? utilization in petrochemical and steel industries, China’s CO?-to-methanol commercial programs at industrial clusters, and Australia’s strategic development as a green hydrogen production hub with CO?-derived chemicals as a value-added export pathway.

The transportation and fuels end-use industry is expected to register the highest CAGR during the forecast period, driven by the structural demand for sustainable aviation fuel from aviation decarbonization mandates, the maritime shipping industry’s large-scale adoption of methanol as a low-carbon marine fuel, and the growing regulatory pressure across road transport for low-carbon synthetic fuel blendstocks as part of broader powertrain decarbonization strategies.

Published Date: Apr-2026

Published Date: May-2022

Published Date: Feb-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates