Resources

About Us

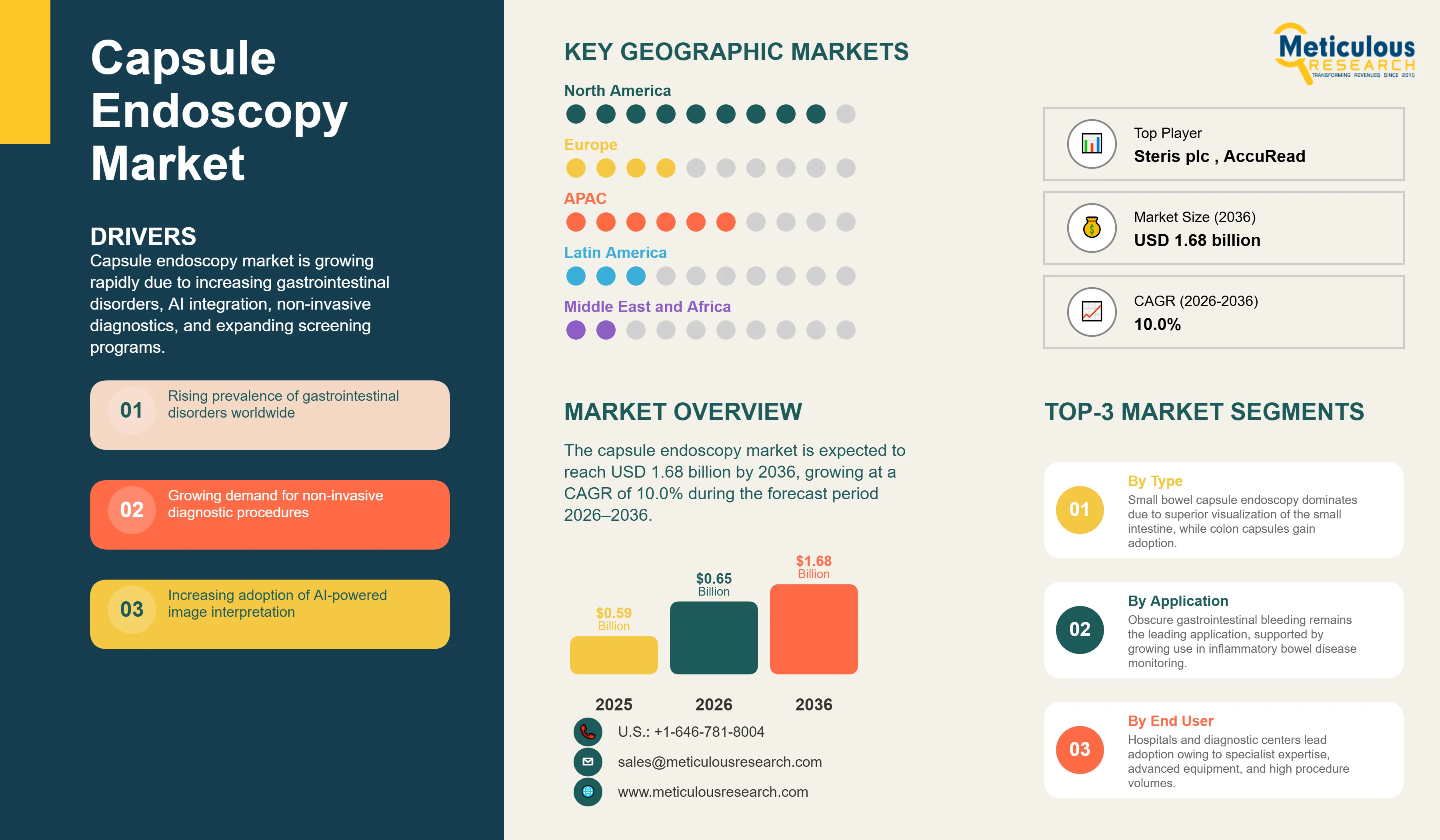

The global capsule endoscopy market is estimated to be USD 0.65 billion in 2026. This market is expected to reach USD 1.68 billion by 2036, growing at a CAGR of 10.0% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global capsule endoscopy market represents a transformative segment of the gastrointestinal diagnostic industry, providing a patient-friendly, non-invasive alternative to traditional endoscopy for visualizing the entire digestive tract. Capsule endoscopy involves the use of a swallowable, pill-sized camera that captures high-resolution images as it travels naturally through the gastrointestinal system, offering unparalleled access to the small bowel—an area traditionally difficult to reach. This market is primarily driven by the rising global incidence of gastrointestinal diseases such as Crohn's disease and colorectal cancer, the increasing patient preference for non-invasive procedures, and the rapid integration of artificial intelligence (AI) to streamline image analysis. According to clinical guidelines from the World Endoscopy Organization (WEO) and the American Society for Gastrointestinal Endoscopy (ASGE), capsule endoscopy is an essential diagnostic tool for obscure gastrointestinal bleeding and inflammatory bowel disease monitoring. As the technology evolves toward magnetically controlled navigation and enhanced battery life, the market is expected to witness significant expansion, supported by the shift toward decentralized, outpatient diagnostic care.

The growth of the global capsule endoscopy market is primarily driven by the increasing clinical shift toward patient-centric, non-invasive diagnostics and the technological breakthrough of AI-driven workflow automation.

Increasing Patient Preference for Non-Invasive and Sedation-Free Diagnostic Procedures

A major driver for the capsule endoscopy market is the significant patient preference for non-invasive diagnostic solutions that do not require sedation or invasive tube insertion. According to the World Health Organization, colorectal cancer accounted for approximately 1.9 million new cases globally in 2022, making it the third most commonly diagnosed cancer worldwide and underscoring the need for improved patient participation in gastrointestinal screening programs. Furthermore, the Crohn's & Colitis Foundation estimates that more than 10 million people worldwide are living with inflammatory bowel disease (IBD), many of whom require repeated gastrointestinal evaluation throughout their lifetime. Capsule endoscopy offers a comfortable, swallow-and-go alternative that enables patients to continue their daily activities while capturing high-quality diagnostic images of the gastrointestinal tract. The absence of sedation, reduced procedural discomfort, and minimal recovery time contribute to higher patient acceptance, particularly for small bowel evaluation, colorectal cancer screening, and long-term monitoring of Crohn's disease, thereby supporting sustained market growth.

Integration of Artificial Intelligence and Machine Learning in Image Interpretation

The integration of artificial intelligence (AI) and machine learning (ML) is revolutionizing the capsule endoscopy market by addressing the primary challenge of long reading times. A single capsule procedure can generate over 50,000 images, making manual review a time-consuming task for gastroenterologists. AI-assisted reading platforms can now automatically identify and prioritize suspicious lesions, bleeding sources, and mucosal abnormalities, significantly reducing the time required for diagnosis while improving accuracy. This technological evolution is enhancing the clinical efficiency of capsule endoscopy, making it more scalable and attractive for healthcare providers, thereby driving market adoption.

Despite its diagnostic advantages, the capsule endoscopy market faces challenges related to the clinical risk of device retention and the inconsistencies in insurance coverage across different regions.

Clinical Concerns Regarding Capsule Retention and Technical Diagnostic Limitations

A significant restraint for the market is the risk of capsule retention, particularly in patients with known or suspected intestinal strictures, adhesions, or severe inflammatory bowel disease. While rare, a retained capsule may require surgical or endoscopic intervention for removal, leading to clinical caution in certain patient populations. Furthermore, unlike traditional endoscopy, standard capsule endoscopy is purely diagnostic and does not allow for immediate therapeutic intervention, such as biopsy or hemostasis. This limitation necessitates follow-up procedures if an abnormality is found, which can impact the overall cost-effectiveness and adoption rate of the technology in certain clinical scenarios.

Inconsistent Reimbursement Policies and High Cost of Advanced Systems

The global capsule endoscopy market is impacted by variable reimbursement landscapes. While well-covered for small bowel indications in North America and parts of Europe, reimbursement for colon and esophageal capsule endoscopy remains inconsistent in many regions. The high initial cost of workstations and the recurring cost of single-use capsules can be a barrier for smaller clinics and healthcare systems in developing countries. Without robust and widespread insurance coverage, the high out-of-pocket costs for patients can significantly limit the volume of procedures and the overall growth potential of the market in price-sensitive regions.

Future growth opportunities in the capsule endoscopy market are centered on the development of actively controlled capsules and the expansion of non-invasive colorectal cancer screening programs.

Development and Commercialization of Magnetically Controlled Capsule Endoscopy (MCCE)

The development of magnetically controlled capsule endoscopy (MCCE) represents a major opportunity for market expansion. Unlike traditional passive capsules that rely on natural peristalsis, MCCE allows clinicians to actively navigate the capsule within the stomach and other areas using external magnetic fields. This capability enables a more comprehensive and targeted examination, potentially allowing capsule endoscopy to compete directly with traditional upper gastrointestinal endoscopy for gastric cancer screening. Manufacturers that can successfully commercialize reliable and intuitive MCCE systems are likely to tap into a massive new diagnostic segment.

Expansion of Non-Invasive Colorectal Cancer Screening Programs

There is a significant opportunity for growth in the use of capsule endoscopy for colorectal cancer (CRC) screening. As healthcare systems strive to increase CRC screening compliance, colon capsule endoscopy offers a compelling, non-invasive alternative for patients who are unwilling or unable to undergo traditional colonoscopy. With the increasing clinical validation of colon capsules and the potential for inclusion in national screening guidelines, the volume of procedures is expected to surge. This expansion is particularly relevant in aging populations where the risk of CRC is high but the tolerance for invasive procedures may be lower.

Emergence of Home-Based and Decentralized Capsule Endoscopy Models

A prominent trend in 2026 is the shift toward home-based and decentralized capsule endoscopy. This model allows patients to swallow the capsule at home and transmit data wirelessly to a healthcare provider, eliminating the need for hospital visits and reducing the burden on clinical facilities. This trend, accelerated by the lessons learned from the COVID-19 pandemic and the growth of telehealth, is making gastrointestinal diagnostics more accessible and convenient, particularly for patients in remote areas or those with limited mobility.

Widespread Adoption of AI-Powered Triage and Lesion Detection Software

The widespread adoption of AI-powered software for automated triage and lesion detection is a significant trend shaping the market. These platforms are no longer just research tools but are being integrated into standard clinical workflows. By automatically flagging high-priority images, AI software allows gastroenterologists to focus their attention on the most clinically relevant data, improving diagnostic yield and significantly reducing the time-to-report. This trend is fostering a more data-driven and efficient approach to gastrointestinal diagnostics, reflecting a broader shift toward digital health in gastroenterology.

Analysis by Product Type

Based on product type, the small bowel capsule endoscopy segment is expected to hold the largest share of the global capsule endoscopy market in 2026. This dominant position is substantiated by its status as the clinical gold standard for non-invasive visualization of the small intestine, an area that is largely inaccessible to traditional endoscopy. Its established role in diagnosing obscure GI bleeding and Crohn's disease, backed by robust reimbursement, ensures its market leadership. However, the colon capsule endoscopy segment is projected to register the highest CAGR during the forecast period. The increasing clinical validation of colon capsules for colorectal cancer screening and the rising patient demand for non-invasive alternatives to traditional colonoscopy are driving this segment's rapid growth.

Analysis by Application

By application, the obscure gastrointestinal bleeding (OGIB) segment is expected to hold the largest share in 2026. This leadership is driven by the unique ability of capsule endoscopy to provide high-resolution imaging of the entire small bowel, making it the most effective tool for identifying the source of unexplained bleeding. However, the inflammatory bowel disease (IBD) segment is projected to grow at the fastest CAGR during the forecast period. The rising global prevalence of Crohn's disease and the increasing use of capsule endoscopy for non-invasive monitoring of mucosal healing and disease extent are accelerating growth in this application area.

Analysis by End User

By end user, the hospitals & diagnostic centers segment is expected to hold the largest share in 2026. These facilities are the primary setting for capsule endoscopy due to the requirement for specialized recording equipment and expert interpretation by gastroenterologists. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing trend toward moving diagnostic procedures to outpatient settings to improve efficiency and reduce costs is driving the rapid adoption of capsule endoscopy in ASCs, which can handle high patient volumes with lower overhead costs.

Largest Share: North America

North America is expected to dominate the global capsule endoscopy market in 2026. This leading position is attributed to the high prevalence of gastrointestinal disorders, well-established reimbursement models, and the early adoption of AI-assisted diagnostic platforms. The region benefits from a highly developed healthcare infrastructure and a strong presence of leading players like Medtronic and CapsoVision. Key companies operating in the North America market are Medtronic plc, CapsoVision, Inc., and Olympus Corporation.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global capsule endoscopy market, with a CAGR of 11.8% during the forecast period. This rapid expansion is driven by the large patient population, increasing healthcare expenditure, and the rapid modernization of diagnostic facilities in countries like China, Japan, and India. The region is also a hub for innovation in magnetically controlled capsule technology. Key companies operating in the Asia Pacific market are Olympus Corporation, Ankon Medical Technologies, IntroMedic Co., Ltd., and Fujifilm Holdings Corporation.

The global capsule endoscopy market is characterized by a mix of major global medical technology corporations and specialized innovative players focusing on imaging and AI. Competition is primarily focused on improving image resolution, battery life, and field of view, while simultaneously developing AI-powered software to automate image analysis. Key players are investing in magnetically controlled navigation systems that allow for active examination of the stomach and other organs. There is also a significant emphasis on developing specialized capsules for the colon and esophagus to expand the diagnostic reach of the technology. Strategic developments often involve partnerships between hardware manufacturers and AI software developers to provide comprehensive, end-to-end diagnostic solutions. Furthermore, manufacturers are increasingly focusing on clinical validation studies to support the inclusion of capsule endoscopy in national screening programs and to secure favorable reimbursement, which is critical for maintaining market leadership in an increasingly patient-centric diagnostic field.

Medtronic plc, Olympus Corporation, IntroMedic Co., Ltd., Ankon Medical Technologies, CapsoVision, Inc., Fujifilm Holdings Corporation, Jinshan Science and Technology, RF System lab, Check-Cap Ltd., PillCam (Medtronic), Given Imaging (Medtronic), Shangxian Medical, ZRE (Shenzhen Zhaori), AccuRead, AnX Robotics, Chongqing Jinshan Science & Technology, Shenzhen Jifu Medical Technology, IntroMedic (MiroCam), CapsoCam (CapsoVision), Medtronic (PillCam COLON) (US)

The global market is estimated at USD 0.65 billion in 2026, with a projected growth to USD 1.68 billion by 2036, at a CAGR of 10.0%.

Primary drivers include the rising demand for non-invasive diagnostics and the integration of AI-assisted reading platforms.

Major restraints include the risk of capsule retention and inconsistent global reimbursement policies.

Opportunities lie in the development of magnetically controlled capsules and the expansion of non-invasive colorectal screening.

Small bowel capsule endoscopy is expected to hold the largest share as the clinical gold standard for non-invasive small intestine visualization.

Inflammatory bowel disease (IBD) is projected to grow at the fastest CAGR, driven by the need for non-invasive mucosal monitoring.

Hospitals & diagnostic centers are expected to hold the largest share as the primary setting for specialized capsule procedures.

North America is expected to dominate the market due to high disease prevalence and established reimbursement models.

Asia Pacific is projected to witness the fastest growth, fueled by rapid diagnostic modernization and technological innovation.

Key trends include the emergence of home-based diagnostic models and the widespread adoption of AI-powered triage software.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Patient Preference for Non-Invasive and Sedation-Free Diagnostic Procedures

4.2.1.2. Integration of Artificial Intelligence and Machine Learning in Image Interpretation

4.2.2. Restraints

4.2.2.1. Clinical Concerns Regarding Capsule Retention and Technical Diagnostic Limitations

4.2.2.2. Inconsistent Reimbursement Policies and High Cost of Advanced Systems

4.2.3. Opportunities

4.2.3.1. Development and Commercialization of Magnetically Controlled Capsule Endoscopy (MCCE)

4.2.3.2. Expansion of Non-Invasive Colorectal Cancer Screening Programs

4.2.4. Trends

4.2.4.1. Emergence of Home-Based and Decentralized Capsule Endoscopy Models

4.2.4.2. Widespread Adoption of AI-Powered Triage and Lesion Detection Software

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Capsule Endoscopy Market, by Product Type

5.1. Small Bowel Capsule Endoscopy Systems

5.1.1. Capsule Endoscopes

5.1.2. Data Recorders & Sensor Arrays

5.1.3. Workstations & Software

5.2. Colon Capsule Endoscopy Systems

5.2.1. Capsule Endoscopes

5.2.2. Data Recorders & Sensor Arrays

5.2.3. Workstations & Software

5.3. Esophageal Capsule Endoscopy Systems

5.3.1. Capsule Endoscopes

5.3.2. Data Recorders & Sensor Arrays

5.3.3. Workstations & Software

6. Global Capsule Endoscopy Market, by Application

6.1. Obscure Gastrointestinal Bleeding (OGIB)

6.2. Inflammatory Bowel Disease (IBD)

6.3. Small Bowel Tumors

6.4. Celiac Disease

6.5. Polyposis Syndromes

6.6. Esophageal Disorders

6.7. Others

7. Global Capsule Endoscopy Market, by End User

7.1. Hospitals & Diagnostic Centers

7.2. Ambulatory Surgical Centers (ASCs)

7.3. Others

8. Global Capsule Endoscopy Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Share/Ranking Analysis, By Key Player (2025)

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Medtronic plc

10.2. Olympus Corporation

10.3. IntroMedic Co., Ltd.

10.4. Ankon Medical Technologies

10.5. CapsoVision, Inc.

10.6. Fujifilm Holdings Corporation

10.7. Jinshan Science and Technology

10.8. RF System lab

10.9. Check-Cap Ltd.

10.10. AnX Robotics

10.11. Chongqing Jinshan Science & Technology

10.12. Shenzhen Jifu Medical Technology

10.13. Shangxian Medical

10.14. ZRE (Shenzhen Zhaori)

10.15. AccuRead

10.16. B. Braun Melsungen AG

10.17. PENTAX Medical (Hoya Corporation)

10.18. Steris plc

10.19. Cook Medical

10.20. Boston Scientific Corporation

11. Appendix

11.1. Abbreviations

11.2. Disclaimer

12. Key Questions Answered

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Nov-2022

Published Date: Sep-2022

Subscribe to get the latest industry updates