Resources

About Us

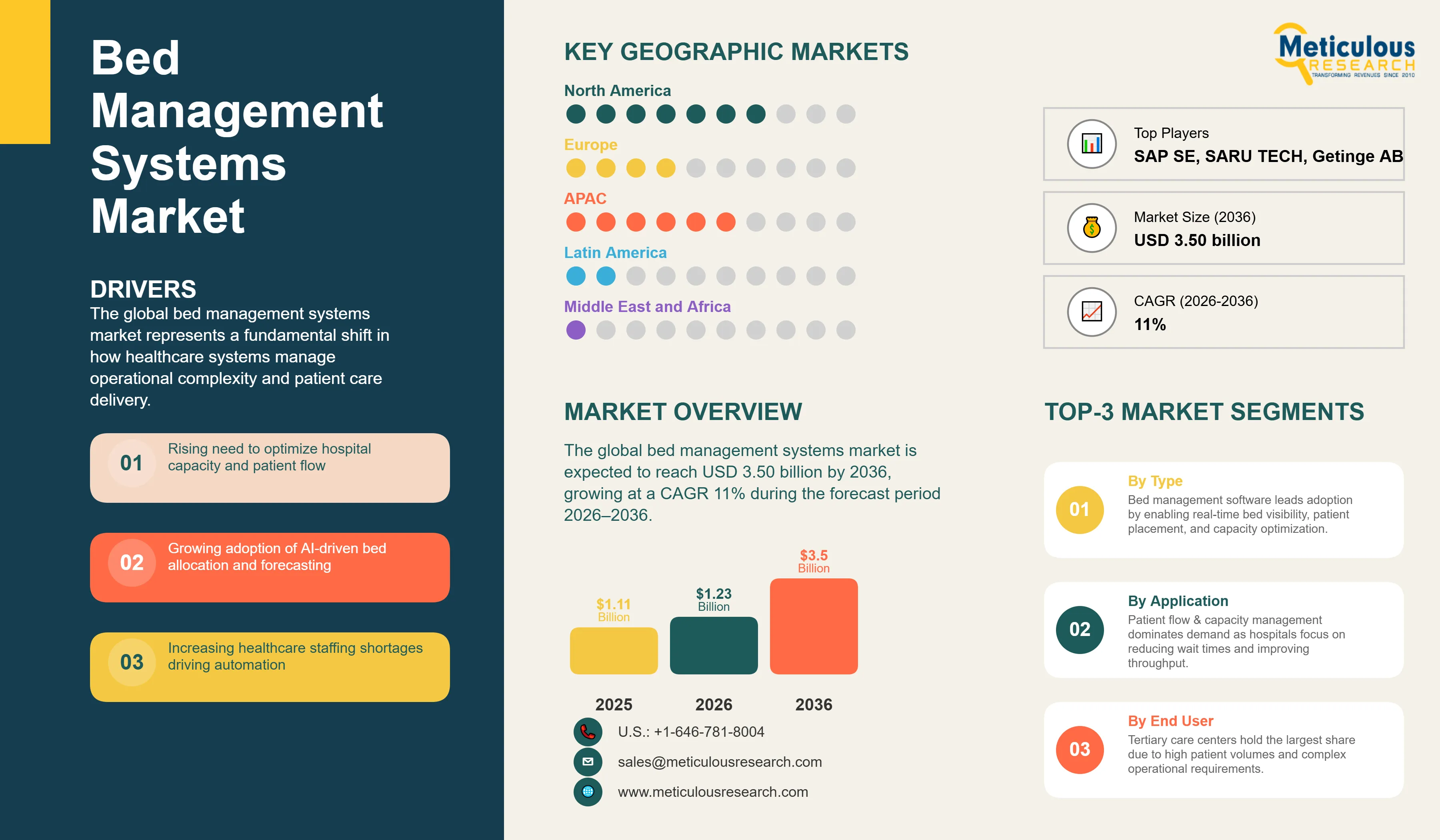

The global bed management systems market is estimated at USD 1.23 billion in 2026. This market is expected to reach USD 3.50 billion by 2036, growing at a CAGR 11% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global bed management systems market represents a fundamental shift in how healthcare systems manage operational complexity and patient care delivery. These systems serve as the 'operational brain' of a healthcare system, integrating real-time data from electronic health records (EHRs), real-time location systems (RTLS), and admission, discharge, and transfer (ADT) systems to provide a unified view of patient flow, resource allocation, and clinical risk. According to the American Hospital Association (AHA) 2026 Costs of Caring report, hospitals are facing unprecedented pressure from rising patient complexity, with the case-mix index rising by approximately 5% between 2019 and 2024. This increasing acuity necessitates the move beyond reactive reporting toward proactive, AI-driven care orchestration enabled by bed management systems.

As of 2026, the demand for hospital bed management systems is being propelled by the global rise in chronic disease prevalence and an aging population. According to the World Health Organization (WHO), by 2030, one in six people worldwide will be aged 60 years or over, placing immense strain on existing healthcare infrastructure. In the U.S., the AHA reported that total staffed beds reached 907,216 in 2026, highlighting the scale of resource management required. Bed management software facilitates capacity optimization and patient placement functionalities, allowing administrators to reduce emergency department (ED) boarding times and improve overall hospital throughput management. The integration of these systems with clinical telemetry and operational dashboards ensures that stakeholders have immediate access to actionable insights, thereby enhancing patient safety and clinical outcomes.

Drivers: Addressing the Global Healthcare Capacity Crisis

The growth of the overall market is primarily driven by the critical need for throughput optimization and the rising adoption of predictive analytics to manage chronic emergency department (ED) boarding. Industry data indicates that hospitals are caring for sicker patients, with inpatient volumes increasing by 5.3% in 2025 while total expenses grew by 7.5% (Source: AHA/Strata Decision Technology). Furthermore, the global shortage of 10 million health workers projected by the WHO for 2030 is compelling health systems to adopt AI-driven staffing and resource models. Bed management systems have demonstrated the ability to reduce ambulance dispatch times by 43 minutes and cut bed allocation delays by 3.5 hours for emergency department patients (Source: NHS/BMJ Informatics). Effective bed management software helps reduce the length of stay (LOS) and improve patient placement, thereby enhancing hospital throughput management and alleviating capacity pressures.

Restraints: Capital Expenditure and Change Management Barriers

Despite the clear operational benefits, market growth is restrained by high capital expenditure and the significant organizational change management required for implementation. Enterprise-wide bed management projects typically range from USD 1.5 million to USD 4 million, representing a substantial investment for systems already operating on thin margins. Additionally, the NHS Digital Hospital Episode Statistics (HES) and recent studies in the UK highlight that data quality remains a persistent challenge, with missing clinician assessment dates reaching 23.4% in some systems, which can compromise the effectiveness of predictive analytics (Source: PMC/NHS). The complexity of mapping data elements between different software versions can lead to implementation delays, which acts as a deterrent for resource-constrained mid-sized and community hospitals.

Opportunities: Scaling Virtual Care and Digital Twin Simulation

Emerging opportunities in 'hospital-at-home' models and 'Digital Twin' technology are creating new growth avenues. By 2026, digital twin simulations are enabling health systems to forecast bed-request spikes with 95% accuracy, leading to an 18% reduction in ambulance diversions. The expansion of virtual care hubs allows bed management systems to monitor low-acuity patients remotely, preserving acute care beds for the most critically ill. This trend is particularly strong in North America, where hospitals are investing heavily in telehealth and remote monitoring integration to extend the reach of the operational hubs. Vendors like LeanTaaS and Qventus have demonstrated that AI-driven patient flow optimization solutions can reduce the average length of stay by up to 1.1 days, representing a massive cost-saving opportunity for healthcare providers.

Transition to Autonomous and Self-Healing Operational Logistics

A defining trend in 2026 is the evolution of bed management systems from decision-support tools into autonomous orchestration hubs. Advanced platforms are increasingly capable of 'self-healing' operational logistics, where AI engines automatically trigger housekeeping requests or adjust discharge planning tasks based on predicted inpatient census. This automation reduces the cognitive load on staff, allowing them to focus on high-acuity clinical triage. The integration of generative AI is further accelerating this trend by automating the generation of clinical summaries, ensuring that stakeholders have immediate access to actionable insights.

Ambient Clinical Intelligence for Virtual Nursing and Patient Safety

The convergence of ambient intelligence and computer vision is revolutionizing the scope of bed management. By integrating data from AI-enabled sensors, systems can monitor patient safety milestones—such as fall prevention and hand hygiene—without physical room entries. This 'virtual nursing' capability is becoming a standard feature in high-end operational hubs, particularly in regions facing severe nursing shortages. The ability to provide 24/7 situational awareness over high-risk patients significantly reduces hospital-acquired conditions (HACs) and improves clinical outcomes.

Analysis by Type

Based on type, the bed management software segment is expected to hold the largest share in 2026. This dominance is driven by the consolidation of hospitals into large integrated delivery networks (IDNs) that require a centralized 'source of truth' to manage regional patient flow. However, the patient flow management solutions segment is projected to register the highest CAGR during the forecast period. This growth is fueled by the expansion of 'hospital-at-home' programs, where remote monitoring hubs coordinate care for patients outside traditional hospital walls, thereby increasing system capacity without physical bed expansion.

Analysis by Technology

Based on technology, the AI/ML segment is expected to account for the largest share in 2026. AI engines are foundational to modern bed management, enabling the prediction of patient census and discharge readiness. The AI/ML segment is also projected to register the highest CAGR, as health systems increasingly adopt autonomous operational modules. The integration of IoT and RTLS technology remains a critical secondary segment, providing the real-time location data of equipment and staff necessary for precise operational coordination.

North America is expected to dominate the global bed management systems market in 2026, accounting for an estimated 38.5% of total revenue. The region's dominance is supported by a mature healthcare IT landscape and the widespread adoption of centralized operational models by large IDNs like AdventHealth and Providence Swedish. These systems have reported serving thousands of additional patients annually through optimized bed orchestration. The presence of leading vendors and significant investment in digital health infrastructure continue to drive the market in the U.S. and Canada.

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This is driven by rapid healthcare infrastructure expansion and 'Smart Hospital' initiatives across China, India, and Australia. For example, major private healthcare providers in India are standardizing on centralized operational models to manage large patient volumes across multi-facility networks. The increasing adoption of cloud-based platforms and the digital transformation of public health agencies in the region are creating substantial opportunities for global and local technology integrators. The key companies operating in the Asia Pacific market are GE HealthCare, Philips, Siemens Healthineers, and various local technology integrators.

The competitive landscape of the global bed management systems market is characterized by intense innovation and strategic acquisitions as vendors seek to provide end-to-end operational orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide demonstrated ROI in terms of length-of-stay reduction. Strategic moves, such as the integration of patient communication and throughput modules into unified ecosystems, are redefining vendor positioning in the June 2026 landscape.

Key players operating in the global bed management systems market include GE HealthCare Technologies Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), Oracle Corporation (Oracle Health/Cerner) (U.S.), Microsoft Corporation (U.S.), Salesforce, Inc. (U.S.), GetWellNetwork, Inc. (U.S.), TeleTracking Technologies, Inc. (U.S.), McKesson Corporation (U.S.), NVIDIA Corporation (U.S.), symplr (U.S.), Health Catalyst, Inc. (U.S.), Infor (U.S.), Stryker Corporation (U.S.), Care.ai (U.S.), Artisight, Inc. (U.S.), Qventus, Inc. (U.S.), LeanTaaS, Inc. (U.S.), Wolters Kluwer (Netherlands), and Ascom Holding AG (Switzerland).

The market is projected to reach USD 3.50 billion by 2036, growing at a CAGR of 11% from 2026 to 2036.

Hospitals report an average 15% reduction in length of stay (LOS) and a 20% increase in patient throughput.

The Artificial Intelligence & Machine Learning (AI/ML) segment is the fastest-growing, as predictive analytics becomes essential for forecasting.

Approximately 65% of new deployments are cloud-native, enabling regional coordination and rapid scalability.

North America holds the largest share, estimated at 38.5% in 2026, driven by a mature IT infrastructure and high demand for efficiency.

Digital twins allow for 95% accuracy in simulating bed-request spikes and staffing models, reducing ambulance diversions by 18%.

AI-driven resource models reduce staff overtime by 12% and improve clinician satisfaction scores by an average of 18%.

Tertiary Care Centers and multi-hospital Integrated Delivery Networks (IDNs) are the primary adopters of enterprise-wide hubs.

Integrated monitoring within operational hubs has been shown to improve clinical safety compliance by 22% and reduce hospital-acquired conditions.

The top 5 players are Epic Systems Corporation, Oracle Health (Cerner), GE HealthCare, TeleTracking Technologies, and CentralSquare Technologies.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Type

3.2.2. Market Analysis, by Component

3.2.3. Market Analysis, by Technology

3.2.4. Market Analysis, by Application

3.2.5. Market Analysis, by End User

3.2.6. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Need for Throughput Optimization Amid Chronic ED Boarding

4.2.1.2. Global Healthcare Staffing Crisis and Predictive Resource Alignment

4.2.1.3. Transition Toward Value-Based Care and Real-time Clinical Risk Monitoring

4.2.2. Restraints

4.2.2.1. High Initial Capital Expenditure and Multi-Year ROI Cycles

4.2.2.2. Organizational Change Management Resistance and Cultural Shifts

4.2.3. Opportunities

4.2.3.1. Expansion into Regional Virtual Care Hubs and Hospital-at-Home Models

4.2.3.2. Integration of Digital Twin Technology for Operational Stress-Testing

4.2.3.3. Greenfield Smart Hospital Infrastructure Projects in Emerging Markets

4.2.4. Challenges

4.2.4.1. Data Interoperability Across Fragmented Legacy IT Systems

4.2.4.2. Cybersecurity Vulnerabilities in Centralized Operational Hubs

4.2.4.3. Managing Alert Fatigue and Operator Desensitization

4.2.5. Trends

4.2.5.1. Move Toward Autonomous and Self-Healing Operational Logistics

4.2.5.2. Integration of Ambient Intelligence and Computer Vision for Virtual Nursing

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Bed Management Systems Market, by Type

5.1. Overview

5.2. Bed Management Software

5.3. Admission, Discharge, and Transfer (ADT) Systems

5.4. Patient Flow Management Solutions

5.5. Capacity Optimization Software

6. Global Bed Management Systems Market, by Component

6.1. Overview

6.2. Software

6.2.1. Real-time Visualization & Dashboards

6.2.2. Predictive Analytics & AI/ML Engines

6.2.3. Resource & Bed Orchestration Modules

6.3. Services

6.3.1. Strategic Consulting & Change Management

6.3.2. Custom Implementation & Integration

6.3.3. Post-Deployment Support & Maintenance

6.4. Hardware

7. Global Bed Management Systems Market, by Technology

7.1. Overview

7.2. Artificial Intelligence & Machine Learning

7.3. IoT & Real-time Location Systems (RTLS)

7.4. Telehealth & Remote Monitoring Integration

8. Global Bed Management Systems Market, by Application

8.1. Overview

8.2. Patient Flow & Capacity Management

8.3. Workforce & Staffing Optimization

8.4. Clinical Risk Monitoring

9. Global Bed Management Systems Market, by End User

9.1. Overview

9.2. Tertiary Care Centers

9.3. Multi-hospital Systems & IDNs

9.4. Mid-sized and Small Hospitals

9.5. Specialized Facilities & Clinics

10. Global Bed Management Systems Market, by Geography

10.1. Overview

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. India

10.4.4. South Korea

10.4.5. Australia

10.4.6. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East & Africa

10.6.1. GCC Countries

10.6.2. South Africa

10.6.3. Rest of Middle East & Africa

11. Competitive Landscape

11.1. Overview

11.2. Key Strategic Developments

11.3. Market Share Analysis

11.4. Competitive Benchmarking

12. Company Profiles

12.1. Epic Systems Corporation

12.2. Oracle Health (Oracle Corporation)

12.3. GE HealthCare Technologies Inc.

12.4. TeleTracking Technologies, Inc.

12.5. CentralSquare Technologies

12.6. Advanced Data Systems Corporation

12.7. Lyngsoe Systems A/S

12.8. The Access Group

12.9. EMIS Health (UnitedHealth Group)

12.10. SAP SE

12.11. IMS MAXIMS

12.12. Blueberry Health

12.13. Wise Technologies Ltd.

12.14. Patient Focus Systems

12.15. SARU TECH

12.16. LeanTaaS, Inc.

12.17. Qventus, Inc.

12.18. Getinge AB

12.19. Philips Healthcare

12.20. Siemens Healthineers AG

13. Appendix

Published Date: Nov-2023

Published Date: Sep-2023

Subscribe to get the latest industry updates