Resources

About Us

Autonomous Naval Systems Market Size, Share & Trends Analysis by Platform Type (USVs, AUVs, ROVs, Hybrid and Swarm Systems), Application, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

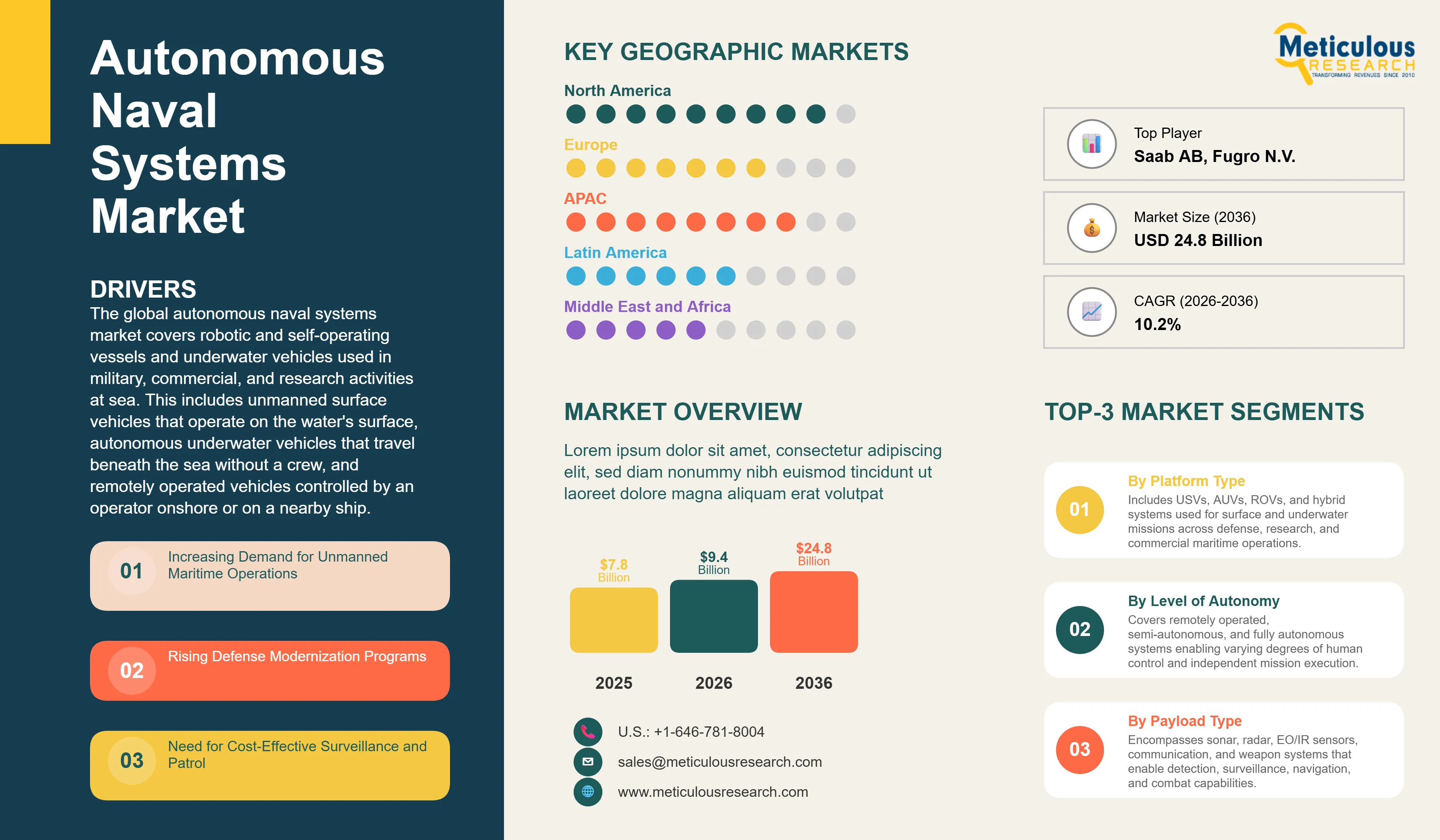

Report ID: MRAD - 1041909 Pages: 280 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global autonomous naval systems market was valued at USD 7.8 billion in 2025. This market is expected to reach USD 24.8 billion by 2036 from an estimated USD 9.4 billion in 2026, growing at a CAGR of 10.2% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global autonomous naval systems market covers robotic and self-operating vessels and underwater vehicles used in military, commercial, and research activities at sea. This includes unmanned surface vehicles that operate on the water's surface, autonomous underwater vehicles that travel beneath the sea without a crew, and remotely operated vehicles controlled by an operator onshore or on a nearby ship. These systems carry sensors, cameras, sonar equipment, communication tools, and in some military cases, weapons, enabling navies and commercial operators to conduct ocean missions safely, cheaply, and without putting personnel at risk.

The market is growing primarily because navies around the world need smarter, more affordable ways to monitor large ocean areas, detect underwater threats, and secure coastlines without deploying large crewed ships. Autonomous systems can stay at sea longer, cover wider areas, and operate in dangerous conditions where sending a crewed vessel would be too risky. Defense spending on unmanned maritime systems has been rising steadily across the United States, United Kingdom, Australia, and several Asian countries as governments recognize that autonomous vessels offer a cost-effective way to extend naval reach, particularly in large ocean territories where continuous human-crewed patrol is not practical.

Two significant opportunities are shaping the market going forward. The growing use of AI-based navigation and decision-making software is making autonomous vessels smarter and more capable, allowing them to complete complex missions with minimal human input. This is opening new possibilities in areas like underwater mine detection, submarine tracking, and long-range ocean surveys. In addition, the commercial sector is increasingly adopting autonomous vessels for offshore oil and gas inspection, environmental monitoring, and underwater infrastructure surveys, creating a fast-growing non-military customer base that is expanding the market well beyond its traditional defense roots.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 24.8 Billion |

|

Market Size in 2026 |

USD 9.4 Billion |

|

Market Size in 2025 |

USD 7.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.2% |

|

Dominating Platform Type |

Unmanned Surface Vehicles (USVs) |

|

Fastest Growing Platform Type |

Autonomous Underwater Vehicles (AUVs) |

|

Dominating Level of Autonomy |

Semi-Autonomous Systems |

|

Fastest Growing Level of Autonomy |

Fully Autonomous Systems |

|

Dominating Payload Type |

Sonar Systems |

|

Fastest Growing Payload Type |

Weapon Systems |

|

Dominating Application |

ISR (Intelligence, Surveillance & Reconnaissance) |

|

Fastest Growing Application |

Anti-Submarine Warfare (ASW) |

|

Dominating End User |

Navy |

|

Fastest Growing End User |

Commercial Maritime Operators |

|

Dominating Deployment Mode |

Standalone Systems |

|

Fastest Growing Deployment Mode |

Fleet/Swarm-Based Systems |

|

Dominating Propulsion Type |

Electric Propulsion |

|

Fastest Growing Propulsion Type |

Hybrid Propulsion |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Navies Replacing Crewed Ships with Unmanned Vessels for Routine Missions

One of the clearest trends in the market is that navies are increasingly using autonomous surface and underwater vehicles to handle routine but important tasks such as patrolling coastlines, detecting mines, and gathering intelligence. These missions used to require a crewed ship and a full team of sailors, but now they can be done at a fraction of the cost using an unmanned vessel. The U.S. Navy's Ghost Fleet Overlord program, which uses large unmanned surface ships to conduct patrols and surveillance missions, is one of the best examples of this shift. The United Kingdom, Australia, and Norway have all launched similar programs, buying or developing their own unmanned naval vessels to free up their crewed warships for higher-priority tasks.

This trend is not just about cutting costs. It is also about managing risk. Sending an autonomous vessel into a minefield to clear a path is far safer than sending a crew. Operating an unmanned submarine tracker near a rival country's waters avoids potential diplomatic incidents. Navies have recognized that many dangerous, dull, or repetitive missions are well-suited for autonomous systems, and they are now actively building these capabilities into their long-term fleet plans. This shift is creating steady, growing demand for autonomous naval platforms and the sensors and software systems that make them work.

AI and Smarter Software Making Autonomous Vessels More Capable

Early autonomous naval systems required constant human supervision and could only follow a pre-planned route with limited ability to adapt to unexpected situations. That is changing rapidly. Today's AI-powered systems can avoid collisions automatically, respond to changes in weather or sea conditions, identify suspicious vessels, and even make basic tactical decisions without waiting for a human operator to intervene. This improvement in capability is making autonomous systems useful for a much wider range of missions and is accelerating their adoption across both military and commercial customers.

Companies like Kongsberg, L3Harris, and Ocean Infinity are investing heavily in the software platforms that run autonomous vessels, treating the software as just as important as the vessel itself. A more capable software system means the same physical vessel can be upgraded over time to handle new tasks, giving customers a better long-term return on their investment. The growing availability of AI-based navigation and mission-planning tools is also helping smaller navies and coast guards that lack the large technical teams required to operate earlier generations of remotely controlled systems, broadening the customer base for autonomous naval products.

Commercial Sector Becoming a Major Growth Driver

While the military was the original customer for autonomous naval systems, the commercial sector has become an important and fast-growing part of the market. Offshore oil and gas companies need to regularly inspect pipelines, wellheads, and other underwater infrastructure, and autonomous underwater vehicles can do this work more cheaply and safely than sending human divers. Environmental agencies and research institutions use autonomous vessels to monitor ocean temperatures, track pollution, map the seabed, and collect data that would be too expensive to gather using research ships. Cable companies use ROVs and AUVs to inspect and repair undersea telecommunications cables.

Ocean Infinity and Fugro are among the leading companies building businesses around commercial autonomous maritime services, offering clients the ability to conduct large-scale ocean surveys and inspections using fleets of autonomous vessels rather than crewed ships. This approach can complete surveys in less time and at lower cost, which is attracting growing interest from the energy sector, telecoms companies, and government environmental agencies. The commercial segment is expected to be the fastest-growing non-defense part of the autonomous naval systems market through the forecast period, broadening the market beyond its traditional military base.

Increasing Demand for Unmanned Maritime Operations

The clearest driver of this market is a simple need: navies and maritime agencies want to monitor vast ocean areas and conduct dangerous missions without putting sailors at risk or spending the full cost of a crewed warship. The world's oceans are enormous, and no country can afford to keep crewed ships everywhere they need a maritime presence. Autonomous surface and underwater vehicles solve this problem by operating for days or weeks without a crew, covering large areas at low cost. The U.S. Navy alone manages millions of square kilometers of ocean territory and has been one of the most active buyers of autonomous naval systems for this reason. Coast guards in Southeast Asia, the Middle East, and Europe face similar challenges in protecting long coastlines and exclusive economic zones, and autonomous patrol vessels are increasingly seen as a cost-effective solution. As these programs demonstrate success, more countries are following suit, creating a steadily expanding global customer base.

Need for Cost-Effective Surveillance and Patrol

Operating a crewed naval vessel costs tens of thousands of dollars per day when crew salaries, fuel, maintenance, and logistics are included. An autonomous vessel performing the same patrol mission can cost a fraction of that amount. For countries with limited defense budgets but large maritime responsibilities, this cost difference is a compelling reason to invest in autonomous systems. The economic argument is especially strong for coast guards and smaller navies in Southeast Asia, Latin America, and Africa that need to protect fisheries, monitor illegal immigration, and guard coastline infrastructure but cannot afford to maintain large crewed ship fleets. As the cost of autonomous vessel platforms continues to fall with improving technology and rising production volumes, the economic case for autonomous maritime patrol is becoming convincing for a wider range of potential customers globally.

Integration of AI and Autonomous Navigation

The growing capability of AI-based navigation, decision-making, and mission-planning software is creating a major commercial opportunity for companies that can develop autonomous vessels able to complete complex missions with little or no human input. A fully autonomous vessel that can navigate to a target location, conduct a survey or patrol mission, respond safely to unexpected obstacles, and return to base on its own is worth far more to a customer than a remotely piloted vehicle that requires a trained operator watching a screen at all times. As AI software capabilities improve and the cost of the computing hardware required to run these systems falls, the business case for truly autonomous vessels is becoming much stronger. Companies that establish strong AI navigation platform capabilities early, backed by operational data from real-world deployments, will be in an excellent position to win the largest and most valuable autonomous naval system contracts over the forecast period.

Growth in Offshore Energy and Environmental Monitoring

The offshore energy sector represents one of the most commercially attractive markets for autonomous underwater vehicles and remotely operated vehicles. Oil and gas companies spend billions of dollars each year inspecting and maintaining undersea pipelines, wellheads, and production platforms. Replacing human divers and crewed support vessels with autonomous systems for routine inspection work can reduce costs significantly while improving safety. As the offshore wind energy sector grows rapidly, particularly in Europe and Asia-Pacific, the demand for undersea inspection and cable-laying support using autonomous vehicles is also growing. Environmental monitoring agencies and governments are increasing investment in ocean data collection using autonomous vessels to track climate-related changes in ocean temperature, acidity, and biodiversity. These commercial and environmental applications are growing quickly and provide revenue diversification for autonomous naval system suppliers beyond their traditional military customer base.

By Platform Type: In 2026, USVs to Dominate

Based on platform type, the global autonomous naval systems market is segmented into unmanned surface vehicles (USVs), autonomous underwater vehicles (AUVs), remotely operated vehicles (ROVs), and hybrid and swarm systems. In 2026, the USV segment is expected to account for the largest share of the global autonomous naval systems market. USVs are the most visible and commercially established autonomous naval platform category. They can be seen and tracked easily, are relatively straightforward to deploy and recover, and are versatile enough to carry sensors, cameras, and communication equipment for a wide range of missions including coastal patrol, mine detection support, intelligence gathering, and maritime security. Several navies including the U.S. Navy, Royal Navy, and Israeli Navy have already bought and deployed USVs operationally, creating a solid commercial foundation that makes USVs the current revenue leader in this market.

However, the AUV segment is poised to register the highest CAGR during the forecast period. AUVs travel underwater without being connected to a surface ship by a cable, making them ideal for covert military missions and for deep-water commercial surveys that surface vessels cannot conduct. The rapid growth of undersea cable inspection, offshore energy surveys, and anti-submarine warfare programs is creating strong demand for AUVs across both military and commercial customers. Advances in battery technology are extending AUV endurance from days to weeks, opening up longer-range mission possibilities that are attracting growing investment from navies and commercial operators alike.

By Level of Autonomy: In 2026, Semi-Autonomous Systems to Hold the Largest Share

Based on level of autonomy, the global autonomous naval systems market is segmented into remotely operated systems, semi-autonomous systems, and fully autonomous systems. In 2026, the semi-autonomous systems segment is expected to account for the largest share of the global autonomous naval systems market. Most operational autonomous naval vessels today sit in the semi-autonomous category. They can handle routine navigation, collision avoidance, and basic mission tasks on their own, but a human operator remains in the loop for key decisions such as engaging a potential threat or changing the mission plan in response to a new situation. This balance of automation and human oversight is preferred by most military customers, who want the efficiency benefits of autonomous operation without fully removing humans from decision-making, particularly in situations where the consequences of a mistake could be serious.

However, the fully autonomous systems segment is projected to register the highest CAGR during the forecast period. As AI navigation and decision-making software matures, and as navies build trust in autonomous systems through operational experience, the market is gradually shifting toward platforms that can complete entire missions without human intervention. Fully autonomous systems are particularly attractive for long-endurance underwater missions where maintaining a communication link to a human operator is not practical, and for swarm operations where dozens of vehicles must coordinate with each other faster than any human team could manage.

By Payload Type: In 2026, Sonar Systems to Hold the Largest Share

Based on payload type, the global autonomous naval systems market is segmented into sonar systems, radar systems, EO/IR sensors, communication systems, and weapon systems. In 2026, the sonar systems segment is expected to account for the largest share of the global autonomous naval systems market. Sonar is the most commonly carried payload on autonomous naval systems because it is essential for nearly every underwater mission. AUVs and ROVs use sonar to map the seafloor, detect mines, find undersea cables and pipelines, and track submarines. USVs tow sonar arrays for anti-submarine patrol and mine countermeasure missions. The very broad applicability of sonar across both military and commercial missions makes it the dominant payload category by revenue.

However, the weapon systems segment is projected to register the highest CAGR during the forecast period. Several major navies are actively developing and testing autonomous vessels capable of carrying and deploying weapons, including torpedo tubes on AUVs and small missile or gun systems on large USVs. The U.S. Navy's Large Unmanned Surface Vehicle program and similar programs in Israel and the UK include weapon system options. As these programs move from development into procurement, the weapon systems payload segment will grow rapidly, driven by the high per-unit value of armed autonomous naval systems compared with sensor-only platforms.

By Application: In 2026, ISR to Hold the Largest Share

Based on application, the global autonomous naval systems market is segmented into intelligence, surveillance and reconnaissance (ISR), mine countermeasures, anti-submarine warfare, border and coastal security, environmental monitoring, and offshore energy inspection. In 2026, the ISR segment is expected to account for the largest share of the global autonomous naval systems market. ISR is the most widely practiced application for autonomous naval systems today. Navies use autonomous vessels to gather information about what is happening in their territorial waters and in areas of strategic interest, tracking ship movements, monitoring for suspicious activity, and collecting intelligence data that is transmitted back to shore-based command centers. Because ISR missions are continuous and cover large geographic areas, they are ideal for autonomous vehicles that can operate without crew rotation.

However, the anti-submarine warfare (ASW) segment is projected to register the highest CAGR during the forecast period. Finding and tracking submarines is one of the most technically demanding and strategically important naval missions, and it is also one of the most expensive when conducted using crewed ships. Autonomous underwater gliders and AUVs equipped with advanced sonar can cover large ocean areas hunting for submarine signatures at a much lower cost than crewed ASW frigates or maritime patrol aircraft. The growing submarine fleets of China, Russia, North Korea, and Iran are creating urgency across NATO and Indo-Pacific allied navies to invest more in ASW capability, and autonomous systems are seen as an affordable way to extend ASW coverage without proportional increases in crewed ship and aircraft numbers.

By End User: In 2026, Navy to Hold the Largest Share

Based on end user, the global autonomous naval systems market is segmented into navy, coast guard, commercial maritime operators, offshore energy companies, and research institutions. In 2026, the navy segment is expected to account for the largest share of the global autonomous naval systems market. National navies are the largest buyers of autonomous naval systems because their missions are the most complex, their budgets are the largest, and their need for unmanned capability is most pressing. The U.S. Navy, Royal Navy, Australian Navy, and Israeli Navy are among the most active early adopters, with ongoing procurement programs for USVs, AUVs, and unmanned underwater systems that collectively represent the majority of total market revenue. Other navies including India, France, Germany, South Korea, and Japan are also investing in autonomous naval capability as part of their broader force modernization plans.

However, the commercial maritime operators segment is projected to register the highest CAGR during the forecast period. Companies providing ocean surveys, cable inspection, port management, and offshore infrastructure services are increasingly replacing expensive crewed survey ships with fleets of autonomous vessels that can complete the same work at lower cost. As autonomous vessel technology matures and becomes more reliable, more commercial applications are becoming financially attractive, creating a rapidly expanding commercial customer base for autonomous naval system manufacturers and operators.

By Deployment Mode: In 2026, Standalone Systems to Hold the Largest Share

Based on deployment mode, the global autonomous naval systems market is segmented into standalone systems, fleet and swarm-based systems, and systems integrated with manned platforms. In 2026, the standalone systems segment is expected to account for the largest share of the global autonomous naval systems market. The majority of current autonomous naval deployments involve a single vessel completing a defined mission independently, which is the simplest and most operationally proven deployment model. Standalone autonomous vessels require simpler control infrastructure and can be procured and operated without the complex coordination systems needed for multi-vessel swarms.

However, the fleet and swarm-based systems segment is projected to register the highest CAGR during the forecast period. Operating multiple autonomous vessels together as a coordinated team multiplies the area covered, speed of mission completion, and resilience compared with a single vessel, making swarm approaches highly attractive for large-scale ocean surveys, coordinated mine clearing, and distributed surveillance. U.S. DARPA programs and commercial ocean survey companies are actively developing swarm coordination capabilities, and as this technology matures it will unlock a significant expansion of what autonomous naval systems can accomplish.

Autonomous Naval Systems Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global autonomous naval systems market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global autonomous naval systems market. The United States is the world's largest buyer of autonomous naval systems by a significant margin, driven by the U.S. Navy's active programs to develop and buy unmanned surface vessels and underwater vehicles as part of its strategic plan to operate larger numbers of ships with a reduced total crew size and budget. The U.S. Navy's Ghost Fleet Overlord program for large unmanned surface ships, the Extra Large Unmanned Underwater Vehicle program for long-range submarine-like AUVs, and a wide range of smaller USV and AUV procurement programs represent billions of dollars in annual spending that make North America the world's dominant autonomous naval systems market. The U.S. defense industrial base, which includes companies like L3Harris, Textron, General Dynamics, Huntington Ingalls Industries, and Teledyne Technologies, is home to many of the world's leading autonomous naval system developers. Canada's growing investment in Arctic maritime surveillance using autonomous systems adds further demand to the North American market.

However, the Asia-Pacific autonomous naval systems market is expected to grow at the fastest CAGR during the forecast period. The rapid build-up of Chinese naval power and the rising tensions in the South China Sea and Taiwan Strait are compelling Japan, South Korea, Australia, India, and several Southeast Asian nations to invest urgently in autonomous maritime capabilities that can provide a surveillance and deterrence presence without requiring additional crewed warships. Australia has been one of the most aggressive investors in autonomous naval systems in the region, running the Ghost Shark and Bluezone autonomous underwater programs. Japan's Maritime Self-Defense Force is testing autonomous patrol vessels. South Korea is investing in unmanned naval systems as part of its broader defense technology modernization. India's growing maritime security focus is generating new interest in autonomous coastal patrol systems. China is also a major developer and buyer of autonomous naval systems for its own navy, making Asia-Pacific the most dynamic and fastest-growing regional market in the world.

Europe is a well-developed autonomous naval systems market with strong technology capabilities and growing government investment. Norway's Kongsberg Gruppen is a world leader in autonomous ship technology, and the company's HUGIN AUV series is used by navies and commercial operators on every continent. The UK's Royal Navy has been an early adopter of USVs including the autonomous mine-hunting systems. France, Germany, Italy, and Sweden are all running military autonomous naval programs. The strong commercial maritime and offshore energy sectors in the North Sea provide important commercial demand alongside the military procurement programs. The Middle East is a growing market, particularly in Israel, which has one of the world's most advanced autonomous naval industries through Elbit Systems and IAI, and in the Gulf states investing in autonomous coastal security for their long and strategically important coastlines.

The autonomous naval systems market includes a mix of large established defense companies, specialist maritime technology firms, and newer technology-focused companies. Competition is based on the performance and reliability of autonomous platforms in real ocean conditions, the quality of the navigation and sensor software, certification credentials for naval use, track record of successful program delivery, and the ability to provide long-term maintenance and support in remote locations.

Kongsberg Gruppen of Norway is a global technology leader in the market, with its HUGIN AUV series widely used by navies and commercial survey companies around the world, and its autonomous ship systems platform used in commercial shipping applications. L3Harris provides a range of autonomous surface and underwater platforms primarily for U.S. and allied military customers. Huntington Ingalls Industries is building large unmanned surface vessels for the U.S. Navy. Saab AB from Sweden provides autonomous mine countermeasures systems and underwater vehicles. Textron produces the Common Unmanned Surface Vehicle used by the U.S. Navy. Ocean Infinity operates the world's largest fleet of autonomous survey vessels for commercial ocean exploration and infrastructure inspection. Teledyne Technologies and Fugro are major providers of autonomous underwater vehicles for commercial survey and inspection work.

The report provides a comprehensive competitive analysis based on an extensive review of leading players' product portfolios, military and commercial customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global autonomous naval systems market include Kongsberg Gruppen ASA (Norway), L3Harris Technologies Inc. (U.S.), Huntington Ingalls Industries Inc. (U.S.), Saab AB (Sweden), Textron Inc. (U.S.), Thales Group (France), Leonardo S.p.A. (Italy), BAE Systems plc (UK), General Dynamics Corporation (U.S.), Elbit Systems Ltd. (Israel), Israel Aerospace Industries (Israel), Ocean Infinity Ltd. (UK), Teledyne Technologies Incorporated (U.S.), Fugro N.V. (Netherlands), and ECA Group (France), among others.

The global autonomous naval systems market is expected to reach USD 24.8 billion by 2036 from an estimated USD 9.4 billion in 2026, at a CAGR of 10.2% during the forecast period 2026-2036.

In 2026, the USV segment is expected to hold the largest share of the global autonomous naval systems market, driven by USVs being the most widely deployed autonomous naval platform across military and commercial customers with multiple active procurement programs already underway.

The AUV segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by growing demand from navies for underwater surveillance and anti-submarine patrol, the expansion of commercial deep-water survey and offshore energy inspection applications, and improvements in battery technology enabling longer-range AUV missions.

In 2026, the intelligence, surveillance and reconnaissance (ISR) segment is expected to hold the largest share of the global autonomous naval systems market, reflecting ISR as the most common and commercially established application for autonomous naval vessels across navies and coast guards worldwide.

The anti-submarine warfare segment is expected to register the highest CAGR during the forecast period, driven by growing submarine threats in multiple regions compelling NATO and Indo-Pacific allied navies to invest in affordable autonomous ASW patrol systems that can cover larger ocean areas than crewed ships at lower cost.

The market is primarily driven by navies and maritime agencies needing affordable ways to monitor large ocean areas and conduct dangerous missions without risking crew members, and by the growing commercial demand from offshore energy companies, survey firms, and environmental agencies using autonomous vessels to replace expensive crewed ships for inspection and data collection work.

Key players are Kongsberg Gruppen ASA (Norway), L3Harris Technologies Inc. (U.S.), Huntington Ingalls Industries Inc. (U.S.), Saab AB (Sweden), Textron Inc. (U.S.), Thales Group (France), Leonardo S.p.A. (Italy), BAE Systems plc (UK), General Dynamics Corporation (U.S.), Elbit Systems Ltd. (Israel), Israel Aerospace Industries (Israel), Ocean Infinity Ltd. (UK), Teledyne Technologies Incorporated (U.S.), Fugro N.V. (Netherlands), and ECA Group (France), among others.

Asia-Pacific is expected to register the highest growth rate in the global autonomous naval systems market during the forecast period 2026-2036, driven by rising maritime security tensions in the South China Sea compelling Japan, South Korea, Australia, and India to urgently expand their autonomous naval capabilities alongside China's own large domestic autonomous naval development programs.

Published Date: Jan-2026

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates