Resources

About Us

Loitering Munitions Market Size, Share and Trends Analysis by Munition Type, Range/Endurance, Launch Platform, Guidance System, Application, End User, and Warhead Type - Global Opportunity Analysis and Industry Forecast (2026 to 2036)

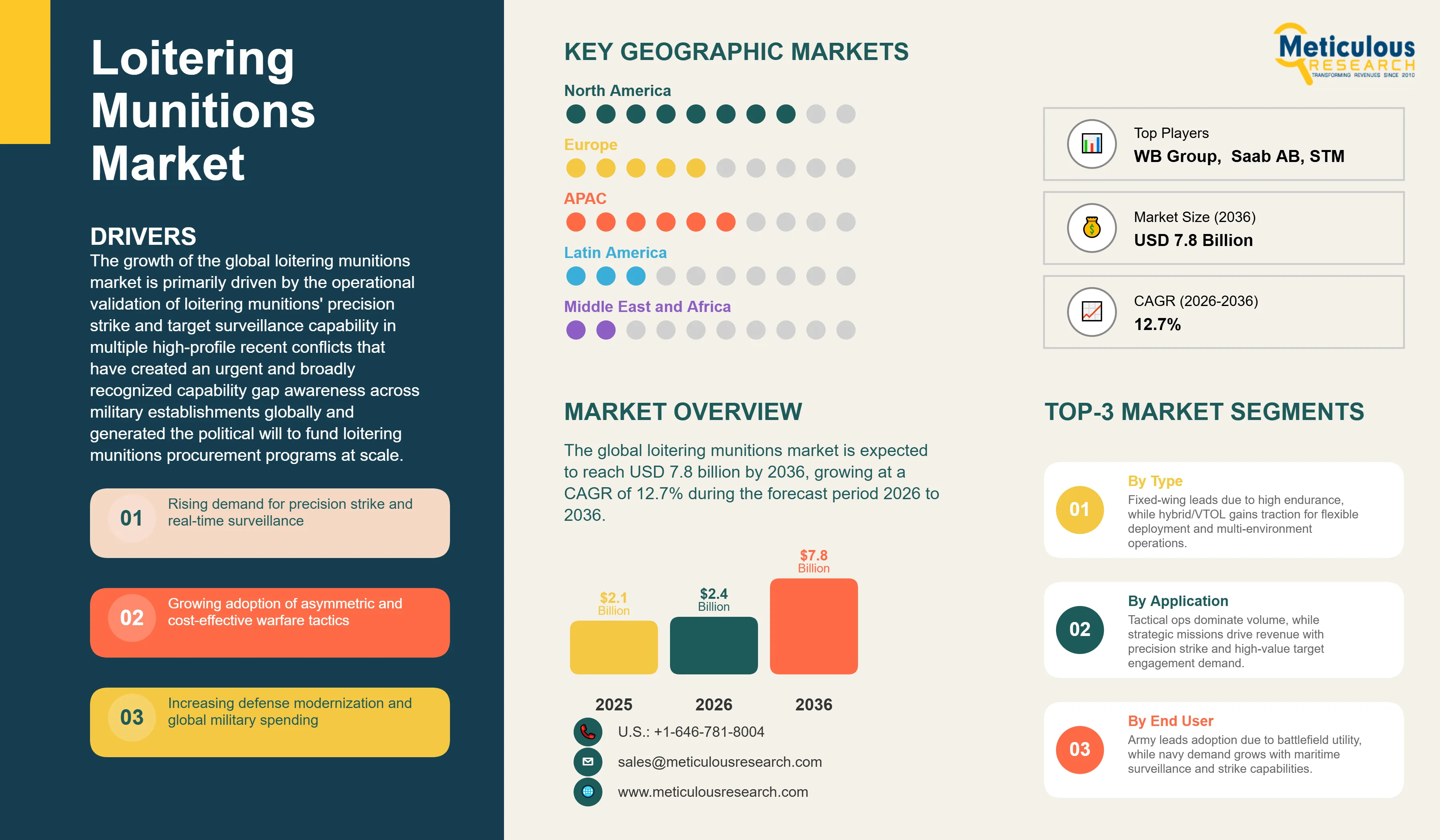

Report ID: MRAD - 1041907 Pages: 275 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global loitering munitions market was valued at USD 2.1 billion in 2025. This market is expected to reach USD 7.8 billion by 2036 from an estimated USD 2.4 billion in 2026, growing at a CAGR of 12.7% during the forecast period 2026 to 2036.

Click here to: Get Free Sample Pages of this Report

The global loitering munitions market covers unmanned aerial weapon systems that combine extended target area surveillance capability with terminal precision strike functionality, enabling operators to loiter over a target area for periods ranging from minutes to hours before committing to a strike engagement — a capability combination that no conventional munition or armed UAV system provides in a single, integrated, expendable platform. The market spans man-portable tactical systems weighing under 5 kilograms and costing under USD 10,000 through operational and strategic systems weighing hundreds of kilograms with unit costs exceeding USD 2 million, serving army, navy, air force, and special operations force end users across the full spectrum of military procurement budgets and operational environments.

The growth of the global loitering munitions market is primarily driven by the operational validation of loitering munitions' precision strike and target surveillance capability in multiple high-profile recent conflicts that have created an urgent and broadly recognized capability gap awareness across military establishments globally and generated the political will to fund loitering munitions procurement programs at scale. The Nagorno-Karabakh conflict's demonstration that loitering munitions could systematically defeat sophisticated Soviet-legacy air defense systems and armored vehicle fleets at minimal cost per engagement shocked the global defense community and triggered a wave of loitering munitions procurement program initiation that continues to generate market demand growth. The Ukraine conflict's ongoing documentation of both Russian and Ukrainian loitering munitions employment, including the operationally significant Shahed-136 and Lancet systems on the Russian side and Ukrainian use of multiple domestically developed and internationally supplied systems, has maintained the operational lessons impetus that is sustaining procurement program momentum across NATO and partner nation defense establishments.

Two transformative opportunities are shaping the market's long-term growth trajectory. The integration of advanced artificial intelligence target recognition algorithms into loitering munitions seekers is enabling a transition from purely operator-directed to operator-supervised engagement, allowing single operators to manage multiple simultaneously airborne loitering munitions and engage time-sensitive targets in scenarios where communication link latency or operator cognitive overload would otherwise prevent effective engagement. The development of swarm-capable loitering munitions architectures is advancing from DARPA research programs toward operational procurement readiness, with the potential to fundamentally alter the balance between attack and defense in conventional warfare by overwhelming adversary active protection and air defense systems with simultaneous engagement that exceeds their engagement capacity.

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 7.8 Billion |

|

Market Size in 2026 |

USD 2.4 Billion |

|

Market Size in 2025 |

USD 2.1 Billion |

|

Revenue Growth Rate (2026 to 2036) |

CAGR of 12.7% |

|

Dominating Munition Type |

Fixed-Wing Loitering Munitions |

|

Fastest Growing Munition Type |

Hybrid/VTOL Loitering Munitions |

|

Dominating Range/Endurance |

Medium Range (50–200 km) |

|

Fastest Growing Range/Endurance |

Long Range (>200 km) |

|

Dominating Launch Platform |

Man-Portable Systems (Unit Volume) |

|

Fastest Growing Launch Platform |

Naval Platforms |

|

Dominating Guidance System |

EO/IR-Based Targeting |

|

Fastest Growing Guidance System |

Autonomous/AI-Based Targeting |

|

Dominating Application |

Strategic Operations (Revenue) |

|

Fastest Growing Application |

Surveillance and Reconnaissance Strike |

|

Dominating End User |

Army |

|

Fastest Growing End User |

Navy |

|

Dominating Warhead Type |

Anti-Armor Warheads (Revenue) |

|

Fastest Growing Warhead Type |

Multi-Purpose Warheads |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI-Powered Autonomous Target Recognition and Engagement Decision Support: The integration of artificial intelligence machine learning algorithms into loitering munitions seeker and mission management systems is the most consequential technology trend reshaping the capability trajectory and competitive landscape of the global market. AI-based automatic target recognition systems trained on extensive ground vehicle and weapon system imagery datasets are enabling real-time target classification within loitering munitions EO/IR seeker fields of view, providing operators with target type confidence assessments that accelerate engagement decision-making and support the development of higher-automation engagement modes in which the system autonomously locks and tracks operator-designated target types while awaiting engagement authorization. Leading developers including Elbit Systems and AeroVironment are positioning AI-enabled targeting as the primary competitive differentiator for next-generation loitering munitions procurement programs.

Swarm Loitering Munitions Development and Collaborative Engagement Architectures: The transition of swarm loitering munitions from research laboratory demonstration to pre-operational development is one of the most strategically significant trends in the global defense market, with the potential to fundamentally alter the tactical balance between attack and defense in conventional warfare by enabling mass coordinated precision strike that exceeds the engagement capacity of adversary active protection and air defense systems. U.S. DoD investment through DARPA's CODE program and the Strategic Capabilities Office's previous Perdix demonstrations has established the foundational autonomy and inter-swarm communication technology on which operational swarm loitering munitions architectures will be built. Multiple allied and partner nations including Australia, the United Kingdom, and Israel are funding parallel swarm loitering munitions development programs, and the competition to operationalize swarm capability before adversaries develop effective counter-swarm defenses is accelerating development investment and procurement timeline urgency.

Electronic Warfare Resistance and GPS-Independent Navigation Integration: The operational experience of the Ukraine conflict — where both GPS jamming and communication link disruption have materially affected loitering munitions operational effectiveness in the contested electromagnetic environment of high-intensity conventional warfare — has elevated electronic warfare resistance to a primary development priority and procurement specification requirement across the global loitering munitions market. Anti-jamming GPS receiver technology, multi-mode navigation combining inertial, terrain-referenced, and passive optical flow navigation, frequency-hopping communication protocols, and stored-mission autonomous execution capability that maintains mission effectiveness through communication link disruption are among the EW resistance features being prioritized in next-generation development programs and retrofitted where possible into current-generation systems to address the lessons of operational employment in GPS and communication-contested environments.

Naval Application Development and Maritime Strike Capability: The expanding development and procurement of loitering munitions for naval applications — ship-launched anti-ship strike, expeditionary maritime patrol and area denial, and naval force protection — represents one of the most significant near-term market expansion opportunities, as naval forces across multiple major navies recognize the operational advantage of persistent surveillance-strike capability against maritime targets and the practical limitations of existing naval strike assets for engaging small, fast-moving, and dispersed maritime threat categories. The U.S. Marine Corps' EABO operational concept, which envisions small dispersed island-based teams with organic long-range precision anti-ship strike capability, is among the most demanding and consequential naval loitering munitions requirements driving system development, and the resulting capability investment is expected to generate broadly applicable naval loitering munitions technology that will address procurement requirements across allied and partner navies globally.

Loitering Munitions Market by Munition Type: Fixed-Wing Leading by Share, Hybrid/VTOL by Growth

Based on munition type, the global loitering munitions market is segmented into fixed-wing loitering munitions, rotary-wing loitering munitions, and hybrid/VTOL loitering munitions. In 2026, the fixed-wing loitering munitions segment is expected to account for the largest share of the global market. Fixed-wing loitering munitions' dominant market position reflects the aerodynamic efficiency of fixed-wing flight, which delivers the highest endurance-to-platform-weight ratio achievable with current propulsion technology, and the operational primacy of endurance as the defining performance parameter in the operational and strategic strike applications that account for the largest share of market revenue. Systems including the IAI Harop (>9 hours), AeroVironment ALTIUS-600 (4+ hours), and Elbit SkyStriker (2 hours) address the high-value precision strike missions in which multi-hour target area persistence is required to achieve reliable high-value target engagement.

However, the hybrid/VTOL loitering munitions segment is projected to register the highest CAGR during the forecast period. Hybrid VTOL systems that combine vertical takeoff and landing flexibility with fixed-wing cruise flight efficiency are attracting rapidly growing procurement interest from naval and special operations force customers for whom the absence of launch infrastructure requirements is a critical operational enabler, and from army customers who require the versatility of VTOL launch in confined and space-constrained deployment environments that tube-launch fixed-wing systems cannot always accommodate. As propulsion efficiency advances close the endurance gap between hybrid VTOL and pure fixed-wing designs of equivalent size, the operational versatility advantage of VTOL capability is expected to drive procurement share gain at the expense of fixed-wing systems in applications where launch flexibility is a valued capability differentiator.

Loitering Munitions Market by Guidance System: EO/IR-Based Targeting Leading, AI-Autonomous Growing Fastest

Based on guidance system, the global loitering munitions market is segmented into GPS/INS-based guidance, EO/IR-based targeting, laser-guided systems, and autonomous/AI-based targeting. In 2026, the EO/IR-based targeting segment is expected to account for the largest share of the global loitering munitions market. EO/IR guidance dominates the market because it is the primary terminal guidance technology in the large majority of current loitering munitions platforms, providing the day-night, all-weather target imaging capability through which operators identify and designate targets for engagement decision. The combination of GPS/INS navigation for area transit with EO/IR terminal guidance is the standard dual-mode guidance architecture in the most widely deployed loitering munitions systems globally, and the continued procurement of these systems at scale is expected to maintain EO/IR guidance's dominant market position through the early forecast period.

However, the autonomous/AI-based targeting segment is projected to register the highest CAGR during the forecast period. As artificial intelligence target recognition algorithms mature from laboratory demonstration into operationally reliable capability, the procurement preference of advanced military customers is shifting toward systems with validated autonomous target recognition and classification capability that reduces operator workload, enables faster engagement of time-sensitive targets, and supports the development of multi-loitering-munitions management architectures in which single operators supervise rather than directly control individual system engagements. The operational imperative of managing multiple simultaneous loitering munitions in the swarm employment scenarios anticipated in future high-intensity conflicts makes AI-based targeting capability a necessity rather than an option for the advanced procurement programs that will define next-generation market requirements.

Loitering Munitions Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global loitering munitions market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of the global loitering munitions market. North America's dominant market position reflects the United States' position as the world's largest defense spender, the most technically advanced developer of loitering munitions systems, and the most active near-term procurer of loitering munitions capability across its Army, Marine Corps, Navy, and special operations force requirements. The U.S. DoD's procurement of Switchblade systems in the thousands of units, both for U.S. military fielding and as security assistance to Ukraine, has established a production scale and investment environment at AeroVironment and associated suppliers that is funding the next-generation development programs that will define the U.S. market through the forecast period. The U.S. industrial base's technology leadership in AI-enabled guidance, electronic warfare resistance, and autonomous systems architecture provides a competitive foundation that is expected to sustain North American revenue leadership throughout the forecast period.

However, the Asia-Pacific loitering munitions market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific's high growth trajectory reflects the convergence of multiple high-intensity demand drivers operating simultaneously across the region's largest defense markets. India's defense modernization investment — supported by the government's Make in India defense industrial development policy and the urgent operational requirement for loitering munitions along the Line of Actual Control following the 2020 Galwan Valley confrontation with China — is generating both domestic development investment and accelerated import procurement that collectively represent one of the largest single-nation procurement growth opportunities in the global market. Japan's historic defense spending increase toward 2% of GDP is funding a new generation of loitering munitions capability development by Mitsubishi Heavy Industries and associated manufacturers, creating a substantial new procurement program in the Asia-Pacific region's third-largest defense market. South Korea's urgent precision fires procurement in response to documented North Korean drone violations and the evolving threat along the Demilitarized Zone is driving accelerated evaluation and procurement of multiple loitering munitions systems for rapid fielding across ROK Army and special forces formations.

The Middle East and Africa region represents the second-largest regional market and the world's most significant loitering munitions export hub, anchored by Israel's globally pre-eminent defense industry that produces and exports the majority of the world's most technically advanced loitering munitions systems. The region's multiple active conflict environments, including the Yemen conflict, the Libya intervention, and multiple sub-Saharan African security operations, provide operational deployment contexts that generate both direct consumption demand and the combat effectiveness documentation that drives international procurement interest in battle-proven systems. Gulf Cooperation Council nations, particularly the UAE, Saudi Arabia, and Qatar, maintain defense procurement budgets large enough to fund significant loitering munitions acquisition programs, and the regional security competition environment creates sustained demand growth that is expected to maintain the Middle East and Africa as a top-three global region through the forecast period.

The global loitering munitions market is moderately concentrated, with Israeli manufacturers including Israel Aerospace Industries, Elbit Systems, and UVision Air holding a dominant position based on decades of technology leadership and extensive operational deployment track records, competing alongside U.S. manufacturers including AeroVironment, L3Harris Technologies, Northrop Grumman, and Lockheed Martin that lead in AI-enabled guidance and electronic warfare resistance capability, and facing intensifying competition from Turkish manufacturer STM, Polish developer WB Group, and emerging indigenous developers across India, South Korea, Australia, and multiple other nations. Competition is focused on guidance system performance and AI capability, electronic warfare resistance, endurance-to-platform-size ratio, production cost and delivery timeline reliability, and the ability to structure industrial partnership arrangements that satisfy domestic content and technology development requirements of major procurement nations.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' loitering munitions technology portfolios, customer deployment bases, geographic market presence, and key strategic developments. Some of the key players operating in the global loitering munitions market include AeroVironment, Inc. (U.S.), UVision Air Ltd. (Israel), Elbit Systems Ltd. (Israel), Israel Aerospace Industries (Israel), Rheinmetall AG (Germany), Thales Group (France), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Leonardo S.p.A. (Italy), L3Harris Technologies, Inc. (U.S.), Saab AB (Sweden), ZALA Aero Group/Kalashnikov Concern (Russia), WB Group (Poland), STM — Savunma Teknolojileri Mühendislik (Turkey), and Paramount Group (South Africa), among others.

The global loitering munitions market is expected to reach USD 7.8 billion by 2036 from an estimated USD 2.4 billion in 2026, at a CAGR of 12.7% during the forecast period 2026 to 2036.

In 2026, the fixed-wing loitering munitions segment is expected to hold the largest share of the global loitering munitions market, driven by the aerodynamic efficiency of fixed-wing flight that provides the highest endurance-to-platform-weight ratios achievable with current propulsion technology and the operational primacy of endurance in the high-value strategic and operational strike applications that account for the largest share of market revenue.

The hybrid/VTOL loitering munitions segment is expected to register the highest CAGR during the forecast period 2026 to 2036, driven by the growing procurement preference of naval and special operations force customers for systems that eliminate launch infrastructure requirements while providing fixed-wing cruise flight endurance efficiency, and the progressive improvement in hybrid VTOL propulsion technology that is narrowing the endurance gap with pure fixed-wing designs.

In 2026, the EO/IR-based targeting segment is expected to hold the largest share of the global loitering munitions market, reflecting EO/IR guidance's position as the primary terminal guidance technology in the large majority of current loitering munitions platforms, providing the day-night, all-weather target imaging capability that enables operator target identification and engagement decision-making and supports the development of AI-based automatic target recognition capability.

The autonomous/AI-based targeting segment is expected to register the highest CAGR during the forecast period, driven by the maturation of machine learning target recognition algorithms from laboratory demonstration into operationally reliable capability, the procurement preference of advanced military customers for systems that reduce operator workload and enable faster engagement of time-sensitive targets, and the operational imperative of multi-loitering-munitions management in swarm employment scenarios.

Which region is expected to hold the largest share of the global loitering munitions market in 2026?

North America is expected to account for the largest share of the global loitering munitions market in 2026, driven by the United States' position as the world's largest defense spender, most technically advanced loitering munitions developer, and most active near-term procurer across Army, Marine Corps, Navy, and special operations force loitering munitions requirements.

Asia-Pacific is expected to register the highest growth rate in the global loitering munitions market during the forecast period 2026 to 2036, driven by India's large-scale defense modernization and loitering munitions procurement programs, Japan's historic defense spending increase creating new loitering munitions development and procurement programs, South Korea's urgent precision fires procurement in response to North Korean threats, and the loitering munitions capability investment of Australia, Taiwan, and multiple Southeast Asian nations.

The growth of this market is primarily driven by the operational validation of loitering munitions' precision strike effectiveness in recent high-profile conflicts including the Nagorno-Karabakh conflict and the Russia-Ukraine conflict, the broadly recognized capability gap awareness these conflicts have created across global military establishments, the rising demand for precision strike capability that minimizes collateral damage in both high-intensity and counter-insurgency operations, the cost competitiveness of loitering munitions relative to conventional guided missiles and manned aviation strike, the progressive integration of AI-based guidance that is expanding operational effectiveness and commercial addressability, and the broad and sustained increase in defense budgets across NATO member states and major Indo-Pacific defense spenders.

Key players are AeroVironment, Inc. (U.S.), UVision Air Ltd. (Israel), Elbit Systems Ltd. (Israel), Israel Aerospace Industries (Israel), Rheinmetall AG (Germany), Thales Group (France), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Leonardo S.p.A. (Italy), L3Harris Technologies, Inc. (U.S.), Saab AB (Sweden), ZALA Aero Group/Kalashnikov Concern (Russia), WB Group (Poland), STM — Savunma Teknolojileri Mühendislik (Turkey), and Paramount Group (South Africa), among others.

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates