Resources

About Us

Asset Performance Management Market Size, Share & Trends Analysis by Deployment Mode, Solution, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

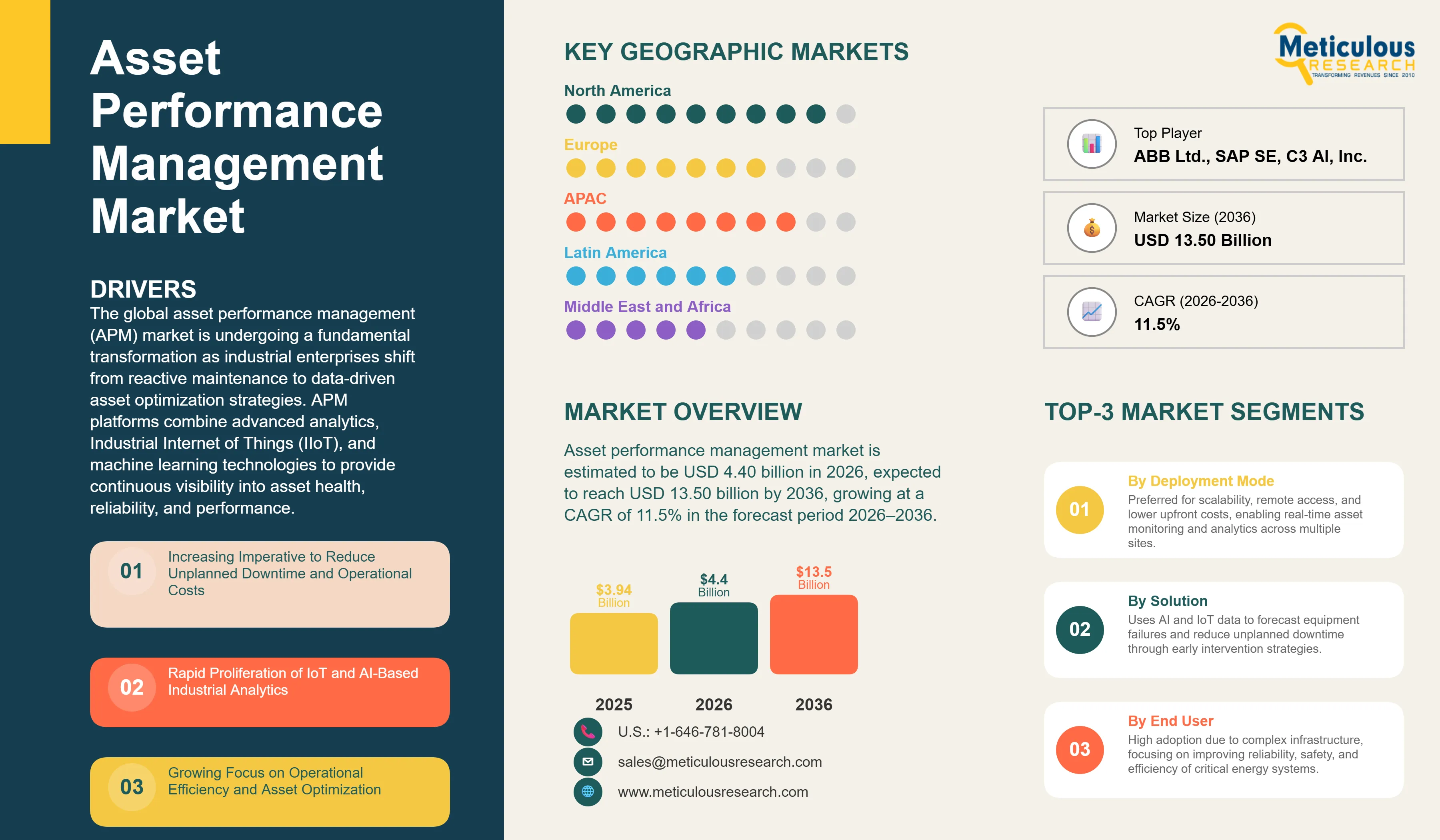

Report ID: MRICT - 1042060 Pages: 317 Jun-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe global asset performance management market is estimated to be USD 4.40 billion in 2026. This market is expected to reach USD 13.50 billion by 2036, growing at a CAGR of 11.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global asset performance management (APM) market is undergoing a fundamental transformation as industrial enterprises shift from reactive maintenance to data-driven asset optimization strategies. APM platforms combine advanced analytics, Industrial Internet of Things (IIoT), and machine learning technologies to provide continuous visibility into asset health, reliability, and performance. According to the International Energy Agency (IEA), industry accounts for nearly 40% of global final energy consumption, underscoring the importance of maximizing asset efficiency and reducing operational losses. In the United States, manufacturers represent approximately 71% of industrial electricity consumption, according to the U.S. Energy Information Administration (EIA), highlighting the need for intelligent asset management solutions to improve energy utilization and equipment effectiveness.

The market is being driven by the increasing complexity of industrial assets, the high cost of unexpected equipment failures, and the growing emphasis on sustainability and operational resilience. Industry studies indicate that unplanned downtime costs U.S. manufacturers nearly USD 50 billion annually, while Fortune Global 500 companies collectively lose about USD 1.4 trillion each year due to equipment-related disruptions. According to the International Society of Automation (ISA) and ARC Advisory Group, APM technologies are key enablers of Industry 4.0, facilitating convergence between operational technology (OT) and information technology (IT) and enabling predictive maintenance and asset optimization. As organizations seek greater resilience and longer asset lifecycles, APM adoption has become a strategic priority for achieving sustainable operational excellence.

Drivers: Enhancing Operational Efficiency and Asset Reliability through Digital Transformation

The growth of the global asset performance management market is primarily driven by the imperative to reduce operational risks and the increasing adoption of AI and IoT for industrial digitalization. Enterprises are increasingly recognizing that traditional maintenance strategies are insufficient for managing the complexities of modern industrial assets.

Increasing Imperative to Reduce Unplanned Downtime and Operational Costs

Unplanned downtime remains one of the most significant challenges for industrial enterprises, often resulting in millions of dollars in lost revenue and increased maintenance costs. APM solutions provide the predictive capabilities necessary to identify potential failures before they occur, allowing for proactive intervention. This shift from 'run-to-fail' to 'predict-and-prevent' strategies is a powerful driver for APM adoption, as companies seek to maximize asset availability and optimize their maintenance budgets in an increasingly competitive global landscape.

Rapid Proliferation of IoT and AI-Based Industrial Analytics

The convergence of low-cost IoT sensors and advanced AI algorithms has revolutionized asset monitoring. Industrial assets are now generating vast amounts of data that can be analyzed to gain deep insights into their performance and health. APM platforms leverage this data to create 'Digital Twins' of physical assets, allowing for real-time simulation and optimization. The ability to transform raw sensor data into actionable intelligence for reliability-centered maintenance is a major driver for the expansion of the APM market across diverse industrial sectors.

Restraints: Overcoming Data Silos and the Complexity of Legacy System Integration

Despite the clear benefits, the widespread adoption of APM is hindered by challenges related to data integration and the lack of a skilled workforce capable of managing advanced industrial analytics. Many organizations struggle with fragmented data landscapes and the complexities of connecting modern APM software with aging legacy equipment.

Challenges in Integrating APM with Fragmented Legacy Infrastructure

Many industrial plants operate with a mix of modern and legacy equipment, often with proprietary communication protocols. Integrating these disparate assets into a unified APM platform is a complex and costly endeavor. Data silos across different departments and the lack of standardized data models further complicate the realization of a truly enterprise-wide view of asset performance. This integration challenge often leads to localized, 'pilot' implementations that fail to scale, restraining the overall pace of APM market penetration.

Significant Skills Gap in Industrial Data Science and Reliability Engineering

The effective implementation of APM requires a unique blend of domain expertise in reliability engineering and advanced data science skills. However, there is a significant global shortage of professionals who can bridge these two disciplines. Organizations often find it difficult to find the talent necessary to build, deploy, and maintain the complex AI models that drive modern APM solutions. This skills gap can lead to underutilized platforms and a slower-than-expected ROI, deterring some organizations from making large-scale investments in APM technology.

Opportunities: Leveraging Digital Twins and ESG Mandates for Sustainable Asset Management

The future of the APM market lies in the integration of Digital Twin technology and the alignment of asset strategies with Environmental, Social, and Governance (ESG) goals. These trends offer the potential to create highly transparent, efficient, and sustainable industrial operations.

Advancements in High-Fidelity Digital Twins for Real-Time Optimization

Digital Twin technology is evolving from static models to high-fidelity, real-time representations of physical assets. By integrating real-time sensor data with physics-based simulations, Digital Twins allow for the continuous optimization of asset performance under varying conditions. This capability offers a significant opportunity for APM vendors to provide value-added services such as 'What-If' scenario analysis and autonomous performance tuning, particularly in complex industries like power generation and aerospace.

Rising Focus on ESG and Sustainable Industrial Asset Management

Global ESG mandates are pushing organizations to improve their energy efficiency and reduce their environmental footprint. APM solutions play a critical role in this by optimizing asset performance to reduce energy consumption and preventing hazardous leaks or failures. The integration of sustainability metrics into APM platforms offers a significant growth opportunity, as companies seek to demonstrate their commitment to responsible and efficient resource management through data-driven asset strategies.

Rapid Proliferation of APM-as-a-Service and Cloud-Native Platforms

A major trend in 2026 is the transition toward APM-as-a-Service (APMaaS) and cloud-native platforms. According to Eurostat, 45.2% of enterprises in the EU purchased cloud computing services in 2023, up from 38.9% in 2021, reflecting accelerating digital transformation. Meanwhile, the U.S. Census Bureau reported that more than half of manufacturing firms have adopted advanced digital technologies, including cloud-based analytics. Cloud-native APM platforms offer scalability, lower upfront investment, and continuous software updates, enabling rapid deployment across geographically dispersed assets. The International Society of Automation (ISA) identifies cloud-enabled predictive maintenance and asset analytics as key pillars of Industry 4.0, allowing even small and medium-sized enterprises to access capabilities that were previously limited to large industrial organizations. This shift is significantly accelerating the democratization of APM technologies.

Convergence of Edge Computing and Cloud Analytics for Real-Time Insights

To address latency, cybersecurity, and data sovereignty requirements, industrial organizations are increasingly combining edge computing with cloud analytics. According to the International Data Corporation (IDC), nearly 50% of new enterprise IT infrastructure deployments are expected to occur at the edge, while the International Energy Agency (IEA) estimates that industry accounts for almost 40% of global final energy consumption, increasing the need for real-time optimization of energy-intensive assets. In parallel, the U.S. National Institute of Standards and Technology (NIST) emphasizes edge architectures as a means to improve resilience and reduce response times in industrial control systems. This hybrid approach enables critical decisions to be executed near the asset while leveraging cloud platforms for historical analysis, fleet-wide benchmarking, and long-term asset optimization, thereby improving reliability and operational efficiency.

Analysis by Deployment Mode

Based on deployment mode, the cloud-based segment is expected to hold the largest share of the global asset performance management market in 2026. This dominance is driven by the increasing demand for high scalability, remote accessibility, and lower upfront capital expenditure. Cloud-based APM platforms allow for the seamless integration of AI and machine learning models across multiple sites, providing a unified view of asset health that is essential for global enterprises. However, the hybrid deployment segment is projected to register the highest CAGR during the forecast period. Many critical infrastructure and heavy industrial players are adopting hybrid models to balance the real-time processing needs of edge computing with the deep analytics capabilities of the cloud. This approach effectively addresses data sovereignty, security, and latency concerns while still providing the scalability and collaborative features of the cloud, making it the fastest-growing segment for complex industrial environments.

Analysis by Solution

By solution, the predictive maintenance segment is expected to hold the largest share in 2026. Predictive maintenance is the primary entry point for organizations embarking on their APM journey. The immediate and quantifiable ROI from reducing unplanned downtime and extending asset life through AI-driven failure prediction makes this the largest revenue-generating segment. However, the **asset integrity management segment** is projected to grow at the fastest CAGR during the forecast period. Increasing regulatory pressure on safety and environmental compliance, especially in the energy, chemical, and pharmaceutical sectors, is a major driver. The industry's shift toward long-term asset health monitoring and risk-based inspection strategies is accelerating the demand for advanced integrity management solutions that can ensure safe and sustainable operations over the entire asset lifecycle.

Analysis by End User

By end user, the **energy & utilities segment** is expected to hold the largest share in 2026. The extreme complexity and high value of assets in power generation, transmission, and water utilities make them the largest adopters of APM. The ongoing energy transition and the critical need to manage aging infrastructure while ensuring reliability are key drivers for extensive APM implementation in this sector. However, the **manufacturing segment** is projected to register the highest CAGR during the forecast period. The rapid adoption of Industry 4.0 and the digitalization of factory floors are creating a surge in demand for APM in manufacturing. The intense focus on maximizing OEE (Overall Equipment Effectiveness), reducing waste, and improving agility in highly competitive global markets is pushing manufacturers to adopt advanced APM solutions to gain a competitive edge.

Geographic Analysis: North American Leadership and Asia-Pacific's Rapid Expansion in Industrial APM

Largest Share: North America

North America is expected to dominate the global asset performance management market in 2026, holding a market share of approximately 40%. This leading position is attributed to the high concentration of technology-forward industrial players, the early adoption of IoT and AI-based reliability solutions, and stringent regulatory standards for asset safety. The region's focus on digital transformation in the energy and manufacturing sectors drives significant demand for advanced APM software. The key companies operating in the North America market are GE Vernova, IBM Corporation, Honeywell International Inc., and Aspen Technology (Emerson).

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global asset performance management market, with a CAGR of 13.8% during the forecast period. This rapid expansion is fueled by massive investments in infrastructure and industrial capacity in China, India, and Southeast Asia. The push for 'Smart Manufacturing' and the modernization of energy grids to improve operational efficiency and global competitiveness are driving the rapid adoption of APM solutions. The key companies operating in the Asia Pacific market are ABB Ltd., Siemens AG, and various regional technology integrators for global software providers.

The global asset performance management market is characterized by intense innovation and strategic consolidation. Key players are focusing on developing integrated, cloud-native platforms that can handle the scale and complexity of modern industrial data. Strategic partnerships between software vendors and industrial equipment manufacturers are common as they seek to provide 'pre-integrated' APM solutions. Furthermore, there is an increasing emphasis on the integration of AI and Digital Twins to provide autonomous performance optimization. The market is also seeing a surge in 'As-a-Service' models to lower the barriers to entry for smaller organizations and to provide continuous value through data-driven insights.

GE Vernova (GE Digital), AVEVA Group plc (Schneider Electric), IBM Corporation, SAP SE, Honeywell International Inc., Emerson Electric Co. (AspenTech), ABB Ltd., Siemens AG, Rockwell Automation, Inc., Baker Hughes Company (Bently Nevada), Bentley Systems, Incorporated, Oracle Corporation, Infor (Koch Industries), C3 AI, Inc., SymphonyAI, DNV, Hexagon AB, IFS AB, Uptake Technologies, Inc., Fluke Reliability

The global market is estimated at USD 4.40 billion in 2026, with a projected growth to USD 13.50 billion by 2036, at a CAGR of 11.5%.

Primary drivers include the increasing imperative to reduce unplanned downtime and the rapid proliferation of IoT and AI-based industrial analytics.

Major restraints include challenges in integrating with fragmented legacy infrastructure and a significant global skills gap in industrial data science.

Opportunities lie in the development of high-fidelity Digital Twins and the rising focus on ESG and sustainable asset management.

The cloud-based segment is expected to hold the largest share due to its high scalability and lower upfront capital expenditure.

The asset integrity management segment is projected to grow at the fastest CAGR, driven by increasing regulatory pressure on safety and environmental compliance.

The energy & utilities segment is expected to hold the largest share, necessitated by the management of complex and high-value critical infrastructure.

North America is expected to dominate the market due to its mature industrial digitalization landscape and early adoption of AI reliability solutions.

Asia Pacific is projected to witness the fastest growth, fueled by massive investments in smart manufacturing and infrastructure modernization.

Key trends include the rapid proliferation of APM-as-a-Service models and the convergence of edge computing and cloud analytics.

Published Date: Feb-2026

Published Date: Jun-2025

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates