Resources

About Us

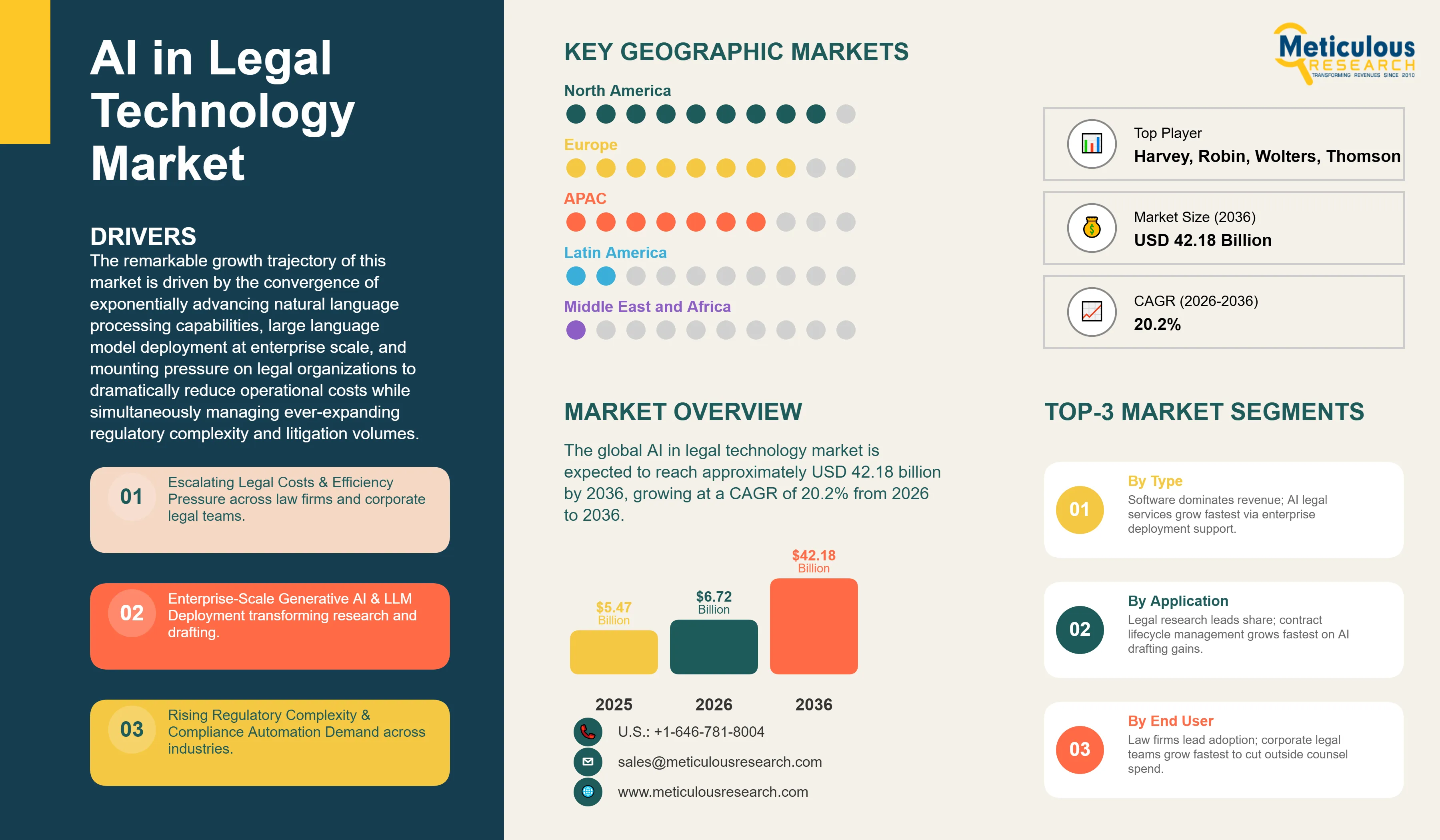

The global AI in legal technology market was valued at USD 5.47 billion in 2025. The market is expected to reach approximately USD 42.18 billion by 2036 from USD 6.72 billion in 2026, growing at a CAGR of 20.2% from 2026 to 2036. The remarkable growth trajectory of this market is driven by the convergence of exponentially advancing natural language processing capabilities, large language model deployment at enterprise scale, and mounting pressure on legal organizations to dramatically reduce operational costs while simultaneously managing ever-expanding regulatory complexity and litigation volumes. Traditional legal workflows — characterized by labor-intensive document review, manual contract drafting and analysis, and time-consuming legal research conducted through iterative database queries — are being fundamentally transformed by AI systems capable of processing millions of documents in hours, identifying relevant precedents across vast case law databases, and extracting critical clauses from complex agreements with accuracy rivaling senior associates. The integration of generative AI into legal practice represents the most significant technological disruption the legal industry has experienced, creating both substantial cost-reduction opportunities for legal buyers and existential competitive pressures for legal service providers failing to adapt their business models and workflow architecture to AI-augmented service delivery.

Click here to: Get Free Sample Pages of this Report

AI in legal technology encompasses a broad and rapidly evolving category of software solutions and services that apply artificial intelligence — particularly natural language processing, machine learning, computer vision, and large language models — to automate, augment, and enhance legal workflows across the full spectrum of legal practice. These solutions address the fundamental challenge of legal work: that it is inherently language-intensive, requiring comprehension of complex documents, identification of relevant patterns across vast textual corpora, and application of nuanced reasoning to specific factual circumstances. AI systems have demonstrated particular aptitude for tasks including contract review and analysis — identifying non-standard clauses, extracting key obligations and rights, flagging risk provisions — e-discovery document review classifying millions of records for relevance and privilege, legal research synthesizing case law and statutory authority across multiple jurisdictions, and compliance monitoring identifying regulatory changes affecting specific business operations.

The contemporary AI legal technology landscape is stratified across several distinct market segments serving different buyer needs and use cases. Enterprise contract lifecycle management platforms integrate AI-powered clause extraction, obligation tracking, and renewal management into comprehensive workflow systems managing thousands of agreements simultaneously. Legal research platforms leverage large language models and sophisticated retrieval-augmented generation architectures to provide contextual research assistance that moves beyond keyword-based database queries toward conversational research dialogue enabling attorneys to explore legal questions iteratively. E-discovery platforms deploy predictive coding, technology-assisted review, and conceptual clustering to dramatically reduce the human review burden in litigation and investigation matters. Regulatory compliance platforms monitor real-time regulatory changes across multiple jurisdictions, automatically identifying affected business processes and generating remediation guidance tailored to specific organizational contexts.

The arrival of foundation model-based generative AI — exemplified by large language models with legal domain fine-tuning — has fundamentally altered the competitive dynamics of the legal technology market, enabling rapid development of capable AI legal assistants by startups with smaller engineering teams while simultaneously creating performance benchmarks that legacy legal technology providers must urgently match. Established players including Thomson Reuters (Westlaw AI), LexisNexis (Lexis+ AI), and Wolters Kluwer (CCH AnswerConnect AI) are investing substantial resources in embedding generative AI capabilities throughout their existing product suites, while a vibrant startup ecosystem including Harvey AI, Robin AI, Spellbook, and Ironclad AI race to capture specific workflow niches with focused AI solutions. This competitive dynamic drives rapid capability advancement but creates evaluation complexity for legal buyers assessing AI tools against risk tolerance, accuracy requirements, and professional responsibility obligations governing attorney supervision of AI-generated legal work.

Generative AI Integration and Large Language Model Deployment Across Legal Workflows

The integration of large language models with legal domain expertise represents the defining trend reshaping the AI legal technology market, transforming AI tools from narrow task-specific applications toward comprehensive legal intelligence platforms capable of assisting with virtually any language-based legal task. Law firms including Allen & Overy, Dentons, and Paul Weiss have deployed custom LLM-based assistants trained on proprietary work product, enabling attorneys to leverage institutional knowledge accumulated over decades across practice groups and geographies. Corporate legal departments at major enterprises including Microsoft, JPMorgan Chase, and Goldman Sachs have implemented AI legal assistants reducing contract review time by 60-80% and enabling lean legal teams to manage substantially higher transaction volumes without proportionate headcount growth. The technical evolution toward retrieval-augmented generation architectures — combining parametric LLM knowledge with real-time retrieval from authoritative legal databases — addresses the critical challenge of hallucination in legal AI, ensuring responses are grounded in verified legal authority rather than confidently stated but potentially inaccurate generated content. This architecture enables AI legal tools to provide responses with proper citations to cases, statutes, and regulations, meeting the professional responsibility standards requiring attorneys to verify AI-generated legal research before relying upon it in client advice or court filings.

AI-Powered Contract Intelligence Driving Corporate Legal Department Transformation

Contract lifecycle management represents the highest-value AI legal technology application for corporate legal departments, where thousands of commercial agreements governing supplier relationships, customer commitments, licensing rights, and financing arrangements create massive administrative burden that traditional manual processes cannot efficiently manage. AI contract analytics platforms — led by vendors including Ironclad, ContractPodAi, Evisort, Kira Systems (now part of Litera), and Luminance — enable corporate legal teams to extract, standardize, and analyze contract data at scale, answering complex portfolio questions such as identifying all contracts with change-of-control provisions, most-favored-nation clauses, or automatic renewal dates within days rather than months of manual review. The economic proposition is compelling: organizations with thousands of contracts in portfolio can identify millions in revenue leakage from unfavorable terms, unpursued audit rights, and missed renewal opportunities that manual contract management systematically misses. Generative AI advances the capability further from extraction to drafting assistance — generating first drafts of standard commercial agreements, suggesting fallback positions for negotiated provisions based on historical negotiation outcomes, and identifying deviations from pre-approved playbooks requiring attorney escalation — creating AI-assisted contract workflows where attorneys focus on judgment and negotiation while AI handles routine drafting and review.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 42.18 Billion |

|

Market Size in 2026 |

USD 6.72 Billion |

|

Market Size in 2025 |

USD 5.47 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 20.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Application, Deployment, End-User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Escalating Legal Costs and Pressure for Operational Efficiency

The primary driver of AI legal technology adoption is the relentless economic pressure on legal organizations to deliver more legal work at lower cost without sacrificing quality or increasing risk. Corporate legal departments face constant pressure from CFOs to reduce outside counsel spend — which averages 0.5-1.0% of revenue for large corporations but can reach 3-5% for companies in regulated industries or active litigation — while simultaneously managing expanding regulatory obligations, increasing contract volumes driven by digital business model complexity, and heightened enforcement activity across financial services, healthcare, technology, and environmental sectors. Law firms face mirror-image pressure as sophisticated corporate clients leverage competitive intelligence from legal market benchmarking tools to demand pricing transparency, alternative fee arrangements, and demonstrable efficiency improvements. AI legal tools create compelling economic cases: technology-assisted review in e-discovery reduces document review costs by 50-80% compared to linear human review; AI contract review reduces attorney time per agreement by 40-60%; AI legal research tools cut research time by 30-50% while improving comprehensiveness. These efficiency gains translate directly to either margin improvement for law firms maintaining hourly billing or substantial fee reductions in fixed-fee and capped arrangements increasingly prevalent in sophisticated client relationships.

Opportunity: Regulatory Complexity and Compliance Automation

The explosive growth of global regulatory complexity — with major regulatory initiatives including GDPR, AI Act, Digital Markets Act, SEC climate disclosure rules, and expanding financial services regulations creating compliance obligations affecting virtually every significant enterprise — creates massive opportunity for AI-powered regulatory intelligence and compliance automation platforms. Organizations operating across multiple jurisdictions face the impossible task of monitoring thousands of regulatory changes annually across dozens of regulatory bodies using traditional manual processes, creating systematic compliance gaps and enforcement risk that AI monitoring platforms directly address. Thomson Reuters Regulatory Intelligence, Wolters Kluwer's OneSumX, and specialized regtech startups including Ascent RegTech, RegTek Solutions, and Continuity address this demand through AI platforms that ingest regulatory sources globally, extract obligations relevant to specific business activities, map requirements to internal controls and policies, and generate gap analysis identifying compliance deficiencies requiring remediation. The intersection of AI regulation specifically — with the EU AI Act, emerging US state AI legislation, and sector-specific AI governance requirements creating new compliance domains requiring AI-assisted compliance management — creates recursive demand where AI regulation drives demand for AI compliance tools, representing a particularly compelling growth vector for the regulatory technology segment of the AI legal technology market.

Why Does Software Dominate the AI Legal Technology Market?

The software segment commands approximately 68-72% of total AI legal technology market revenue in 2026, reflecting the platform economics of legal AI solutions where scalable software products generate recurring subscription revenue across large user bases without proportionate cost growth. AI legal software spans multiple distinct categories — standalone legal research tools, comprehensive contract lifecycle management suites, e-discovery platforms, compliance management systems, and emerging AI legal assistant products — each commanding substantial annual contract values from enterprise legal buyers. Leading software platforms including Thomson Reuters Westlaw AI, LexisNexis Lexis+ AI, and Relativity in e-discovery generate hundreds of millions in annual subscription revenue from large firm and corporate customer bases. The AI software segment benefits from network effects in training data: platforms with larger customer bases generate more usage data enabling continuous model improvement, creating compounding competitive advantages as leading platforms accumulate training signals unavailable to smaller competitors. The services segment — encompassing implementation services, training, custom model development, and legal process outsourcing leveraging AI tools — demonstrates the highest growth rate at approximately 22-25% CAGR, driven by enterprise demand for implementation support deploying complex AI platforms within existing legal workflows, change management services addressing attorney resistance to AI adoption, and custom AI development projects tailoring foundation models to specific practice area needs.

How Does Legal Research & Analytics Maintain Market Leadership?

The legal research & analytics segment represents approximately 28-32% of total AI legal technology market in 2026, reflecting both the historical maturity of AI-powered legal research tools — legal databases have incorporated machine learning and natural language search capabilities for over a decade — and the transformative impact of generative AI making research assistance conversational and comprehensive. Thomson Reuters and LexisNexis collectively serve the majority of US law firm legal research needs, with their AI-enhanced platforms enabling attorneys to ask complex legal questions in natural language and receive synthesized answers with comprehensive citation support across statutes, regulations, case law, and secondary sources. The contract management segment demonstrates the highest growth rate at 24-26% CAGR, driven by recognition that enterprise contract portfolios represent both significant risk exposure and substantial value creation opportunity when managed intelligently, combined with maturing AI contract analytics capabilities delivering demonstrable ROI. E-discovery AI maintains substantial market share given the significant per-matter cost savings it enables in commercial litigation, regulatory investigations, and internal compliance investigations where document review costs historically dominated total matter budgets. Compliance & regulatory management is the fastest-growing application segment outside contracts, reflecting escalating regulatory complexity creating sustained enterprise investment in AI-powered compliance infrastructure.

Why Does Cloud-Based Deployment Dominate?

Cloud-based deployment captures approximately 70-75% of the AI legal technology market in 2026, driven by the fundamental architectural requirements of modern AI systems — requiring massive compute resources for model inference, continuous retraining on updated legal data, and seamless software updates delivering improved AI capabilities without disruptive on-premise upgrade cycles. Leading AI legal platforms including Harvey AI, Ironclad, Evisort, and Luminance are cloud-native architectures that cannot be practically deployed on-premise without sacrificing core AI capabilities. The cloud deployment model also aligns with legal technology buying patterns, where mid-market law firms and corporate legal departments prefer subscription-based SaaS solutions with predictable per-user or per-matter pricing over substantial on-premise infrastructure investment requiring dedicated IT support. Security and data residency concerns have historically created cloud adoption friction in legal — where attorney-client privilege and work product doctrine create heightened sensitivity to data handling — but major cloud providers' investments in legal-sector compliance certifications, data residency options enabling processing within specific geographic boundaries, and enterprise agreement provisions explicitly addressing professional responsibility requirements have substantially mitigated these concerns for most legal organizations. On-premise deployment retains preference among the largest law firms, financial services in-house legal teams, and government legal organizations with classified matter handling requirements or jurisdiction-specific data sovereignty obligations preventing cloud processing.

How Do Law Firms Command Market Leadership?

Law firms account for approximately 45-50% of global AI legal technology market revenue in 2026, reflecting both their role as early technology adopters within the legal ecosystem and competitive pressure compelling AI investment to defend client relationships and maintain profitability under pricing pressure. Large law firms — the AmLaw 200 in the United States, Magic Circle and Silver Circle firms in the UK, and global elite firms with multi-jurisdictional practices — are investing tens of millions annually in AI infrastructure, including enterprise contracts with Thomson Reuters and LexisNexis for AI-enhanced research and drafting assistance, Harvey AI and similar generative AI platforms for broad workflow augmentation, and Relativity or Reveal for AI-powered e-discovery. Midsize law firms are adopting AI tools at accelerating rates as pricing becomes more accessible and competitive pressure from AI-equipped larger competitors creates urgency to close the efficiency gap. Corporate legal departments represent the fastest-growing end-user segment at approximately 22-24% CAGR, as general counsels recognize that AI tools enabling lean in-house teams to handle work previously sent to outside counsel deliver both cost savings and knowledge retention advantages. Government and courts represent an emerging segment with significant growth potential as court systems invest in AI-assisted case management, document processing, and public access portals, with notable investments in AI legal assistance tools by the US federal court system, UK Ministry of Justice, and several EU member state judicial systems.

How is North America Maintaining Market Leadership?

North America holds approximately 46-50% of the global AI legal technology market in 2026, anchored by the United States which represents the world's largest legal market with an estimated USD 350-400 billion in annual legal services expenditure. The concentration of technology innovation — both legal technology vendors and the AI research institutions driving foundational model development — in major US metropolitan areas creates a uniquely fertile ecosystem for AI legal technology commercialization. Silicon Valley and New York host the majority of well-funded AI legal startups, while established legal information companies including Thomson Reuters and LexisNexis operate their primary AI development centers in the US market. The US legal market's characteristics — large matters with high document volumes driving e-discovery demand, sophisticated in-house legal departments at major corporations actively investing in technology, and highly competitive law firm market creating differentiation pressure — create ideal conditions for AI legal technology adoption. Regulatory clarity from state bar ethics opinions addressing AI use in legal practice reduces adoption barriers for law firms concerned about professional responsibility compliance, with major state bars including California, New York, and Florida having issued guidance supporting AI use subject to attorney supervision requirements.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at 22-24% CAGR, propelled by China's rapidly expanding corporate legal market driven by M&A activity and international trade complexity, India's large English-common-law legal system with growing corporate legal department sophistication, and Southeast Asian economies experiencing rapid formalization and contract intensification of business relationships driving contract management demand. Japan and South Korea maintain advanced legal technology markets with domestic vendors serving local language legal research needs while internationally oriented practices adopt global AI legal platforms. China presents a distinctive market dynamic with domestic legal AI companies including iCourt, OpenLaw, and Legalzoom China developing AI legal tools specifically designed for Chinese law and language while international vendors face both market access challenges and data localization requirements limiting cloud service deployment. Australia and Singapore function as regional technology adoption leaders — particularly Singapore, where the government's active legal technology promotion through the Technology, Innovation and Law Practice (TILP) programme and Smart Nation legal technology initiatives have made the city-state a center for legal technology experimentation and deployment serving Southeast Asian markets broadly.

The leading companies shaping the global AI in legal technology market include Thomson Reuters Corporation (Westlaw AI, CoCounsel), RELX Group / LexisNexis (Lexis+ AI), Wolters Kluwer (ViaCounsel, ELM Solutions), and Relativity (Relativity AI, RelativityOne), which lead through established customer bases, proprietary legal data assets, and substantial AI R&D investment. Harvey AI, Robin AI, Ironclad, Evisort (now part of Workday), and Kira Systems (Litera) are capturing significant market share through purpose-built generative AI legal platforms offering superior user experience and rapid capability advancement compared to legacy incumbents. Emerging innovators including Luminance, ContractPodAi, Leya, CaseMark Systems, Spellbook, Darrow AI, and Casetext (acquired by Thomson Reuters) are advancing the competitive frontier through specialized AI capabilities in specific legal workflows — document review, arbitration analysis, litigation prediction, and regulatory compliance — while international players including ROSS Intelligence successors, Legal Robot, and region-specific players in European and Asian markets contribute to a highly dynamic and fragmented competitive landscape that is consolidating rapidly through both acquisition and organic platform expansion.

The global AI in legal technology market is expected to grow from USD 6.72 billion in 2026 to USD 42.18 billion by 2036.

The global AI in legal technology market is projected to grow at a CAGR of 20.2% from 2026 to 2036.

Software dominates representing 68-72% of revenue through scalable subscription platforms in legal research, contract management, and e-discovery. Services demonstrates the fastest growth at 22-25% CAGR driven by enterprise AI implementation support and custom model development demand.

Large language models enable conversational legal research with comprehensive citation support, AI-assisted contract drafting with playbook-based clause suggestions, automated document review with near-attorney accuracy, and generative compliance guidance synthesizing regulatory requirements — collectively shifting AI legal tools from task-specific automations to comprehensive legal intelligence platforms capable of augmenting the full spectrum of attorney workflows.

North America holds 46-50% of global market driven by the world's largest legal market, dense AI vendor ecosystem, and sophisticated enterprise legal buyers. Asia-Pacific demonstrates fastest growth at 22-24% CAGR propelled by expanding corporate legal markets in China and India and government-supported legal technology adoption in Singapore and Australia.

The leading companies include Thomson Reuters (Westlaw AI, CoCounsel), RELX Group/LexisNexis (Lexis+ AI), Wolters Kluwer, Relativity, Harvey AI, Robin AI, Ironclad, Evisort, Luminance, and ContractPodAi, with major technology companies including Microsoft (Copilot for Legal) and Google increasingly entering the market through AI platform integrations with legal workflow software.

1. Introduction

1.1 Market Definition

1.2 Market Scope

1.3 Research Methodology

1.4 Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3 Regulatory & Professional Responsibility Landscape for AI Legal Tools

3.4 Generative AI Impact & Large Language Model Evolution in Legal Practice

3.5 Porter's Five Forces Analysis

4. Global AI in Legal Technology Market, by Component

4.1 Introduction

4.2 Software

4.2.1 AI Legal Research Platforms

4.2.2 Contract Lifecycle Management Software

4.2.3 E-Discovery & Litigation Support Software

4.2.4 Compliance & Regulatory Management Software

4.3 Services

4.3.1 Implementation & Integration Services

4.3.2 Training & Change Management Services

4.3.3 Custom AI Development & Managed Services

5. Global AI in Legal Technology Market, by Application

5.1 Introduction

5.2 Legal Research & Analytics

5.2.1 Case Law & Statutory Research

5.2.2 Litigation Analytics & Outcome Prediction

5.3 Contract Management

5.3.1 AI Contract Review & Analysis

5.3.2 Contract Drafting & Negotiation Assistance

5.3.3 Contract Obligation & Renewal Management

5.4 E-Discovery

5.4.1 Technology-Assisted Review (TAR)

5.4.2 Predictive Coding & Conceptual Clustering

5.5 Compliance & Regulatory Management

5.5.1 Regulatory Change Monitoring

5.5.2 Compliance Gap Analysis & Remediation

5.6 Litigation Support

5.7 Intellectual Property Management

6. Global AI in Legal Technology Market, by Deployment

6.1 Introduction

6.2 Cloud-Based

6.2.1 Public Cloud

6.2.2 Private Cloud

6.2.3 Hybrid Cloud

6.3 On-Premise

7. Global AI in Legal Technology Market, by End-User

7.1 Introduction

7.2 Law Firms

7.2.1 Large Law Firms (AmLaw 200 / Global Elite)

7.2.2 Mid-Size Law Firms

7.2.3 Small & Solo Practices

7.3 Corporate Legal Departments

7.3.1 Fortune 500 In-House Legal Teams

7.3.2 Mid-Market Corporate Legal Departments

7.4 Government & Courts

7.4.1 Federal & National Government Legal Departments

7.4.2 Judiciary & Court Systems

7.5 Legal Process Outsourcing Firms

8. Global AI in Legal Technology Market, by Region

8.1 Introduction

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 U.K.

8.3.2 Germany

8.3.3 France

8.3.4 Netherlands

8.3.5 Rest of Europe

8.4 Asia-Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 Singapore

8.4.5 Australia

8.4.6 Rest of Asia-Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Rest of Latin America

8.6 Middle East & Africa

8.6.1 UAE

8.6.2 Saudi Arabia

8.6.3 South Africa

8.6.4 Rest of Middle East & Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Ranking/Positioning Analysis of Key Players, 2025

10. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1 Thomson Reuters Corporation (Westlaw AI / CoCounsel)

10.2 RELX Group / LexisNexis (Lexis+ AI)

10.3 Wolters Kluwer (ViaCounsel, ELM Solutions)

10.4 Relativity (RelativityOne)

10.5 Harvey AI

10.6 Robin AI

10.7 Ironclad

10.8 Luminance

10.9 ContractPodAi

10.10 Evisort (Workday)

10.11 Litera / Kira Systems

10.12 Casetext (Thomson Reuters)

10.13 Spellbook (Rally Legal)

10.14 Darrow AI

10.15 CaseMark Systems

11. Appendix

11.1 Questionnaire

11.2 Related Reports

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Aug-2025

Published Date: Apr-2025

Subscribe to get the latest industry updates