Resources

About Us

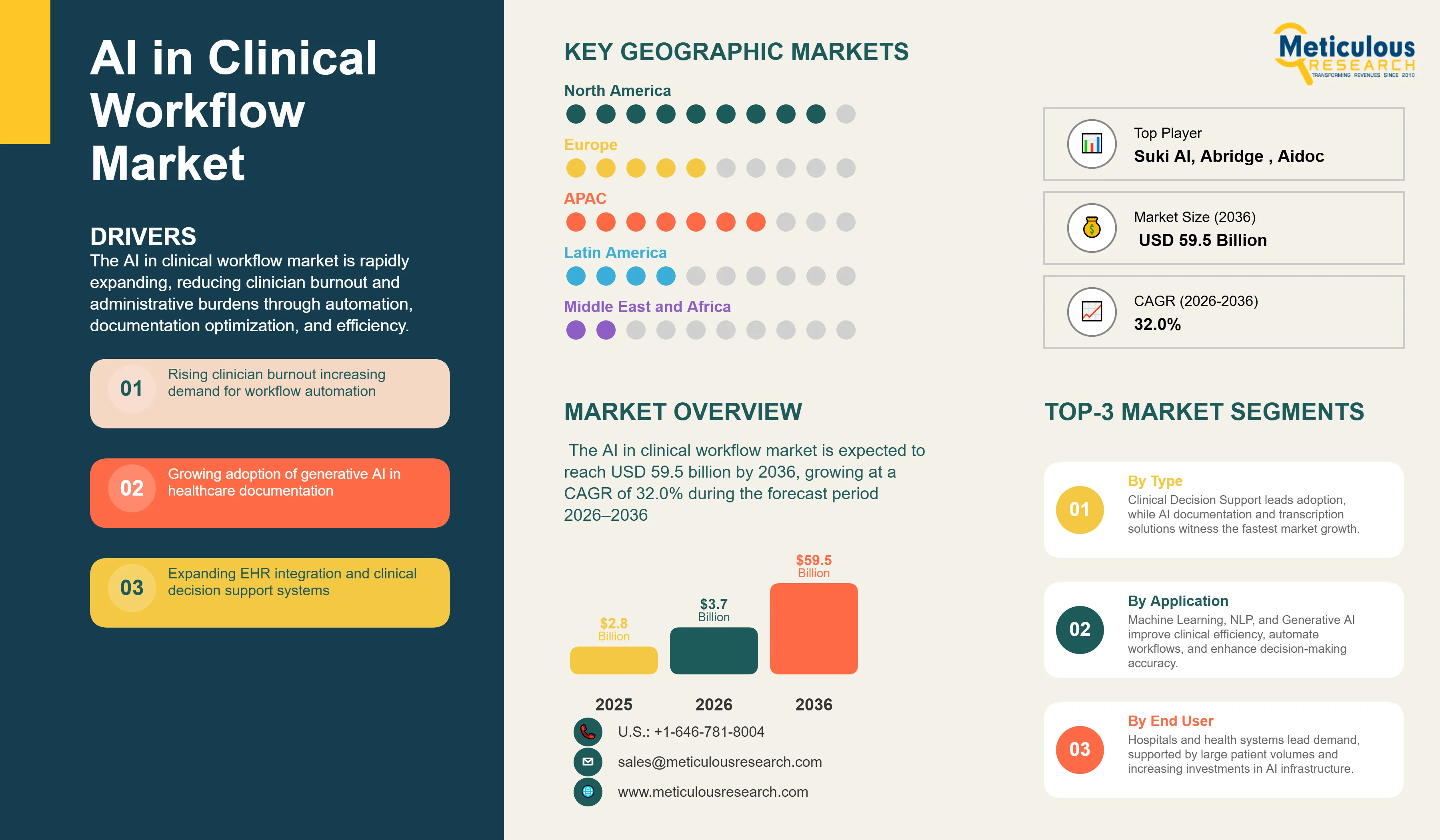

The global AI in clinical workflow market was valued at USD 3.7 billion in 2026. This market is expected to reach USD 59.5 billion by 2036, growing at a CAGR of 32.0% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global AI in clinical workflow market is entering a phase of exponential expansion, redefining the operational and clinical standards of modern healthcare delivery. At its core, this market addresses the growing crisis of clinician burnout and systemic inefficiencies across healthcare systems. According to the American Medical Association (AMA), approximately 45% of physicians report at least one symptom of burnout, while studies indicate that clinicians spend nearly two hours on documentation and administrative activities for every hour of direct patient care. The widespread adoption of electronic health records (EHRs) has intensified administrative workloads, creating significant demand for AI-driven workflow automation. Artificial intelligence, particularly advances in Generative AI and Natural Language Processing (NLP), is emerging as a transformative solution by automating documentation, streamlining administrative tasks, enhancing diagnostic accuracy, and improving patient throughput.

The integration of AI into clinical workflows is no longer a peripheral innovation but a fundamental necessity for sustainable healthcare. The market's growth is fueled by the rapid adoption of ambient clinical intelligence, which uses AI to listen to patient-clinician encounters and automatically generate structured medical notes. Clinical studies have shown that these tools can reduce documentation time by as much as 50-70%, directly translating into more patient-facing time and improved quality of care. Furthermore, the rise of AI-powered Clinical Decision Support (CDS) systems is enabling personalized medicine at scale, providing clinicians with real-time, evidence-based recommendations for diagnosis and treatment planning based on massive datasets that exceed human cognitive capacity.

The technological ecosystem of the AI in clinical workflow market is characterized by a convergence of Big Tech players and specialized healthcare AI startups. Companies like Microsoft (through Nuance), Google Health, and NVIDIA are providing the foundational infrastructure and large language models (LLMs) specifically tuned for medical terminology. Simultaneously, a vibrant startup ecosystem is developing point solutions for administrative automation, such as prior authorization, patient scheduling, and revenue cycle management (RCM). These solutions are increasingly being integrated directly into major EHR platforms like Epic and Cerner, creating a seamless user experience that minimizes disruption to established clinical routines.

Geographically, North America remains the primary revenue driver, accounting for a significant portion of the global market share. This dominance is due to the early adoption of digital health technologies in the U.S., a robust regulatory framework for AI-enabled medical devices, and a high concentration of leading AI research institutions. However, the Asia-Pacific region is projected to witness the fastest growth, with countries like China and India investing heavily in AI to overcome shortages in clinical staff and improve healthcare access for their massive populations. As clinical AI continues to demonstrate a clear Return on Investment (ROI)—with some hospitals reporting a 15-20% increase in operational efficiency—the market is poised for sustained, long-term growth across all global regions.

The primary driver for the AI in clinical workflow market is the urgent need to mitigate clinician burnout and address growing healthcare workforce shortages. According to the World Health Organization (WHO), the world is projected to face a shortage of approximately 10 million healthcare workers by 2030, with the greatest gaps occurring in low- and middle-income countries. Simultaneously, physicians spend nearly two hours on administrative and documentation activities for every one hour of direct patient care, contributing significantly to burnout and reduced productivity. According to the American Medical Association (AMA), approximately 45% of physicians report at least one symptom of burnout, highlighting the need for workflow automation solutions.

Furthermore, the rapid advancement in Generative AI and Large Language Models (LLMs) has made medical transcription and summarization significantly more accurate and reliable. The rising volume and complexity of healthcare data also necessitate the use of AI to synthesize information and provide actionable insights at the point of care, improving both clinical outcomes and operational efficiency.

Data privacy and security concerns remain significant restraints for the market. Managing sensitive patient information in cloud-based AI systems requires stringent compliance with regulations like HIPAA in the U.S. and GDPR in Europe, which can be complex and costly for providers. Furthermore, interoperability challenges between AI solutions and legacy EHR systems can hinder seamless integration and slow down adoption. The potential for algorithmic bias and the 'black box' nature of some deep learning models also raise concerns regarding transparency and clinical accountability.

Significant opportunities exist in the development of AI agents for comprehensive patient navigation and population health management. These agents can automate the entire patient journey, from initial triage and scheduling to post-discharge follow-up and remote monitoring. Additionally, the use of predictive analytics to identify high-risk patients before they require hospitalization presents a major opportunity for value-based care organizations. The expansion of AI into under-resourced regions, where it can serve as a force multiplier for limited clinical staff, also offers high growth potential.

A critical challenge is navigating the evolving regulatory landscape for clinical AI. As AI models become more autonomous, regulatory bodies like the FDA are developing new frameworks for continuous monitoring and post-market surveillance. Ensuring the fairness and explainability of AI algorithms to gain physician trust is also a persistent challenge. Furthermore, the high cost of implementing and maintaining advanced AI infrastructure may limit adoption in smaller medical practices and community hospitals, potentially widening the digital divide in healthcare.

The most prominent trend in the market is the shift toward Generative AI-powered ambient clinical intelligence. Unlike traditional dictation tools, these systems can understand the context of a conversation and automatically populate the correct sections of a medical note. This trend is significantly reducing the 'cognitive load' on clinicians and is being rapidly integrated into mobile and wearable devices for hands-free documentation, making it one of the most sought-after technologies in healthcare today.

There is a growing trend toward using AI to automate the 'back-office' of healthcare, including prior authorization, medical coding, and claim denial management. By applying NLP and predictive modeling to administrative workflows, health systems can significantly reduce overhead costs and improve revenue capture. This trend is attracting substantial investment from both venture capital and major technology firms looking to provide a comprehensive 'healthcare operating system'.

Based on solution type, the market is segmented into Clinical Documentation & Transcription, Clinical Decision Support (CDS), Administrative Workflow, and Patient Management. In 2026, the Clinical Decision Support (CDS) segment is expected to hold the largest share of the market. This dominance is due to the established use of AI for diagnostic image analysis, drug interaction alerts, and treatment planning across major medical specialties like radiology and oncology.

The Clinical Documentation & Transcription segment is projected to register the fastest CAGR during the forecast period. This growth is driven by the explosive demand for ambient clinical intelligence to combat clinician burnout. The ability of Generative AI to accurately summarize complex patient encounters in real-time is a 'game-changer' for healthcare providers, leading to rapid and widespread adoption.

Based on specialty, the market is segmented into Radiology, Cardiology, Oncology, Pathology, and Primary Care & Internal Medicine. In 2026, the Radiology segment is expected to hold the largest share of the market. Radiology was the first specialty to broadly adopt AI for automated image interpretation and workflow prioritization. The high volume of diagnostic imaging data makes it an ideal environment for AI-driven optimization.

The Primary Care segment is projected to witness the fastest growth during the forecast period. Primary care clinicians face the highest administrative burden and the greatest volume of patient interactions. AI solutions that can streamline documentation, triage, and routine patient communication offer immense value in this setting, driving rapid market expansion.

North America is expected to hold the largest share of the global AI in clinical workflow market in 2026, driven by a robust digital health ecosystem and high adoption of AI in the United States. The region accounts for a significant portion of the global share, supported by the presence of major technology firms and a favorable regulatory environment for AI-enabled medical software. Key companies operating in the North American market include Microsoft (Nuance), Google Health, and Epic Systems.

Asia-Pacific is projected to witness the fastest growth during the forecast period. Countries like China and India are investing heavily in healthcare AI to address shortages in clinical staff and improve care delivery for their large populations. The rapid expansion of digital health infrastructure and a rising number of AI startups in the region present significant opportunities for growth. Key companies operating in the Asia-Pacific market include Philips Healthcare, Siemens Healthineers, and various emerging domestic AI providers.

The global AI in clinical workflow market is highly competitive and characterized by a convergence of Big Tech and specialized healthcare AI firms. Microsoft, through its acquisition of Nuance Communications, is a dominant player in clinical documentation. Google and NVIDIA are providing the foundational infrastructure and advanced models that power many third-party AI solutions. Competition is focused on model accuracy, seamless EHR integration, and the ability to demonstrate a clear ROI in terms of clinician time savings and improved operational efficiency.

Strategic partnerships between AI vendors and major EHR providers are a key competitive advantage, as they ensure that AI tools are available directly within the clinician's existing workflow. Clinical validation and FDA clearances also play a critical role in market positioning, particularly for diagnostic and decision support tools. Key players in the global AI in clinical workflow market include Microsoft Corporation (Nuance), NVIDIA Corporation, Google Health, Amazon Web Services (AWS), Oracle Corporation (Cerner), Epic Systems Corporation, Philips Healthcare, GE HealthCare, and Siemens Healthineers.

The market is projected to reach USD 59.5 billion by 2036, growing at a CAGR of 32.0% from 2026 to 2036.

Clinical Decision Support (CDS) is expected to hold the largest share in 2026 due to its established use in diagnostics.

The urgent need to mitigate clinician burnout and the rapid advancement in Generative AI are the primary drivers.

Primary Care is expected to grow the fastest due to its high administrative burden and patient volume.

It automatically generates structured medical notes from patient encounters, reducing documentation time by 50-70%.

Asia-Pacific is projected to witness the highest CAGR due to massive investments in digital health infrastructure.

Generative AI powers advanced medical transcription, automated summaries, and personalized patient communication.

Data privacy concerns, interoperability challenges, and regulatory hurdles are the main restraints.

ROI is measured through time savings for clinicians, increased operational efficiency, and reduced claim denials.

The market is led by Microsoft (Nuance), NVIDIA, Google Health, AWS, and major EHR providers like Epic and Oracle.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Solution Type

3.2.2. Market Analysis, by Technology

3.2.3. Market Analysis, by Specialty

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Urgent Need to Mitigate Clinician Burnout (Stats: >40% Burnout Rate)

4.2.1.2. Rapid Advancement in Generative AI and Ambient Clinical Intelligence

4.2.1.3. Rising Volume and Complexity of Healthcare Data

4.2.2. Restraints

4.2.2.1. Data Privacy and Security Concerns (HIPAA/GDPR Compliance)

4.2.2.2. Interoperability Challenges with Legacy EHR Systems

4.2.3. Opportunities

4.2.3.1. AI Agents for Comprehensive Patient Navigation and Population Health

4.2.3.2. Predictive Analytics for Early Intervention and Value-Based Care

4.2.4. Challenges

4.2.4.1. Navigating the Evolving Regulatory Landscape for Clinical AI

4.2.4.2. Ensuring Algorithmic Fairness and Physician Trust

4.2.5. Trends

4.2.5.1. Shift Toward Software-Defined, AI-First Clinical Workflows

4.2.5.2. Rise of Real-Time AI-Guided Diagnostic and Administrative Optimization

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global AI in Clinical Workflow Market, by Solution Type

5.1. Overview

5.2. Clinical Documentation & Transcription

5.2.1. Ambient Clinical Intelligence

5.2.2. AI Voice Assistants

5.3. Clinical Decision Support (CDS)

5.3.1. Diagnostic AI

5.3.2. Treatment Planning

5.4. Administrative Workflow

5.4.1. Prior Authorization Automation

5.4.2. Revenue Cycle Management (RCM) Automation

5.5. Patient Management

5.5.1. Triage & Virtual Assistants

5.5.2. Remote Patient Monitoring (RPM) AI

6. Global AI in Clinical Workflow Market, by Technology

6.1. Overview

6.2. Machine Learning & Deep Learning

6.3. Natural Language Processing (NLP)

6.4. Generative AI (LLMs)

6.5. Computer Vision

7. Global AI in Clinical Workflow Market, by Specialty

7.1. Overview

7.2. Radiology

7.3. Cardiology

7.4. Oncology

7.5. Pathology

7.6. Primary Care & Internal Medicine

8. Global AI in Clinical Workflow Market, by End User

8.1. Overview

8.2. Hospitals & Health Systems

8.3. Ambulatory Surgical Centers (ASCs)

8.4. Specialty Clinics & Physician Practices

8.5. Payer Organizations

9. Global AI in Clinical Workflow Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S. (Stats: Leading AI adoption market)

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China (Stats: Massive healthcare AI investment)

9.4.2. Japan

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Microsoft Corporation (Nuance Communications)

11.2. NVIDIA Corporation

11.3. Google Health (Alphabet Inc.)

11.4. Amazon Web Services (AWS)

11.5. Oracle Corporation (Cerner)

11.6. Epic Systems Corporation

11.7. Philips Healthcare

11.8. GE HealthCare

11.9. Siemens Healthineers

11.10. IBM Corporation (Merative)

11.11. Abridge

11.12. Suki AI

11.13. Innovaccer Inc.

11.14. AKASA

11.15. CodaMetrix

11.16. Aidoc

12. Appendix

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates