Resources

About Us

Ultra-Fast EV Charging Market Size, Share & Trends Analysis by Charger Power Output (150-250 kW, 250-350 kW), Charger Type, Connector Type, Vehicle Type, Application, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

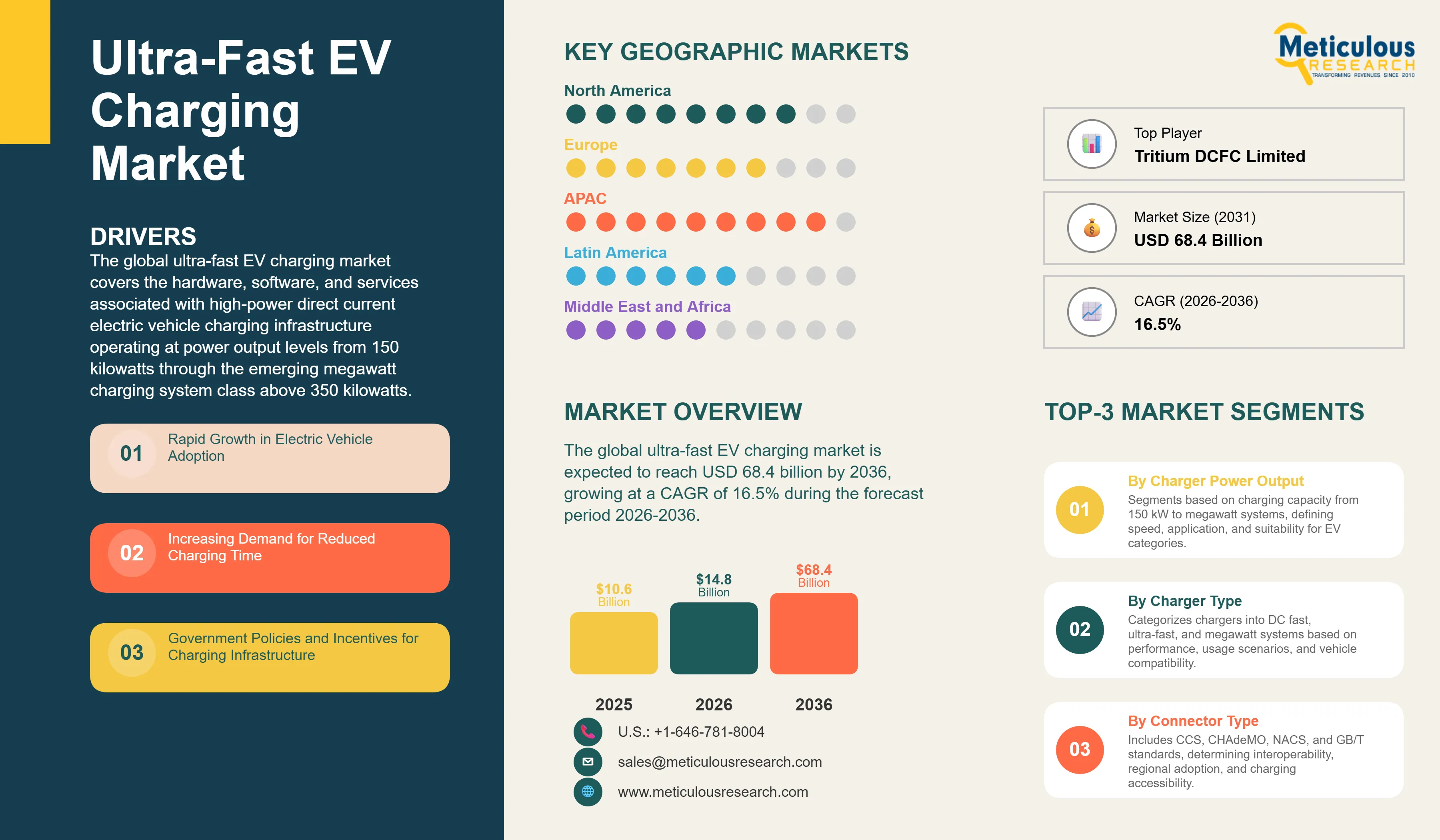

Report ID: MRAUTO - 1041899 Pages: 282 Apr-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global ultra-fast EV charging market was valued at USD 10.6 billion in 2025. This market is expected to reach USD 68.4 billion by 2036 from an estimated USD 14.8 billion in 2026, growing at a CAGR of 16.5% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global ultra-fast EV charging market covers the hardware, software, and services associated with high-power direct current electric vehicle charging infrastructure operating at power output levels from 150 kilowatts through the emerging megawatt charging system class above 350 kilowatts. This encompasses ultra-fast DC charging stations and columns, the power electronics including rectifiers and converters that deliver controlled high-current charging power to vehicles, charging network management software platforms, grid integration and demand management systems, and the installation, operations, and maintenance services that support ultra-fast charging infrastructure deployment across public highway corridor locations, urban charging hubs, fleet depot charging facilities, and commercial semi-public charging destinations.

The growth of the global ultra-fast EV charging market is primarily driven by the rapid global expansion of electric vehicle adoption across passenger and commercial vehicle segments, which is creating strong consumer and operator demand for charging infrastructure that can deliver meaningful charge restoration in 10 to 20 minutes rather than the 30 to 60 minutes required by first-generation DC fast chargers, addressing the range anxiety and charging time inconvenience that remain the primary barriers to broader EV adoption among consumers accustomed to 5-minute refueling experiences. Government infrastructure investment programs including the U.S. National Electric Vehicle Infrastructure program providing USD 5 billion for charging corridor deployment, the EU's Alternative Fuels Infrastructure Regulation mandating ultra-fast charging stations at defined highway intervals, and equivalent national programs in China, the UK, and major EV markets are providing the public funding and regulatory mandates that are translating market demand into large-scale funded deployment programs.

Two significant opportunities are shaping the market's long-term trajectory. The development and commercial deployment of megawatt charging systems targeting heavy-duty electric truck charging at power levels of 1 to 3.75 megawatts represents the highest-growth frontier of the ultra-fast charging market, as the electrification of freight trucking creates charging power requirements an order of magnitude larger than passenger vehicle charging and demands specialized MCS infrastructure at truck stops, distribution centers, and freight corridors. The integration of ultra-fast charging stations with co-located battery energy storage systems, enabling high-power charging at locations with limited grid connection capacity by buffering energy from the grid and releasing it during peak charging sessions, represents a critical technical and commercial opportunity that is enabling ultra-fast charging deployment at highway locations where grid upgrade costs would otherwise make rapid charging deployment economically unviable.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 68.4 Billion |

|

Market Size in 2026 |

USD 14.8 Billion |

|

Market Size in 2025 |

USD 10.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 16.5% |

|

Dominating Charger Power Output |

150 kW-250 kW |

|

Fastest Growing Charger Power Output |

Above 350 kW (MCS) |

|

Dominating Charger Type |

DC Fast Chargers |

|

Fastest Growing Charger Type |

Megawatt Charging Systems (MCS) |

|

Dominating Connector Type |

CCS (Combined Charging System) |

|

Fastest Growing Connector Type |

Tesla/NACS |

|

Dominating Installation Type |

Public Charging Stations |

|

Fastest Growing Installation Type |

Private/Fleet Charging |

|

Dominating Vehicle Type |

Passenger Vehicles |

|

Fastest Growing Vehicle Type |

Electric Trucks |

|

Dominating Application |

Highway/Intercity Charging |

|

Fastest Growing Application |

Fleet Charging |

|

Dominating End User |

Individual EV Owners |

|

Fastest Growing End User |

Fleet Operators |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Emergence of Megawatt Charging Systems for Heavy-Duty Electrification

The development and commercial rollout of megawatt charging system infrastructure for heavy-duty electric trucks and buses represents the most consequential emerging trend in the ultra-fast EV charging market, creating a new and very large charging power segment that dwarfs the power levels of passenger vehicle ultra-fast charging and requires fundamentally different infrastructure architecture, grid connection capacity, and site design than existing charging stations. The CharIN Megawatt Charging System standard, defining charging communication protocols and connector specifications for power levels from 600 kilowatts to 3.75 megawatts, has been adopted by major truck OEMs including Daimler Truck, Volvo Trucks, Traton Group, PACCAR, and Navistar as the universal MCS charging standard, creating the interoperability foundation required for the commercial rollout of MCS infrastructure at scale. ABB, Siemens, and a growing ecosystem of charging infrastructure specialists are developing MCS charger hardware validated to the CharIN standard, with early commercial installations at highway truck stops, distribution center parking areas, and port facilities where heavy-duty electric vehicle charging demand is first concentrating.

The commercial urgency of MCS deployment is created by the progressive entry of electric heavy-duty trucks into fleet operations at companies including Amazon, UPS, Walmart, DHL, and major European freight carriers that have committed to electric truck adoption timelines and require depot and highway charging infrastructure capable of restoring operational range within mandatory driver rest period windows of 30 to 45 minutes. A Class 8 electric truck with a 1,000 kilowatt-hour battery pack requires 45 minutes of MCS charging at 1.2 megawatts to achieve 400 kilometers of restored range, representing a technically and commercially demanding charging requirement that only MCS infrastructure can satisfy within operationally acceptable time constraints. The intersection of regulatory zero-emission truck mandates in California, the EU, and other jurisdictions with commercial fleet electrification commitments is creating a defined and time-constrained demand for MCS infrastructure that is driving accelerated investment from charging network operators, truck OEMs, and logistics operators.

NACS Standardization and Connector Ecosystem Consolidation

The rapid emergence of the North American Charging Standard developed by Tesla as the dominant connector standard in the North American market, following the decisions of Ford, General Motors, Honda, Nissan, Toyota, Volvo, and other major OEMs to adopt NACS connectors on their U.S. and Canadian market vehicles, is driving a significant realignment of the North American ultra-fast charging infrastructure landscape. SAE International's adoption of NACS as the SAE J3400 standard in 2023, combined with the major charging network operators including Electrify America, EVgo, ChargePoint, Blink, and BP Pulse announcing NACS adapter availability and hardware upgrade programs for their DC fast charger networks, is creating a progressively converged North American charging connector ecosystem that simplifies the EV charging experience for consumers and operators while driving substantial hardware investment in station upgrades and new installations.

The NACS standardization dynamic represents a significant commercial opportunity for charger hardware manufacturers and charging network operators, as the large installed base of CCS1-equipped DC fast chargers at North American charging networks requires either hardware replacement or NACS adapter retrofitting to serve the growing fleet of NACS-equipped EVs entering the market. ChargePoint, EVgo, and Electrify America have announced multi-year hardware upgrade programs to equip their charging stations with NACS ports alongside CCS1, representing hundreds of millions of dollars in hardware procurement that is benefiting charger manufacturers including ABB, Tritium, Delta Electronics, Alpitronic, and Kempower whose NACS-capable hardware is qualifying for network operator procurement programs. The SAE J3400 standardization additionally creates a pathway for NACS adoption outside North America as an alternative or complementary standard to CCS2 in markets currently served by the European CCS standard.

Integration of Energy Storage and Smart Charging at Highway Locations

The co-location of battery energy storage systems with ultra-fast charging stations is transitioning from a niche solution for grid-constrained locations toward a mainstream infrastructure architecture that is enabling charging network operators to deploy high-power charging at highway locations, commercial real estate sites, and urban charging hubs where the cost of grid upgrades to support peak ultra-fast charging demand would otherwise make economically viable rapid charging deployment impossible. A 6-stall ultra-fast charging hub with 350 kilowatt chargers draws up to 2.1 megawatts at peak simultaneous utilization, requiring grid transformer upgrades and distribution network reinforcement that can add USD 500,000 to USD 2 million or more to site development costs at locations with limited existing grid capacity. Co-located battery storage systems of 500 kilowatt-hours to 2 megawatt-hours charged slowly from existing grid connections and discharged during peak charging sessions can eliminate or substantially reduce grid upgrade requirements, reducing site development cost and accelerating deployment timelines.

Tesla's V3 Supercharger stations increasingly incorporate on-site battery storage, and ABB, Siemens, and Schneider Electric are offering integrated charging plus storage system solutions targeting highway charging hub applications. The economic case for storage integration is further strengthened in electricity markets with time-of-use pricing, where storage enables charging network operators to shift energy purchase to off-peak hours and reduce peak demand charges that otherwise represent a significant operating cost element for high-utilization fast charging locations. The integration of solar photovoltaic generation with charging plus storage at large charging hub sites creates fully renewable-powered charging operations that satisfy EV operator sustainability requirements and can qualify for additional government incentives available for clean energy infrastructure in multiple major markets.

Rapid Growth in Electric Vehicle Adoption

The primary driver of the global ultra-fast EV charging market is the extraordinary pace of global electric vehicle adoption that is generating rapidly growing demand for convenient, fast, and widely distributed public charging infrastructure capable of supporting the long-distance and frequent travel patterns of an expanding EV-owning population. Global EV sales exceeded 17 million units in 2024 and are projected to continue growing strongly toward 40 to 50 million annual sales by 2030, building a cumulative global EV fleet that will require charging infrastructure investment several orders of magnitude larger than what currently exists. The transition from EV ownership being dominated by home-charging-capable consumers with dedicated private parking toward broader adoption by apartment dwellers, urban residents, and frequent long-distance travelers who depend on public charging creates a structural demand shift toward higher-power public charging infrastructure that can provide the speed and convenience of refueling equivalent that these consumers require for EV ownership to be practical.

Government Policies and Incentives for Charging Infrastructure

The comprehensive government policy and funding frameworks being implemented across major EV markets to accelerate charging infrastructure deployment are transforming ultra-fast charging from a commercially driven voluntary investment into a partially grant-funded infrastructure buildout with defined coverage and performance targets that are mandating rapid network expansion. The U.S. NEVI Formula Program provides USD 5 billion over five years specifically for ultra-fast charging stations at maximum 50-mile intervals along designated alternative fuel corridors, with minimum 150 kilowatt per port and 4 ports per station specifications that align directly with the ultra-fast charging market's power output range. The EU's AFIR regulation mandates ultra-fast charging with minimum 150 kilowatt aggregate power at major motorway service areas by 2025 and progressive coverage expansion through the decade, creating binding deployment obligations for EU member states. China's New Energy Vehicle charging infrastructure development plans mandate rapid expansion of fast charging coverage in both urban and highway locations, with the State Grid Corporation of China and private charging operators executing large-scale deployment programs under national guidance.

Development of Megawatt Charging Systems (MCS)

The commercial development and infrastructure rollout of megawatt charging systems for heavy-duty electric vehicles represents the largest single growth opportunity in the ultra-fast EV charging market over the forecast period, creating a new charging power tier with average selling prices, infrastructure complexity, and revenue potential per installation substantially exceeding current ultra-fast passenger vehicle charger deployments. An MCS installation at a major truck stop providing 4 to 8 charging bays at 1 to 2 megawatts per bay requires grid connection and distribution infrastructure investment in the range of USD 1 to 5 million per site, representing a per-location capital intensity several times that of passenger vehicle ultra-fast charging hubs and creating a very high-value market segment for infrastructure developers, equipment manufacturers, and charging network operators who establish positions in this emerging category. The global heavy-duty truck fleet, comprising approximately 25 million Class 6 to 8 trucks in major markets, represents a progressively electrifying asset base that will require MCS charging infrastructure at hundreds of thousands of freight corridors, distribution centers, and terminal locations globally through the forecast period.

Growth in Fleet Electrification

The accelerating electrification of commercial vehicle fleets across logistics, public transit, municipal, and corporate transportation represents a large and fast-growing demand source for ultra-fast and megawatt charging infrastructure at fleet depot, workplace, and route charging locations. Fleet operators including Amazon, UPS, FedEx, DHL, and major public transit agencies are deploying electric vehicles at scale against defined electrification timelines, each requiring dedicated high-power charging infrastructure at their operating bases that generates concentrated and high-utilization charging load representing the most economically attractive commercial charging market for infrastructure operators. Fleet charging generates more predictable, higher-utilization revenue streams than public highway charging, where utilization rates can be variable and location-dependent, making fleet charging contracts an important revenue stability element for charging infrastructure operators and investors. The Charging-as-a-Service business model, in which charging network operators finance and operate fleet charging infrastructure at customer sites in exchange for long-term energy service contracts, is gaining commercial traction as a capital-efficient pathway for fleet operators to access high-power charging without upfront infrastructure investment.

By Charger Power Output: In 2026, the 150 kW-250 kW Segment to Dominate

Based on charger power output, the global ultra-fast EV charging market is segmented into 150 kW to 250 kW, 250 kW to 350 kW, and above 350 kW (megawatt charging systems). In 2026, the 150 kW to 250 kW segment is expected to account for the largest share of the global ultra-fast EV charging market. The large share of this segment is attributed to the 150 to 250 kilowatt power range representing the dominant power output specification for the current generation of ultra-fast charging station deployments across NEVI-funded U.S. highway corridor programs, EU AFIR-compliant motorway service area installations, and the commercial charging hub rollouts of leading network operators including Electrify America, EVgo, Shell Recharge, and BP Pulse. This power range is compatible with the onboard charging acceptance capability of the majority of current generation battery electric passenger vehicles, which typically support peak AC or DC charging rates of 150 to 250 kilowatts, making it the optimal power delivery specification for current vehicle technology.

However, the above 350 kW (megawatt charging systems) segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the advancing commercial deployment of heavy-duty electric trucks requiring MCS charging infrastructure, the adoption of the CharIN MCS standard by major truck OEMs creating the interoperability foundation for commercial MCS rollout, and the progressively increasing onboard charging acceptance capability of next-generation passenger EVs targeting 400 to 800 kilowatt acceptance rates that will expand the addressable vehicle population for above-350 kilowatt charging infrastructure.

By Charger Type: In 2026, DC Fast Chargers to Hold the Largest Share

Based on charger type, the global ultra-fast EV charging market is segmented into DC fast chargers, ultra-fast DC chargers, and megawatt charging systems. In 2026, the DC fast chargers segment is expected to account for the largest share of the global ultra-fast EV charging market. The dominance of DC fast chargers reflects the very large installed base of DC fast charging infrastructure globally that has been built over the past decade at power levels from 50 to 150 kilowatts and is now being supplemented by the upgraded ultra-fast charging products that most major charger manufacturers are deploying as replacements and additions to their existing installations. The broad compatibility of DC fast chargers with the full range of DC-charging-capable EVs across CCS, CHAdeMO, and NACS connector formats makes this charger category the most universally accessible option across the global EV fleet.

However, the megawatt charging systems segment is projected to register the highest CAGR during the forecast period, driven by the emergence of MCS as a commercially deployed product category enabled by the CharIN standard finalization and the entry of heavy-duty electric trucks into commercial fleet operations requiring MCS charging capability.

By Connector Type: In 2026, CCS to Hold the Largest Share

Based on connector type, the global ultra-fast EV charging market is segmented into Combined Charging System (CCS), CHAdeMO, Tesla/NACS, and GB/T. In 2026, the CCS segment is expected to account for the largest share of the global ultra-fast EV charging market. CCS encompasses both the CCS1 variant used in North America and the CCS2 variant used in Europe and increasingly in other global markets, making it collectively the most widely deployed DC fast charging connector standard globally with the largest installed base of compatible charging infrastructure and the broadest vehicle compatibility across European and North American OEM EV product portfolios. The EU's regulatory endorsement of CCS2 as the mandatory charging standard for European markets and the adoption of CCS by the majority of European and non-Tesla North American EV manufacturers has made CCS the global standard of record for DC fast charging outside China.

However, the Tesla/NACS segment is projected to register the highest CAGR during the forecast period. This growth is driven by the unprecedented wave of North American OEM NACS adoption following Ford and GM's announcements in 2023, the SAE J3400 standardization of NACS, the major charging network hardware upgrade programs to add NACS ports, and Tesla's massive and growing Supercharger network opening to all NACS-compatible vehicles, collectively creating the fastest connector standard transition in EV charging history.

By Installation Type: In 2026, Public Charging Stations to Hold the Largest Share

Based on installation type, the global ultra-fast EV charging market is segmented into public charging stations, semi-public charging (commercial and workplace), and private and fleet charging. In 2026, the public charging stations segment is expected to account for the largest share of the global ultra-fast EV charging market. Public highway corridor and urban charging hub installations represent the primary deployment environment for ultra-fast charging infrastructure, as the high-power delivery that ultra-fast chargers provide is most commercially valuable at public locations serving drivers who need rapid charge restoration during long-distance journeys or in time-constrained urban charging situations. The large and well-funded public charging deployment programs of Electrify America, EVgo, Tesla Supercharger, Shell Recharge, BP Pulse, and government-backed charging network operators across Europe and China are executing the majority of current ultra-fast charger installations as public infrastructure.

However, the private and fleet charging segment is projected to register the highest CAGR during the forecast period, driven by the accelerating deployment of high-power depot and workplace charging at fleet operator facilities, the growth of MCS infrastructure at freight terminals and distribution centers, and the Charging-as-a-Service business model expansion enabling more fleet operators to access dedicated ultra-fast charging infrastructure.

By Vehicle Type: In 2026, Passenger Vehicles to Hold the Largest Share

Based on vehicle type, the global ultra-fast EV charging market is segmented into passenger vehicles, commercial vehicles, electric buses, and electric trucks. In 2026, the passenger vehicles segment is expected to account for the largest share of the global ultra-fast EV charging market. Passenger EVs represent the largest and most established segment of the global electric vehicle fleet and the primary user base for the existing installed base of ultra-fast charging infrastructure at public highway and urban locations. The very large and rapidly growing global passenger EV fleet, driven by the commercial success of Tesla, BYD, Volkswagen Group EV models, and the expanding EV portfolios of virtually all major automotive OEMs, generates the greatest aggregate ultra-fast charging demand and revenue among all vehicle type segments.

However, the electric trucks segment is projected to register the highest CAGR during the forecast period. This growth is driven by the progressive entry of Class 6 to 8 electric trucks into commercial fleet operations from Tesla Semi, Daimler Truck's eCascadia and eActros, Volvo FH Electric, and other commercial EV platforms requiring MCS infrastructure at power levels orders of magnitude above passenger vehicle charging, and the very high per-session energy delivery of heavy-duty truck charging that generates substantially higher revenue per charging event than passenger vehicle sessions.

By Application: In 2026, Highway/Intercity Charging to Hold the Largest Share

Based on application, the global ultra-fast EV charging market is segmented into highway/intercity charging, urban charging, fleet charging, and depot charging. In 2026, the highway/intercity charging segment is expected to account for the largest share of the global ultra-fast EV charging market. Highway and intercity corridor charging represents the highest-priority public ultra-fast charging deployment category, as it addresses the range anxiety that most directly constrains long-distance EV travel and represents the application where rapid charging time is most commercially valuable relative to alternative DC fast charging power levels. The NEVI program in the U.S., the AFIR mandate in the EU, and equivalent national corridor charging programs in China, Japan, South Korea, and Australia are all specifically targeting highway corridor ultra-fast charging deployment as the primary funded infrastructure category, making this application the leading driver of government-funded ultra-fast charger installations globally.

However, the fleet charging segment is projected to register the highest CAGR during the forecast period, driven by the accelerating electrification of logistics, transit, and commercial vehicle fleets creating concentrated high-power charging demand at depot and operational base locations, and the favorable commercial economics of fleet charging contracts that generate predictable, high-utilization revenue streams for infrastructure operators.

By End User: In 2026, Individual EV Owners to Hold the Largest Share

Based on end user, the global ultra-fast EV charging market is segmented into individual EV owners, fleet operators, commercial establishments, and government and municipal authorities. In 2026, the individual EV owners segment is expected to account for the largest share of the global ultra-fast EV charging market. Individual EV drivers using public highway and urban ultra-fast charging stations represent the largest aggregate revenue source for charging network operators, as the growing population of EV owners without home charging access or requiring range extension for long-distance travel generates the majority of public charging session volume. The pay-per-use pricing model that dominates public charging generates per-session revenue from individual EV owners that constitutes the primary commercial revenue stream for network operators including Tesla Supercharger, Electrify America, EVgo, and Shell Recharge.

However, the fleet operators segment is projected to register the highest CAGR during the forecast period, driven by the large and growing commercial vehicle fleet electrification programs generating concentrated high-power depot and operational charging demand, the higher per-session energy volumes and favorable contract revenue economics of fleet charging relationships, and the rapid expansion of CaaS business models that are converting fleet electrification infrastructure from capital purchase to service contract revenue streams.

Ultra-Fast EV Charging Market by Region: Asia-Pacific Leading by Share, North America by Growth

Based on geography, the global ultra-fast EV charging market is segmented into Asia-Pacific, Europe, North America, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global ultra-fast EV charging market. The largest share of this region is mainly due to China's dominant position as the world's largest EV market and the world's largest installed base of public EV charging infrastructure, with over 3 million public charging points including a large and rapidly growing ultra-fast DC charging network operated by State Grid, Southern Power Grid, TGOOD, Star Charge, and NIO's Power network. China's national EV charging infrastructure development plans, combined with the extraordinary pace of domestic EV adoption driven by BYD, SAIC, NIO, XPeng, Li Auto, and Huawei-backed Aito, are generating the largest single-country ultra-fast charging deployment program globally. South Korea's rapid EV adoption and advanced charging technology ecosystem anchored by companies including Hyundai Kia's charger subsidiary and SK Signet, Japan's highway ultra-fast charger network expansion driven by Toyota and Nissan EV adoption, and India's rapidly developing national EV charging framework under FAME II and successor programs collectively contribute to Asia-Pacific's dominant regional position.

However, the North American ultra-fast EV charging market is expected to grow at the fastest CAGR during the forecast period. North America's rapid growth is driven by the NEVI program's USD 5 billion commitment to national EV charging corridor infrastructure creating the largest single government charging infrastructure investment program in U.S. history, the NACS connector standard consolidation creating a significantly simplified and more commercially viable charging ecosystem that is accelerating both consumer EV adoption and infrastructure investment, and the large-scale proprietary charging network expansions of Tesla, Electrify America, EVgo, ChargePoint, and Blink that are collectively deploying thousands of ultra-fast charging stalls annually across the U.S. and Canada. The emergence of MCS heavy-duty truck charging as a commercial product category is expected to contribute disproportionately to North American market growth, as the U.S. freight corridor and distribution center infrastructure represents one of the highest-priority global deployment environments for MCS charging technology given the advanced state of electric heavy-duty truck adoption in California and the growing federal mandates for zero-emission trucking.

Europe represents an advanced and rapidly developing ultra-fast EV charging market, anchored by the AFIR regulation's mandatory coverage targets, the advanced state of ultra-fast charger deployment by Ionity, Fastned, Allego, Shell Recharge, and BP Pulse across major European motorway networks, and the leading EV adoption rates of Norway, the Netherlands, Sweden, and Germany that are generating the highest public charging utilization rates of any regional market globally. European charger hardware manufacturers including Alpitronic, ABB, Kempower, and Siemens are also significant market participants contributing to the regional market's technology leadership position.

The global ultra-fast EV charging market is moderately fragmented across charger hardware manufacturers, charging network operators, and integrated players that develop both hardware and operate networks. Competition is focused on charger power output and reliability, network coverage and convenience, software platform capability, charging speed and session experience, and the ability to deliver large-scale deployment programs for government and commercial customers within defined timelines and cost structures.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, network coverage, geographic presence, and key strategic developments. Some of the key players operating in the global ultra-fast EV charging market include ABB Ltd. (Switzerland), Siemens AG (Germany), Tesla Inc. (U.S.), ChargePoint Holdings Inc. (U.S.), EVgo Inc. (U.S.), Electrify America LLC (U.S.), Shell Recharge Solutions (Netherlands), BP Pulse (U.K.), Tritium DCFC Limited (Australia/U.S.), Delta Electronics Inc. (Taiwan), Blink Charging Co. (U.S.), Alpitronic GmbH (Italy), Kempower Oyj (Finland), NIO Inc. (China), and Schneider Electric SE (France), among others.

The global ultra-fast EV charging market is expected to reach USD 68.4 billion by 2036 from an estimated USD 14.8 billion in 2026, at a CAGR of 16.5% during the forecast period 2026-2036.

In 2026, the 150 kW-250 kW segment is expected to hold the largest share of the global ultra-fast EV charging market, reflecting this power range's alignment with current-generation EV onboard charging capability and its specification in major government-funded charging corridor programs.

The above 350 kW (megawatt charging systems) segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the commercial deployment of MCS infrastructure for heavy-duty electric trucks and the advancing onboard charging acceptance capability of next-generation EVs.

In 2026, the CCS segment is expected to hold the largest share of the global ultra-fast EV charging market, reflecting CCS1 and CCS2's combined position as the most widely deployed DC fast charging connector standard across European and North American markets.

In 2026, the highway/intercity charging segment is expected to hold the largest share of the global ultra-fast EV charging market, driven by highway corridor deployment programs under NEVI in the U.S. and AFIR in Europe and the concentration of ultra-fast charging investment at long-distance travel charging locations.

The growth of this market is primarily driven by the rapid global expansion of EV adoption creating strong consumer demand for faster and more convenient public charging infrastructure, and the comprehensive government infrastructure investment programs including the U.S. NEVI program and EU AFIR regulation providing funded mandates for national ultra-fast charging network deployment at highway and urban locations.

Key players are ABB Ltd. (Switzerland), Siemens AG (Germany), Tesla Inc. (U.S.), ChargePoint Holdings Inc. (U.S.), EVgo Inc. (U.S.), Electrify America LLC (U.S.), Shell Recharge Solutions (Netherlands), BP Pulse (U.K.), Tritium DCFC Limited (Australia/U.S.), Delta Electronics Inc. (Taiwan), Blink Charging Co. (U.S.), Alpitronic GmbH (Italy), Kempower Oyj (Finland), NIO Inc. (China), and Schneider Electric SE (France), among others.

North America is expected to register the highest growth rate in the global ultra-fast EV charging market during the forecast period 2026-2036, driven by the NEVI program's USD 5 billion charging corridor deployment mandate, the NACS connector ecosystem consolidation simplifying the charging landscape, and the emergence of MCS heavy-duty truck charging as a major new infrastructure investment category in U.S. freight corridors.

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Oct-2025

Published Date: Sep-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates