Resources

About Us

Spatial Biology Market Size, Share & Trends Analysis by Product (Instruments, Consumables, Software, Services), Technology (Spatial Transcriptomics, Spatial Proteomics, Spatial Genomics), Application, End User, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

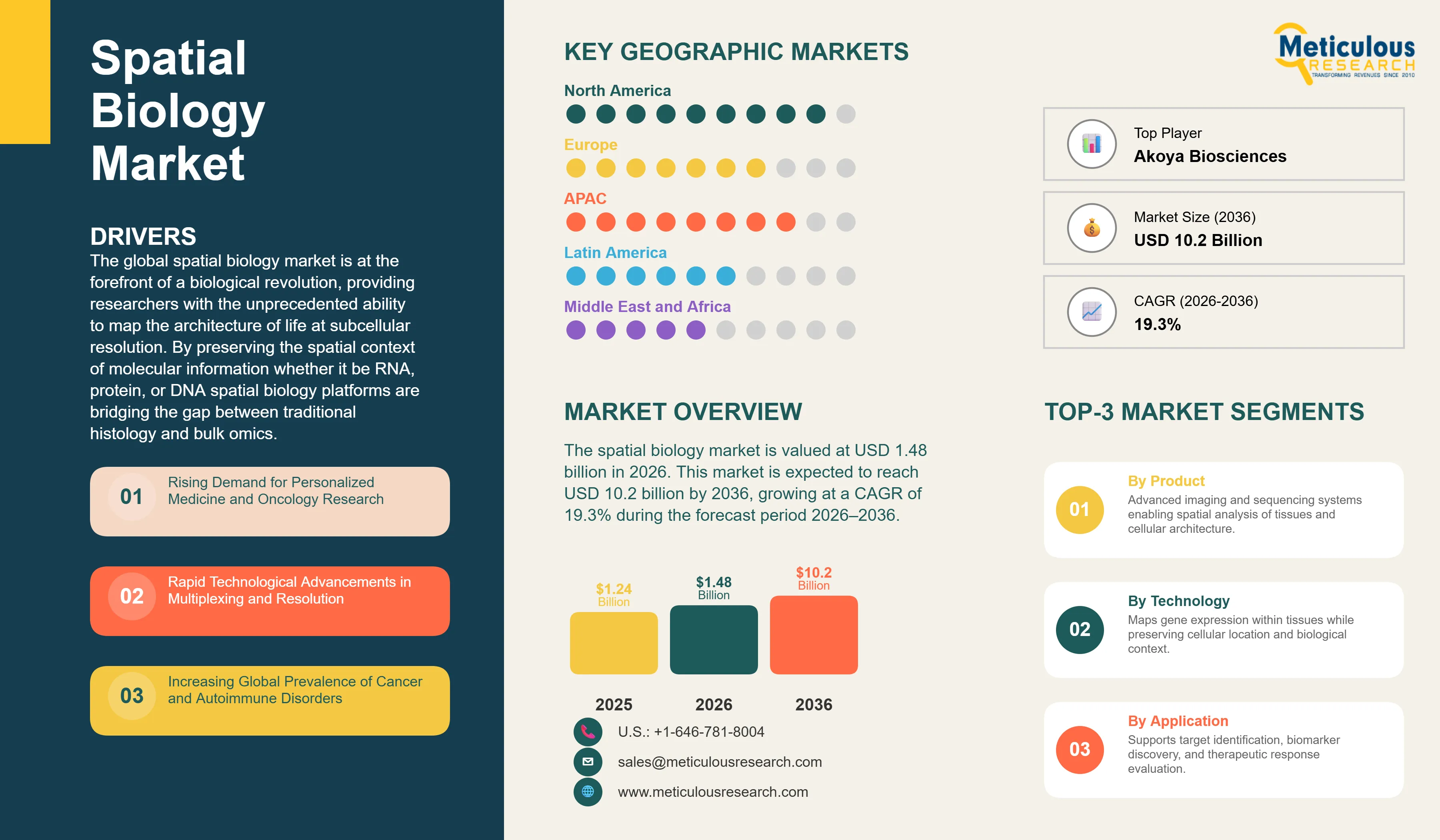

Report ID: MRHC - 1042031 Pages: 286 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global spatial biology market is valued at USD 1.48 billion in 2026. This market is expected to reach USD 10.2 billion by 2036, growing at a CAGR of 19.3% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global spatial biology market is at the forefront of a biological revolution, providing researchers with the unprecedented ability to map the architecture of life at subcellular resolution. By preserving the spatial context of molecular information whether it be RNA, protein, or DNA spatial biology platforms are bridging the gap between traditional histology and bulk omics. This market's rapid expansion is a direct result of the realization that 'where' a molecule is located within a tissue is just as important as 'what' it is. This spatial context is critical for understanding complex biological systems, such as the tumor microenvironment, where the proximity of immune cells to cancer cells can determine the success or failure of immunotherapy.

The growth of the spatial biology market is primarily driven by the increasing demand for precision medicine and the rising burden of chronic diseases, particularly cancer. Oncology remains the leading application area, supported by the growing use of spatial biology technologies for tumor microenvironment characterization, biomarker discovery, and immuno-oncology research. Scientific adoption has accelerated significantly over the past decade, with a substantial increase in peer-reviewed publications related to spatial transcriptomics, spatial proteomics, and multi-omics research. In parallel, public funding agencies, including the National Institutes of Health (NIH), have expanded investments in spatial biology through programs such as the Human BioMolecular Atlas Program (HuBMAP), Human Tumor Atlas Network (HTAN), and Cancer Moonshot initiatives, supporting continued technology innovation and market growth.

The spatial biology ecosystem is characterized by rapid technological innovation and a high degree of strategic consolidation. Leading players are increasingly moving toward 'multi-omic' platforms that can simultaneously detect hundreds of RNA targets and dozens of proteins in a single tissue section. The market is also witnessing a shift from 'Research Use Only' (RUO) toward clinical diagnostics, as spatial biomarkers begin to enter clinical trials for patient stratification. However, the complexity of data analysis remains a significant challenge, driving a surge in the development of AI-powered spatial informatics and cloud-based visualization tools. As these platforms become more standardized and user-friendly, the global spatial biology market is poised for sustained, long-term growth across both research and clinical sectors.

Geographically, North America is expected to maintain its leadership position in the global spatial biology market, accounting for approximately 42% of total revenue in 2026. The region's dominance is supported by the presence of leading spatial biology technology providers, substantial funding from the National Institutes of Health (NIH), advanced research infrastructure, and significant pharmaceutical and biotechnology R&D investments. Asia-Pacific is projected to register the fastest growth during the forecast period, driven by expanding genomics and multi-omics research activities, increasing healthcare expenditures, and growing investments in precision medicine initiatives across China, Japan, South Korea, and Singapore. Furthermore, the global cancer burden is expected to rise substantially, with new cancer cases projected to reach approximately 28.4 million by 2040, creating sustained demand for advanced spatial biology technologies in translational research, drug development, and precision medicine applications.

The primary driver for the spatial biology market is the critical need for deeper biological insights in personalized medicine and oncology. As bulk sequencing fails to capture the heterogeneity of tissues, spatial biology provides the necessary resolution to identify patient-specific biomarkers. Furthermore, rapid technological advancements in multiplexing and resolution have made it possible to detect hundreds of targets in a single section. The increasing global prevalence of cancer and autoimmune disorders is also a major catalyst, as researchers strive to understand disease mechanisms and develop more effective therapies.

The high cost of spatial biology instruments and consumables remains a significant restraint, limiting adoption to well-funded academic centers and large pharmaceutical companies. Furthermore, the complexity of the data generated—often terabytes of imaging and sequencing information—requires specialized bioinformatics expertise that is currently in short supply. There are also concerns regarding the lack of standardization in sample preparation and data output across different platforms, which can lead to variability in research results and hinder the transition to clinical diagnostics.

Significant opportunities exist in the transition of spatial biology from research to clinical diagnostics. As spatial biomarkers demonstrate their predictive value in clinical trials, the development of IVD-certified platforms will open a massive new market. The integration of AI and machine learning for automated image analysis and data interpretation also presents a major growth path. Additionally, the expansion of spatial biology into non-oncology areas, such as neuroscience and infectious diseases, offers high potential for market expansion. The development of more affordable, benchtop spatial systems could also democratize the technology for smaller labs.

A critical challenge for spatial biology providers is the preservation of tissue integrity during complex sample preparation and staining procedures. Maintaining spatial relationships while achieving high signal-to-noise ratios is technically demanding. Furthermore, ensuring the interoperability of spatial data with other omics datasets is a persistent challenge. As the market scales, vendors must also address the computational burden of storing and processing massive spatial datasets. Overcoming the regulatory hurdles for clinical validation and achieving reimbursement for spatial diagnostic tests are also significant long-term challenges.

The most significant trend in the spatial biology market is the rapid shift toward spatial multi-omics platforms capable of simultaneously analyzing RNA, proteins, DNA, and other molecular markers within the same tissue section. This evolution is being accelerated by large-scale research initiatives such as the NIH's Human BioMolecular Atlas Program (HuBMAP), which is focused on mapping the spatial organization of cells across human tissues using advanced multi-omics technologies. The growing adoption of spatial transcriptomics and proteomics in oncology, neuroscience, and immunology research is driving demand for integrated workflows that provide a more comprehensive understanding of cellular function, tissue architecture, and disease biology.

A parallel trend is the increasing integration of artificial intelligence (AI) and machine learning into spatial biology data analysis. As high-plex imaging and spatial omics platforms generate increasingly complex datasets, researchers are adopting AI-enabled tools for automated image segmentation, cell classification, spatial neighborhood mapping, and biomarker discovery. Recent advances in computational spatial transcriptomics and graph-based analytical models are enabling more accurate interpretation of tissue-level biological interactions while reducing analysis time. The growing use of AI in biomedical research and drug development is expected to further strengthen the role of spatial informatics as a critical component of next-generation precision medicine workflows.

Based on product, the market is segmented into Instruments, Consumables, Software, and Services. In 2026, the Consumables segment is expected to hold the largest share of the market. The high recurring revenue from reagent kits, staining panels, and flow cells drives the dominance of this segment. As the installed base of spatial instruments grows and the volume of samples increases, the value of the consumables market continues to expand.

The Software & Data Analysis segment is projected to register the fastest CAGR during the forecast period. This growth is driven by the massive influx of spatial data and the critical need for AI-driven visualization and informatics tools to interpret complex biological patterns.

Based on technology, the market is segmented into Spatial Transcriptomics, Spatial Proteomics, and Spatial Genomics. In 2026, the Spatial Transcriptomics segment is expected to hold the largest share of the market. This technology offers the most comprehensive view of gene expression and has been the primary focus of early spatial biology adoption, particularly in oncology research.

The Spatial Multi-omics segment (often categorized within transcriptomics or proteomics) is projected to witness the fastest growth. The demand for simultaneous detection of multiple molecular classes to understand functional biology is driving the rapid adoption of multi-omic platforms.

North America is expected to hold the largest share of the global spatial biology market in 2026, driven by a high concentration of leading spatial biology vendors and robust research funding from the NIH. The region accounts for approximately 42% of the global share, supported by a mature biotechnology sector and early adoption by major pharmaceutical companies. Key companies operating in the North American market include 10x Genomics, Akoya Biosciences, and Bruker.

Asia-Pacific is projected to witness the fastest growth during the forecast period. Countries like China and Japan are aggressively investing in genomics and precision medicine initiatives. The rising number of spatial biology research centers and the growing focus on oncology research in the region present significant opportunities for market expansion. Key companies operating in the Asia-Pacific market include BGI Group, MGI Tech, and local biotechnology providers.

The global spatial biology market is highly competitive and is characterized by a mix of established genomics companies and specialized spatial startups. 10x Genomics and Akoya Biosciences are current market leaders, but the landscape is rapidly shifting due to strategic acquisitions. Bruker's acquisition of NanoString and Canopy Biosciences has made it a major player, while Bio-Techne's acquisition of Lunaphore has strengthened its spatial proteomics portfolio.

Strategic consolidation and the move toward 'all-in-one' multi-omic platforms are the primary growth strategies. Companies are increasingly focusing on subcellular resolution, high multiplexing, and automated workflows to differentiate their offerings. Evidence of clinical utility and the development of diagnostic partnerships are also critical for long-term market positioning. Key players in the global spatial biology market include 10x Genomics, Bruker (NanoString), Akoya Biosciences, Standard BioTools, Vizgen, Bio-Techne, Danaher (Leica), Illumina, Resolve Biosciences, and Lunaphore.

The market is projected to reach USD 10.2 billion by 2036, growing at a CAGR of 19.3% from 2026 to 2036.

The Consumables segment is expected to hold the largest share in 2026 due to high recurring reagent revenue.

Oncology research is the largest application area for spatial biology, driven by growing demand for tumor microenvironment analysis, biomarker discovery, immuno-oncology studies, and precision medicine research.

Spatial Multi-omics is expected to grow the fastest as researchers demand simultaneous RNA and protein detection.

The market is expected to grow at a CAGR of 19.3% during the forecast period 2026–2036.

North America holds the largest share, accounting for approximately 42% of the global market in 2026.

The high cost of instruments and the complexity of spatial data analysis are the main restraints.

Spatial biology preserves the location of molecules within a tissue, whereas bulk sequencing loses spatial context.

The market is led by 10x Genomics, Bruker (NanoString), Akoya Biosciences, and Bio-Techne.

Published Date: Aug-2024

Published Date: Jan-2024

Published Date: Feb-2024

Published Date: Jan-2025

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates