Resources

About Us

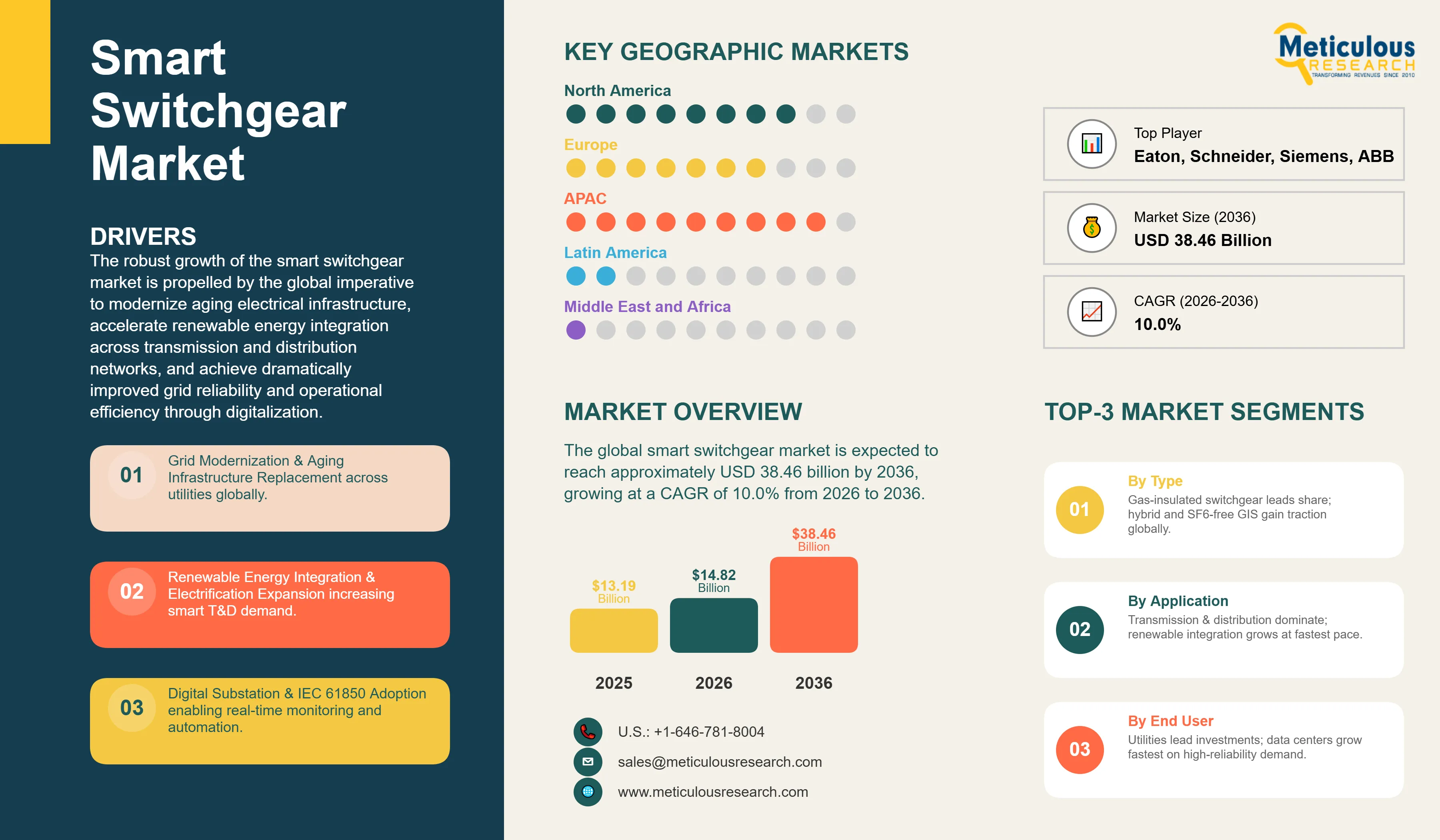

The global smart switchgear market was valued at USD 13.19 billion in 2025. The market is expected to reach approximately USD 38.46 billion by 2036 from USD 14.82 billion in 2026, growing at a CAGR of 10.0% from 2026 to 2036. The robust growth of the smart switchgear market is propelled by the global imperative to modernize aging electrical infrastructure, accelerate renewable energy integration across transmission and distribution networks, and achieve dramatically improved grid reliability and operational efficiency through digitalization. As power utilities, industrial operators, and governments confront the dual challenge of transitioning energy systems toward decarbonization while ensuring uninterrupted power supply to increasingly electricity-dependent economies, smart switchgear — integrating advanced sensing, communications, automation, and self-diagnostic capabilities into traditional switching apparatus — has emerged as the foundational infrastructure element enabling the intelligent, flexible, and resilient electrical grids of the future. The convergence of IEC 61850 digital substation standards, Industrial Internet of Things platforms enabling real-time asset health monitoring, and AI-powered predictive maintenance analytics is transforming switchgear from passive electrical isolation equipment into active, communicating nodes within comprehensive grid intelligence architectures.

Click here to: Get Free Sample Pages of this Report

Smart switchgear represents the evolution of conventional electrical switching apparatus through integration of digital intelligence, advanced sensing technologies, and communication interfaces that enable real-time monitoring, remote control, self-diagnostic capabilities, and seamless integration with supervisory control and data acquisition (SCADA) systems, energy management platforms, and grid automation frameworks. Unlike traditional switchgear that operates as passive electrical infrastructure requiring manual inspection and reactive maintenance, smart switchgear continuously measures and transmits operational parameters including current, voltage, power quality metrics, temperature, gas density (for GIS), arc flash energy, and contact wear — enabling predictive maintenance strategies that dramatically reduce unplanned outages and extend equipment service life beyond nominal design ratings. The integration of IEC 61850 communication protocols enabling interoperability between switchgear from different manufacturers and higher-level grid management systems represents a critical standardization milestone enabling utilities to deploy multi-vendor smart grid architectures without proprietary communication lock-in.

The smart switchgear market encompasses distinct product categories addressing different voltage levels and application contexts. High-voltage gas-insulated switchgear — typically operating at 72.5 kV and above — serves transmission substations, offshore wind platforms, and urban underground substations where space constraints make conventional air-insulated switchgear impractical. Medium-voltage switchgear spanning 1-52 kV represents the largest installed base globally, serving industrial facilities, commercial buildings, data centers, and distribution substations as the primary interface between transmission infrastructure and end consumers. Low-voltage smart switchgear below 1 kV addresses commercial and industrial power distribution within facilities, incorporating arc fault detection, energy metering, and motor protection intelligence. Emerging hybrid switchgear combining elements of GIS and air-insulated switchgear in compact configurations is gaining traction for applications requiring the compactness advantages of GIS at cost points closer to conventional air-insulated designs, particularly attractive for renewable energy generation substations requiring standardized, rapidly deployable switchgear solutions.

The digital transformation of switchgear is enabled by embedded electronic intelligence at multiple levels — intelligent electronic devices (IEDs) providing protection and control functions, merging units digitizing analog measurements for IEC 61850 GOOSE message transmission, process bus architectures replacing conventional copper wiring with fiber optic communications, and cloud-connected condition monitoring platforms aggregating data from thousands of switchgear assets for fleet-level analytics. Manufacturers including ABB, Siemens, Schneider Electric, and Eaton have invested substantially in developing proprietary digital ecosystems — ABB Ability, Siemens MindSphere, Schneider EcoStruxure, and Eaton Brightlayer — that connect smart switchgear to enterprise asset management and operational technology platforms, creating subscription-based digital service revenue streams complementing traditional hardware sales and establishing stickier customer relationships through continuous value delivery via software-enabled features and analytics insights.

Accelerating Renewable Energy Integration Driving Grid Modernization Investment

The global transition toward renewable energy generation is creating unprecedented demand for smart switchgear capable of managing the operational complexity introduced by variable, distributed energy resources. Solar PV and wind generation — characterized by intermittency, bidirectional power flows, and connection at diverse grid voltage levels — require fundamentally different protection schemes, switching speeds, and communication capabilities compared to conventional centralized generation paradigms. Smart switchgear with adaptive protection relaying capable of adjusting settings based on real-time generation and load conditions, automated fault isolation and network restoration through self-healing grid schemes, and advanced power quality monitoring detecting voltage disturbances, frequency deviations, and harmonic distortion introduced by inverter-based resources has become essential grid infrastructure. The offshore wind sector particularly drives demand for compact, maintenance-minimized smart switchgear solutions capable of reliable operation in harsh marine environments with extended service intervals, with major offshore wind developments in the North Sea, Baltic Sea, and emerging Asian markets requiring specialized GIS solutions rated for offshore platform installation. Energy storage system integration at utility and industrial scale creates additional switchgear demand for battery energy storage system (BESS) connections, requiring smart switchgear with specialized protection for DC-AC interface management and fire safety isolation capabilities.

Digital Substation Transformation and IEC 61850 Protocol Adoption

The transition from conventional analog substation architectures to fully digital substations based on IEC 61850 communication standards represents a transformative trend reshaping smart switchgear specifications, procurement criteria, and competitive positioning. Digital substations replace the extensive copper wiring of conventional protection and control architectures with process bus fiber optic networks transmitting sampled measured values and generic object-oriented substation event (GOOSE) messages between merging units, intelligent electronic devices, and substation automation systems — dramatically reducing engineering complexity, installation costs, and commissioning time while enabling new capabilities including non-invasive current measurement, centralized protection functions, and comprehensive digital twin representations supporting virtual commissioning and training. Smart switchgear natively supporting IEC 61850-9-2 sampled values and GOOSE messaging has become the default specification for new utility substation projects globally, with major utilities including National Grid, RTE, State Grid China, and PowerGrid India mandating digital substation architectures for all new capital projects. The interoperability benefits of IEC 61850 enable utilities to specify best-in-class protection, automation, and switchgear components from different manufacturers within coherent digital architectures, breaking the proprietary system integration approaches that previously created vendor lock-in and elevated total project costs.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 38.46 Billion |

|

Market Size in 2026 |

USD 14.82 Billion |

|

Market Size in 2025 |

USD 13.19 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 10.0% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Voltage, Component, Application, End-User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Grid Modernization Investment and Aging Infrastructure Replacement

The primary driver of smart switchgear market growth is the enormous global investment in electrical grid modernization driven by aging infrastructure replacement needs, renewable energy integration requirements, and electrification of transportation and industrial processes. The International Energy Agency estimates that annual global electricity network investment must reach USD 600-800 billion by 2030 to support net-zero energy transition pathways — representing a more than doubling of current investment levels and creating sustained, multi-decade demand for smart switchgear across all voltage levels and geographies. In North America, the Department of Energy's Grid Resilience and Innovation Partnership (GRIP) program and Infrastructure Investment and Jobs Act allocate substantial funding for grid modernization projects specifically targeting smart switchgear deployment to improve resilience against extreme weather events — hurricane, wildfire, and ice storm damage — that have caused billions in economic losses from extended outages. European utilities face mandatory smart grid investment requirements under EU regulatory frameworks including the Clean Energy Package and national decarbonization plans committing to net-zero power systems by 2035-2050, requiring comprehensive automation of distribution networks to accommodate mass deployment of rooftop solar, electric vehicle charging, and heat pump loads creating bidirectional power flows and demand flexibility opportunities.

Opportunity: Data Center and Mission-Critical Facility Expansion

The explosive growth of hyperscale data centers, cloud computing facilities, and artificial intelligence training infrastructure is creating a rapidly expanding premium market segment for smart switchgear combining the highest reliability standards with comprehensive condition monitoring and predictive maintenance capabilities. Data center operators including Amazon Web Services, Microsoft Azure, Google Cloud, and Meta are commissioning gigawatt-scale campuses with tier III and tier IV electrical infrastructure requiring redundant switchgear configurations with millisecond-level fault clearing, continuous insulation monitoring, and zero-downtime maintenance capabilities. Smart switchgear for data center applications commands substantial price premiums over standard utility-grade equipment given the catastrophic financial consequences of unexpected outages — estimated at USD 300,000-1 million per hour for large cloud operators — creating strong willingness-to-pay for advanced digital monitoring, arc flash mitigation, and predictive maintenance features. The geographic diversification of data center construction to Tier 2 cities, northern climates for cooling efficiency, and renewable energy proximity in regions including the Nordics, Middle East, and Southeast Asia creates global demand for smart switchgear across diverse environmental and grid conditions. Simultaneously, semiconductor fabrication facilities, pharmaceutical manufacturing plants, and hospital campuses represent premium end-users applying similar reliability standards and digital monitoring requirements to switchgear procurement.

How Does Gas-Insulated Switchgear Maintain Market Leadership?

Gas-insulated switchgear commands approximately 42-46% of total smart switchgear market revenue in 2026, reflecting its dominant position in high-voltage transmission infrastructure where the combination of compact footprint, exceptional reliability, minimal maintenance requirements, and suitability for urban underground installations makes GIS the preferred solution despite substantially higher unit costs compared to conventional air-insulated switchgear. Modern smart GIS integrates SF6 gas density monitoring with temperature compensation providing continuous insulation integrity verification, partial discharge detection systems enabling early identification of insulation defects before catastrophic failure, digital position indicators with electronic position feedback replacing conventional mechanical target indicators, and IEC 61850-compliant bay controllers enabling remote operation and integration with substation automation systems. The environmental profile of traditional SF6-insulated GIS is under increasing regulatory scrutiny given SF6's global warming potential approximately 23,500 times that of CO2 — driving accelerating development and commercial deployment of alternative insulation media including clean air (N2/O2 mixtures), CO2-based mixtures, fluoronitrile-based gases (3M Novec, g3), and vacuum interrupter technology extended to higher voltage classes. Siemens Energy, ABB, Hitachi Energy, and GE Vernova are each investing substantially in SF6-free GIS development, with clean air GIS now commercially available up to 145 kV and roadmaps for 420 kV solutions targeting regulatory deadline compliance in jurisdictions implementing F-gas phase-down schedules.

Why Does Medium Voltage Dominate the Smart Switchgear Market?

The medium voltage segment — encompassing switchgear operating between 1 kV and 52 kV — represents approximately 55-60% of total smart switchgear market volume in 2026, reflecting the vast scale of global distribution network infrastructure and the dense installed base of medium-voltage switchgear serving industrial facilities, commercial buildings, and urban distribution substations. Smart medium-voltage switchgear incorporating microprocessor-based protection relays, advanced metering infrastructure integration, arc flash detection, and remote monitoring capabilities is experiencing particularly strong demand from distribution utilities implementing advanced distribution management system (ADMS) architectures requiring communicating field assets throughout their networks. The industrial sector drives significant MV smart switchgear demand from process industries including oil and gas, chemical, cement, and steel that operate captive medium-voltage networks powering large motor loads, with smart switchgear providing motor protection coordination, power quality monitoring, and energy management data essential for operational efficiency optimization. High-voltage switchgear above 52 kV demonstrates the highest growth rate within the voltage segmentation at approximately 11-13% CAGR, driven by transmission network expansion and reinforcement projects globally accommodating large-scale renewable energy generation interconnection and cross-border power trade infrastructure.

How Does Transmission & Distribution Dominate Application Segments?

The transmission and distribution application segment accounts for approximately 45-50% of total smart switchgear market in 2026, representing the sustained capital investment by electric utilities globally in substation modernization, distribution automation, and grid resilience enhancement programs. Utility T&D smart switchgear deployments are characterized by large-scale procurement contracts spanning multiple years, comprehensive specification requirements ensuring interoperability with existing SCADA and energy management systems, and stringent reliability and safety certification requirements creating high barriers to entry for new suppliers. The renewable energy integration application demonstrates the highest growth rate at approximately 13-15% CAGR, driven by the enormous scale of solar, wind, and storage project commissioning globally — the IEA estimates 7,300 GW of new renewable capacity must be added globally by 2030 to achieve net-zero pathways, each requiring switchgear solutions for generation interconnection, collection system protection, and storage integration. Industrial application smart switchgear demand is driven by Industry 4.0 and digital factory initiatives embedding power quality monitoring and energy management capabilities into manufacturing infrastructure, combined with process safety requirements in hazardous industries mandating arc flash mitigation and fault discrimination capabilities exceeding standard utility specifications.

Why Do Utilities Command Market Leadership?

The utilities end-user segment commands approximately 50-55% of smart switchgear market revenue in 2026, reflecting electric power utilities' position as the primary infrastructure investors in generation, transmission, and distribution systems globally. Utility smart switchgear procurement is driven by regulatory mandates for grid reliability improvement, renewable portfolio standards requiring renewable energy accommodation, and customer expectations for service quality that translate into financial penalties for extended outages under performance-based regulation frameworks. Vertically integrated utilities in regulated markets and transmission system operators in liberalized markets represent the most significant individual buyers, with organizations including State Grid China, PowerGrid India, National Grid, RTE, and Enel procuring smart switchgear at scales ranging from individual substation upgrades to comprehensive national network modernization programs spanning multiple years and billions in capital expenditure. The data center end-user segment represents the fastest-growing market at approximately 14-16% CAGR, propelled by hyperscale cloud infrastructure expansion and AI computing demand creating voracious appetite for high-reliability smart switchgear with comprehensive digital monitoring. Oil and gas end-users represent a premium segment requiring explosion-proof and zone-classified smart switchgear capable of operation in hazardous environments while providing the same digital monitoring and remote operation capabilities demanded in conventional utility applications.

How is Asia-Pacific Maintaining Market Leadership?

Asia-Pacific holds approximately 38-42% of the global smart switchgear market in 2026, anchored by China's position as both the world's largest electricity consumer and most ambitious grid modernization investor. China's State Grid Corporation and China Southern Grid collectively invest over USD 60 billion annually in power grid infrastructure, with smart grid programs incorporating digital substation construction, distribution automation deployment, and advanced metering infrastructure rollout creating the world's largest single-country smart switchgear market. India represents the second major Asia-Pacific growth engine, with the government's Revamped Distribution Sector Scheme (RDSS) committing USD 40 billion over 2021-2026 to distribution infrastructure modernization and smart grid deployment targeting reduction of aggregate technical and commercial losses that cost Indian utilities billions annually. Japan and South Korea maintain advanced smart switchgear markets with domestic manufacturers including Mitsubishi Electric, Hitachi, and Hyundai Electric competing with global leaders across utility and industrial segments, supported by mature regulatory frameworks mandating grid modernization investment. Southeast Asian markets including Vietnam, Indonesia, and Thailand represent high-growth opportunity as rapidly industrializing economies expand transmission and distribution infrastructure to support manufacturing sector growth and urbanization.

Which Factors Drive Middle East & Africa's Rapid Growth?

Middle East & Africa demonstrates the highest regional growth rate at approximately 11-13% CAGR, driven by contrasting but equally compelling growth forces across the two sub-regions. The Middle East — particularly Saudi Arabia, UAE, Qatar, and Kuwait — is investing on an unprecedented scale in power infrastructure to support economic diversification under Vision 2030 and similar national transformation programs, with Saudi Aramco's industrial electrification initiative, NEOM megacity power infrastructure, and Saudi Arabia's 50% renewable energy target by 2030 collectively requiring massive smart switchgear deployment across generation, transmission, distribution, and industrial applications. UAE's decarbonization ambitions — including 100% clean energy targets and Mohammed bin Rashid Al Maktoum Solar Park expansion — drive substantial renewable energy switchgear demand, while Dubai Electricity and Water Authority's smart grid investments create comprehensive distribution automation requirements. The African sub-region presents a distinct growth profile driven by electrification expansion rather than modernization, with the International Energy Agency estimating USD 25 billion annual investment needed to achieve universal electricity access in sub-Saharan Africa by 2030 — creating greenfield demand for smart switchgear architectures designed from inception for remote monitoring and minimized maintenance intervention given the challenging operating environments and limited technical support infrastructure characterizing many African deployment contexts.

The global smart switchgear market is led by ABB Ltd. (ABB Ability digital switchgear portfolio), Siemens Energy AG (SIVACON, NXPLUS C, and Blue GIS SF6-free solutions), Schneider Electric SE (EcoStruxure Power, SM6 and PIX smart switchgear), and GE Vernova (EntelliGuard, GE digital substation solutions), which dominate through comprehensive product portfolios spanning all voltage levels, established utility relationships, and substantial digital platform ecosystems. Eaton Corporation (Power Defense, Xiria), Hitachi Energy (SafeRing, SafePlus, and Relion protection systems), Mitsubishi Electric Corporation (MELPRO digital protection, HV GIS solutions), and Legrand SA (smart low-voltage distribution) represent strong second-tier competitors with significant regional strength and specialized product capabilities. Emerging innovators including Lucy Electric (Aegis ring main units), Tavrida Electric (smart vacuum circuit breakers), and SOJO Electric (Chinese domestic smart switchgear) are expanding competitive dynamics through cost-optimized smart switchgear solutions targeting emerging market utilities and industrial customers, while regional players including Hyundai Electric, LS Electric, and CG Power challenge global leaders across Asian markets through competitive pricing, local manufacturing, and strong government relationships supporting domestic procurement preferences.

The global smart switchgear market is expected to grow from USD 14.82 billion in 2026 to USD 38.46 billion by 2036.

The global smart switchgear market is projected to grow at a CAGR of 10.0% from 2026 to 2036.

Gas-insulated switchgear dominates the market representing 42-46% of revenue through leadership in high-voltage transmission applications. Hybrid switchgear demonstrates the fastest growth driven by renewable energy generation substation demand and SF6-alternative technology adoption combining GIS compactness with reduced environmental footprint.

IEC 61850 adoption enables process bus architectures replacing conventional copper wiring with fiber optic communications, standardized interoperability between multi-vendor switchgear and protection systems, digital twin capabilities supporting virtual commissioning, and real-time GOOSE messaging enabling faster protection operating times than conventional hardwired schemes — collectively transforming substations from isolated electromechanical facilities into communicating nodes within comprehensive grid intelligence architectures.

Asia-Pacific leads with approximately 38-42% of global market driven by China's massive grid modernization investment and India's distribution infrastructure programs. Middle East & Africa demonstrates fastest regional growth at 11-13% CAGR propelled by Gulf state energy transition investment and sub-Saharan Africa electrification expansion.

The leading companies include ABB Ltd., Siemens Energy AG, Schneider Electric SE, GE Vernova, Eaton Corporation, Hitachi Energy, Mitsubishi Electric, and Legrand SA, with regional challengers including Hyundai Electric, LS Electric, CG Power, Lucy Electric, and domestic Chinese manufacturers competing aggressively across emerging market segments.

1. Introduction

1.1 Market Definition

1.2 Market Scope

1.3 Research Methodology

1.4 Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3 Digital Substation Evolution & IEC 61850 Adoption Landscape

3.4 SF6 Alternatives & Environmental Regulatory Impact on GIS Development

3.5 Porter's Five Forces Analysis

4. Global Smart Switchgear Market, by Type

4.1 Introduction

4.2 Air-Insulated Switchgear (AIS)

4.2.1 Indoor AIS

4.2.2 Outdoor AIS

4.3 Gas-Insulated Switchgear (GIS)

4.3.1 SF6-Insulated GIS

4.3.2 SF6-Free / Clean Air GIS

4.4 Hybrid Switchgear

4.5 Solid-Insulated Switchgear (SIS)

5. Global Smart Switchgear Market, by Voltage

5.1 Introduction

5.2 Low Voltage (Below 1 kV)

5.2.1 Smart LV Distribution Boards

5.2.2 Intelligent Molded Case & Air Circuit Breakers

5.3 Medium Voltage (1 kV - 52 kV)

5.3.1 Primary Distribution Switchgear (11-36 kV)

5.3.2 Secondary Distribution Switchgear (1-11 kV)

5.4 High Voltage (Above 52 kV)

5.4.1 Extra High Voltage (72.5-300 kV)

5.4.2 Ultra High Voltage (Above 300 kV)

6. Global Smart Switchgear Market, by Component

6.1 Introduction

6.2 Circuit Breakers

6.2.1 Vacuum Circuit Breakers

6.2.2 SF6 Circuit Breakers

6.2.3 Air Circuit Breakers

6.3 Disconnectors & Isolators

6.4 Busbars & Busduct Systems

6.5 Instrument Transformers

6.5.1 Current Transformers

6.5.2 Voltage Transformers

6.5.3 Electronic / Optical Instrument Transformers

6.6 Control & Protection Relays (IEDs)

7. Global Smart Switchgear Market, by Application

7.1 Introduction

7.2 Power Generation

7.2.1 Thermal & Nuclear Power Plants

7.2.2 Hydropower Facilities

7.3 Transmission & Distribution

7.3.1 Transmission Substations

7.3.2 Distribution Automation & Ring Main Units

7.4 Renewable Energy Integration

7.4.1 Solar PV Generation Substations

7.4.2 Onshore & Offshore Wind Substations

7.4.3 Battery Energy Storage System Connections

7.5 Industrial Applications

7.5.1 Oil, Gas & Petrochemical

7.5.2 Mining & Metals

7.5.3 Chemical & Process Industries

7.6 Commercial & Infrastructure

7.6.1 Data Centers & Hyperscale Facilities

7.6.2 Airports, Ports & Transportation Hubs

8. Global Smart Switchgear Market, by End-User

8.1 Introduction

8.2 Electric Utilities

8.2.1 Transmission System Operators

8.2.2 Distribution System Operators

8.3 Oil & Gas

8.4 Mining

8.5 Manufacturing & Industrial

8.6 Data Centers

8.7 Transportation & Infrastructure

9. Global Smart Switchgear Market, by Region

9.1 Introduction

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 U.K.

9.3.3 France

9.3.4 Italy

9.3.5 Spain

9.3.6 Nordics

9.3.7 Rest of Europe

9.4 Asia-Pacific

9.4.1 China

9.4.2 India

9.4.3 Japan

9.4.4 South Korea

9.4.5 Australia

9.4.6 Southeast Asia

9.4.7 Rest of Asia-Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Rest of Latin America

9.6 Middle East & Africa

9.6.1 Saudi Arabia

9.6.2 UAE

9.6.3 Qatar

9.6.4 South Africa

9.6.5 Rest of Middle East & Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Ranking/Positioning Analysis of Key Players, 2025

11. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

11.1 ABB Ltd.

11.2 Siemens Energy AG

11.3 Schneider Electric SE

11.4 GE Vernova

11.5 Eaton Corporation

11.6 Hitachi Energy Ltd.

11.7 Mitsubishi Electric Corporation

11.8 Legrand SA

11.9 Hyundai Electric & Energy Systems Co., Ltd.

11.10 LS Electric Co., Ltd.

11.11 CG Power and Industrial Solutions Ltd.

11.12 Lucy Electric (Lucy Group)

11.13 Tavrida Electric AG

11.14 Ormazabal (Velatia Group)

11.15 SOJO Electric Co., Ltd.

12. Appendix

12.1 Questionnaire

12.2 Related Reports

Published Date: Mar-2025

Published Date: Jun-2026

Subscribe to get the latest industry updates