Resources

About Us

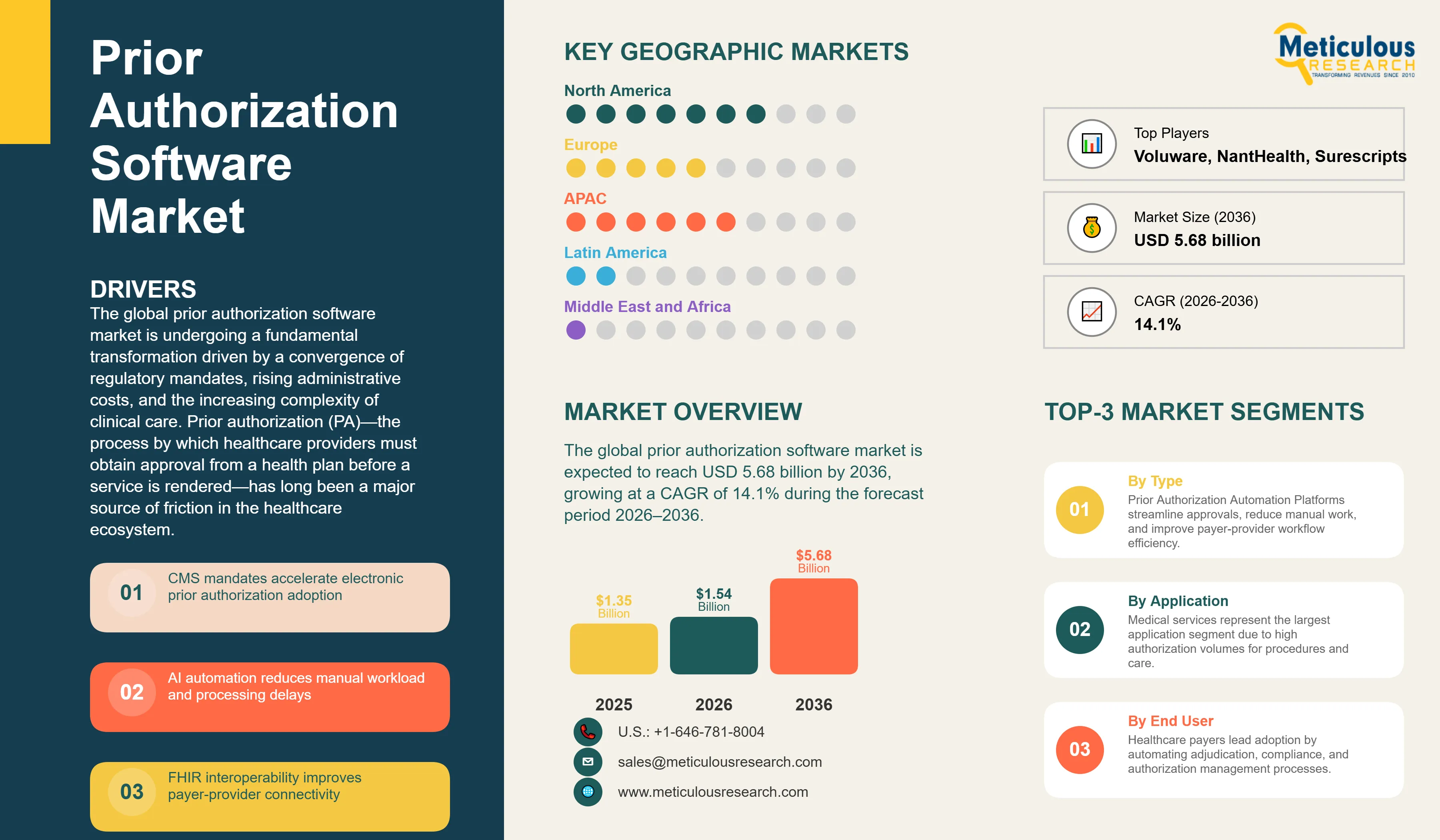

The global prior authorization software market was valued at USD 1.54 billion in 2026. This market is expected to reach USD 5.68 billion by 2036, growing at a CAGR of 14.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global prior authorization software market is undergoing a fundamental transformation driven by a convergence of regulatory mandates, rising administrative costs, and the increasing complexity of clinical care. Prior authorization (PA)—the process by which healthcare providers must obtain approval from a health plan before a service is rendered—has long been a major source of friction in the healthcare ecosystem. According to the American Medical Association (2024), physicians and their staff spend an average of 14 hours per week on PA requests, with 35% of physicians reporting that these delays have led to serious adverse events for patients. The hidden administrative tax of manual PA is estimated to cost the U.S. healthcare system approximately USD 35 billion annually, creating an urgent economic imperative for automation.

The growth of the overall prior authorization software market is being significantly driven by the implementation of the CMS Interoperability and Prior Authorization Final Rule (CMS-0057-F). By 2026, mandated payers are required to implement FHIR-based APIs for electronic prior authorization and adhere to strict decision turnaround times—72 hours for urgent requests and seven calendar days for standard requests. This regulatory push is moving the industry away from legacy methods like fax and telephone toward real-time, automated connectivity. Transitioning from manual to fully electronic PA can save an average of USD 16.52 per transaction for providers and USD 22.13 for payers, according to the 2024 CAQH Index. Consequently, healthcare organizations are increasingly investing in end-to-end automation platforms that utilize artificial intelligence and clinical decision support (CDS) to streamline the adjudication process.

The rise of specialty services, including oncology, genetic testing, and high-cost imaging, has further intensified the need for robust software solutions. Approximately 99% of Medicare Advantage enrollees are now in plans that require prior authorization for at least one category of health care services. While PA is a primary tool for cost containment for payers, the high rate of overturned denials—82% in some Medicare Advantage cohorts—highlights the critical need for software that ensures documentation accuracy and aligns with evidence-based medical necessity criteria. As AI and Large Language Models (LLMs) begin to automate the extraction of clinical data from patient charts, the market is poised to move toward a future of 'instant' approvals for low-risk procedures.

Geographically, North America dominates the market, holding an estimated 65% share in 2026. This is largely due to the unique complexity of the U.S. multi-payer system and the immediate pressure of CMS compliance. However, the Asia-Pacific region is projected to be the fastest-growing market through 2036. As private health insurance sectors expand in China, India, and Southeast Asia, the demand for administrative automation tools is surging. With the global shift toward digital health and interoperable ecosystems, prior authorization software is becoming a cornerstone of efficient healthcare administration.

The primary driver for the prior authorization software market is the implementation of the CMS Interoperability and Prior Authorization Final Rule (CMS-0057-F). This regulation mandates that certain payers implement FHIR-based APIs and meet strict decision timelines by 2026, forcing a massive industry-wide shift toward automation. Furthermore, the staggering administrative burden on providers is a major catalyst. With staff spending an average of 14 hours per week on PA requests, the economic case for software that reduces this 'hidden tax' is compelling. The 2024 CAQH Index reports that fully electronic PA can save payers over USD 22 per transaction, providing a strong financial incentive for large-scale technology adoption.

A key restraint for the market is the lack of uniformity in payer rules and documentation requirements across thousands of different health plans. This fragmentation makes it difficult for software to provide a single, seamless solution for all providers. Additionally, high integration costs remain a significant hurdle. Embedding advanced PA software into diverse legacy Electronic Health Record (EHR) systems requires substantial time and capital, which can be prohibitive for smaller physician groups and community hospitals. These technical and economic barriers can slow the pace of market penetration, particularly in less digitally mature regions.

The integration of Artificial Intelligence and Large Language Models (LLMs) presents a substantial growth opportunity. AI can automate the extraction of clinical data from unstructured charts to support medical necessity claims, significantly reducing the manual effort required for complex specialty requests. There is also a major opportunity in the move toward real-time payer-provider connectivity. By establishing direct FHIR-based links, the industry can move toward 'instant' approvals for low-risk, high-volume procedures, dramatically improving the patient experience. Furthermore, the expansion of private insurance in the Asia-Pacific region offers a vast untapped market for administrative automation as these systems digitize their workflows.

Maintaining documentation accuracy while increasing the speed of requests is a critical challenge. AI-generated PA requests must still meet strict medical necessity criteria to avoid increased denial rates. Furthermore, the slow adoption of FHIR standards across all segments of the healthcare ecosystem remains a hurdle for achieving true end-to-end interoperability. Software providers also face the challenge of keeping their clinical decision support modules updated with the latest evidence-based guidelines and changing payer policies, requiring continuous investment in content management and clinical validation.

AI is moving beyond basic workflow automation to support clinical review, with advanced algorithms capable of evaluating documentation against payer-specific medical policies and predicting approval probability before submission. The increasing administrative burden associated with prior authorization is accelerating adoption of these technologies. According to the American Medical Association (AMA), physicians complete an average of 39 prior authorization requests per week and spend approximately 13 hours weekly managing these processes. In addition, the CMS-0057-F Interoperability and Prior Authorization Final Rule is expected to accelerate investments in AI-enabled and electronic prior authorization solutions. As healthcare organizations seek to reduce delays and improve approval rates, AI-driven clinical review is becoming a key growth driver for the prior authorization software market.

The prior authorization ecosystem is increasingly converging on HL7 FHIR standards, enabling more seamless data exchange between providers and payers while reducing reliance on proprietary portals and fax-based workflows. Regulatory initiatives are accelerating this transition, with the Centers for Medicare & Medicaid Services (CMS) finalizing the CMS-0057-F Interoperability and Prior Authorization Rule requiring impacted payers to implement FHIR-based electronic prior authorization capabilities beginning in 2027. In addition, the Office of the National Coordinator for Health Information Technology (ONC) reported that nearly 96% of non-federal acute care hospitals and 78% of office-based physicians had adopted certified electronic health record systems, providing a strong foundation for standards-based interoperability. As healthcare organizations seek to improve efficiency and reduce administrative burden, adoption of FHIR-enabled prior authorization solutions is expected to accelerate significantly.

Based on solution type, the market is segmented into Prior Authorization Automation Platforms, Connectivity & Interoperability Solutions, and EHR-Integrated PA Modules (instead of CDS Integration). In 2026, the Prior Authorization Automation Platforms segment is expected to hold the largest share because these platforms provide comprehensive, end-to-end workflow solutions that both providers and payers require to manage the entire PA lifecycle.

The Connectivity & Interoperability Solutions segment is projected to witness the fastest growth, driven by the immediate 2026 CMS mandate for FHIR-based electronic data exchange between payers and providers.

Based on end user, the market is segmented into Healthcare Payers, Healthcare Providers, and Pharmaceutical & Diagnostic Companies. In 2026, the Healthcare Payers segment is expected to hold the largest share. Payers are the primary adjudicators of PA requests and are under direct regulatory pressure to implement the systems required for CMS compliance.

The Healthcare Providers segment is projected to witness the fastest growth. As administrative costs continue to rise, clinics and hospitals are aggressively seeking software to eliminate the massive staff time spent on manual PA requests and to reduce care delays.

North America is expected to hold the largest share of the global prior authorization software market in 2026, accounting for around 65% of total revenue. This position is primarily due to the unique complexity of the U.S. healthcare system and the immediate pressure of the CMS-0057-F regulation. In the U.S., 94% of physicians report that PA has led to care delays, and the high volume of Medicare Advantage enrollees further drives the demand for automated adjudication.

In Europe, the market is growing as public health systems increasingly use PA to manage the costs of high-priced biologics and specialty drugs. Meanwhile, Asia-Pacific is projected to be the fastest-growing region. The rapid digitization of private insurance sectors in China, India, and Southeast Asia is driving a surge in demand for administrative automation tools. Key companies operating in the global market include Waystar, Availity, and Change Healthcare (UnitedHealth Group).

The global prior authorization software market is highly competitive, featuring a mix of established revenue cycle management (RCM) providers, EHR vendors, and specialized AI startups. Competition is increasingly focused on the depth of payer connectivity, the accuracy of AI-driven clinical reviews, and the ease of integration into existing clinical workflows. Strategic acquisitions, such as UnitedHealth Group's acquisition of Change Healthcare, are a major trend in market consolidation.

Key players in the global market include Waystar (U.S.), Availity, LLC (U.S.), Change Healthcare (UnitedHealth Group) (U.S.), Epic Systems Corporation (U.S.), Oracle Health (Cerner) (U.S.), Experian Health (U.S.), Olive (U.S.), Myndshft Technologies (U.S.), Glidian (U.S.), Itiliti Health (U.S.), Rhyme (U.S.), PriorAuthNow (U.S.), Infinitus (U.S.), Cohere Health (U.S.), EviCore healthcare (Cigna) (U.S.), Magellan Health (Centene) (U.S.), NantHealth (U.S.), Health-E-Map (U.S.), MCG Health (Hearst) (U.S.), and InterQual (Change Healthcare) (U.S.).

The market is projected to reach USD 5.68 million by 2036, growing at a CAGR of 14.1% from 2026 to 2036.

Manual prior authorization is estimated to cost the U.S. healthcare system approximately USD 35 billion annually in administrative overhead.

Providers can save an average of USD 6.62 per transaction by moving from manual to fully electronic prior authorization.

The Asia-Pacific region is projected to witness the fastest growth due to the rapid digitization of private healthcare systems.

The mandate requires payers to implement FHIR-based electronic PA and meet strict decision turnaround times by 2026, driving massive automation adoption.

Regulatory mandates, the high administrative burden on staff, and the rising volume of specialty services are the primary drivers.

The market is expected to grow at a CAGR of 14.1% during the forecast period 2026–2036.

Prior Authorization Automation Platforms hold the largest share as they provide end-to-end workflow management.

The average denial rate is approximately 7.8% as of 2024, with 82% of denials being partially or fully overturned upon appeal.

Leading players include Waystar, Availity, Change Healthcare, Epic Systems, and Oracle Health.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Solution Type

3.2.2. Market Analysis, by Deployment Mode

3.2.3. Market Analysis, by End User

3.2.4. Market Analysis, by Application

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Implementation of CMS Interoperability and Prior Authorization Final Rule (CMS-0057-F)

4.2.1.2. Urgent Need to Reduce Staggering Administrative Costs (USD 35 Billion Annually)

4.2.1.3. Compelling Financial Savings from Electronic PA (USD 22.13 Per Transaction for Payers)

4.2.1.4. Rising Volume of Specialty Services and Medicare Advantage Enrollees

4.2.2. Restraints

4.2.2.1. Fragmentation of Payer Rules and Documentation Requirements

4.2.2.2. High Integration Costs with Diverse Legacy EHR Systems

4.2.3. Opportunities

4.2.3.1. Integration of AI and LLMs for Automated Clinical Data Extraction

4.2.3.2. Transition Toward Real-Time 'Instant' Adjudication and Approvals

4.2.3.3. Rapid Digitization of Private Insurance in Asia-Pacific Markets

4.2.4. Challenges

4.2.4.1. Maintaining Adjudication Accuracy and Reducing High Appeal Overturn Rates

4.2.4.2. Slow Global Adoption of Unified Interoperability Standards (FHIR)

4.2.5. Trends

4.2.5.1. Mainstreaming of AI-Driven Clinical Review and Predicted Approval Odds

4.2.5.2. Rapid Industry Convergence on HL7 FHIR-Based Data Exchange

4.3. Porter's Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Prior Authorization Software Market, by Solution Type

5.1. Overview

5.2. Prior Authorization Automation Platforms (Largest Share)

5.3. Connectivity & Interoperability Solutions (Fastest Growth)

5.4. EHR-Integrated PA Modules

6. Global Prior Authorization Software Market, by Deployment Mode

6.1. Overview

6.2. Cloud-based Solutions

6.3. On-premise Solutions

7. Global Prior Authorization Software Market, by End User

7.1. Overview

7.2. Healthcare Payers (Largest Share)

7.3. Healthcare Providers (Fastest Growth)

7.4. Pharmacies & Pharmacy Benefit Managers (PBMs)

8. Global Prior Authorization Software Market, by Application

8.1. Overview

8.2. Medical Services (Largest Share)

8.3. Prescription Drugs (Fastest Growth)

8.4. Durable Medical Equipment (DME)

9. Global Prior Authorization Software Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. Saudi Arabia

9.6.2. UAE

9.6.3. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Waystar

11.2. Availity, LLC

11.3. Change Healthcare (UnitedHealth Group)

11.4. Epic Systems Corporation

11.5. Oracle Health (Cerner)

11.6. Experian Health

11.7. CoverMyMeds

11.8. Cohere Health

11.9. Surescripts

11.10. MCG Health

11.11. EviCore Healthcare

11.12. Voluware

11.13. NantHealth

11.14. Veradigm LLC

11.15. athenahealth, Inc.

11.16. eClinicalWorks

11.17. NextGen Healthcare, Inc.

11.18. Myndshft Technologies, Inc.

11.19. Infinitus Systems, Inc.

11.20. Itiliti Health, Inc.

12. Appendix

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Sep-2016

Subscribe to get the latest industry updates