Resources

About Us

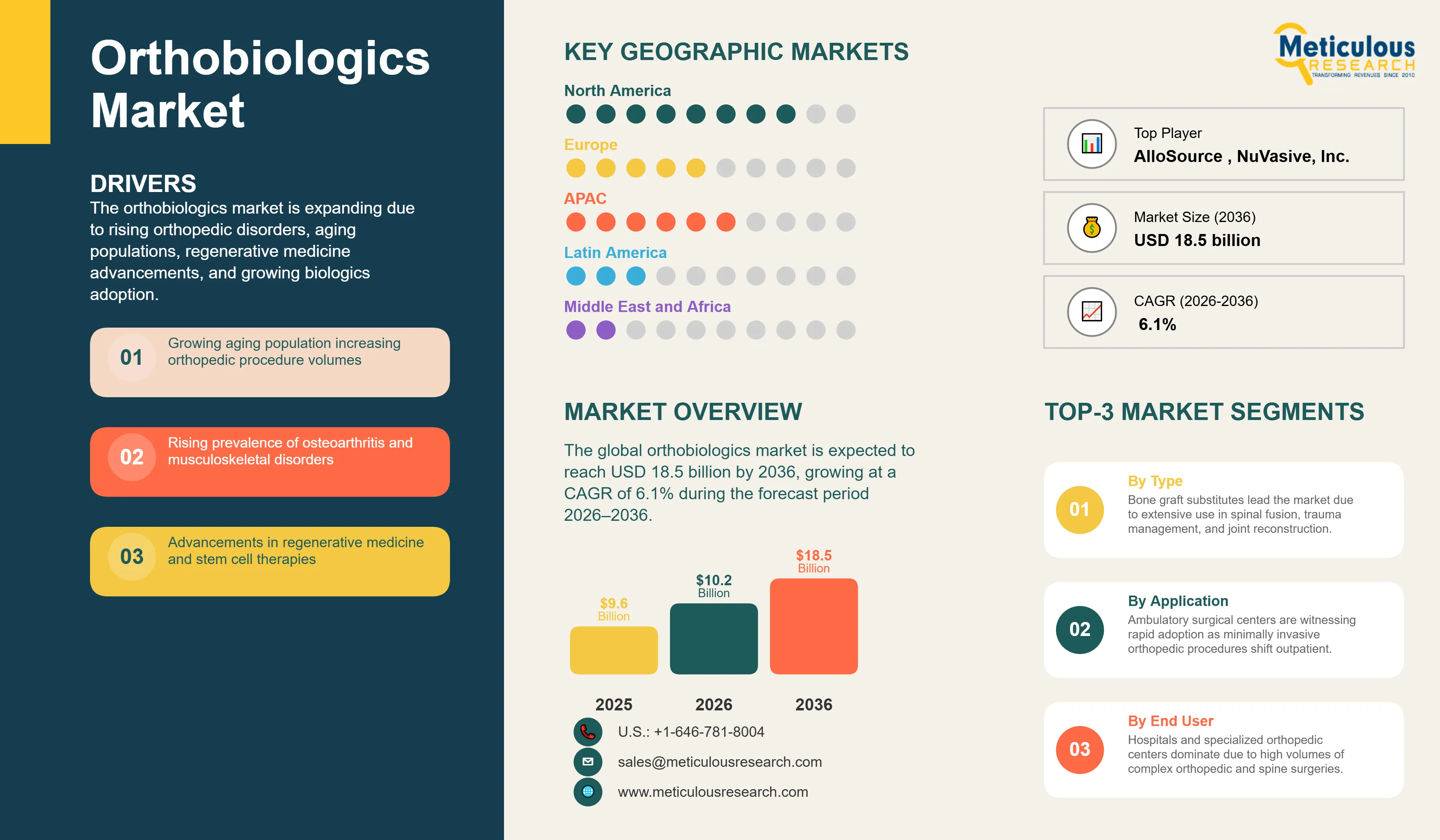

The global orthobiologics market is estimated to be USD 10.2 billion in 2026. This market is expected to reach USD 18.5 billion by 2036, growing at a CAGR of 6.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global orthobiologics market is entering a transformative era, defined by the convergence of biological innovation and advanced surgical techniques to enhance the natural healing processes of bone and soft tissue. As the global population ages and the incidence of musculoskeletal disorders surges, the demand for biological solutions that can accelerate recovery and improve surgical outcomes has never been higher. The market is primarily driven by the increasing adoption of bone graft substitutes, viscosupplementation, and regenerative cell therapies, which are becoming integral to spinal fusion, trauma management, and joint reconstruction. Clinical guidelines from the American Academy of Orthopaedic Surgeons (AAOS) and the Orthopaedic Research Society (ORS) emphasize the importance of using substantiated biological products to optimize bone union and tissue regeneration. The market is also witnessing a significant shift toward synthetic and allograft-based substitutes that minimize donor-site morbidity and improve surgical efficiency. Furthermore, the development of specialized, minimally invasive orthobiologic kits is facilitating the migration of these procedures to specialized ambulatory surgical centers (ASCs), enhancing patient access and reducing overall healthcare costs. As the industry focuses on precision regenerative medicine and personalized orthopedic stabilization, the integration of stem cell therapies and bioactive scaffolds is expected to further drive market growth, ensuring sustained expansion through 2036.

The growth of the global orthobiologics market is primarily driven by the increasing burden of orthopedic conditions and the rapid advancement of biological healing technologies.

Escalating Global Incidence of Osteoarthritis and Age-Related Musculoskeletal Degeneration

A major driver for the market is the rising global prevalence of osteoarthritis and other degenerative musculoskeletal conditions, which are increasingly affecting the aging population. According to the World Health Organization, approximately 528 million people worldwide were living with osteoarthritis in 2019, representing an increase of nearly 113% since 1990. Furthermore, the WHO estimates that approximately 1.71 billion people globally are affected by musculoskeletal conditions, making them the leading contributor to disability worldwide. As life expectancy continues to increase, the burden of age-related joint degeneration is expected to rise substantially. According to the United Nations, the global population aged 65 years and older is projected to reach nearly 1.6 billion by 2050, significantly expanding the patient population requiring musculoskeletal care. Government initiatives focused on healthy aging and the growing awareness of regenerative medicine approaches are further supporting demand for orthobiologic therapies. This sustained need for effective bone, cartilage, and soft tissue repair solutions continues to drive the adoption of orthobiologics across orthopedic and sports medicine applications.

Technological Advancements in Regenerative Medicine and the Increasing Adoption of Stem Cell Therapies

The market is significantly driven by rapid technological advancements in regenerative medicine, particularly the development of stem cell therapies and bioactive scaffolds. These innovations are providing new avenues for enhancing natural tissue healing and treating complex orthopedic injuries. The increasing adoption of bone marrow aspirate concentrate (BMAC) and adipose-derived stem cells is attracting significant clinical interest and investment. These therapies offer the potential for faster recovery times and improved long-term clinical outcomes compared to traditional surgical methods. Continuous research into the molecular mechanisms of bone regeneration and the development of next-generation biological products are further accelerating market adoption across diverse orthopedic specialties.

Despite its growth potential, the orthobiologics market faces challenges related to rigorous regulatory approval processes and the significant costs associated with advanced regenerative products.

Rigorous Regulatory Approval Processes for Complex Biological and Cell-Based Products

A major restraint for the market is the complex and rigorous regulatory landscape for biological and cell-based orthopedic products. Agencies like the FDA and EMA have established stringent requirements for safety and efficacy, which can lead to long approval timelines and high development costs. The need for extensive clinical trial data to substantiate regenerative claims can be a significant barrier for smaller biotech firms. These regulatory challenges can slow the market entry of innovative biological therapies and impact the overall pace of technological advancement in the field, particularly for advanced stem cell and gene therapy products.

High Cost of Advanced Orthobiologic Consumables and Limited Reimbursement Coverage in Emerging Markets

The market is also impacted by the high cost associated with advanced orthobiologic products, such as specialized stem cell kits and recombinant growth factors. These premium prices can limit the adoption of these therapies in cost-sensitive healthcare environments. Furthermore, inconsistent reimbursement coverage for regenerative orthopedic procedures, especially in emerging economies, can restrain market growth. As highlighted by various orthopedic societies, the lack of standardized reimbursement frameworks for newer biological interventions remains a challenge for manufacturers in gaining universal clinical acceptance and expanding their market reach.

Future growth opportunities in the orthobiologics market are centered on the rapid expansion of ambulatory surgical centers and the integration of advanced materials science.

Rising Migration of Minimally Invasive Orthopedic Procedures to Ambulatory Surgical Centers (ASCs)

There is a significant opportunity for market growth driven by the increasing migration of minimally invasive orthopedic procedures to specialized ambulatory surgical centers (ASCs). These facilities offer a more efficient, patient-centric environment and are increasingly performing procedures that utilize orthobiologic products. The development of specialized, easy-to-use biological kits that are optimized for outpatient workflows is a key opportunity for manufacturers. Manufacturers that can provide comprehensive procedural support and cost-effective biological solutions tailored to the ASC setting are well-positioned to capitalize on this high-growth end-user segment.

Technological Advancements in Bioactive Materials and the Integration of 3D-Printed Biological Scaffolds

The development of next-generation bioactive materials and the integration of 3D-printed biological scaffolds represent a major opportunity. These technologies allow for the creation of patient-specific implants that can be seeded with biological factors to enhance bone integration and tissue repair. Manufacturers that can innovate in materials science and combine it with biological expertise are likely to lead the next phase of market expansion. The integration of these advanced scaffolds into existing orthopedic workflows will enhance procedural success rates and improve long-term clinical outcomes, driving further demand for specialized orthobiologic solutions.

Increasing Shift toward Personalized Regenerative Medicine and Patient-Specific Biological Therapies

A prominent trend in 2026 is the increasing shift toward personalized regenerative medicine, where biological therapies are tailored to the specific needs of the patient. This trend is driven by advancements in genomics and molecular diagnostics, allowing clinicians to select the most effective biological interventions for each individual. Manufacturers are increasingly focusing on developing patient-specific orthobiologic products and integrating precision medicine approaches to optimize healing outcomes. This shift reflects a broader market trend toward the individualization of orthopedic care, where biological solutions play a central role in achieving superior clinical results.

Rising Clinical Adoption of Bone Marrow Aspirate Concentrates (BMAC) for Point-of-Care Regenerative Treatment

The market is witnessing an increasing trend toward the clinical adoption of bone marrow aspirate concentrates (BMAC) for point-of-care regenerative treatment. This technique allows for the rapid collection and concentration of a patient's own stem cells and growth factors during a surgical procedure. The development of specialized, automated concentration systems is facilitating this shift, providing clinicians with a convenient and effective way to enhance natural healing. This trend is aligning with the broader goal of optimizing biological healing while minimizing patient trauma, marking a significant step toward the standardization of regenerative orthopedic practices.

Analysis by Product Type

Based on product type, the bone graft substitutes segment is expected to hold the largest share of the global orthobiologics market in 2026. This leadership is substantiated by its extensive use in spinal fusion procedures, trauma management, and joint reconstructions. The clinical shift from autografts to synthetic and allograft-based substitutes is driving this segment's dominance. However, the **stem cell therapy segment** is projected to register the **highest CAGR** during the forecast period. The increasing research into regenerative medicine and its potential to enhance natural tissue healing, particularly for chronic orthopedic conditions like osteoarthritis, are driving its rapid and sustained growth.

Analysis by End User

By end user, the hospitals & specialized orthopedic centers segment is expected to hold the largest share in 2026, as these facilities perform the majority of complex orthopedic surgeries that require significant biological interventions. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing shift toward outpatient-based, minimally invasive orthopedic care and the development of specialized biological kits that are optimized for ASC workflows are significantly accelerating adoption in this segment.

Largest Share: North America

North America is expected to dominate the global orthobiologics market in 2026. This leading position is attributed to its advanced healthcare infrastructure, high healthcare spending, and a large population suffering from sports-related injuries and age-related orthopedic conditions. The region has a high adoption rate of innovative biological therapies and a well-established network of specialized orthopedic centers. Data from the American Academy of Orthopaedic Surgeons (AAOS) and the Orthopaedic Research Society (ORS) indicate a high volume of spinal and joint procedures annually, which are key consumers of orthobiologic products.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global orthobiologics market, with a CAGR of 8-10% during the forecast period. This rapid expansion is driven by the rapidly aging population in countries like China and Japan, increasing healthcare access, and the rising prevalence of musculoskeletal disorders. Government investments in healthcare infrastructure and a growing middle class with higher disposable income are accelerating the adoption of advanced regenerative orthopedic treatments. According to the World Health Organization (WHO), the APAC region has one of the fastest-growing geriatric populations globally, directly correlating with the increased demand for bone and joint health solutions.

The global orthobiologics market is characterized by intense competition between established medical technology giants and specialized regenerative medicine firms. Competition is primarily focused on enhancing the regenerative potential and clinical safety of biological products and improving the patient experience through minimally invasive delivery techniques. Key players are investing heavily in R&D to develop next-generation bone graft substitutes and advanced stem cell therapies to capture the growing specialized and outpatient markets. Strategic developments often involve acquisitions of innovative biotech firms and partnerships with leading orthopedic centers to validate new biological protocols. Furthermore, there is a growing focus on providing integrated biological solutions that combine bioactive scaffolds with precise delivery systems. Manufacturers are also increasingly focusing on comprehensive clinical training programs and robust supply chain management to ensure the successful implementation and consistent availability of their biological products in diverse healthcare settings, which is critical for maintaining market leadership in this rapidly evolving regenerative orthopedic field.

Medtronic plc, Stryker Corporation, Johnson & Johnson (DePuy Synthes), Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Enovis (DJO), Bioventus Inc., Arthrex, Inc., SeaSpine Holdings Corporation, Globus Medical, Inc., Orthofix Medical Inc., MTF Biologics, AlloSource, LifeNet Health, NuVasive, Inc., Xtant Medical Holdings, Inc., BoneSupport AB, Collagen Matrix, Inc., Cerapedics, Inc., Baxter International Inc.

The global market is estimated at USD 10.2 billion in 2026, with a projected growth to USD 18.5 billion by 2036, at a CAGR of 6.1%.

Primary drivers include the rising prevalence of musculoskeletal disorders and the shift toward regenerative orthopedic therapies like stem cell treatments.

Major restraints include stringent regulatory requirements for cell-based products and the high cost of advanced biological consumables.

Opportunities lie in the expansion of outpatient orthopedic care in ASCs and the development of bioactive and 3D-printed scaffolds.

Bone graft substitutes are expected to hold the largest share due to their extensive use in spinal fusion and trauma management.

Stem cell therapy is projected to grow at the fastest CAGR, driven by increasing research and its potential for natural tissue healing.

Hospitals & specialized orthopedic centers are expected to hold the largest share, as they perform the majority of complex surgeries.

North America is expected to dominate the market due to its advanced healthcare infrastructure and high healthcare spending.

Asia-Pacific is projected to witness the fastest growth, fueled by a rapidly aging population and increasing healthcare access.

Key trends include the shift toward personalized regenerative medicine and the increasing use of bone marrow aspirate concentrates.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Escalating Global Incidence of Osteoarthritis and Age-Related Musculoskeletal Degeneration

4.2.1.2. Technological Advancements in Regenerative Medicine and the Increasing Adoption of Stem Cell Therapies

4.2.2. Restraints

4.2.2.1. Rigorous Regulatory Approval Processes for Complex Biological and Cell-Based Products

4.2.2.2. High Cost of Advanced Orthobiologic Consumables and Limited Reimbursement Coverage in Emerging Markets

4.2.3. Opportunities

4.2.3.1. Rising Migration of Minimally Invasive Orthopedic Procedures to Ambulatory Surgical Centers (ASCs)

4.2.3.2. Technological Advancements in Bioactive Materials and the Integration of 3D-Printed Biological Scaffolds

4.2.4. Trends

4.2.4.1. Increasing Shift toward Personalized Regenerative Medicine and Patient-Specific Biological Therapies

4.2.4.2. Rising Clinical Adoption of Bone Marrow Aspirate Concentrates (BMAC) for Point-of-Care Regenerative Treatment

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Orthobiologics Market, by Product Type

5.1. Bone Graft Substitutes

5.1.1. Demineralized Bone Matrix (DBM)

5.1.2. Synthetic Bone Grafts

5.1.3. Ceramic-Based Bone Grafts

5.2. Viscosupplementation

5.2.1. Single-Injection Viscosupplements

5.2.2. Multi-Injection Viscosupplements

5.3. Stem Cell Therapy

5.3.1. Autologous Stem Cell Therapy

5.3.2. Allogeneic Stem Cell Therapy

5.4. Allografts

5.4.1. Structural Allografts

5.4.2. Soft Tissue Allografts

5.4.3. Osteochondral Allografts

5.5. Others

5.5.1. Platelet-Rich Plasma (PRP)

5.5.2. Bone Morphogenetic Proteins (BMPs)

6. Global Orthobiologics Market, by End User

6.1. Hospitals & Specialized Orthopedic Centers

6.2. Ambulatory Surgical Centers (ASCs)

7. Global Orthobiologics Market, by Geography

7.1. North America

7.1.1. U.S.

7.1.2. Canada

7.2. Europe

7.2.1. Germany

7.2.2. U.K.

7.2.3. France

7.2.4. Italy

7.2.5. Spain

7.2.6. Rest of Europe

7.3. Asia Pacific

7.3.1 China

7.3.2. Japan

7.3.3. India

7.3.4. South Korea

7.3.5. Rest of Asia Pacific

7.4. Latin America

7.4.1. Brazil

7.4.2. Argentina

7.4.3. Mexico

7.4.4. Rest of Latin America

7.5. Middle East & Africa

7.5.1. UAE

7.5.2. Saudi Arabia

7.5.3. Rest of Middle East & Africa

8. Competitive Landscape

8.1. Overview

8.2. Key Growth Strategies

8.3. Competitive Benchmarking

8.4. Competitive Dashboard

8.4.1. Industry Leaders

8.2. Market Differentiators

8.4.3. Vanguards

8.4.4. Emerging Companies

18.5. Market Share/Ranking Analysis, By Key Player (2025)

9. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

9.1. Medtronic plc

9.2. Stryker Corporation

9.3. Johnson & Johnson (DePuy Synthes)

9.4. Zimmer Biomet Holdings, Inc.

9.5. Smith & Nephew plc

9.6. Enovis (DJO)

9.7. Bioventus Inc.

9.8. Arthrex, Inc.

9.9. SeaSpine Holdings Corporation

9.10. Globus Medical, Inc.

9.11. Orthofix Medical Inc.

9.12. MTF Biologics

9.13. AlloSource

9.14. LifeNet Health

9.15. NuVasive, Inc.

9.16. Xtant Medical Holdings, Inc.

9.17. BoneSupport AB

9.18. Collagen Matrix, Inc.

9.19. Cerapedics, Inc.

9.20. Baxter International Inc.

10. Appendix

10.1. Disclaimer

11. Key Questions Answered

Published Date: Feb-2026

Published Date: Aug-2018

Subscribe to get the latest industry updates