Resources

About Us

Online Language Learning Market Size, Share, Forecast, & Trends Analysis by Learning Mode (Self-learning Apps & Applications, AI-Powered Virtual Tutors), Age Group, Language (English, Spanish, Mandarin), End User (Individual Learners, Educational Institutions, Corporate Learners), and Geography — Global Forecast to 2036

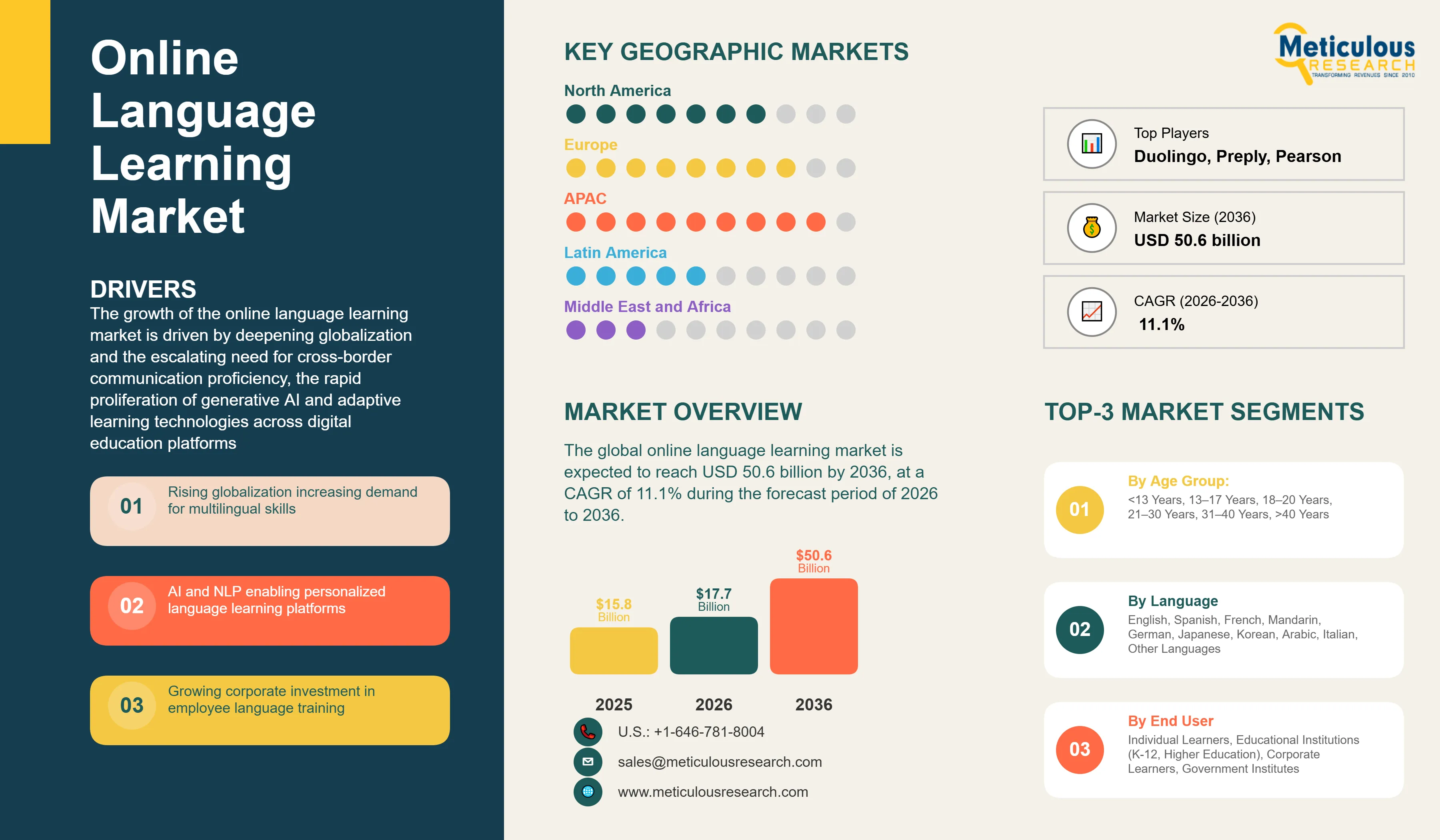

Report ID: MRICT - 104325 Pages: 350 Mar-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 48 Hours Download Free Sample ReportThe global online language learning market was valued at USD 15.8 billion in 2025. This market is expected to reach USD 50.6 billion by 2036 from USD 17.7 billion in 2026, at a CAGR of 11.1% during the forecast period of 2026 to 2036.

The growth of the online language learning market is driven by deepening globalization and the escalating need for cross-border communication proficiency, the rapid proliferation of generative AI and adaptive learning technologies across digital education platforms, and the expanding integration of language learning within corporate workforce development and ESG-aligned diversity, equity, and inclusion (DEI) programs. The combination of artificial intelligence, natural language processing (NLP), speech recognition, and large language models (LLMs) is fundamentally redefining how learners acquire, practice, and retain new languages, enabling highly personalized, real-time, and contextually adaptive learning experiences at scale.

Platforms such as Duolingo, Inc. have significantly expanded their use of generative AI in language learning. Duolingo Max integrates generative AI to simulate real-world conversational practice through features such as dynamic roleplay scenarios and instant grammar explanations. The company surpassed USD 1 billion in annual revenue in 2025, reflecting the growing adoption of AI-enabled language learning platforms. At the same time, structured curriculum-based platforms such as Babbel GmbH continue to evolve their offerings by integrating speech recognition, personalized review sessions, and podcast-based learning modules to support learners seeking grammar-progressive language instruction.

The growing demand for multilingual capabilities driven by international trade expansion, rising international student mobility, cross-border migration, and the digitalization of education, mainly in Asia-Pacific economies, is generating substantial growth opportunities across the global online language learning ecosystem. According to the International Telecommunication Union (ITU), approximately 6 billion people (around 74% of the global population) were using the internet in 2025, providing an expanding digital foundation for the adoption of online education platforms, including language learning applications. Furthermore, strong government investment in digital education infrastructure and the rising preference of multinational corporations for multilingual employees are expected to create significant growth opportunities for the companies operating in this market throughout the forecast period.

Click here to: Get Free Sample Pages of this Report

The online language learning market includes the full spectrum of digital platforms, applications, services, and technologies enabling individuals, educational institutions, corporations, and government bodies to acquire proficiency in a new language through internet-connected delivery models. Core solution categories within this market include self-learning apps and applications such as AI-powered language apps, web-based platforms, and gamified learning applications; and tutoring services, including one-on-one online tutoring, group online tutoring, and increasingly, AI-powered virtual tutors deployed through conversational AI systems. The market by end user is primarily driven by individual learners pursuing personal development, professional advancement, or travel preparation; educational institutions spanning K-12 and higher education; corporate learners engaging in employee development, global talent management, and DEI-aligned workforce programs; and government institutes investing in national language education and public workforce development programs.

Accelerating Integration of Generative AI and Large Language Models in Language Learning Platforms

The integration of generative artificial intelligence (AI) and large language models (LLMs) into online language learning platforms is the most transformative technology trend driving the market in 2026. AI-powered systems now enable real-time adaptive content generation, dynamic conversation simulation, and highly personalized feedback on pronunciation, grammar, and vocabulary. Platforms deploying these technologies are showing meaningfully higher learner retention rates and engagement depth compared to traditional static curriculum approaches.

Duolingo’s rollout of Duolingo Max, its generative AI-powered tutoring tier, demonstrates this transition, leveraging AI to simulate real-world conversations, provide contextual grammar explanations, and adapt lesson sequencing dynamically based on individual learner performance data. More broadly, the industry is shifting toward AI-native content infrastructure, where AI-generated lessons verified by human educators significantly reduce the cost and timeline of launching new language courses, thereby enabling platforms to expand language coverage and personalize learning at a global scale. This trend is driving competitive differentiation and accelerating the consolidation of market share among AI-capable platform leaders.

Rise of Hybrid and Blended Learning Models Combining AI Self-Learning with Live Tutoring

Another major trend in the online language learning market is the growing adoption of hybrid and blended learning models that combine the scalability and personalization of AI-driven self-learning applications with the communicative effectiveness and motivational benefits of live human tutoring. While self-learning apps continue to dominate the market by volume, learner outcomes research consistently highlights the irreplaceable value of live conversational practice for achieving meaningful fluency milestones, driving demand for hybrid formats that integrate both modalities.

Tutoring marketplaces, live instruction platforms, and structured curriculum providers are responding by building complementary pathways that transition learners between self-paced modules and live sessions based on their progress stage. Corporate language training programs, in particular, are increasingly structuring employee language development through blended frameworks that combine platform-based microlearning with scheduled live practice, maximizing both scalability and measurable proficiency outcomes. This is also influencing platform positioning strategies, with leading players expanding their offering architectures to serve learners across the full learning journey.

Expanding Corporate Language Learning Investment Driven by ESG, DEI, and Global Workforce Strategies

Corporate investment in language learning programs is growing substantially, driven by the growing strategic priority of DEI objectives, the globalization of enterprise talent pools, and the recognition of multilingual capability as a key competitive differentiator in international markets. Corporations across technology, financial services, healthcare, manufacturing, and consumer goods sectors are increasingly integrating structured language training into employee development programs, purchasing enterprise platform licenses and analytics dashboards from leading online language learning providers.

This trend is primarily pronounced in multinational organizations managing cross-functional teams across diverse linguistic geographies, where language proficiency gaps directly affect productivity, collaboration, and client-facing effectiveness. The rise of ESG-aligned corporate governance frameworks is also driving demand, as language access programs are increasingly recognized as instruments of inclusive workforce development. Enterprise clients offer higher average revenue per user and greater lifetime value compared to individual learners, making corporate segment growth a key driver of this market.

|

Market Size by 2036 |

USD 50.6 Billion |

|

Market Size in 2025 |

USD 15.8 Billion |

|

Market Size in 2026 |

USD 17.7 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 11.1% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Learning Mode: Self-learning Apps & Applications (AI-Powered Language Apps, Web-Based Platforms, Gamified Learning Apps) and Tutoring (One-on-One Online Tutoring, Group Online Tutoring, AI-Powered Virtual Tutors) By Age Group: <13 Years, 13–17 Years, 18–20 Years, 21–30 Years, 31–40 Years, >40 Years By Language: English, Spanish, French, Mandarin, German, Japanese, Korean, Arabic, Italian, Other Languages By End User: Individual Learners, Educational Institutions (K-12, Higher Education), Corporate Learners, Government Institutes By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Why Does the Self-Learning Apps and Applications Segment Dominate the Online Language Learning Market?

Based on learning mode, the self-learning apps and applications segment is expected to account for the largest share of the global online language learning market in 2026. This is primarily attributed to the widespread adoption of smartphones globally, the low cost and high accessibility of mobile learning applications, and the accelerating integration of AI personalization and gamification features that drive daily engagement and learner retention. The ease of entry for self-directed learners, including free-to-use or freemium access models offered by platforms such as Duolingo, has expanded the addressable learner base across income groups and geographies. Within the self-learning segment, AI-powered language apps segment is the fastest-growing sub-category, with generative AI enabling an unprecedented degree of personalization in vocabulary sequencing, pronunciation feedback, and contextual conversation practice.

The tutoring segment, while representing a smaller market share, is expected to grow at the fastest CAGR from 2026 to 2036. The AI-powered virtual tutor market is disrupting traditional one-on-one tutoring economics by delivering scalable conversational practice at a fraction of the cost of live human instruction. One-on-one online tutoring through platforms such as iTalki and Cambly remains highly valued for advanced learners and those requiring tailored professional or academic language development, while group online tutoring is gaining adoption within corporate training and institutional program contexts.

Why Does the 13–17 Years Segment Dominate the Online Language Learning Market?

Based on age group, the 13–17 years segment is expected to account for the largest share of the global online language learning market in 2026. The largest market share of this segment is attributed to the growing integration of online language learning into secondary school curricula across major markets, the high digital nativity of this demographic, and the increasing significance of multilingual competency for higher education access, competitive examinations such as IELTS and TOEFL, and study abroad aspirations.

Educational institutions serving this age cohort are increasingly adopting digital language learning platforms as complements to classroom instruction, driving institutional purchasing alongside individual subscription growth. The 21–30 years segment also maintains a significant market share, showing strong demand among university students and early-career professionals investing in language skills for professional advancement and international mobility.

However, the <13 years segment is projected to grow at the fastest CAGR during the forecast period, driven by growing parental investment in early language acquisition, the proven cognitive advantages of childhood language learning, the expansion of gamified and child-appropriate platform interfaces specifically designed for young learners, and increasing institutional adoption of digital language programs in K-12 primary education settings globally.

Why Does the English Language Segment Dominate the Online Language Learning Market?

Based on language, the English segment is expected to account for the largest share of the global online language learning market in 2026. The dominance of this language reflects its status as the primary language of international business, academic research, digital media, and cross-border communication, driving strong demand across all major geographies, mainly in Asia-Pacific, Latin America, and the Middle East & Africa. The proliferation of standardized English proficiency assessments, including IELTS, TOEFL, and the Duolingo English Test (DET), further drives demand for English instruction at scale.

The Spanish language is expected to grow at the fastest CAGR through 2036. This language is the third most widely used language on the internet. Additionally, the growth of Spanish-speaking populations in the U.S. and globally, and expanding learner interest in Spanish across North America, Europe, and the Asia-Pacific, further drives the growth of this market.

Why Do Individual Learners Dominate the Online Language Learning Market?

Based on end user, individual learners are expected to account for the largest share of the global online language learning market in 2026. The accessibility of consumer-facing language learning applications, including freemium platforms have successfully lowered the barrier to language learning for learners across all income segments and geographies. Individual learners are motivated by a diverse range of objectives, including travel preparation, professional development, immigration and relocation readiness, heritage language reconnection, and cognitive enrichment, creating broad and strong demand for language learning.

This segment is also expected to register strong growth during the forecast period, driven by continued expansion of smartphone access globally, rising consumer expenditure on self-directed digital education, and the compelling value proposition of AI-personalized learning experiences available at accessible subscription price points.

Asia-Pacific: Largest Regional Market and Fastest-Growing Region

Based on geography, Asia-Pacific is expected to hold the largest share of the global online language learning market in 2026 and is also projected to grow the fastest CAGR during the forecast period. This is primarily attributed to its vast and highly engaged language learner base, concentrated in China, India, Japan, South Korea, Indonesia, and Southeast Asia, combined with the rapid expansion of digital education infrastructure and high mobile internet penetration rates. Government-led initiatives to strengthen national digital education ecosystems, such as India’s National Education Policy promoting multilingual learning and China’s sustained emphasis on English proficiency within its education system are driving long-term demand.

Asia-Pacific is also home to the largest population of English language learners globally, as well as significant demand for Mandarin, Japanese, Korean, and regional languages, creating a diverse and multi-directional market for online language learning services. The rapid growth of the regional EdTech investment ecosystem, combined with the global cultural resonance of Korean and Japanese media driving demand for those languages among younger demographics, further driving the growth of online language learning market in Asia-Pacific region.

North America holds a significant market share, driven by large individual consumer and corporate learner bases, high digital education spending, and the presence of major platform operators including Duolingo, Rosetta Stone (IXL Learning), and Cambly. The diverse immigrant population pf this region also offers a strong demand for both English language acquisition and heritage language maintenance platforms.

Europe is a mature but steadily growing market, driven by the its inherently multilingual character, the EU’s institutional commitment to multilingual education policy, and strong corporate investment in language training in major markets including Germany, France, the United Kingdom, Spain, and the Netherlands. The presence of leading European platform operators such as Babbel GmbH (Germany) and Busuu Limited (U.K.) further strengthens its position in the global market.

Latin America and the Middle East & Africa are high-growth emerging regional markets, driven by increasing smartphone penetration, young and digitally engaged populations, strong demand for English proficiency as a pathway to economic mobility, and increasing government and institutional investment in digital education programs.

The report includes a competitive landscape based on an extensive assessment of the key growth strategies adopted by leading market players in the online language learning market. The key companies profiled in the report include Duolingo, Inc. (U.S.), Babbel GmbH (Germany), Rosetta Stone LLC (IXL Learning) (U.S.), EF Education First Ltd. (Switzerland), Berlitz Corporation (U.S.), Busuu Limited (U.K.), New Oriental Education & Technology Group Inc. (China), Cambridge University Press & Assessment (U.K.), Pearson plc (U.K.), McGraw Hill LLC (U.S.), Cambly Inc. (U.S.), Preply Inc. (U.S.), Lingoda GmbH (Germany), Open English (U.S./Latin America), Memrise Ltd. (U.K.), HelloTalk (China), ELSA Corp. (U.S.), Mango Languages (U.S.), iTalki (China/U.S.), inlingua International Ltd. (Switzerland), Transparent Language, Inc. (U.S.), Pimsleur (Simon & Schuster, a Paramount Global company) (U.S.), and LingoAce (Singapore), among others.

Online Language Learning Market, by Learning Mode

Online Language Learning Market, by Age Group

Online Language Learning Market, by Language

Online Language Learning Market, by End User

Online Language Learning Market, by Geography

The global online language learning market is projected to reach USD 50.6 billion by 2036 from USD 17.7 billion in 2026, growing at a CAGR of 11.1% during the forecast period of 2026 to 2036.

The self-learning apps and applications segment is expected to account for the largest share of the online language learning market in 2026, driven by widespread smartphone adoption and the increasing use of AI-powered personalization and gamification features.

The tutoring segment, particularly AI-powered virtual tutors, is projected to register the highest growth during the forecast period due to increasing demand for interactive and conversational learning experiences.

The 13–17 years segment is expected to account for the largest share of the market, supported by increasing adoption of digital learning platforms among school-age learners.

The <13 years segment is projected to register the highest growth rate during the forecast period, driven by increasing adoption of early childhood digital learning platforms.

The English language segment is expected to account for the largest share of the global online language learning market due to its widespread use in international communication, education, and business.

The Spanish language segment is projected to register one of the fastest growth rates during the forecast period due to expanding learner populations across the Americas and Europe.

The individual learners segment is expected to account for the largest share of the online language learning market due to the widespread adoption of mobile language learning applications.

The corporate learners segment is projected to register the highest CAGR during the forecast period due to increasing enterprise investment in workforce language training.

Which region is expected to dominate the online language learning market during the forecast period?

Asia-Pacific is expected to account for the largest share of the online language learning market due to its large learner population and rapid growth in digital education platforms.

Asia-Pacific is projected to register the highest CAGR during the forecast period due to expanding EdTech ecosystems and increasing demand for foreign language learning across major economies.

Key growth drivers include increasing globalization, rising demand for multilingual communication skills, advances in AI-powered language learning technologies, and growing smartphone and internet penetration worldwide.

Major opportunities include the expansion of AI-powered virtual tutors, the growth of hybrid learning models combining apps with live tutoring, and the increasing demand for corporate language training solutions.

Key innovations include generative AI-powered conversational learning, adaptive learning algorithms, speech recognition technologies, and AI-driven virtual tutors, which enable personalized and scalable language learning experiences.

Major companies operating in the online language learning market include Duolingo, Inc., Babbel GmbH, Rosetta Stone LLC (IXL Learning), EF Education First Ltd., Berlitz Corporation, Busuu Limited, New Oriental Education & Technology Group Inc., Cambridge University Press & Assessment, Pearson plc, McGraw Hill LLC, Cambly Inc., Preply Inc., Lingoda GmbH, Open English, Memrise Ltd., HelloTalk, ELSA Corp., Mango Languages, iTalki, inlingua International Ltd., Transparent Language, Inc., Pimsleur (Simon & Schuster, a Paramount Global company), and LingoAce, among others.

Leading companies are focusing on AI integration, strategic partnerships, subscription-based learning models, platform expansion, and the development of personalized learning experiences to strengthen their market positions.

Published Date: May-2025

Published Date: May-2025

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates