Resources

About Us

Nanosatellite and Microsatellite Market Size, Share, Trends by Satellite Type (Nanosatellites 1–10 kg, CubeSats 1U, 3U, 6U, 12U, Microsatellites 10–100 kg), Component, Orbit, Application, End User, Geography - Global Opportunity Analysis & Forecast 2026–2036

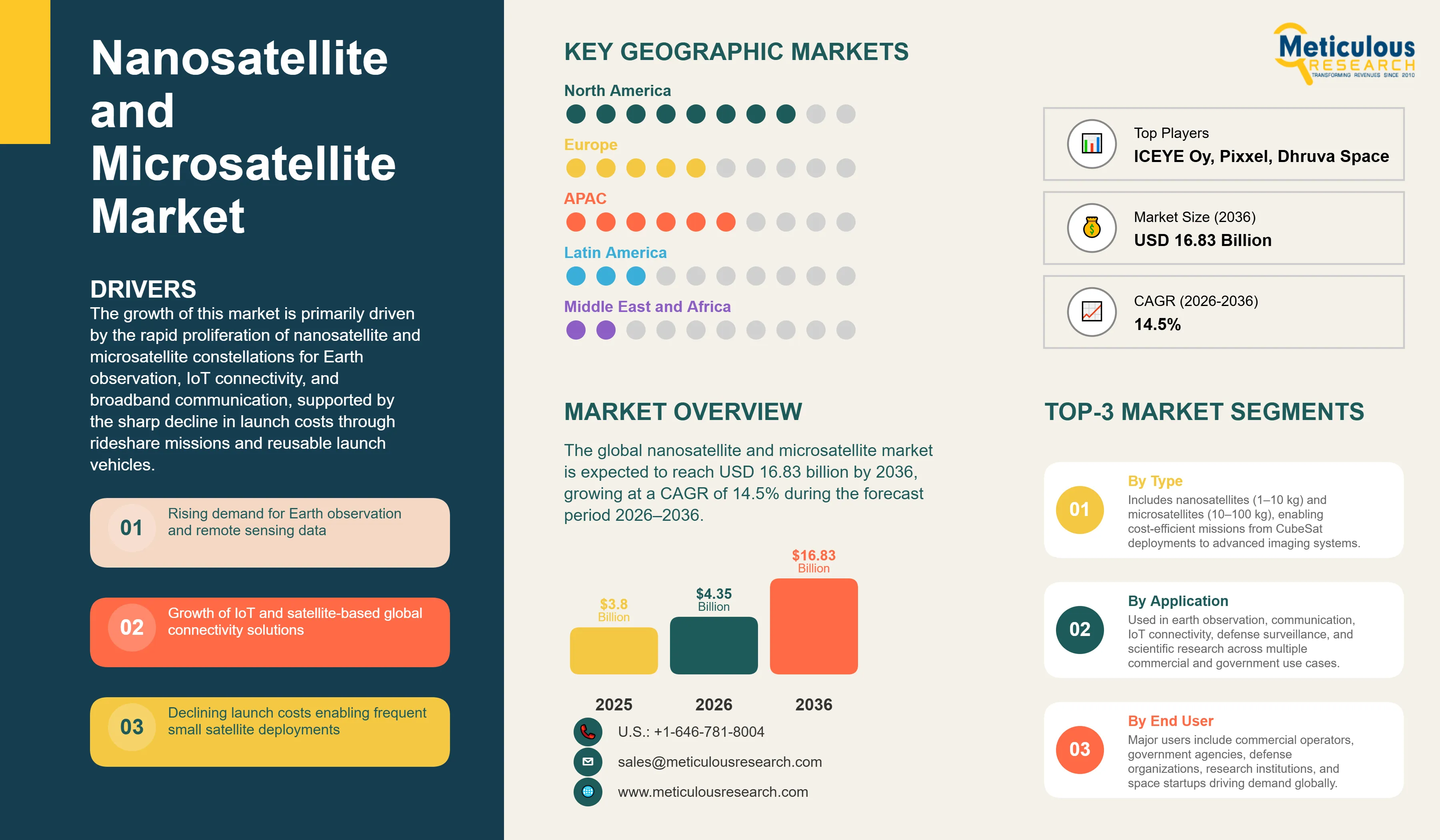

Report ID: MRAD - 1041866 Pages: 278 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global nanosatellite and microsatellite market was valued at USD 3.80 billion in 2025. This market is expected to reach USD 16.83 billion by 2036 from an estimated USD 4.35 billion in 2026, growing at a CAGR of 14.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global nanosatellite and microsatellite market encompasses compact satellite platforms across the nanosatellite mass class (1–10 kg, including CubeSats in standardized 1U to 27U configurations) and the microsatellite mass class (10–100 kg), along with associated components, subsystems, software, launch services, and downstream data services.

These satellites represent the fastest-growing segment within the broader small satellite market, driven by their low unit manufacturing costs, significantly shorter development cycles (typically 12–24 months compared to 5–10 years for conventional satellites), compatibility with cost-efficient rideshare launches, and their ability to operate in large-scale constellations. Such constellations enable high revisit rates and near-global coverage, making them highly suitable for data-intensive applications across multiple end-use sectors.

The growth of this market is primarily driven by the rapid proliferation of nanosatellite and microsatellite constellations for Earth observation, IoT connectivity, and broadband communication, supported by the sharp decline in launch costs through rideshare missions and reusable launch vehicles. Additionally, continuous miniaturization of satellite components is enabling higher mission capabilities within stringent mass, volume, and power constraints, while the adoption of standardized CubeSat form factors and modular bus architectures is facilitating faster and more cost-efficient deployment across commercial, government, academic, and defense sectors.

However, market growth is constrained by the relatively short operational lifespan and limited propulsion capabilities of nanosatellites compared to larger platforms, increasing congestion in LEO leading to collision avoidance complexities, and evolving regulatory requirements related to end-of-life deorbiting and space sustainability.

On the other hand, rising demand for defense and intelligence-driven surveillance, increasing commercialization of satellite data across agriculture, maritime monitoring, and climate analytics, and advancements in software-defined payloads and onboard AI processing are expected to create significant growth opportunities. Furthermore, the shift toward iodine-based and green propulsion systems, enabling deorbit capabilities in smaller satellite classes, is emerging as a key trend shaping the market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 16.83 Billion |

|

Market Size in 2026 |

USD 4.35 Billion |

|

Market Size in 2025 |

USD 3.80 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 14.5% |

|

Dominating Satellite Type |

Nanosatellites (1–10 kg) |

|

Fastest Growing Satellite Type |

Microsatellites (10–100 kg) |

|

Dominating Component |

Hardware |

|

Fastest Growing Component |

Software & Data Processing |

|

Dominating Orbit |

Sun-Synchronous Orbit (SSO) |

|

Fastest Growing Orbit |

Low Earth Orbit – Non-Polar Inclined |

|

Dominating Application |

Earth Observation & Remote Sensing |

|

Fastest Growing Application |

Defense, Security & Intelligence |

|

Dominating End User |

Commercial |

|

Fastest Growing End User |

Defense & Security |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Synthetic Aperture Radar Microsatellites Democratizing All-Weather Earth Observation

The commercial deployment of synthetic aperture radar (SAR) microsatellites, capable of delivering high-resolution Earth imagery independent of cloud cover and lighting conditions, a capability historically limited to large, government-operated radar satellites, represents a major advancement in the nanosatellite and microsatellite market during the forecast period.

ICEYE operates the world’s largest commercial SAR constellation, with more than 30 microsatellites delivering sub-meter resolution imagery for applications including maritime monitoring, flood mapping, defense intelligence, and infrastructure surveillance. In parallel, Capella Space, Synspective, and Satellogic are deploying competing SAR microsatellite constellations, intensifying competition and driving the commercialization of radar-based Earth observation data.

This competitive landscape is significantly reducing the cost of high-value SAR data, thereby expanding accessibility across commercial and government users. Consequently, the SAR microsatellite segment is expected to witness robust growth over 2026–2036, driven by increasing demand for persistent surveillance in defense and intelligence, real-time disaster response, and maritime domain awareness, use cases where optical imaging systems remain constrained by weather and illumination limitations.

IoT and Direct-to-Device Connectivity Driving Nanosatellite Network Deployments

The growing demand for IoT and direct-to-device connectivity is significantly driving the deployment of nanosatellite constellations. These networks enable seamless, low-power communication for sensors and devices in remote regions, where terrestrial infrastructure is limited or unavailable.

Key players such as Spire Global, Astrocast, Lacuna Space, and Sateliot are advancing nanosatellite-based IoT networks that support applications, such as asset tracking, maritime logistics, agriculture, and environmental monitoring. These solutions provide a cost-effective alternative to traditional satellite broadband, enabling scalable connectivity for low-data-rate use cases.

A key evolution within this trend is the emergence of direct-to-device connectivity, mainly through integration with terrestrial standards such as NB-IoT and LTE-M. This approach allows standard cellular devices to connect directly to satellites without specialized hardware, positioning nanosatellite networks as a critical enabler of global IoT coverage and a foundational layer in the future of hybrid terrestrial-satellite communication ecosystems.

Defense Nanosatellite Constellations for Persistent Surveillance and Rapid Revisit

The increasing adoption of nanosatellite and microsatellite constellations by defense and intelligence agencies is emerging as a major trend, driven by the need for persistent surveillance and rapid revisit capabilities. Unlike traditional large reconnaissance satellites, distributed nanosatellite constellations enable near-continuous monitoring of target areas at significantly lower cost, enhancing situational awareness and operational responsiveness.

Programs led by organizations such as the National Reconnaissance Office, along with initiatives from the U.K. Ministry of Defence (including the Juno program with Surrey Satellite Technology Ltd), Australia’s Buccaneer program, and Japan’s defense satellite developments, highlight the expanding global procurement of small satellite-based intelligence systems.

This shift reflects a broader move toward resilient, disaggregated space architectures that reduce single-point vulnerabilities while improving coverage and data refresh rates. As a result, the defense and security segment is expected to register the highest growth within the nanosatellite and microsatellite market, driven by increasing investments in space-based ISR (intelligence, surveillance, and reconnaissance) capabilities and the strategic importance of real-time geospatial intelligence.

By Satellite Type: In 2026, the Nanosatellites Segment to Dominate the Global Nanosatellite and Microsatellite Market

Based on satellite type, the global nanosatellite and microsatellite market is segmented into nanosatellites (1–10 kg, including CubeSats) and microsatellites (10–100 kg).

In 2026, the nanosatellites segment is expected to account for the largest share of the global nanosatellite and microsatellite market. This dominance is primarily driven by significantly higher deployment volumes, supported by commercial Earth observation operators such as Planet Labs, IoT connectivity providers including Spire Global and Astrocast, as well as defense-led technology demonstration programs.

Compared to microsatellites, nanosatellites leverage lower manufacturing costs and faster deployment cycles, enabling large-scale constellation rollouts. Furthermore, CubeSat standardization has enabled the development of an open and interoperable ecosystem, allowing cost-effective and rapid mission development for universities, startups, and emerging space nations.

However, the microsatellites segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing commercial deployment of SAR imaging microsatellites by players such as ICEYE, Capella Space, and Synspective. In addition, rising demand for higher-performance payloads in defense and intelligence applications, where CubeSat platforms face limitations in mass, power, and payload capacity, is driving the adoption of microsatellite-class systems. The growth of this segment is also driven by the deployment of advanced narrowband and broadband communication microsatellites supporting IoT and LEO connectivity constellations.

By Component: In 2026, the Hardware Segment to Account for the Largest Share

Based on component, the global nanosatellite and microsatellite market is segmented into hardware (payloads, satellite bus, propulsion systems, power systems, communication subsystems, ADCS, thermal control, and C&DH), software and data processing, launch services, and space services.

In 2026, the hardware segment is expected to account for the largest share of the market. This dominance is attributed to the substantial revenue contribution of satellite hardware procurement, particularly imaging payloads, SAR systems, communication transponders, and CubeSat bus platforms, which account for the highest-value components per satellite and scale directly with the increasing volume of nanosatellite and microsatellite deployments.

However, the software and data processing segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rising commercial value of satellite-derived data analytics, including Earth observation imagery, maritime intelligence, weather analytics, and IoT data aggregation. These services generate recurring, subscription-based revenues that often exceed the initial hardware value over a satellite’s operational lifecycle. Additionally, the increasing integration of onboard AI and advanced processing software, enabling autonomous operations and real-time data insights, is further driving the growth of this market.

By Orbit Type: In 2026, the Sun-Synchronous Orbit Segment to Hold the Largest Share

Based on orbit type, the global nanosatellite and microsatellite market is segmented into sun-synchronous orbit (SSO), low Earth orbit (non-polar inclined), polar orbit, medium Earth orbit, and geostationary Earth orbit. In 2026, the sun-synchronous orbit segment is expected to account for the largest share of the global market.

This dominance is primarily attributed to the unique advantage of SSO in maintaining consistent solar illumination conditions, enabling satellites to pass over the same location at nearly identical local solar times. Such predictability is critical for Earth observation applications, particularly multispectral and optical imaging, where uniform lighting conditions are essential for accurate data comparison and analysis.

Moreover, the majority of commercial Earth observation nanosatellite constellations are deployed in SSO at altitudes ranging from 400 to 600 km, further further strengthening its leading position.

By Application: In 2026, the Earth Observation & Remote Sensing Segment to Hold the Largest Share

Based on application, the global nanosatellite and microsatellite market is segmented into Earth observation and remote sensing, communication, defense, security and intelligence, scientific research and space exploration, technology demonstration and verification, navigation and positioning, IoT and M2M connectivity, and academic training.

In 2026, the Earth observation and remote sensing segment is expected to account for the largest share of the global market. This dominance is driven by the central role of Earth observation as the primary commercial application, enabling recurring, subscription-based data revenues, alongside the highest level of global investment in nanosatellite and microsatellite constellation deployments. The expanding range of use cases, including agriculture, forestry, disaster management, urban planning, energy infrastructure monitoring, and maritime tracking, further strengthens its leading position.

However, the defense, security, and intelligence segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing strategic need for proliferated and resilient space-based surveillance and communication systems that offer lower costs and higher revisit frequencies compared to traditional large satellites. This trend is reflected in programs such as Australia’s Buccaneer initiative, the U.K. Ministry of Defence’s Juno program, and small satellite initiatives led by the United States Space Force.

By End User: In 2026, the Commercial Segment to Account for the Largest Share

Based on end user, the global nanosatellite and microsatellite market is segmented into commercial, government, defense and security, civil, academic and research, and energy and infrastructure. In 2026, the commercial segment is expected to account for the largest share of the global market, driven by the leading role of private operators, including Earth observation companies, IoT connectivity providers, and constellation developers, as the primary procurers of nanosatellite and microsatellite platforms by volume. The rapid expansion of the commercial space ecosystem, characterized by the emergence of numerous startups alongside established players, is further supporting large-scale deployments across diverse revenue-generating applications.

However, the defense and security segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing strategic emphasis among defense agencies on proliferated nanosatellite and microsatellite constellations, which offer enhanced situational awareness, improved communications resilience, and greater resistance to anti-satellite threats compared to traditional large satellite systems. This shift is demonstrated by expanding procurement programs and long-term investments across key markets, including the U.S., U.K., Australia, Japan, and increasingly France, Germany, and India.

Based on geography, the global nanosatellite and microsatellite market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of the global nanosatellite and microsatellite market.

This dominance is driven by the high concentration of commercial nanosatellite and microsatellite operators, such as Planet Labs, Spire Global, BlackSky, Capella Space, Swarm Technologies, and Terran Orbital. The growth of this region is further driven by the strong and ongoing government investments through programs led by NASA, DARPA, and the United States Space Force, particularly focused on proliferated LEO constellations, technology demonstration missions, and commercial rideshare initiatives. In addition, the presence of a mature satellite manufacturing and component ecosystem, driven by leading players such as Blue Canyon Technologies and Rocket Lab, further strengthens the region’s market leadership.

However, Asia Pacific nanosatellite and microsatellite market is expected to register the highest CAGR during the forecast period. This growth is driven by the rapid expansion of national and commercial space programs across key countries. India is emerging as a high-growth market, supported by regulatory liberalization through IN-SPACe, enabling private sector participation by companies such as Pixxel and Dhruva Space in Earth observation and IoT nanosatellite deployments. China continues to advance aggressive domestic constellation development through China Aerospace Science and Technology Corporation and a growing base of commercial operators, reflecting a hybrid state-commercial expansion model.

Furthermore, Japan’s evolving commercial nanosatellite ecosystem, led by Axelspace and Institute for Q-shu Pioneers of Space, alongside South Korea’s increasing investments in indigenous satellite capabilities, is contributing to the regional growth. Collectively, these developments position the Asia Pacific as the fastest-growing regional market for nanosatellite and microsatellite over the forecast period.

The global nanosatellite and microsatellite market is characterized by a highly fragmented competitive landscape comprising commercial Earth observation operators, standardized satellite bus manufacturers, defense-focused integrators, and subsystem providers.

Planet Labs leads the commercial nanosatellite Earth observation segment in terms of constellation scale and data-driven revenue generation. ICEYE holds a leading position in the SAR microsatellite segment, driven by its extensive constellation and advanced analytics offerings. In the satellite platform domain, GomSpace and NanoAvionics specialize in modular CubeSat and small satellite bus solutions, enabling rapid and cost-effective mission deployment across commercial and academic users.

Surrey Satellite Technology Ltd maintains a strong presence in government and defense-oriented microsatellite missions, while companies such as AAC Clyde Space, Axelspace, and Terran Orbital are actively competing across Earth observation, communications, and technology demonstration segments.

The report provides a comprehensive competitive assessment based on the detailed analysis of key players’ product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Key players operating in the global nanosatellite and microsatellite market include Planet Labs (U.S.), ICEYE (Finland), Spire Global (U.S.), GomSpace (Denmark), NanoAvionics (Lithuania/U.S.), Surrey Satellite Technology Ltd (U.K.), AAC Clyde Space (Sweden), Axelspace (Japan), Terran Orbital (U.S.), BlackSky (U.S.), Satellogic (Argentina/U.S.), Capella Space (U.S.), L3Harris Technologies (U.S.), Sierra Space (U.S.), and Tyvak Nano-Satellite Systems (U.S.), among others.

The global nanosatellite and microsatellite market is expected to reach USD 16.83 billion by 2036 from an estimated USD 4.35 billion in 2026, at a CAGR of 14.5% during the forecast period 2026–2036.

In 2026, the nanosatellites segment is expected to hold the largest share of approximately 62% of the global nanosatellite and microsatellite market, driven by the highest deployment volumes from commercial Earth observation constellations and IoT connectivity providers.

The microsatellites segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the expanding deployment of SAR imaging microsatellites and defense intelligence microsatellite programs.

In 2026, the earth observation and remote sensing segment is expected to hold the largest share of approximately 47% of the global nanosatellite and microsatellite market.

The defense, security and intelligence segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by proliferated surveillance nanosatellite constellation procurement by defense agencies across the U.S., U.K., Australia, and Japan.

What are the major factors driving the growth of the global nanosatellite and microsatellite market?

The growth of this market is primarily driven by the rapid expansion of nanosatellite and microsatellite constellations for Earth observation, IoT connectivity, and broadband communication services; the dramatic decline in launch costs through rideshare programs; and the growing adoption of standardized CubeSat form factors enabling rapid, cost-effective mission deployment. Key opportunities include SAR microsatellite democratization of all-weather Earth observation, IoT direct-to-device nanosatellite networks, and defense proliferated surveillance constellation programs.

Key players are Planet Labs PBC (U.S.), ICEYE Oy (Finland), Spire Global, Inc. (U.S.), GomSpace Group AB (Denmark), NanoAvionics Corp. (Lithuania/U.S.), Surrey Satellite Technology Ltd. (U.K.), AAC Clyde Space AB (Sweden), Axelspace Corporation (Japan), Terran Orbital Corporation (U.S.), BlackSky Technology Inc. (U.S.), Satellogic Inc. (Argentina/U.S.), Capella Space Corp. (U.S.), L3Harris Technologies, Inc. (U.S.), Sierra Space Corporation (U.S.), and Tyvak Nano-Satellite Systems, LLC (U.S.).

Asia Pacific is expected to register the highest growth rate in the global nanosatellite and microsatellite market during the forecast period 2026–2036, with India expected to register the highest country-level CAGR driven by IN-SPACe liberalization and rapid commercial ecosystem growth.

Published Date: Feb-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates