Resources

About Us

Global Moisture Sensors Market Size, Share & Trends Analysis, by Sensor Type (Capacitive, Resistive, Optical, Microwave, Thermal Conductivity), Output Type (Analog, Digital), End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

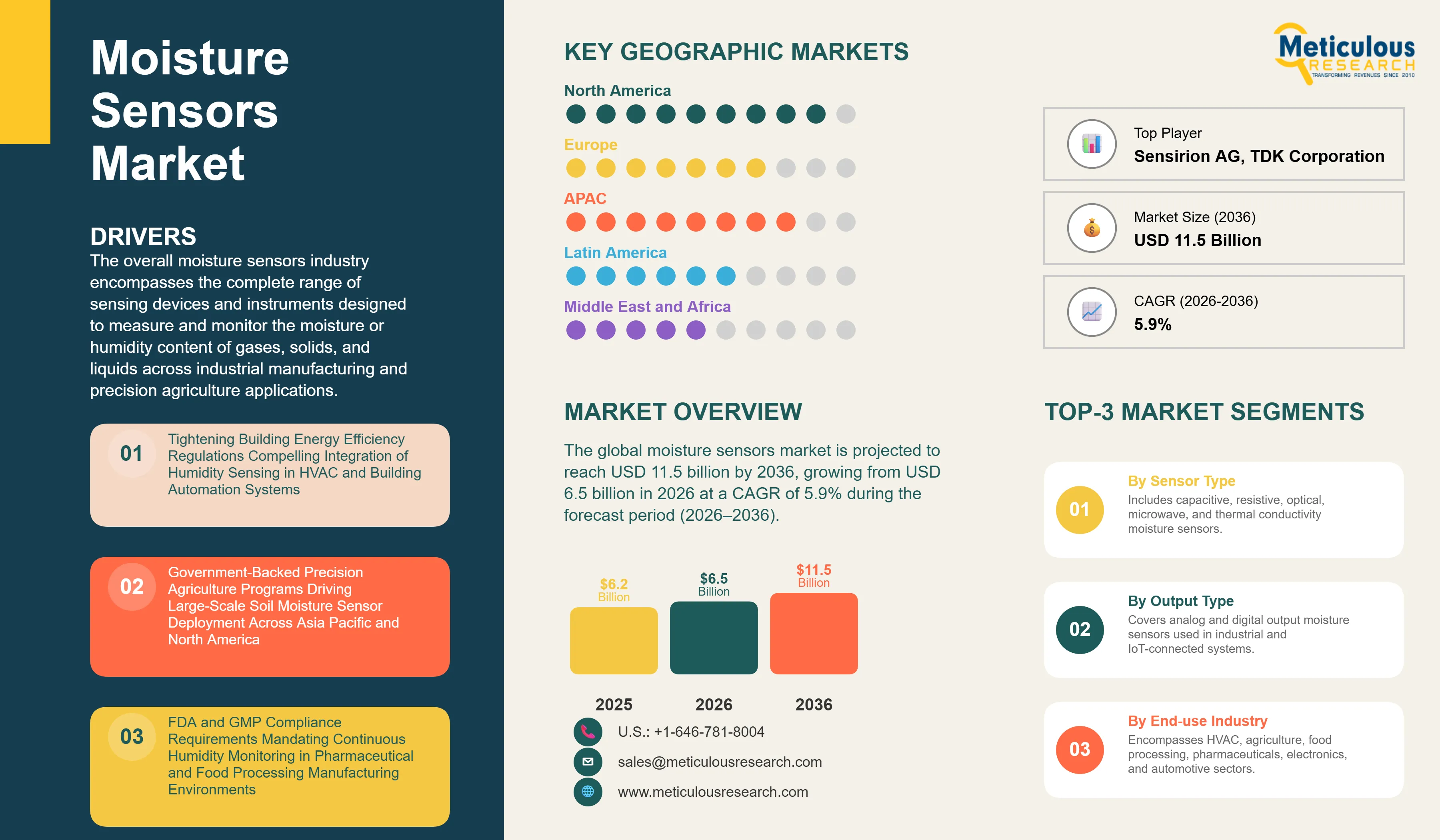

Report ID: MRSE - 1041982 Pages: 297 May-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global moisture sensors market was valued at USD 6.2 billion in 2025. The market is projected to reach USD 11.5 billion by 2036, growing from USD 6.5 billion in 2026 at a CAGR of 5.9% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall moisture sensors industry encompasses the complete range of sensing devices and instruments designed to measure and monitor the moisture or humidity content of gases, solids, and liquids across industrial manufacturing, process control, environmental monitoring, building automation, and precision agriculture applications. The market includes capacitive moisture sensors, resistive moisture sensors, optical moisture sensors operating across near-infrared and mid-infrared wavelengths, microwave moisture sensors, and thermal conductivity-based sensors deployed across a broad range of end-use industries including building automation and HVAC, agriculture and horticulture, food and beverage processing, pharmaceutical and healthcare, electronics and semiconductor manufacturing, automotive, oil and gas, and environmental monitoring and meteorology.

Moisture sensors serve as critical measurement components in applications where excess or insufficient moisture directly affects product quality, process stability, equipment reliability, occupant comfort, regulatory compliance, or energy efficiency. These sensors are deployed as discrete sensing elements embedded in OEM products, as stand-alone measurement transmitters for process control, as wireless nodes in agricultural field monitoring networks, and as integrated modules within building management systems and industrial IoT platforms. Products are available in both analog output configurations using voltage and current interfaces for compatibility with legacy instrumentation and digital output configurations using I2C, SPI, RS-485, and wireless protocols for integration with modern connected systems.

the growth of the moisture sensors market is driven by the convergence of three macro‑level forces the tightening of energy efficiency and food‑safety regulations across major industrial economies, the large‑scale global adoption of precision agriculture practices supported by government policy in Asia Pacific, North America, and Europe, and the proliferation of IoT‑connected devices and smart building platforms that require reliable, low‑cost humidity sensing as a foundational measurement input; in the building sector, the revised EU Energy Performance of Buildings Directive (Directive 2024/1275), which entered into force on May 28, 2024, sets a zero‑emission‑performance trajectory for new buildings from 2030, which translates in practice into a sustained renovation and construction cycle that embeds integrated humidity sensing across heating, ventilation, and air conditioning systems; in the food and pharmaceutical sectors, regulatory frameworks such as FDA’s Current Good Manufacturing Practice standards under 21 CFR Part 211 and the Food Safety Modernization Act’s Preventive Controls for Human Food rule require manufacturers to monitor and document environmental humidity conditions as a core element of process quality and compliance, even if the wording does not always explicitly mandate “humidity sensors” by name.

In addition to regulatory compliance, the growing deployment of industrial IoT platforms, edge computing nodes, and cloud-connected process monitoring systems is reshaping procurement patterns across the moisture sensor supply chain, with demand shifting progressively toward digital output sensor modules that can integrate directly into connected data architectures without additional signal conditioning hardware. The integration of multi-parameter sensing capability into single-package devices combining relative humidity, temperature, CO2, and volatile organic compound measurement is further expanding the total addressable market for moisture sensing technology by delivering additional sensing value within the same physical and cost envelope as a traditional single-parameter humidity sensor.

Despite strong structural growth drivers, the market faces challenges associated with sensor drift and long-term measurement accuracy degradation in harsh environments, including applications involving chemical exposure, extreme temperature cycling, condensation, or contamination by process dust and aerosols. The calibration and recertification requirements embedded in pharmaceutical GMP and food safety compliance frameworks impose additional lifecycle costs that influence procurement decisions in these regulated sectors. Additionally, the commoditization of capacitive sensor technology in high-volume consumer and IoT markets has intensified price pressure across the sensor supply chain, compressing margins for manufacturers that lack the product differentiation provided by advanced packaging, multi-parameter integration, or application-specific calibration capabilities.

The growing complexity of building energy efficiency mandates across major construction markets is creating significant commercial opportunities for sensor manufacturers that can deliver integrated multi-parameter environmental sensing modules combining humidity, temperature, CO2, and particulate measurement in a single platform compatible with major building management system standards. The rapid expansion of precision agriculture infrastructure across Asia Pacific and Latin America, where government subsidy programs are actively reducing the cost of adoption for smallholder and mid-size farming operations, is creating a structurally new growth segment for low-cost wireless soil moisture sensing solutions. The accelerating adoption of Industry 4.0 connected manufacturing platforms in automotive, electronics, and pharmaceutical production facilities is similarly creating sustained demand for high-accuracy, digitally integrated moisture sensing solutions capable of meeting the data quality and connectivity requirements of modern industrial process analytics systems.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 11.5 Billion |

|

Market Size in 2026 |

USD 6.5 Billion |

|

Market Size in 2025 |

USD 6.2 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.9% |

|

Dominating Sensor Type |

Capacitive Moisture Sensors |

|

Fastest Growing Sensor Type |

Optical Moisture Sensors |

|

Dominating Output Type |

Analog Output |

|

Fastest Growing Output Type |

Digital Output |

|

Dominating End-use Industry |

Building Automation & HVAC |

|

Fastest Growing End-use Industry |

Agriculture & Horticulture |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Global Food Security Imperatives and Government-Backed Precision Agriculture Programs Accelerating Soil Moisture Sensor Deployment

The combination of rising global food demand, intensifying water scarcity, and coordinated government policy mandating sustainable agricultural water use is fundamentally reshaping the adoption profile of soil moisture sensors across the agricultural sector. The Food and Agriculture Organization of the United Nations has long established that agriculture accounts for approximately 70 percent of global freshwater withdrawals, and this structural reality has placed soil moisture monitoring at the center of national irrigation management strategies across major agricultural economies. The resulting policy response is translating into direct and sustained demand for soil moisture sensing hardware across both developed market and emerging market agricultural geographies.

In the United States, the USDA Natural Resources Conservation Service has expanded its Environmental Quality Incentives Program and the Regional Conservation Partnership Program to include cost-share assistance for agricultural producers adopting soil moisture monitoring equipment as part of approved irrigation water management plans, directly subsidizing precision sensing hardware procurement across the country's major irrigated crop production regions. These programs reflect the federal government's recognition that sensor-driven irrigation management represents one of the most cost-effective interventions for achieving measurable water savings at scale across the U.S. agricultural sector.

In India, the Pradhan Mantri Krishi Sinchayee Yojana scheme, which operates under the Ministry of Agriculture and Farmers' Welfare with the stated objective of achieving Har Khet Ko Pani (water to every field) and More Crop Per Drop, has progressively expanded to integrate soil moisture monitoring as a component of micro-irrigation system adoption across smallholder farming operations. The scheme has supported the installation of drip and sprinkler irrigation systems across tens of millions of hectares, and the convergence of this infrastructure buildout with the government's broader Digital Agriculture Mission is creating a policy-backed demand pipeline for affordable capacitive soil moisture sensors suited to smallholder deployment contexts. China's 14th Five-Year Plan for Agricultural and Rural Development explicitly identified smart irrigation and precision water management as priority areas, with provincial governments implementing targeted subsidy programs for IoT-connected soil moisture monitoring equipment across major grain-producing regions including Heilongjiang, Henan, and Shandong provinces.

The European Union’s Common Agricultural Policy reform for 2023–2027 is strengthening the link between area‑based payments and farm‑level sustainability measures, including the use of digital tools and data to support soil health and nutrient‑management practices; while current EU guidance emphasizes eco‑schemes and digital advisory platforms rather than a blanket legal mandate specifically for “soil moisture monitoring,” national and regional implementations are increasingly tying compliance‑linked conditionality to soil‑health and precision‑irrigation systems that incorporate soil moisture sensing, effectively creating a policy‑driven rationale for adoption that extends beyond voluntary efficiency gains into routine record‑keeping. At the technology level, the convergence of low‑cost capacitive soil moisture sensors with LoRaWAN, NB‑IoT, and Zigbee connectivity platforms is enabling the deployment of dense field‑monitoring networks at cost points that were commercially impractical five years ago; companies including METER Group, Campbell Scientific, and Delta‑T Devices are advancing IoT‑ready soil moisture sensor platforms designed for large‑scale rollout in both developed and emerging‑market agricultural settings, while semiconductor manufacturers such as Texas Instruments and Silicon Laboratories are developing ultra‑low‑power sensor‑interface chipsets that extend battery life in wireless soil‑sensing nodes to multi‑year horizons with minimal maintenance.

Revised EU Energy Performance of Buildings Directive and Global Smart Building Mandates Driving Humidity Sensor Integration Across HVAC and Indoor Air Quality Monitoring Systems

The buildings sector represents one of the most structurally significant and rapidly evolving demand drivers in the global moisture sensors market. Buildings account for approximately 30 percent of global final energy consumption according to the International Energy Agency, a substantial share of which is attributable to heating, ventilation, and air conditioning systems that require precise, continuous humidity sensing for effective energy management and occupant comfort optimization. The accelerating legislative response to this energy intensity across major construction markets is establishing mandatory demand for integrated humidity sensing in both new construction and retrofit applications at a scale that is materially expanding the addressable market for building-grade moisture sensing technology.

The revised EU Energy Performance of Buildings Directive (Directive 2024/1275), which entered into force on May 28, 2024, is the most consequential regulatory development in the European building automation sensor market in a generation. The revised directive requires all new buildings to achieve zero-emission performance from January 1, 2030, with new public buildings required to meet this standard from January 1, 2028. Member States are required to establish minimum energy performance standards and national renovation trajectories for the worst-performing existing building stock, creating a multi-decade cycle of system upgrades that incorporates modern HVAC platforms with integrated humidity and indoor air quality monitoring as a standard design element. The Smart Readiness Indicator framework embedded in the revised directive explicitly includes humidity and CO2 monitoring capability as criteria within a building's smart readiness assessment, directly incentivizing sensor integration by developers and building owners seeking to maximize asset valuation under the updated regulatory framework.

In North America, ASHRAE Standard 55-2023 on Thermal Environmental Conditions for Human Occupancy and ASHRAE Standard 62.1-2022 on Ventilation and Acceptable Indoor Air Quality establish specific relative humidity range requirements for occupied commercial and institutional spaces, underpinning moisture sensor procurement in commercial building HVAC systems as a baseline compliance investment. Green building certification programs including LEED v4.1 and WELL Building Standard v2 award credits for continuous indoor environmental monitoring that explicitly includes humidity measurement as a scored parameter, motivating building owners targeting certification to invest in integrated sensing infrastructure beyond minimum code compliance requirements. The U.S. Department of Energy's Building Technologies Office continues to fund research and demonstration programs targeting smart sensor integration for building energy optimization, including humidity-driven HVAC control algorithms that can reduce conditioning energy consumption by a meaningful margin relative to fixed schedule-based operation.

At the product level, leading manufacturers including Honeywell International, Vaisala, and Sensirion are expanding their building automation sensor lines with multi-parameter modules that combine relative humidity, temperature, CO2, and volatile organic compound sensing in a single device, enabling HVAC systems to adjust ventilation and conditioning setpoints simultaneously in response to actual occupancy-driven environmental conditions. This convergence of environmental parameters into integrated sensing nodes is expanding the revenue opportunity for moisture sensor content in building applications beyond single-parameter duct and room sensors, while deepening integration with building management platforms and energy management software from providers including Johnson Controls, Siemens, and Schneider Electric.

Integrated Multi-Parameter Digital Sensor Modules Displacing Discrete Analog Components Across Consumer, IoT, and Industrial OEM Design Platforms

The sustained displacement of discrete, single-parameter analog moisture sensing elements by compact, multi-parameter digital sensor modules is the defining product-level technology transition reshaping the competitive landscape of the global moisture sensors market. This shift is driven fundamentally by the design architecture requirements of IoT-connected devices, smart home products, portable medical monitors, industrial wireless sensing nodes, and automotive cabin environment systems, where the combination of digital output interfaces, on-chip signal processing, factory-calibrated accuracy, and miniaturized form factor delivers decisive advantages over conventional analog sensing architectures that require external signal conditioning and periodic field recalibration.

Modern capacitive humidity sensor integrated circuits such as Sensirion's SHT4x product family, Bosch Sensortec's BME280 and BME680 multi-parameter sensors, and STMicroelectronics' HTS221 combine relative humidity and temperature measurement in a single package with digital output over I2C or SPI interfaces, eliminating external analog-to-digital conversion circuitry and enabling direct connection to host microcontrollers with minimal bill of materials impact. These devices deliver factory-calibrated measurement accuracy of plus or minus 1.5 percent relative humidity or better across their rated operating range, providing a level of long-term measurement stability and production-to-production consistency that analog sensing approaches cannot match at comparable cost points. For OEM system designers, this combination of integration, accuracy, and digital compatibility has shifted new design activity decisively away from discrete analog components toward digital module solutions across consumer electronics, smart building, medical device, and industrial sensing application categories.

The emergence of the Matter smart home connectivity standard, overseen by the Connectivity Standards Alliance and supported by platform providers including Apple, Google, and Amazon, is further accelerating digital humidity sensor adoption in residential applications by establishing standardized device type definitions for temperature and humidity sensors that enable seamless interoperability across smart home ecosystems without manufacturer-specific configuration. Matter-compliant smart thermostats, ventilation controllers, and air quality monitors integrating digital humidity sensor ICs from Sensirion, Bosch Sensortec, and STMicroelectronics are proliferating across the residential market as consumer awareness of indoor air quality has grown substantially following the elevated focus on building ventilation and environmental health that emerged in the post-pandemic period.

In the industrial OEM segment, the migration toward digital output is driven by the data format and connectivity requirements of Industry 4.0 manufacturing execution systems, predictive maintenance platforms, and cloud-based process analytics applications that require sensor data compatible with industrial IoT gateway and edge computing infrastructures. Manufacturers including Honeywell and TE Connectivity are investing in expanding their industrial-grade digital output moisture sensor offerings with enhanced electromagnetic compatibility, broader operating temperature ranges, and support for industrial communication protocols including RS-485 Modbus, IO-Link, and Bluetooth Low Energy. This technology migration is creating replacement demand for legacy analog moisture sensing infrastructure across industrial, building, and agricultural markets while simultaneously expanding the addressable market for digital sensing content by enabling new application categories that could not practically be served by earlier-generation analog sensor architectures.

By Sensor Type: In 2026, the Capacitive Moisture Sensors Segment to Dominate the Global Moisture Sensors Market

Based on sensor type, the moisture sensors industry is segmented into capacitive moisture sensors, resistive moisture sensors, optical moisture sensors, microwave moisture sensors, thermal conductivity moisture sensors, and other moisture sensors. In 2026, the capacitive moisture sensors segment is expected to account for the largest share of this market. The dominant position of this segment is attributed to the inherent technical and commercial advantages of capacitive sensing technology across the broadest range of moisture measurement applications in both gaseous and porous solid media. Capacitive humidity sensors operate by measuring changes in the dielectric properties of a hygroscopic polymer film sandwiched between two electrodes as the film absorbs and releases water vapor in proportion to the ambient relative humidity, delivering a reliable, repeatable measurement signal with low hysteresis, fast response time, and excellent long-term stability. These characteristics, combined with high compatibility with CMOS semiconductor manufacturing processes and the availability of fully integrated sensor IC solutions from leading suppliers including Sensirion, STMicroelectronics, Bosch Sensortec, and Honeywell, have established capacitive technology as the sensor architecture of choice across building automation, consumer electronics, pharmaceutical environmental monitoring, automotive cabin sensing, and agricultural applications.

However, the optical moisture sensors segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the expanding adoption of near-infrared and mid-infrared optical sensing technology in inline, non-contact industrial moisture measurement applications where the limitations of contact-based sensing architectures create significant operational challenges. In food processing, pharmaceutical manufacturing, and paper and pulp production, optical moisture sensors enable continuous, real-time measurement of moisture content in moving product streams on production lines without physical contact with the material, eliminating contamination risks, reducing measurement lag associated with sample extraction and laboratory analysis, and enabling closed-loop moisture control that improves product consistency and reduces energy consumption in drying processes. Leading suppliers of industrial optical moisture sensing solutions including Vaisala and Yokogawa Electric Corporation are expanding their inline NIR and process moisture analyzer portfolios to address a growing range of production environments where the operational advantages of optical measurement are generating compelling returns on sensor investment.

By Output Type: In 2026, the Analog Output Segment to Hold the Largest Share

Based on output type, the moisture sensors industry is segmented into analog output moisture sensors and digital output moisture sensors. In 2026, the analog output segment is expected to account for the largest share of this market. The leading position of this segment reflects the deep entrenchment of analog output moisture sensing infrastructure across large industrial sectors including process manufacturing, heavy industry HVAC, oil and gas, and utility-scale power generation, where decades of installed base accumulation in 4-20mA current loop and 0-10V voltage output process instrumentation architectures has established analog connectivity as the prevailing field wiring standard. Established manufacturers including Honeywell, Vaisala, E+E Elektronik, and Amphenol Advanced Sensors continue to maintain extensive analog output product lines specifically addressing the industrial process control and building automation segments where compatibility with existing programmable logic controllers, distributed control systems, and field device wiring infrastructure is a non-negotiable procurement criterion.

However, the digital output segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating adoption of I2C and SPI interface sensor modules in IoT-connected device platforms, smart building sensor nodes, wearable health monitors, and industrial wireless sensing infrastructure, where digital integration eliminates the need for external analog signal conditioning hardware while enabling factory-calibrated accuracy and on-chip diagnostics that are not achievable in conventional analog architectures. The proliferation of low-cost microcontroller platforms, single-board computing systems, and IoT module reference designs optimized for I2C sensor connectivity is continuously expanding the design ecosystem that makes digital moisture sensor adoption straightforward for OEM system developers across consumer, industrial, and agricultural application domains.

By End-use Industry: In 2026, the Building Automation & HVAC Segment to Hold the Largest Share

Based on end-use industry, the moisture sensors industry is segmented into building automation and HVAC, agriculture and horticulture, food and beverage processing, pharmaceutical and healthcare, electronics and semiconductor manufacturing, automotive, oil and gas, environmental monitoring and meteorology, and other end-use industries. In 2026, the building automation and HVAC segment is expected to account for the largest share of this market, reflecting the ubiquitous deployment of humidity sensors across residential, commercial, and industrial buildings globally as a fundamental requirement for HVAC control, indoor air quality management, condensation prevention, and building energy optimization. Every building equipped with a modern HVAC system or building management platform requires at least one moisture sensing point, and complex commercial and institutional buildings routinely deploy multiple sensing nodes across different zones, floors, and air handling units. The combination of a vast global installed building stock, continuous new construction activity in developing markets, and the accelerating renovation of existing buildings driven by energy efficiency mandates across North America and Europe sustains this segment's position as the largest end-use revenue category for moisture sensors. The rising global awareness of indoor air quality as a public health concern is additionally driving demand for room-level humidity monitoring in schools, hospitals, data centers, and office buildings beyond the minimum requirements established by HVAC design standards.

However, the agriculture and horticulture segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the large-scale global adoption of precision irrigation and smart farming practices, supported by direct government subsidy programs in India, China, the United States, and the European Union that are actively reducing the cost of soil moisture sensor adoption for farming operations of all scales. The rapid expansion of controlled environment agriculture, including commercial greenhouse production, vertical farming facilities, and hydroponic and aeroponic growing systems, is creating a fast-growing category of indoor agricultural applications requiring continuous soil or substrate moisture monitoring for crop quality optimization, water use efficiency, and automated fertigation control. The rising deployment of low-cost wireless sensor networks using LoRaWAN and NB-IoT connectivity is enabling the coverage of large field areas with dense soil moisture monitoring at cost points that are commercially viable for mid-size and large farming operations, creating a new volume market for affordable capacitive soil moisture sensor hardware.

Based on geography, the overall moisture sensors market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This position is supported by the most advanced and densely adopted smart building, precision agriculture, pharmaceutical manufacturing, and food safety compliance infrastructure among all global regions, creating deep and multi-sector demand for moisture sensing technology across a broad range of application categories simultaneously. The United States benefits from well-developed regulatory frameworks including ASHRAE standards governing indoor humidity conditions in commercial buildings, FDA GMP and FSMA rules requiring continuous environmental monitoring in pharmaceutical and food manufacturing environments, and USDA precision agriculture programs providing cost-share support for soil moisture sensor adoption. The concentration of leading moisture sensor manufacturers including Honeywell International, Amphenol Corporation, METER Group, Texas Instruments, and Silicon Laboratories within the North American market ensures a deep local supply chain and strong technical support infrastructure. The large installed base of aging analog output moisture sensing infrastructure across commercial HVAC, food processing, and pharmaceutical manufacturing sectors is additionally generating substantial replacement and technology upgrade demand as facility operators transition to digital-output, IoT-compatible sensing platforms.

However, the Asia Pacific moisture sensors market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the combined effect of large-scale agricultural modernization programs, massive electronics and semiconductor manufacturing capacity, rapidly expanding pharmaceutical and food processing production, and accelerating smart building adoption across China, India, Japan, South Korea, and Southeast Asian markets. China's 14th Five-Year Plan for Agricultural and Rural Development and its associated provincial-level smart irrigation subsidy programs are driving high-volume soil moisture sensor procurement across the world's largest agricultural economy. India's Pradhan Mantri Krishi Sinchayee Yojana scheme and its Digital Agriculture Mission are similarly supporting large-scale deployment of connected moisture monitoring infrastructure across the country's extensive irrigated farmland. In the building sector, China's rapidly expanding commercial real estate stock and the country's push toward energy-efficient green building standards under its national carbon neutrality commitments are driving accelerated integration of humidity sensing into modern building management systems across tier-one and tier-two cities. The concentration of global electronics and semiconductor manufacturing in Japan, South Korea, Taiwan, and China creates a large and captive demand base for high-precision humidity sensors required to maintain controlled cleanroom environments where humidity deviations can damage sensitive wafers and components. Manufacturers with strong Asia Pacific distribution networks including Murata Manufacturing, TDK Corporation, Renesas Electronics, and Panasonic Holdings are well-positioned to serve the growing regional demand across both high-volume consumer electronics and expanding industrial and agricultural application categories.

Europe is a large and well-established market for moisture sensors, underpinned by a stringent regulatory environment that includes the revised Energy Performance of Buildings Directive adopted in 2024, the EU Common Agricultural Policy reform with its Farm Sustainability Tool requirements, the EU GMP guidelines for pharmaceutical manufacturing, and national-level occupational health regulations governing workplace environmental monitoring. European manufacturers including Sensirion AG, TE Connectivity Ltd., Vaisala Oyj, E+E Elektronik GmbH, IST AG, Bosch Sensortec GmbH, and STMicroelectronics N.V. maintain globally leading positions in moisture sensor technology, particularly in high-accuracy capacitive sensing elements and integrated multi-parameter digital sensor modules, supported by deep application engineering expertise and long-standing relationships with European industrial, automotive, and building automation OEM customers.

Latin America and the Middle East and Africa represent smaller but growing markets for moisture sensors, with growth primarily driven by agricultural modernization and infrastructure development activity. Brazil's large agricultural export sector, supported by the Ministry of Agriculture's precision farming digitalization programs, is creating growing demand for soil moisture sensing in soy, sugar cane, and coffee production regions. In the Middle East, the combination of extreme climate conditions, large-scale building construction activity, and rapidly expanding food and pharmaceutical manufacturing capacity is supporting growing adoption of high-performance moisture sensing technology suited to high-temperature and high-humidity operating environments.

The global moisture sensors market is moderately consolidated at the sensor technology level, with competition primarily driven by measurement accuracy and long-term calibration stability, sensing technology type and operating range, digital output interface compatibility, multi-parameter integration capability, application-specific packaging and environmental protection ratings, and the strength of global OEM customer relationships and distribution infrastructure.

Broad-based industrial technology and sensor manufacturers such as Honeywell International Inc. and TE Connectivity Ltd. compete through comprehensive product portfolios spanning capacitive, optical, and thermal conductivity sensing technologies across analog and digital output configurations, global distribution networks, and strong positions across building automation, industrial, and process sensing customer segments. Specialist MEMS sensor IC manufacturers including Sensirion AG and STMicroelectronics N.V. compete on the strength of their proprietary CMOS-compatible MEMS fabrication capabilities, factory-calibrated multi-parameter sensor modules, and deep integration into high-volume consumer electronics, IoT, and smart building OEM supply chains. Process and environmental measurement specialists including Vaisala Oyj and E+E Elektronik GmbH compete through application-specific expertise in demanding industrial, laboratory, and meteorological moisture measurement environments where long-term calibration accuracy and traceability to national standards are differentiating capabilities. Agricultural moisture sensing specialists including METER Group, Inc. provide purpose-built soil moisture sensor platforms with companion data management and irrigation scheduling software that position them as comprehensive precision agriculture solutions providers rather than pure sensor hardware suppliers, strengthening customer retention and creating recurring service revenue streams.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global moisture sensors market include Honeywell International Inc. (U.S.), Sensirion AG (Switzerland), TE Connectivity Ltd. (Switzerland), Amphenol Corporation (U.S.), STMicroelectronics N.V. (Switzerland), Bosch Sensortec GmbH (Germany), Vaisala Oyj (Finland), E+E Elektronik GmbH (Austria), IST AG (Switzerland), Murata Manufacturing Co., Ltd. (Japan), TDK Corporation (Japan), METER Group, Inc. (U.S.), Silicon Laboratories Inc. (U.S.), Texas Instruments Incorporated (U.S.), and Panasonic Holdings Corporation (Japan), among others.

The global moisture sensors market is expected to reach USD 11.5 billion by 2036 from an estimated USD 6.5 billion in 2026, at a CAGR of 5.9% during the forecast period 2026–2036.

In 2026, the capacitive moisture sensors segment is expected to hold the largest share of this market, driven by its broad applicability across building automation, consumer electronics, pharmaceutical environmental monitoring, agricultural sensing, and industrial process control due to its low power consumption, high measurement accuracy, and CMOS fabrication compatibility.

The optical moisture sensors segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the growing adoption of near-infrared and mid-infrared sensing technology for inline, non-contact moisture measurement in food processing, pharmaceutical manufacturing, and paper and pulp production applications.

In 2026, the analog output segment is expected to hold the largest share of this market, reflecting the large installed base of analog output moisture sensing infrastructure across legacy industrial process control, heavy industry HVAC, and agricultural applications compatible with 4-20mA and 0-10V field wiring architectures.

In 2026, the building automation and HVAC segment is expected to hold the largest share of this market, reflecting the ubiquitous deployment of humidity sensors in residential, commercial, and industrial buildings globally as a foundational requirement for HVAC control, indoor air quality management, and building energy optimization.

The agriculture and horticulture segment is projected to register the highest CAGR during the forecast period, driven by the large-scale adoption of precision irrigation and smart farming practices across Asia Pacific, North America, and Europe supported by government subsidy programs, and the rapid expansion of controlled environment agriculture requiring continuous substrate moisture monitoring for automated fertigation and crop quality management.

The growth of this market is primarily driven by the tightening of building energy efficiency regulations globally including the revised EU Energy Performance of Buildings Directive, the large-scale expansion of government-backed precision agriculture programs across Asia Pacific, North America, and Europe, the accelerating shift toward digital output multi-parameter sensor modules in IoT-connected device and smart building platforms, FDA and GMP compliance requirements mandating continuous humidity monitoring in pharmaceutical and food processing manufacturing environments, and the growing adoption of inline optical moisture sensing for real-time process control in food, pharmaceutical, and industrial production applications.

Key players in the global moisture sensors market include Honeywell International Inc. (U.S.), Sensirion AG (Switzerland), TE Connectivity Ltd. (Switzerland), Amphenol Corporation (U.S.), STMicroelectronics N.V. (Switzerland), Bosch Sensortec GmbH (Germany), Vaisala Oyj (Finland), E+E Elektronik GmbH (Austria), IST AG (Switzerland), Murata Manufacturing Co., Ltd. (Japan), TDK Corporation (Japan), METER Group, Inc. (U.S.), Silicon Laboratories Inc. (U.S.), Texas Instruments Incorporated (U.S.), and Panasonic Holdings Corporation (Japan).

Asia Pacific is expected to register the highest growth rate in the global moisture sensors market during the forecast period 2026–2036, driven by large-scale agricultural modernization programs in China and India, rapidly expanding electronics and pharmaceutical manufacturing capacity, and accelerating smart building adoption across the region's major urban economies.

Published Date: Mar-2026

Published Date: Jan-2025

Published Date: Oct-2024

Published Date: Jul-2024

Published Date: Jan-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates