Resources

About Us

Wireless Industrial Sensors Market by Sensor Type (Temperature, Pressure, Flow, Level), Communication Protocol, End-User Industry (Oil & Gas, Chemical & Petrochemical, Food & Beverage), and Application- Global Forecast to 2036

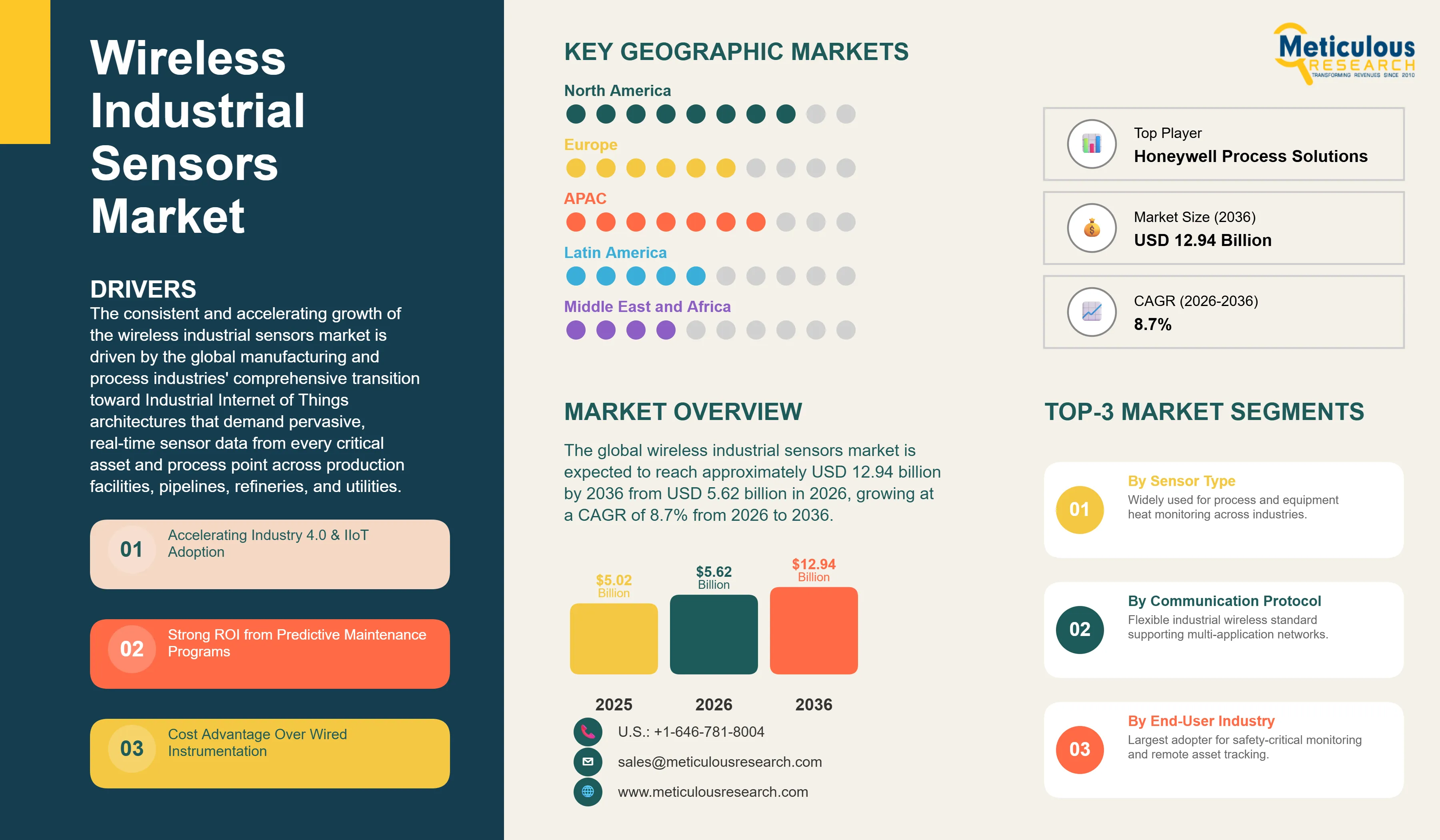

Report ID: MRSE - 1041830 Pages: 315 Mar-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global wireless industrial sensors market was valued at USD 5.02 billion in 2025. The market is expected to reach approximately USD 12.94 billion by 2036 from USD 5.62 billion in 2026, growing at a CAGR of 8.7% from 2026 to 2036. The consistent and accelerating growth of the wireless industrial sensors market is driven by the global manufacturing and process industries' comprehensive transition toward Industrial Internet of Things architectures that demand pervasive, real-time sensor data from every critical asset and process point across production facilities, pipelines, refineries, and utilities. Wireless industrial sensors — integrating sensing elements, signal conditioning, microcontrollers, radio transceivers, and increasingly edge computing intelligence into self-powered or battery-operated devices communicating over standardized industrial wireless protocols — eliminate the prohibitive wiring costs and installation complexity that historically restricted sensor deployment to the most critical measurement points, enabling the dense, facility-wide sensor networks required for comprehensive process optimization, predictive maintenance, and operational safety monitoring. The economic case for wireless sensor deployment has become compelling across virtually all process and manufacturing industries: eliminating instrumentation cable runs costing USD 100-500 per meter in industrial environments enables sensor deployment economics that justify monitoring previously unmonitored assets, while the operational value generated through reduced unplanned downtime, improved product quality, and optimized energy consumption delivers return on investment timelines of 12-24 months in typical process industry applications. The convergence of energy harvesting technologies extending sensor battery life to 5-10 years or enabling perpetual self-powered operation, sub-GHz radio technologies providing reliable penetration through dense metal-rich industrial structures, and AI-powered analytics platforms converting sensor data streams into actionable operational intelligence is creating the technical and economic conditions for wireless sensor adoption to accelerate substantially across the installed base of global industrial facilities.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Wireless industrial sensors are electronic measurement devices specifically engineered for deployment in industrial process and manufacturing environments, combining physical parameter sensing capabilities with wireless communication subsystems, power management circuits, and environmental protection ratings that enable reliable autonomous operation in conditions — including explosive atmospheres, extreme temperatures, high vibration, chemical exposure, and electromagnetic interference — that would compromise consumer-grade wireless sensor products. The industrial wireless sensor market is architecturally organized around specific communication protocol ecosystems that define interoperability, network topology, security, and performance characteristics suited to different industrial application contexts. WirelessHART — standardized as IEC 62591 — dominates process automation wireless sensing as the first and most widely deployed industrial wireless standard, using a self-organizing, self-healing mesh network topology operating in the 2.4 GHz ISM band with time-synchronized channel hopping providing robust communication in electrically noisy process environments. ISA100.11a provides an alternative wireless standard competing with WirelessHART in process automation applications with somewhat more flexible protocol architecture enabling coexistence of multiple industrial wireless applications. Sub-GHz protocols including WirelessHART extensions, LoRaWAN, and proprietary sub-GHz implementations address applications requiring long-range communication through dense metal infrastructure where 2.4 GHz propagation is inadequate.

The industrial wireless sensor hardware ecosystem encompasses diverse sensor types addressing the fundamental measurement parameters required for process monitoring, equipment health assessment, and safety monitoring across industrial operations. Temperature sensors — the most widely deployed wireless sensor type — monitor process fluid temperatures, heat exchanger performance, motor and bearing temperatures, and electrical equipment thermal status using thermocouple, RTD, and thermistor sensing elements with wireless transmitters. Pressure sensors measure process pressures, differential pressures across filters and flow meters, and tank levels through hydrostatic pressure, serving as critical indicators of process conditions and equipment integrity. Vibration sensors — particularly accelerometers measuring bearing vibration signatures, shaft vibration, and structural resonances in rotating machinery — represent the highest-value wireless sensor category for predictive maintenance applications, where early detection of developing bearing defects, imbalance, misalignment, and resonance conditions enables planned maintenance interventions avoiding catastrophic equipment failures costing tens to hundreds of thousands of dollars. Gas and chemical sensors detecting combustible gases, toxic gases, and process leaks serve critical safety monitoring functions in refineries, chemical plants, and mining operations where wireless deployment enables comprehensive area coverage without the wiring cost barriers that historically resulted in sparse fixed gas detector installations supplemented by expensive personal gas monitors.

The integration of wireless industrial sensors into comprehensive IIoT architectures — connecting sensor data through plant-level wireless gateways, industrial edge computing platforms, and cloud analytics services — has fundamentally transformed the value proposition of wireless sensing from simple remote measurement to predictive intelligence. Platforms including Emerson's Plantweb, Honeywell's Connected Plant, ABB's Ability, Siemens MindSphere, and independent IIoT platforms from companies including Seeq, AspenTech, and PTC ThingWorx aggregate multi-sensor data streams with process historian data, maintenance records, and equipment specifications to build machine learning models that predict equipment degradation, optimize process efficiency, and automate alarm management. The business model evolution toward sensor-as-a-service and outcome-based contracts — where vendors commit to delivering specific operational outcomes including uptime improvement percentages or maintenance cost reductions rather than selling hardware — is accelerating adoption by reducing capital expenditure barriers and aligning vendor incentives with customer value creation.

Energy Harvesting and Battery-Free Sensor Technologies Enabling Perpetual Operation

The evolution of energy harvesting technologies — converting ambient environmental energy from vibration, thermal gradients, light, and radio frequency fields into electrical power sufficient to operate wireless sensors indefinitely without battery replacement — represents a transformative development addressing the operational maintenance burden of battery-powered wireless sensors in large-scale industrial deployments where periodic battery replacement across thousands of installed sensors creates substantial ongoing labor costs. Vibration energy harvesters using piezoelectric elements or electromagnetic induction converting the mechanical vibration energy ubiquitous in rotating machinery environments into sensor operating power are achieving average harvested power levels of 100-500 microwatts — sufficient to operate low-power wireless sensors with transmission intervals of minutes in continuous operation. Thermoelectric generators converting the temperature differentials present across pipe walls, heat exchangers, and motor housings into electrical power using Seebeck effect semiconductor devices are achieving power densities of 1-5 mW/cm2 in process environments with temperature differentials of 20-50 degrees Celsius — enabling continuous wireless temperature and vibration monitoring from process infrastructure thermal gradients without any battery or wiring requirement. Companies including EnOcean, Mide Technology, Perpetuum, and SKF's energy harvesting division are commercializing industrial-grade harvesting solutions integrated with wireless sensor platforms, while semiconductor manufacturers including Texas Instruments, Microchip, and Silicon Laboratories are developing ultra-low-power system-on-chip devices requiring only microwatts of average operating power, making energy harvesting power budgets viable for increasingly capable sensor nodes with expanded measurement and edge computation capability.

5G Private Networks and Network Slicing Enabling High-Density, Low-Latency Industrial Sensing

The deployment of private 5G networks in industrial facilities represents a transformative infrastructure development enabling wireless industrial sensor applications previously constrained by the bandwidth, latency, and connection density limitations of legacy industrial wireless protocols. Private 5G networks operating in licensed or shared spectrum bands provide gigabit-class wireless infrastructure within factory perimeters, enabling deployment of wireless sensors at densities of thousands per square kilometer with guaranteed quality of service characteristics — latency below 1 millisecond for time-critical control applications, 99.9999% reliability for safety-critical monitoring, and simultaneous connectivity for thousands of sensor devices across facility footprints spanning hundreds of thousands of square meters. The convergence of 5G connectivity with edge computing infrastructure co-located within industrial facilities enables real-time AI inference on sensor data streams — processing vibration signatures, acoustic emissions, and multi-sensor fusion data within milliseconds to provide immediate process control feedback and safety alerts that the latency of cloud-based analytics architectures cannot support. Automotive manufacturing facilities including those operated by BMW, Volkswagen, and Toyota are deploying private 5G networks as the connectivity backbone for comprehensive wireless sensing across assembly lines, with the precision timing and position accuracy of 5G positioning services enabling sub-centimeter asset location tracking alongside process parameter monitoring from thousands of simultaneous wireless sensors. Industrial 5G ecosystem vendors including Ericsson (Private 5G), Nokia (Digital Automation Cloud), Siemens (Industrial 5G), and Bosch (connected industry 5G solutions) are developing purpose-built private network solutions with pre-integrated OT security frameworks and seamless connectivity with existing industrial automation systems.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 12.94 Billion |

|

Market Size in 2026 |

USD 5.62 Billion |

|

Market Size in 2025 |

USD 5.02 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 8.7% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Sensor Type, Communication Protocol, End-User Industry, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Industry 4.0 Adoption and Predictive Maintenance Value Creation

The primary driver of wireless industrial sensor market growth is the accelerating adoption of Industry 4.0 frameworks across global manufacturing and process industries that demand comprehensive real-time data acquisition from the physical production environment as the foundational input to digital twin models, AI-powered optimization algorithms, and automated process control systems. McKinsey Global Institute estimates that Industry 4.0 adoption in manufacturing could generate USD 1.2-3.7 trillion in annual value by 2025 through productivity improvements, reduced maintenance costs, quality enhancement, and inventory optimization — with wireless sensor networks providing the sensing infrastructure that makes this value creation possible by instrumenting previously unmonitored assets and processes. The predictive maintenance value proposition — where wireless vibration, temperature, and process sensors provide continuous equipment health data enabling machine learning models to identify developing failures weeks to months before catastrophic breakdown — delivers quantified return on investment that justifies wireless sensor investment across virtually all capital-intensive industrial sectors. Studies by Emerson, ABB, and independent industrial analytics firms consistently document 30-50% reductions in unplanned downtime, 20-30% reductions in maintenance costs, and 15-25% extensions in equipment replacement intervals when predictive maintenance programs are implemented using comprehensive wireless sensor networks — translating to millions in annual operational savings for large processing facilities that typically justify capital investment in wireless sensor infrastructure within 12-18 months.

Opportunity: Hazardous Area Monitoring and Remote Asset Surveillance

The expansion of wireless industrial sensor deployment into hazardous area monitoring and remote asset surveillance applications represents a substantial and growing market opportunity where wireless sensing eliminates safety risks and operational constraints that make wired instrumentation either impractical or cost-prohibitive. Explosive atmosphere monitoring in oil and gas facilities, chemical plants, and grain handling operations requires sensor deployment across extensive areas where any ignition source creates catastrophic risk — wireless sensors with ATEX and IECEx explosion-proof certifications enabling installation in Zone 0, Zone 1, and Zone 2 classified areas eliminate the extensive conduit, cable tray, and associated intrinsic safety barriers required for wired instruments, reducing installation costs by 60-80% in classified area applications while enabling more comprehensive coverage than wired alternatives can economically justify. Remote oil and gas production assets — wellheads, pipeline compressor stations, tank farms, and offshore facilities located in geographic environments where continuous human presence is impractical — require autonomous wireless sensing networks communicating over long-range protocols including LoRaWAN and satellite IoT to transmit process parameters, equipment health data, and safety alerts to central operations centers. The industrial pipeline monitoring application — tracking pressure, temperature, flow rates, and leak indicators along hundreds of kilometers of transmission infrastructure — represents a particularly compelling wireless sensor application where fiber-optic cable installation along pipeline corridors is economically infeasible, making satellite-connected wireless sensor nodes every 500-2,000 meters the only practical continuous monitoring solution for the global installed base of 3.5 million kilometers of gas transmission pipelines.

Why Do Temperature Sensors Lead the Market?

Temperature sensors command approximately 28-32% of total wireless industrial sensors market revenue in 2026, reflecting temperature measurement as the most universally required process parameter across all industrial sectors and the broadest deployment opportunity for wireless sensing technology. Wireless temperature sensors serve applications spanning process fluid temperature monitoring in chemical and refining operations, motor winding and bearing temperature surveillance enabling early thermal fault detection, steam trap monitoring detecting failed traps that waste energy through continuous steam blowthrough, heat exchanger performance tracking detecting fouling through declining thermal efficiency, and electrical switchgear and transformer thermal monitoring identifying insulation degradation before catastrophic failure. The specific value proposition of wireless versus wired temperature sensing is strongest in applications including rotating equipment (where cable routing to moving parts creates mechanical fatigue failure risks), high-temperature process equipment (where refractory-lined vessels make cable penetrations structurally complex), and geographically dispersed assets (where cable runs of hundreds of meters create prohibitive costs). Pressure sensors represent the second-largest segment, serving as critical measurement points for process safety and efficiency monitoring, with wireless pressure sensors particularly valuable for monitoring normally static but occasionally variable conditions including pressure relief valve cycling frequency, pressure drops across heat exchangers indicating fouling progression, and tank level measurement through hydrostatic pressure in locations where direct level measurement access is restricted. Vibration sensors represent the highest revenue-per-unit wireless sensor category, with wireless accelerometers and vibration transmitters for rotating equipment health monitoring commanding significant premiums reflecting the high value of predictive maintenance insights they enable and the sophisticated signal processing capability required for bearing fault detection from vibration frequency spectra analysis.

How Does WirelessHART Maintain Market Leadership?

WirelessHART maintains approximately 42-46% of the wireless industrial sensors communication protocol market revenue in 2026, reflecting its dominant position as the established standard for process automation wireless sensing with the largest installed base, broadest device ecosystem, and strongest support from the major distributed control system and process automation vendors that specify wireless sensor infrastructure for refinery, chemical, and power generation facility projects. WirelessHART's self-organizing mesh network architecture — where each device simultaneously functions as a wireless sensor and a routing node forwarding messages from neighboring sensors toward the gateway — provides inherent redundancy and range extension capabilities that create robust networks in challenging industrial radio frequency environments without requiring manual network topology planning. The 10-15 year WirelessHART installed base in major industrial facilities including Saudi Aramco, ExxonMobil, Dow Chemical, and BASF provides significant switching cost barriers that sustain WirelessHART's market position even as competing protocols offer technical advantages in specific applications. ISA100.11a serves as the primary alternative wireless standard in process automation, offering somewhat more flexible protocol architecture with broader support from Japanese automation vendors including Yokogawa and Fuji Electric. LoRaWAN is the fastest-growing communication protocol in the wireless industrial sensor market at approximately 14-16% CAGR, driven by its long-range, low-power characteristics that make it uniquely suitable for large-area outdoor industrial applications — pipeline monitoring, tank farm surveillance, perimeter security sensing, and environmental monitoring — where the range limitations of 2.4 GHz protocols like WirelessHART and ISA100.11a require impractical repeater densities. 5G-connected wireless sensors represent the highest-growth segment longer-term, with private 5G network deployment in advanced manufacturing facilities enabling ultra-dense, low-latency sensor connectivity that addresses the bandwidth and latency limitations constraining wireless sensor applications in precision manufacturing and real-time process control contexts.

Why Does Oil and Gas Lead the Market?

The oil and gas end-user industry commands approximately 25-28% of wireless industrial sensors market revenue in 2026, reflecting the industry's unique combination of extensive wireless sensor deployment history, high operational value of comprehensive real-time monitoring in safety-critical environments, and the large installed base of refineries, processing facilities, and upstream production assets that collectively represent the most mature wireless sensor end-user segment. Oil and gas operations were among the earliest adopters of WirelessHART technology in the mid-2000s, driven by the compelling economics of wireless versus wired instrumentation in classified hazardous areas, the large physical scale of refineries requiring extensive cable infrastructure for wired sensing, and the operational safety value of dense gas detection and process monitoring networks. Major oil and gas operators including Saudi Aramco, Shell, ExxonMobil, BP, and Chevron have deployed hundreds of thousands of wireless sensors across their global facility portfolios, with WirelessHART networks monitoring corrosion rates, heat exchanger efficiency, pump and compressor health, flare management, and safety system bypass conditions that collectively contribute to quantified reductions in operational losses and maintenance costs. The chemical and petrochemical end-user segment represents a closely related and rapidly growing market, with specialty chemical producers, polymer manufacturers, and integrated petrochemical complexes deploying wireless sensors for reactor temperature profiling, distillation column monitoring, and tank farm level management where wireless eliminates the instrumentation cabling complexity in congested process unit environments. The pharmaceutical end-user segment demonstrates above-average growth at approximately 11-13% CAGR, driven by FDA 21 CFR Part 11 compliant wireless temperature and humidity monitoring requirements for pharmaceutical storage, cold chain monitoring for biologics and vaccines, and cleanroom environmental surveillance for GMP compliance.

How Does Predictive Maintenance Drive the Fastest Market Growth?

Predictive maintenance represents the highest-value and fastest-growing application for wireless industrial sensors at approximately 12-14% CAGR, enabled by the combination of wireless vibration, temperature, and acoustic emission sensors providing continuous equipment health data streams and AI-powered analytics platforms capable of extracting failure precursor signatures from complex multi-dimensional sensor data. The business case for wireless sensor-based predictive maintenance has been thoroughly validated across diverse industrial contexts: a typical large refinery with hundreds of rotating equipment assets experiences 2-4 major unplanned failures annually — each costing USD 500,000-5 million in lost production, emergency repair costs, and safety incident potential — creating predictive maintenance program savings of USD 5-20 million annually that easily justify wireless sensor network investments of USD 500,000-2 million. Bearing fault detection from vibration frequency spectrum analysis represents the most commercially mature predictive maintenance wireless sensing application, with algorithms detecting characteristic bearing defect frequencies — ball pass frequency outer race (BPFO), ball pass frequency inner race (BPFI), and ball spin frequency (BSF) — in wireless accelerometer data streams to provide 2-8 weeks advance warning of bearing failure enabling planned maintenance scheduling. Process monitoring and control represents the largest application by deployed sensor volume, encompassing the continuous measurement of process variables — temperature, pressure, flow, level, and composition — required for process control, safety system inputs, and efficiency optimization across manufacturing and process operations. Environmental and safety monitoring is the highest-growth application at approximately 15-17% CAGR, driven by tightening regulatory requirements for facility emissions monitoring, growing adoption of wireless gas detection networks for area-wide flammable and toxic gas surveillance, and increasing deployment of structural health monitoring systems for critical infrastructure including bridges, dams, and industrial structures.

How is North America Maintaining Market Leadership?

North America holds approximately 34-38% of the global wireless industrial sensors market in 2026, driven by the region's position as the world's largest industrial wireless sensor deployment market — anchored by its extensive oil and gas processing infrastructure, advanced manufacturing base, and the operational headquarters of the leading wireless industrial sensor technology developers including Emerson, Honeywell Process Solutions, and key application-specific vendors. The United States hosts the largest concentration of WirelessHART-instrumented process facilities globally, with major refining complexes in Texas, Louisiana, and California representing some of the densest wireless sensor deployments worldwide. The shale oil and gas production boom has driven extensive wireless sensor deployment in unconventional production environments where the distributed nature of wellpads and gathering infrastructure makes wired instrumentation economically challenging, creating substantial demand for battery-powered wireless sensors communicating over LoRaWAN and cellular IoT protocols. Manufacturing sector demand for wireless sensors in automotive, aerospace, food processing, and pharmaceutical production is driven by Industry 4.0 initiatives from major manufacturers including Ford, Boeing, Procter & Gamble, and Pfizer that are instrumenting production lines with wireless sensor networks as the data acquisition layer for digital twin and predictive maintenance programs. Canadian oil sands operations in Alberta — representing one of the world's most extensive heavy oil processing environments — have deployed wireless sensor networks extensively for process monitoring and safety applications where the severe winter climate creates particular challenges for wired instrumentation maintenance.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 11-13% CAGR, propelled by China's massive manufacturing modernization program, rapidly expanding oil and gas infrastructure across Southeast Asia and Australia, and the pharmaceutical and food processing industry growth across India, Japan, and ASEAN nations creating substantial new wireless sensor deployment demand. China's Made in China 2025 industrial policy explicitly targets smart manufacturing transformation across automotive, electronics, chemicals, and heavy industry sectors, with wireless sensor networks serving as the data acquisition infrastructure for the digital factory architectures required to achieve the productivity and quality improvements the program targets. Chinese wireless sensor manufacturers including Sifang Electronics, Accuware, and numerous emerging IIoT-focused companies are developing increasingly competitive products that are gaining market share in domestic applications against international vendors while beginning to target export markets in Southeast Asia and emerging economies where price sensitivity favors cost-optimized offerings. Japan's highly automated manufacturing sector — particularly automotive and electronics production with Toyota, Honda, Panasonic, and Sony deploying IIoT initiatives — creates demand for advanced wireless sensing including precision vibration monitoring for ultra-precise manufacturing processes and environmental monitoring for clean room facilities. India's rapidly growing pharmaceutical manufacturing sector — the world's leading generic medicine exporter — requires comprehensive wireless temperature, humidity, and environmental monitoring for GMP compliance across manufacturing facilities, storage facilities, and cold chain logistics, creating a large and growing domestic wireless sensor market served by both international vendors and emerging domestic suppliers.

The global wireless industrial sensors market is led by Emerson Electric Co. (Rosemount wireless product line, Plantweb IIoT platform), Honeywell Process Solutions (OneWireless network, connected plant platform), ABB Ltd. (wireless field products and Ability platform), Siemens AG (SITRANS wireless sensors, MindSphere platform), and Yokogawa Electric Corporation (ISA100.11a wireless field instruments) — collectively representing the dominant process automation vendors with comprehensive wireless sensor portfolios deeply integrated with their distributed control system and asset management platforms. Endress+Hauser Group, Vega Grieshaber, and Krohne Group serve strong wireless sensor positions in specific measurement applications including level, flow, and analytical measurement. Texas Instruments, STMicroelectronics, and Silicon Laboratories provide the semiconductor components — microcontrollers, radio transceivers, and power management ICs — that enable wireless sensor hardware design, with their development ecosystems accelerating new sensor product development by both established vendors and emerging entrants. SKF Group and Parker Hannifin address the wireless vibration sensor and predictive maintenance segments with specialized rotating equipment monitoring solutions. Advantech, Belden (Hirschmann), and Pepperl+Fuchs serve industrial wireless networking infrastructure and sensor interfacing applications. Emerging IIoT platform companies including Samsara, Augury, and Aspentech APM are building wireless sensor-based predictive maintenance and asset monitoring solutions that integrate hardware, connectivity, and analytics into comprehensive outcome-oriented service offerings, representing a growing competitive threat to traditional component-focused industrial sensor vendors.

The global wireless industrial sensors market is expected to grow from USD 5.62 billion in 2026 to USD 12.94 billion by 2036.

The global wireless industrial sensors market is projected to grow at a CAGR of 8.7% from 2026 to 2036.

Temperature sensors dominate representing 28-32% of revenue through universal deployment across all industrial applications. Vibration and acoustic emission sensors demonstrate the fastest growth driven by predictive maintenance adoption enabling machine learning-powered bearing and rotating equipment failure prediction delivering compelling returns on investment across manufacturing and process industries.

Private 5G networks deployed in industrial facilities provide gigabit-class wireless infrastructure with guaranteed sub-millisecond latency, 99.9999% reliability, and connection density supporting thousands of sensors per square kilometer -- enabling wireless sensor applications in precision manufacturing and real-time process control that the bandwidth and latency limitations of WirelessHART and ISA100.11a cannot support, while co-located edge computing enables real-time AI inference on sensor data streams for immediate control feedback and safety responses.

North America leads with approximately 34-38% of global market driven by the largest installed base of WirelessHART-instrumented process facilities, extensive oil and gas infrastructure, and headquarters of leading wireless sensor technology developers. Asia-Pacific demonstrates the fastest growth at 11-13% CAGR driven by China's Made in China 2025 manufacturing modernization, Southeast Asian oil and gas infrastructure expansion, and pharmaceutical and food processing growth across India and ASEAN.

The leading companies include Emerson Electric, Honeywell Process Solutions, ABB Ltd., Siemens AG, Yokogawa Electric, Endress+Hauser, Vega Grieshaber, Krohne, SKF Group, Parker Hannifin, Texas Instruments (semiconductor), Silicon Laboratories (semiconductor), and IIoT platform entrants including Samsara, Augury, and AspenTech APM competing with outcome-based wireless sensor service offerings.

Published Date: May-2026

Published Date: Jan-2025

Published Date: Oct-2024

Published Date: Jan-2024

Published Date: Jan-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates