Resources

About Us

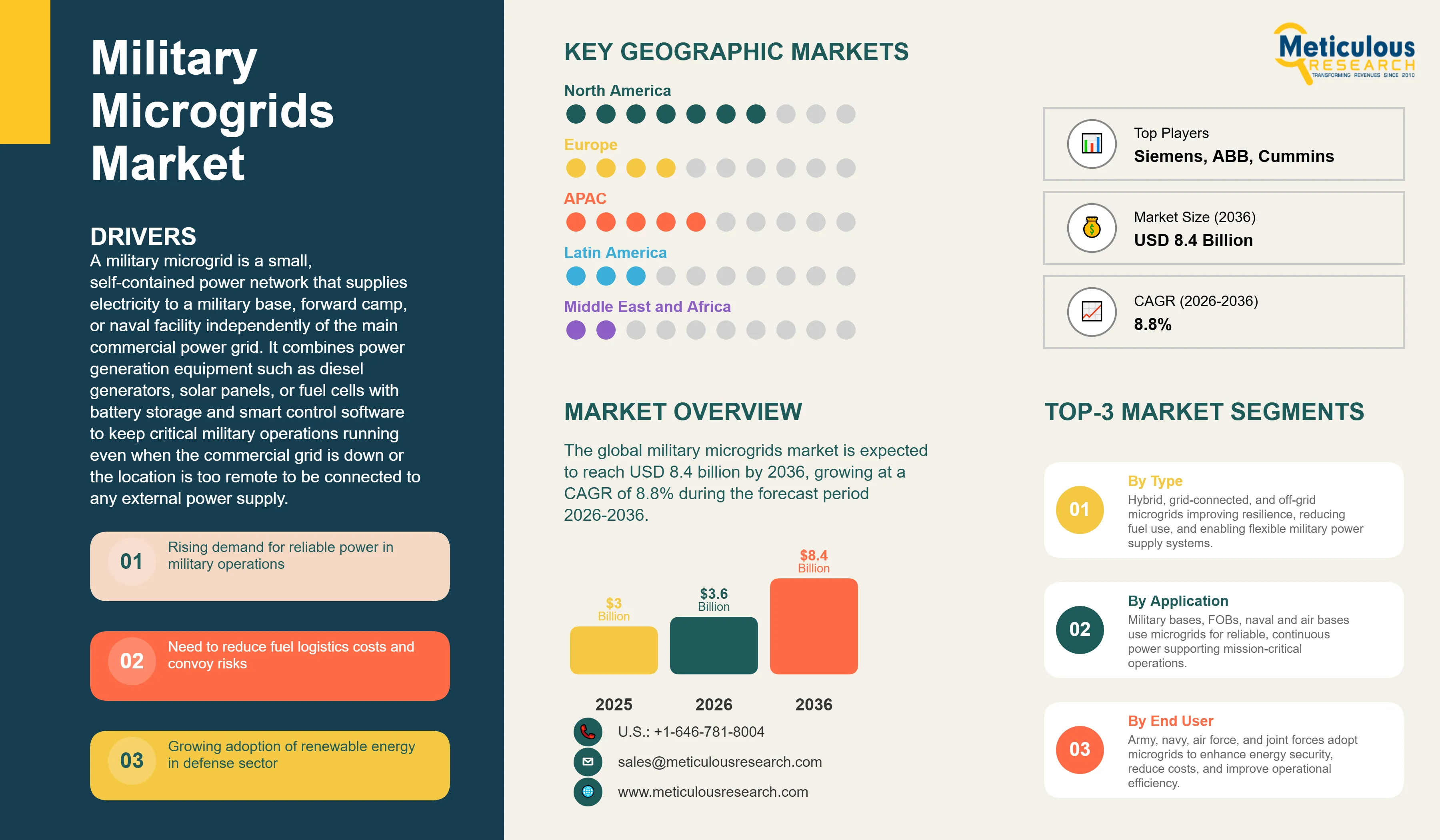

Military Microgrids Market Size, Share & Trends Analysis by Grid Type, Power Source, Component, Application, and End User -Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRAD - 1041910 Pages: 282 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global military microgrids market was valued at USD 3.0 billion in 2025. This market is expected to reach USD 8.4 billion by 2036 from an estimated USD 3.6 billion in 2026, growing at a CAGR of 8.8% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

A military microgrid is a small, self-contained power network that supplies electricity to a military base, forward camp, or naval facility independently of the main commercial power grid. It combines power generation equipment such as diesel generators, solar panels, or fuel cells with battery storage and smart control software to keep critical military operations running even when the commercial grid is down or the location is too remote to be connected to any external power supply. The ability to generate, store, and manage power on-site without depending on external supply lines is an important military advantage, particularly for remote forward operating bases where fuel convoys are expensive, dangerous, and vulnerable to attack.

The market is growing because modern military operations depend on electricity more than at any time in history. Radar systems, communication networks, computer systems, medical facilities, and drone charging stations all require reliable power around the clock. A single power failure at a critical base can disrupt communications, disable defense systems, or halt command-and-control operations. At the same time, transporting diesel fuel to remote military bases is one of the most expensive and dangerous parts of running forward operations. Studies by the U.S. Department of Defense have found that a significant proportion of casualties in recent conflicts occurred during fuel convoy operations. Reducing fuel consumption through renewable energy and better energy management is therefore both a safety issue and a major cost-saving opportunity for defense budgets.

Two significant opportunities are driving the next phase of market growth. The addition of solar panels and battery storage to existing diesel-powered military microgrids is becoming much more affordable as the cost of solar and battery technology continues to fall. A hybrid system that combines solar power during daylight hours with batteries for nighttime and cloudy periods can cut diesel consumption at a remote base by 30 to 60 percent, providing a strong financial return while reducing the frequency of dangerous fuel supply runs. In addition, smart energy management software powered by AI can now monitor power consumption across an entire base, predict demand changes, and automatically balance generation and storage to minimize fuel use and ensure critical systems always get priority power, making military microgrids significantly more efficient and reliable than the basic diesel generator systems they replace.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 8.4 Billion |

|

Market Size in 2026 |

USD 3.6 Billion |

|

Market Size in 2025 |

USD 3.0 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 8.8% |

|

Dominating Grid Type |

Hybrid Microgrids |

|

Fastest Growing Grid Type |

Off-Grid/Islanded Microgrids |

|

Dominating Power Source |

Diesel Generators |

|

Fastest Growing Power Source |

Solar PV Systems |

|

Dominating Component |

Generation Equipment |

|

Fastest Growing Component |

Energy Storage Systems |

|

Dominating Application |

Military Bases and Installations |

|

Fastest Growing Application |

Forward Operating Bases (FOBs) |

|

Dominating End User |

Army |

|

Fastest Growing End User |

Air Force |

|

Dominating Deployment Type |

Fixed Microgrids |

|

Fastest Growing Deployment Type |

Mobile/Containerized Microgrids |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Cutting Fuel Costs and Convoy Risk is the Primary Business Case

The most powerful force driving investment in military microgrids is the very high cost and serious danger of transporting diesel fuel to remote forward bases. The U.S. Army has calculated that the fully loaded cost of a gallon of fuel delivered to a remote forward operating base, including transportation, logistics support, and security, can be many times the wholesale fuel price. In some of the most contested environments, this fully loaded cost has been estimated at over USD 400 per gallon. This makes energy efficiency not just an environmental goal but a direct operational and financial priority that defense ministries and military commanders take seriously. Installing solar panels, batteries, and smart energy management systems at a forward base can cut diesel requirements dramatically, directly reducing the frequency and size of fuel resupply convoys and thereby reducing the risk to logistics personnel and supply chain costs. This financial and safety argument is the core business case that is driving military microgrid adoption, and it is equally compelling for both the richest and most modestly funded military establishments around the world.

The U.S. Department of Defense has been the most active investor in military microgrids as a result of this business case, running major programs including the Smart Power Infrastructure Demonstration for Energy Reliability and Security, known as SPIDERS, and the Operational Energy Strategy that mandates energy efficiency improvements across military installations. The U.K. Ministry of Defence, Australian Defence Force, and French military have all followed with their own energy resilience programs that are driving demand for hybrid microgrid systems at both home bases and deployed operations.

Hybrid Solar and Storage Systems Rapidly Replacing Pure Diesel Power at Bases

The most visible technology trend in the military microgrids market is the rapid adoption of hybrid power systems that combine solar photovoltaic panels and battery storage with existing diesel generators, rather than replacing diesel entirely. This hybrid approach is popular because it is practical and affordable. Solar panels and batteries are added on top of the existing diesel infrastructure, which remains as a backup and for night or high-demand periods. During daylight hours the solar system produces free electricity and charges the batteries. At night or in bad weather the batteries discharge first, and the diesel generator only runs when batteries are low. The result is a significant reduction in diesel consumption without requiring the complete replacement of existing power infrastructure.

Companies including Schneider Electric, ABB, Siemens, Eaton, and Honeywell have all developed packaged hybrid military microgrid systems that can be installed at existing bases or pre-configured in containerized units for deployment to new forward locations. The falling cost of solar panels and lithium-ion batteries over the past decade has made the financial payback period for these hybrid systems short enough that defense budget planners can justify the investment on pure cost-saving grounds, without needing to rely on sustainability arguments. This economic shift is accelerating adoption across a broader range of military customers than the early-adopter U.S. and Western European programs that established the market.

Mobile and Containerized Microgrids Gaining Traction for Deployable Operations

One of the fastest-growing segments of the military microgrids market is mobile and containerized systems that can be packed into standard shipping containers, transported to any location by truck, helicopter, or aircraft, and set up to provide power within hours of arrival. These deployable systems are particularly valuable for forward operating bases that are established quickly in response to an operational situation and may need to be relocated as the mission evolves. Traditional diesel generator sets for field use exist, but adding solar panels, batteries, and smart control systems into a containerized package that deploys as quickly as a generator set but uses far less fuel is a meaningful operational improvement.

Companies including SFC Energy, PowerSecure, and several defense specialists have developed containerized military microgrid products for this deployable market. The U.S. Army's Tactical Microgrid Standard and similar procurement programs in NATO countries are creating defined requirements for deployable microgrid systems that are guiding the market toward standardized products that can be bought in quantity and maintained through common logistics channels. The growing use of forward bases in Africa, the Middle East, and the Indo-Pacific region for counter-terrorism, humanitarian assistance, and security operations is creating real-world demand for these deployable systems, and this demand is expected to grow substantially through the forecast period.

Increasing Demand for Energy Resilience in Military Operations

Military forces today depend on electricity for nearly every critical function. Communications networks, radar and sensor systems, command and control computers, intelligence processing systems, hospital facilities, and drone operations all require continuous, reliable power. If the power supply to a forward base or a major installation fails, the consequences can range from a communication blackout to the complete shutdown of defensive systems at a critical moment. The growing recognition that reliable power is as important to mission success as weapons and personnel is the primary reason defense ministries are investing in military microgrids that can generate and store electricity on-site without depending on external power lines or continuous fuel deliveries. The U.S. Department of Defense's designation of energy as a critical component of national security, combined with NATO's energy resilience guidelines for allied installations, reflects this understanding and is translating it into funded procurement programs that are the primary demand driver of the military microgrids market.

Rising Need to Reduce Fuel Logistics and Costs

Diesel fuel is expensive to buy, extremely expensive to transport to remote locations, and dangerous to move through conflict zones. The financial burden of fuel logistics is a major item in the operating budgets of military forces with deployed operations, and the security risk created by fuel convoys has resulted in significant casualties in recent conflicts. Every gallon of diesel that can be replaced by solar power or energy efficiency savings directly reduces the number of fuel trucks that need to make supply runs, reducing both cost and risk. For large military establishments with hundreds of installations to power, the potential savings from switching to hybrid renewable microgrids are very large. The U.S. Army has estimated that reducing fuel consumption across its installations by 25 percent would save hundreds of millions of dollars annually. This clear and quantifiable financial benefit is making military microgrid investment easy to justify through normal defense budget processes, creating stable and growing procurement demand that does not depend solely on energy security arguments.

Development of Hybrid Renewable Microgrids

The combination of solar panels, wind turbines, battery storage, and fuel cells into a single integrated hybrid microgrid system represents the most commercially attractive product opportunity in the military microgrids market. Pure diesel generator systems are being replaced by hybrid systems that use renewable energy when it is available and fall back on diesel or stored energy when it is not. This approach can cut fuel consumption by 30 to 60 percent at a typical military base while actually improving power reliability compared with a single-source diesel system. The falling cost of solar panels and lithium-ion batteries is making these systems financially attractive to a much wider range of military customers than was the case even five years ago. Defense contractors and energy technology companies that can package hybrid renewable microgrid systems into straightforward, pre-engineered products with proven military certifications and standardized maintenance requirements are positioned to capture large procurement programs as more military establishments move from planning to deployment of these systems.

AI-Based Energy Management Systems

Traditional military generator systems operate on a simple on/off basis, with generators running at full capacity whether demand is high or low and battery systems charged and discharged according to basic threshold rules. AI-based energy management systems replace this simple approach with smart software that monitors power demand across every building and system at a base, forecasts expected demand over the next hours and days, predicts solar and wind generation based on weather data, and automatically adjusts the mix of generation sources and storage dispatch to minimize fuel consumption while ensuring critical systems always have priority access to power. The result is significantly lower fuel consumption, extended battery life, and fewer generator maintenance issues compared with non-AI-managed systems. For large military installations with complex and variable power demand patterns, the fuel savings generated by AI-based energy management can be substantial, and the software can be updated remotely as the base's power requirements change. Companies developing AI energy management platforms specifically validated for military security and reliability requirements are positioned to offer a high-value product that complements hardware-focused microgrid suppliers.

By Grid Type: In 2026, Hybrid Microgrids to Dominate

Based on grid type, the global military microgrids market is segmented into grid-connected microgrids, off-grid/islanded microgrids, and hybrid microgrids. In 2026, the hybrid microgrids segment is expected to account for the largest share of the global military microgrids market. Hybrid microgrids combine multiple power sources, typically diesel generators with solar and battery storage, to reduce fuel consumption and improve reliability compared with single-source systems. This approach is the most widely adopted in current military programs because it can be built on top of existing diesel generator infrastructure without requiring a complete replacement, making it practical and cost-effective for both new installations and upgrades to existing bases. The proven cost savings and fuel reduction benefits of hybrid systems have made them the preferred choice across U.S., European, and Australian military microgrid programs.

However, the off-grid/islanded microgrids segment is projected to register the highest CAGR during the forecast period. The growth of forward operating base deployments in remote areas of Africa, the Indo-Pacific, and Central Asia where there is no commercial grid connection available means that off-grid systems are the fastest-growing deployment category. A base that operates entirely on its own self-generated power, with no external grid connection, has the highest level of energy independence and resilience, which is increasingly valued by military planners who have seen how cyber or physical attacks on commercial power grids can disrupt military operations.

By Power Source: In 2026, Diesel Generators to Hold the Largest Share

Based on power source, the global military microgrids market is segmented into diesel generators, solar PV systems, wind energy, fuel cells, and hybrid energy systems. In 2026, the diesel generators segment is expected to account for the largest share of the global military microgrids market. Diesel generators have been the standard power source for military installations for decades and remain the backbone of military power supply, particularly for large bases and for peak power demand that renewable sources cannot always meet on their own. The very large existing installed base of diesel generators at military facilities globally, combined with the ongoing procurement of diesel generators for new installations, makes this the highest-revenue power source segment. Diesel also has well-understood logistics, maintenance, and operational characteristics that military procurement and operations teams are experienced with.

However, the solar PV systems segment is projected to register the highest CAGR during the forecast period. Solar power costs have fallen dramatically over the past decade, making solar installation on military bases one of the fastest-paying energy investments available. Solar panels require no fuel, produce no emissions, are silent during operation, and reduce the load on diesel generators, cutting both fuel consumption and generator maintenance costs. The U.S. Army, U.S. Air Force, and several European militaries have all launched large solar installation programs at their permanent bases, and portable solar panel systems for forward bases are becoming a standard part of deployable power kits.

By Component: In 2026, Generation Equipment to Hold the Largest Share

Based on component, the global military microgrids market is segmented into generation equipment, energy storage systems, power electronics (inverters and converters), and control systems (EMS and microgrid controllers). In 2026, the generation equipment segment is expected to account for the largest share of the global military microgrids market. Generation equipment encompasses the diesel generators, solar panels, wind turbines, and fuel cells that produce electricity, and represents the largest share of the total capital cost of a military microgrid installation. The ongoing procurement of generators and solar systems for both new installations and replacements at existing bases makes this the dominant revenue component in the market.

However, the energy storage systems segment is projected to register the highest CAGR during the forecast period. Battery energy storage is the component that enables solar power to be used at night, that provides a buffer against sudden changes in power demand, and that allows a military base to operate without generators for extended periods when tactical situations require silent running or when generator fuel is temporarily unavailable. As battery costs continue to fall and military operators experience the operational benefits of energy storage in field deployments, battery procurement for military microgrids is growing rapidly from a relatively small base.

By Application: In 2026, Military Bases and Installations to Hold the Largest Share

Based on application, the global military microgrids market is segmented into forward operating bases, military bases and installations, naval bases and ships, air bases, and disaster relief and emergency operations. In 2026, the military bases and installations segment is expected to account for the largest share of the global military microgrids market. Large permanent military bases and installations represent the highest total power consumption locations in any national defense structure and therefore offer the greatest financial return from microgrid investment. A major army or air force base may consume as much electricity as a small town, and even a modest improvement in energy efficiency or reduction in dependence on the commercial grid translates into large cost savings. The U.S. DoD's installation energy programs have directed billions of dollars toward microgrid and energy efficiency upgrades at major permanent installations, making this the current revenue leader.

However, the forward operating bases segment is projected to register the highest CAGR during the forecast period. Forward bases are established quickly in active operational areas and often have no access to commercial power infrastructure. Their power supply depends entirely on what can be transported and installed by the military unit occupying the location. Because every gallon of diesel at a forward base had to be transported through potentially hostile territory, the financial and safety argument for reducing fuel consumption through solar and battery hybrid systems is even stronger at forward bases than at permanent installations. The growing number of small forward bases established in Africa, the Middle East, and the Pacific as part of security partnerships and counter-terrorism operations is creating rapidly growing demand for mobile and deployable hybrid microgrid systems.

By End User: In 2026, Army to Hold the Largest Share

Based on end user, the global military microgrids market is segmented into army, navy, air force, and joint defense forces. In 2026, the army segment is expected to account for the largest share of the global military microgrids market. Armies operate the largest number of fixed and forward bases of any military service, and they have been the most active in deploying microgrids both at permanent installations and at forward operating bases in active mission areas. The U.S. Army's energy resilience programs, including its Net Zero Energy installations initiative and tactical microgrid programs for deployed forces, have been the single largest driver of military microgrid procurement globally. Army bases are typically the largest power consumers among military installation types, making the financial return from microgrid investment highest for this service.

However, the air force segment is projected to register the highest CAGR during the forecast period. Air force installations have very high and concentrated power demands driven by flight operations, aircraft maintenance systems, radar and air traffic control equipment, weapons storage systems, and the extensive communications infrastructure that modern air operations require. The consequences of a power failure at an airbase, including the grounding of aircraft or the shutdown of air defense systems, are particularly severe, making energy resilience investment a high priority. Several air forces including the U.S. Air Force, Royal Air Force, and the Israeli Air Force have launched major microgrid investment programs at their most critical installations, and these programs are growing.

By Deployment Type: In 2026, Fixed Microgrids to Hold the Largest Share

Based on deployment type, the global military microgrids market is segmented into fixed microgrids and mobile/containerized microgrids. In 2026, the fixed microgrids segment is expected to account for the largest share of the global military microgrids market. Fixed microgrids are installed permanently at established military bases and installations, where the investment in foundation-mounted solar panels, permanent battery storage facilities, and grid-connected control infrastructure can be fully amortized over a long service life. The large number of permanent military installations globally, each representing a potential microgrid upgrade opportunity, makes fixed installations the current revenue leader by a significant margin.

However, the mobile/containerized microgrids segment is projected to register the highest CAGR during the forecast period. The ability to pack a complete hybrid power system into standard shipping containers that can be transported anywhere in the world and set up within hours is a highly valuable capability for military forces that establish forward bases quickly in response to emerging situations. As the cost and size of solar panels and battery systems continue to fall, containerized hybrid microgrid systems are becoming more powerful and more affordable, making them practical for a wider range of forward base applications. Defense contractors are developing increasingly capable packaged mobile microgrid products specifically designed to meet military transportability and ruggedness requirements.

Military Microgrids Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global military microgrids market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global military microgrids market. The United States is by far the world's largest investor in military microgrids, driven by the Department of Defense's formal energy resilience strategy, which classifies energy security as a component of national security and allocates substantial funding to reducing military installations' dependence on the commercial power grid. The U.S. Army's and Air Force's large-scale Net Zero and energy resilience installation programs, the U.S. Navy's energy efficiency initiatives at major naval bases, and DARPA-funded research programs on advanced mobile microgrid technologies collectively make the United States the world's dominant military microgrid market. The presence of major military energy technology suppliers including Lockheed Martin, RTX Corporation, Honeywell, Schneider Electric's North American operations, Eaton, and GE in the U.S. market reinforces North America's leadership position by ensuring a technically advanced and competitive supply base serving the government's large procurement programs.

However, the Asia-Pacific military microgrids market is expected to grow at the fastest CAGR during the forecast period. The escalating security tensions in the Indo-Pacific region, particularly around the South China Sea and Taiwan Strait, are driving Japan, South Korea, Australia, India, and several Southeast Asian nations to invest urgently in hardening their military infrastructure, including its power supply. An installation that relies on the commercial grid is vulnerable to cyber or physical attacks on civilian power infrastructure, and this vulnerability is increasingly recognized as a strategic risk by regional military planners. Australia has been one of the most active adopters, with its Defence Energy Program mandating microgrid and renewable energy installations at major bases including those in the Northern Territory that are most relevant to Indo-Pacific operations. India's growing defense budget and its active forward base expansion program along its borders with China and Pakistan are generating significant demand for deployable and fixed military microgrids. China is also a major developer of military microgrid technology for its own armed forces, making Asia-Pacific the most dynamic growth market globally.

Europe is a growing and increasingly important military microgrids market, driven primarily by the surge in European defense spending that followed Russia's invasion of Ukraine in 2022. European NATO members who increased their defense budgets sharply after 2022 are investing in base hardening and energy resilience as part of their broader force modernization programs, recognizing that the Ukraine conflict demonstrated how attacks on power infrastructure can be a deliberate military strategy. Germany, Poland, and the UK are among the most active European investors in military energy resilience programs. Norway and Sweden, which joined NATO and are upgrading their military infrastructure, are also generating growing microgrid procurement demand. The strong presence of European energy technology companies including Schneider Electric, ABB, Siemens, and Saft in the military microgrid supply chain provides the region with capable domestic suppliers alongside U.S. contractors competing for European defense contracts.

The military microgrids market includes large defense prime contractors that understand both the military requirements and the energy technology, major industrial energy technology companies with strong grid and power management product portfolios, and specialist companies focused on specific components such as batteries, fuel cells, or containerized power systems. The most competitive suppliers are those who can combine proven military program management credentials with strong energy technology know-how and the ability to integrate multiple power sources into a reliable and cybersecure system meeting military specifications.

Lockheed Martin and RTX Corporation serve the military microgrid market through their defense technology divisions, combining defense contracting capability with energy systems integration. Schneider Electric, Siemens, and ABB are the leading industrial energy technology companies in the market, with comprehensive microgrid product portfolios spanning hardware, software, and energy management systems that have been adapted for military use. Eaton and Honeywell offer power management and control systems for military microgrid applications. Caterpillar and Cummins are dominant suppliers of the diesel generator systems that form the backbone of most current military microgrids, and both have expanded into hybrid system products. Saft Groupe and SFC Energy are specialist battery and fuel cell suppliers serving portable and deployed military power requirements.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, defense program track records, geographic presence, and recent strategic developments. Some of the key players operating in the global military microgrids market include Lockheed Martin Corporation (U.S.), RTX Corporation/Raytheon Technologies (U.S.), Schneider Electric SE (France), Siemens AG (Germany), ABB Ltd. (Switzerland), Eaton Corporation plc (Ireland), General Electric Company (U.S.), Honeywell International Inc. (U.S.), Rolls-Royce plc (UK), Caterpillar Inc. (U.S.), Cummins Inc. (U.S.), PowerSecure/Southern Company (U.S.), Saft Groupe S.A. (France), SFC Energy AG (Germany), and Ampcontrol Pty Ltd. (Australia), among others.

The global military microgrids market is expected to reach USD 8.4 billion by 2036 from an estimated USD 3.6 billion in 2026, at a CAGR of 8.8% during the forecast period 2026-2036.

In 2026, the hybrid microgrids segment is expected to hold the largest share of the global military microgrids market, driven by hybrid systems being the most widely adopted configuration combining diesel backup with solar and battery storage to reduce fuel consumption while keeping existing infrastructure in place.

The off-grid/islanded microgrids segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the growing number of forward operating bases in remote areas with no commercial grid access and the rising military priority given to complete energy independence from civilian infrastructure.

In 2026, the military bases and installations segment is expected to hold the largest share of the global military microgrids market, reflecting permanent bases representing the highest total power consumption and the greatest financial return from energy efficiency and resilience investment.

The forward operating bases segment is projected to register the highest CAGR during the forecast period, driven by the growing number of forward deployments in remote areas where fuel logistics are expensive and dangerous, making hybrid microgrid systems with reduced diesel dependence highly attractive.

The market is primarily driven by the military's need for reliable, self-sufficient power at bases that cannot afford to depend on civilian power infrastructure, and by the very high and dangerous cost of transporting diesel fuel to remote forward operating bases, making renewable and hybrid energy systems a compelling investment on both operational security and financial grounds.

Key players are Lockheed Martin Corporation (U.S.), RTX Corporation/Raytheon Technologies (U.S.), Schneider Electric SE (France), Siemens AG (Germany), ABB Ltd. (Switzerland), Eaton Corporation plc (Ireland), General Electric Company (U.S.), Honeywell International Inc. (U.S.), Rolls-Royce plc (UK), Caterpillar Inc. (U.S.), Cummins Inc. (U.S.), PowerSecure/Southern Company (U.S.), Saft Groupe S.A. (France), SFC Energy AG (Germany), and Ampcontrol Pty Ltd. (Australia), among others.

Asia-Pacific is expected to register the highest growth rate in the global military microgrids market during the forecast period 2026-2036, driven by rising security tensions in the Indo-Pacific compelling Australia, Japan, India, and South Korea to invest in base hardening and energy resilience, alongside China's large domestic military energy modernization program.

Published Date: Aug-2025

Published Date: Oct-2024

Published Date: Aug-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates