Resources

About Us

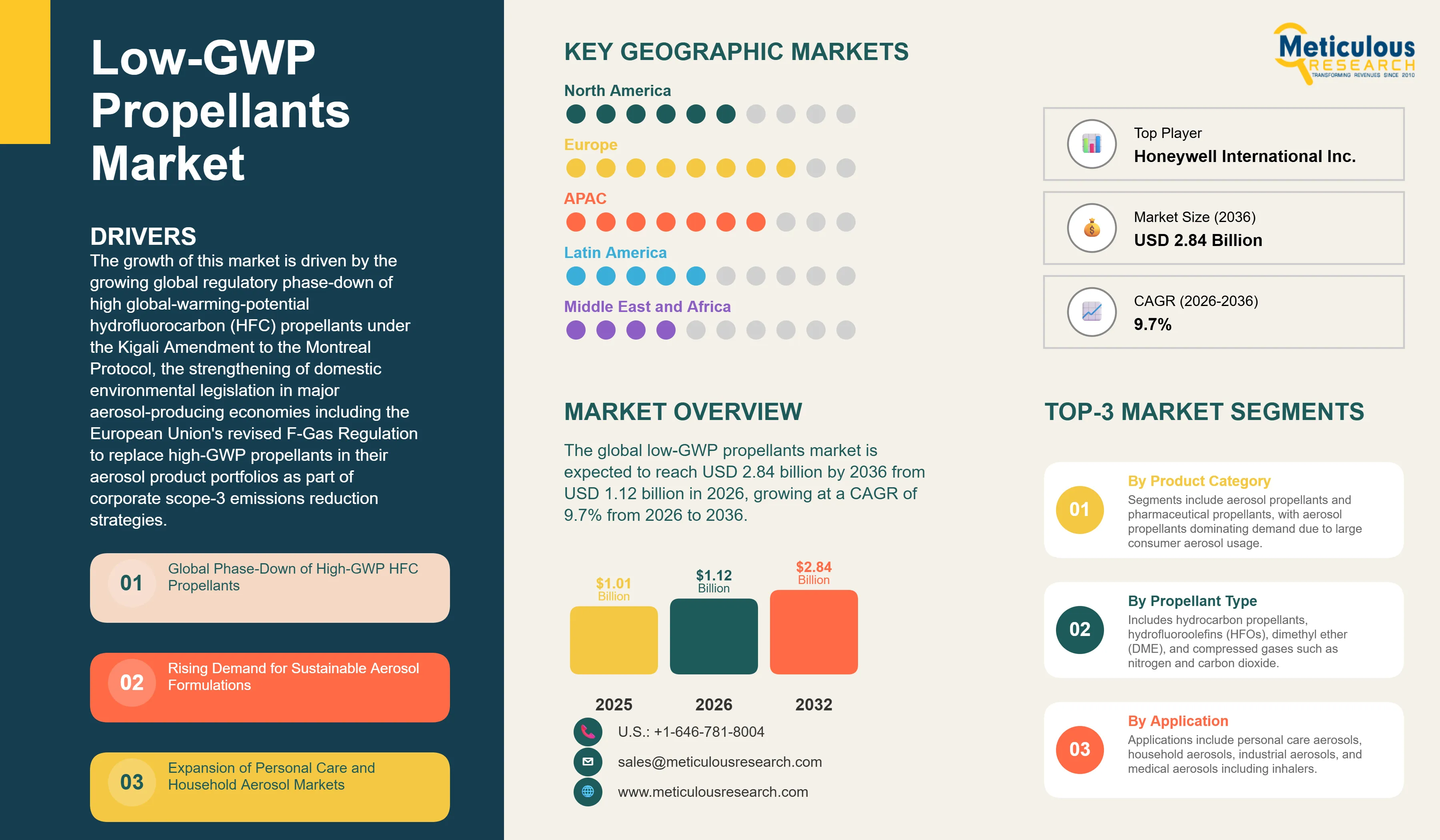

The global low-GWP propellants market was valued at USD 1.01 billion in 2025. This market is expected to reach USD 2.84 billion by 2036 from USD 1.12 billion in 2026, growing at a CAGR of 9.7% from 2026 to 2036.

The growth of this market is driven by the growing global regulatory phase-down of high global-warming-potential hydrofluorocarbon (HFC) propellants under the Kigali Amendment to the Montreal Protocol, the strengthening of domestic environmental legislation in major aerosol-producing economies including the European Union's revised F-Gas Regulation and the United States' American Innovation and Manufacturing (AIM) Act, and the growing commitment of multinational consumer goods and pharmaceutical companies to replace high-GWP propellants in their aerosol product portfolios as part of corporate scope-3 emissions reduction strategies. Low-GWP propellants encompass a diverse family of chemistries including hydrofluoroolefins (HFOs), hydrocarbon propellants, dimethyl ether (DME), and compressed gases including nitrogen, carbon dioxide, and nitrous oxide, each offering significantly reduced climate impact relative to the legacy HFC-134a and HFC-227ea propellants they are progressively replacing across aerosol, pharmaceutical, and specialty gas applications.

The transition to low-GWP propellants is fundamentally restructuring the global aerosol propellants supply chain, creating both significant commercial opportunities for chemical manufacturers with the fluorochemical synthesis capabilities and intellectual property required to produce HFO-based propellants, and near-term challenges for aerosol filling companies and consumer goods brand owners who must reformulate established aerosol product lines to maintain performance equivalence with new propellant chemistries. The pharmaceutical aerosol segment faces the most technically complex and commercially consequential propellant transition, as the replacement of HFA-134a in pressurized metered-dose inhalers (MDIs) used by hundreds of millions of asthma and COPD patients globally requires clinical reformulation, new drug device combination regulatory approvals, and coordinated market introduction that will reshape the pharmaceutical aerosol propellant market through the 2030s.

Click here to: Get Free Sample Pages of this Report

Low-GWP propellants are distinguished from their high-GWP predecessors by their significantly reduced capacity to absorb infrared radiation in the atmosphere and thereby contribute to the greenhouse effect over a 100-year time horizon, the standard metric used in the GWP calculation framework. Legacy HFC propellants including HFC-134a, which has a GWP of 1,430 times that of carbon dioxide, and HFC-227ea, with a GWP of 3,220, have served the aerosol and pharmaceutical industries for decades as technically effective but climatically problematic alternatives to the ozone-depleting chlorofluorocarbon (CFC) propellants they replaced in the 1990s. The current propellant transition is therefore the second major reformulation cycle in 30 years for the global aerosol industry, driven this time not by ozone depletion but by the HFC contribution to anthropogenic climate forcing, which the Kigali Amendment's signatories have committed to reduce by phasing down HFC consumption according to schedules differentiated by country development status

The technical diversity of the low-GWP propellant family reflects the range of performance requirements and regulatory environments across the multiple application segments that aerosol propellants serve. Hydrocarbon propellants including propane, n-butane, and isobutane offer near-zero GWP and very low cost, and are already the dominant propellant type in the European consumer aerosol market, where they account for approximately 65 percent of propellant volume across personal care and household applications. Their primary limitation is flammability, which restricts their use in applications where ignition sources are present, in pharmaceutical MDI applications where flammability is unacceptable for safety reasons, and in certain industrial applications requiring use near heat or electrical equipment. Dimethyl ether (DME) offers a GWP below 1 and additional solvent properties that make it particularly effective in certain specialty aerosol formulations, though its high water reactivity limits its compatibility with some active ingredients.

Hydrofluoroolefin propellants represent the most technically advanced class of low-GWP alternatives, combining very low GWP values — HFO-1234ze has a GWP of 7 and HFO-1234yf a GWP of less than 1 — with non-flammable or mildly flammable characteristics that address the safety constraints of pharmaceutical MDI and premium consumer aerosol applications. The HFO propellant market is dominated by Honeywell International, which holds a commanding intellectual property position through its Solstice HFO product family developed from a significant multi-year research and development investment, and The Chemours Company, with its Opteon-branded HFO products. The duopolistic supply structure of the HFO market, combined with the capital-intensive fluorochemical synthesis facilities required for production, creates a supply concentration dynamic that influences pricing and availability for aerosol fillers and pharmaceutical manufacturers seeking to transition to HFO-based propellant systems.

Compressed gas propellants including nitrogen, carbon dioxide, and nitrous oxide offer genuinely zero or near-zero GWP values and non-flammable operation, but their gas-phase propellant delivery mechanism differs fundamentally from liquefied propellant systems, producing different spray characteristics including diminishing spray pressure as the propellant depletes that limits their suitability for applications requiring consistent spray performance throughout the product's use life. Despite these technical constraints, compressed gas propellants are gaining traction in niche applications including certain cosmetic and food aerosol products where the application performance limitations are acceptable and the extreme environmental profile provides a strong marketing advantage.

Transition Toward Ultra-Low GWP Aerosol Propellants

The most consequential trend reshaping the low-GWP propellants market is the accelerating pace of HFC propellant phase-down under both international treaty obligations and domestic regulatory frameworks, which is converting the long-term substitution imperative into near-term commercial procurement decisions across the aerosol supply chain. The EU F-Gas Regulation's phase-down schedule requires HFC quantities placed on the European market to decline progressively to 15 percent of 2015 baseline levels by 2030, with the propellant sector facing specific restrictions that are effectively forcing the transition to hydrocarbon, HFO, DME, and compressed gas alternatives ahead of the broader HFC market schedule. In the United States, the AIM Act directs EPA to establish HFC phase-down schedules and sector-specific restrictions through its SNAP program review process, with aerosol propellants among the application categories subject to the earliest substitution requirements.

Aerosol filling companies and consumer goods brand owners who have historically formulated products with HFC-134a as a carrier or propellant component are accelerating reformulation programs to comply with these regulatory timelines, creating a surge in demand for HFO-based and hydrocarbon propellant alternatives. Honeywell's Solstice 1234ze propellant, which has been qualified by multiple consumer goods companies as a performance-equivalent substitute for HFC-134a in selected aerosol applications, is experiencing strong demand growth as brand owners progress regulatory compliance reformulation work. The pace of this transition is expected to accelerate significantly through 2026 to 2030 as the regulatory phase-down schedule tightens and the cost of holding HFC-containing aerosol product formulations in the market increases through both rising HFC quotas prices and brand reputation exposure for companies that have made public sustainability commitments.

Development of Next-Generation Propellants for Metered Dose Inhalers

The pharmaceutical MDI propellant transition is the highest-stakes and most technically complex element of the global low-GWP propellant market evolution, involving the reformulation of inhaler products used by an estimated 400 million patients worldwide for the management of asthma and COPD. The current standard MDI propellant, HFA-134a, has a GWP of 1,430 and the pharmaceutical sector's annual MDI propellant consumption represents a material and growing fraction of total HFC usage in markets that track pharmaceutical emissions separately from industrial applications. The UK National Health Service, which has established a formal program to transition its MDI formulary toward low-GWP alternatives, has highlighted pharmaceutical aerosol propellants as one of the NHS's largest single sources of scope-3 greenhouse gas emissions, generating significant policy and procurement pressure for pharmaceutical manufacturers supplying NHS-contracted inhaler products.

AstraZeneca has the most advanced commercial program for next-generation low-GWP MDI development, with its transition program targeting the replacement of HFA-134a across its Symbicort, Pulmicort, and Bricanyl inhaler portfolio using HFO-1234ze(E) propellant, which has a GWP below 10. Chiesi Farmaceutici is pursuing HFA-152a, which has a GWP of 148, as its primary transition propellant across its branded and generic MDI portfolio. GSK, Boehringer Ingelheim, and Teva are at various stages of preclinical and clinical development for low-GWP MDI formulations across their respective inhaler drug portfolios. The regulatory pathway for reformulated MDIs requires demonstration of bioequivalence to the currently marketed formulation, which involves clinical pharmacokinetic studies that represent significant time and investment barriers to market introduction, making the MDI propellant transition a multi-year program rather than a near-term product switch. Propellant suppliers Honeywell and The Chemours Company are both investing in pharmaceutical-grade HFO and HFA production capacity and regulatory master file development to support the clinical and commercial supply requirements of their pharmaceutical manufacturer customers progressing MDI transition programs.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 2.84 Billion |

|

Market Size in 2026 |

USD 1.12 Billion |

|

Market Size in 2025 |

USD 1.01 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 9.7% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Category, Propellant Type, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

How Do Aerosol Propellants Lead the Market?

In 2026, the aerosol propellants segment is expected to hold the largest share of the low-GWP propellants market. Consumer aerosol applications spanning personal care, household, and industrial products collectively represent the largest volume market for propellant gases globally, with annual propellant consumption measured in hundreds of thousands of metric tons. The transition of this large-volume segment toward low-GWP alternatives — predominantly hydrocarbon blends for flammability-tolerant applications and HFO-based propellants for flammability-sensitive premium applications — is generating the largest absolute demand volume for low-GWP propellant producers. In the European market, the transition from HFC-134a to hydrocarbon and HFO alternatives in consumer aerosols is substantially complete for the major international brand owners, with the ongoing transition concentrated in regional and private-label aerosol products and in emerging market supply chains supplying European-regulated end markets.

However, the pharmaceutical propellants segment is expected to witness the fastest growth during the forecast period, driven by the scale and urgency of the MDI propellant transition across major global pharmaceutical markets. The NHS England and NHS Scotland commitments to transition their formularies toward low-GWP MDIs by 2030 are the most specific and binding institutional procurement commitments in the global MDI market, and have stimulated AstraZeneca, Chiesi, and other NHS-contracted manufacturers to accelerate their low-GWP MDI development timelines. The commercial launch of first-wave low-GWP MDI products in the United Kingdom and EU markets within the forecast period will generate initial pharmaceutical propellant demand that scales rapidly as these products gain formulary adoption and manufacturing volumes ramp up. The high per-unit value of pharmaceutical propellant revenues relative to consumer aerosol propellant revenues will drive this segment to represent a disproportionately large share of low-GWP propellant market value growth through 2036.

Why Do Hydrocarbon Propellants Lead the Market by Volume?

In 2026, the hydrocarbon propellants segment is expected to hold the largest share of the low-GWP propellants market by both volume and value. Propane, n-butane, and isobutane have served as the dominant propellant type in European consumer aerosols for over two decades, and their combination of near-zero GWP, very low cost relative to fluorinated alternatives, and established supply chain availability from large-scale petrochemical production makes them the default transition choice for the large majority of personal care and household aerosol applications where flammability is a manageable rather than prohibitive consideration. In Asia-Pacific, Latin America, and the Middle East, where aerosol markets are growing rapidly and price sensitivity constrains the adoption of premium HFO alternatives, hydrocarbon propellants are the dominant low-GWP option adopted by local and regional aerosol producers. The major global aerosol propellant suppliers including Linde, Air Liquide, and a network of regional hydrocarbon gas suppliers provide reliable and competitively priced hydrocarbon propellant supply to aerosol filling operations globally.

However, the HFO segment is expected to witness the fastest growth during the forecast period. HFO-1234ze and HFO-1234yf are positioned as the premium technical solution for applications requiring non-flammable or low-flammability propellant chemistry combined with very low GWP, and the volume of applications requiring this combination will expand significantly as the MDI propellant transition scales and as premium consumer aerosol applications that cannot use hydrocarbon propellants due to flammability concerns complete their transition away from HFC-134a. The progressive expansion of HFO production capacity by Honeywell and Chemours, combined with the entry of additional Asian HFO producers, is expected to improve HFO supply security and exercise moderate pricing pressure through the forecast period.

How Do Personal Care Aerosols Lead the Market?

In 2026, the personal care aerosols segment is expected to hold the largest share of the low-GWP propellants market. Deodorants, body sprays, and hair care products collectively account for the largest category of global aerosol unit production, and personal care aerosols represent the application segment where the low-GWP propellant transition is most commercially advanced. Major multinational personal care companies including Unilever (Dove, Rexona, Axe), Procter & Gamble (Old Spice, Pantene), and Beiersdorf (Nivea, 8x4) have substantially completed transitions of their European aerosol portfolios to hydrocarbon propellant formulations and are actively progressing similar transitions in other regulated markets. The combination of consumer-facing sustainability communication about carbon-reduced products, retailer sustainability procurement requirements, and regulatory compliance obligations is creating aligned incentives throughout the personal care aerosol supply chain for low-GWP propellant adoption.

However, the medical aerosols segment is expected to witness the fastest growth during the forecast period, driven by the MDI propellant transition's progressive commercial scale-up as pharmaceutical companies complete clinical reformulation programs and introduce low-GWP MDI products to market. The medical aerosol application is unique in combining high per-unit propellant value, long-term supply commitment structures tied to pharmaceutical product life cycles, and strong institutional purchasing driver support from health system sustainability programs, creating a highly attractive commercial profile for low-GWP propellant suppliers qualified for pharmaceutical-grade supply.

How is Europe Maintaining Market Leadership?

In 2026, Europe is expected to hold the largest share of the global low-GWP propellants market. Europe's market leadership position is a direct consequence of the EU F-Gas Regulation's aggressive HFC phase-down schedule, which has driven the European aerosol industry to complete the majority of its HFC-to-low-GWP propellant transition ahead of all other global markets. European aerosol production is concentrated in Germany, France, the United Kingdom, Italy, and Spain, which together operate the majority of the EU's aerosol filling capacity and are the primary procurement points for low-GWP propellant supply in the European market. The European propellant supply chain is well-developed for both hydrocarbon and HFO propellants, with established Harp International, Gas Servei, and regional hydrocarbon gas suppliers providing reliable supply infrastructure, and Arkema, Nouryon, and Tazzetti providing European-based fluorocarbon propellant supply capabilities that reduce import dependence for HFO product categories.

The United Kingdom's NHS-driven MDI propellant transition program adds a pharmaceutical dimension to European low-GWP propellant market leadership that other regions have not yet replicated at equivalent institutional scale. The NHS England and NHS Scotland programmes targeting low-GWP inhaler prescribing represent the most advanced government-level commitment to the MDI propellant transition globally, and the United Kingdom's disproportionate influence on global pharmaceutical manufacturing decisions through its NHS market position and MHRA regulatory interactions is expected to accelerate low-GWP MDI introduction timelines for manufacturers seeking to maintain NHS formulary positions.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the low-GWP propellants market during the forecast period, driven by the combination of rapid aerosol market volume growth, progressive tightening of environmental regulations in China, Japan, South Korea, and India, and the region's significant HFO production capacity expansion programs.

China is the largest and most commercially important growth market within Asia-Pacific. China's HFC phase-down commitment under the Kigali Amendment follows the Article 5 developing country schedule, with freeze of HFC consumption baseline scheduled and phase-down steps extending through 2045, but domestic regulatory implementation through China's National Adjustment Plan is expected to drive earlier adoption of low-GWP alternatives in export-oriented aerosol manufacturing than the international treaty minimum schedule would require. Chinese chemical companies including Sinochem Lantian, Zhejiang Juhua, and Shandong Yuean are investing in HFO and HFC-alternative production capacity that will serve both domestic demand and export markets, positioning China as an increasingly significant low-GWP propellant production center through the forecast period. India's aerosol market, while smaller than China's, is growing rapidly driven by personal care product market expansion among a young and increasingly affluent urban population, and India's Article 5 Kigali commitments are beginning to influence domestic aerosol industry formulation practices as major multinational brand owners extend their global low-GWP propellant standards to their Indian manufacturing operations. Japan and South Korea, as developed economies with advanced HFC regulation frameworks and sophisticated aerosol and pharmaceutical manufacturing industries, represent stable and high-value low-GWP propellant markets where transition programs are already well advanced.

Some of the key companies operating in the global low-GWP propellants market are Honeywell International Inc., The Chemours Company, Arkema S.A., Nouryon, Linde plc, Daikin Industries Ltd., AGC Inc., SRF Limited, Orbia (Koura Global), Tazzetti S.p.A., Harp International Ltd., Gas Servei S.A., Sinochem Lantian Co., Ltd., Zhejiang Juhua Co., Ltd., and Shandong Yuean Chemical Industry Co., Ltd.

The global low-GWP propellants market is expected to grow from USD 1.12 billion in 2026 to USD 2.84 billion by 2036.

The global low-GWP propellants market is projected to grow at a CAGR of 9.7% from 2026 to 2036.

The aerosol propellants segment is expected to dominate the overall market in 2026. However, the pharmaceutical propellants segment is expected to witness the fastest CAGR, driven by the large-scale MDI propellant transition across major global pharmaceutical markets, the NHS-mandated low-GWP MDI formulary program in the United Kingdom, and the high per-unit propellant value of pharmaceutical-grade HFO and HFA-152a supply contracts associated with registered inhaler drug product life cycles.

The hydrocarbon propellants segment is expected to dominate the overall market in 2026 by volume, reflecting the maturity of hydrocarbon propellant adoption across European and international consumer aerosol applications. However, the HFO segment is expected to witness the fastest CAGR, driven by HFO adoption in pharmaceutical MDI applications, premium consumer aerosol applications requiring non-flammable low-GWP propellant performance, and new industrial applications where HFO properties enable transition from HFC-based formulations.

The personal care aerosols segment is expected to dominate the overall market in 2026. However, the medical aerosols segment is expected to witness the fastest CAGR, driven by the commercial scale-up of low-GWP MDI products across the global inhaler market and the high revenue intensity of pharmaceutical propellant supply relative to consumer aerosol propellant volumes.

Europe is expected to lead the global market in 2026, supported by the EU F-Gas Regulation's advanced HFC phase-down schedule and the United Kingdom's NHS-driven MDI propellant transition program. However, Asia-Pacific is expected to witness the fastest CAGR, driven by China's large and growing aerosol market, India's rapidly expanding personal care aerosol consumption, and the region's significant investment in new low-GWP propellant production capacity.

Some of the major players are Honeywell International Inc., The Chemours Company, Arkema S.A., Nouryon, Linde plc, Daikin Industries Ltd., AGC Inc., SRF Limited, Orbia (Koura Global), Tazzetti S.p.A., Harp International Ltd., Gas Servei S.A., Sinochem Lantian Co., Ltd., Zhejiang Juhua Co., Ltd., and Shandong Yuean Chemical Industry Co., Ltd.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Global Phase-Down of High-GWP HFC Propellants

4.2.1.2. Rising Demand for Sustainable Aerosol Formulations

4.2.1.3. Expansion of Personal Care and Household Aerosol Markets

4.2.1.4. Increasing Adoption of Low-GWP Propellants in Pharmaceutical Inhalers

4.2.2. Restraints

4.2.2.1. High Production Cost of HFO-Based Propellants

4.2.2.2. Flammability Concerns Associated with Hydrocarbon Propellants

4.2.2.3. Limited Production Capacity for Advanced Low-GWP Propellants

4.2.3. Opportunities

4.2.3.1. Development of Ultra-Low GWP Propellants for Metered Dose Inhalers

4.2.3.2. Expansion of Sustainable Packaging in Consumer Products

4.2.3.3. Increasing Aerosol Consumption in Emerging Markets

4.2.3.4. Innovation in Environment-Friendly Propellant Formulations

4.2.4. Challenges

4.2.4.1. Regulatory Compliance Across Regions

4.2.4.2. Safety and Storage Challenges for Alternative Propellants

4.3. Key Market Trends & Innovation Landscape

4.3.1. Transition Toward Ultra-Low GWP Aerosol Propellants

4.3.2. Increasing Adoption of HFO-Based Propellants in Consumer Aerosols

4.3.3. Development of Next-Generation Propellants for Metered Dose Inhalers

4.3.4. Sustainability Initiatives and Carbon Reduction in Aerosol Packaging

4.3.5. Innovation in Eco-Friendly Aerosol Formulations

4.4. Technology Landscape

4.4.1. Hydrofluoroolefin (HFO) Propellant Technologies

4.4.2. Hydrocarbon Propellant Technologies

4.4.3. Dimethyl Ether (DME) Propellant Technologies

4.4.4. Compressed Gas Propellant Technologies

4.5. Regulatory and Standards Environment

4.5.1. Kigali Amendment to the Montreal Protocol

4.5.2. EU F-Gas Regulation

4.5.3. U.S. AIM Act and EPA SNAP Program

4.5.4. Environmental Regulations in Asia-Pacific

4.6. Porter's Five Forces Analysis

4.7. Supply Chain & Ecosystem Analysis

4.7.1. Feedstock Suppliers

4.7.2. Propellant Manufacturers

4.7.3. Aerosol Can & Packaging Manufacturers

4.7.4. Aerosol Filling Companies

4.7.5. Brand Owners / Consumer Product Companies

4.7.6. Distribution Channels

4.8. Strategic Developments & Investment Landscape

4.8.1. Capacity Expansions for Low-GWP Propellant Production

4.8.2. Strategic Partnerships in Sustainable Aerosol Technologies

4.8.3. Investments in Next-Generation MDI Propellants

4.8.4. Mergers & Acquisitions in the Propellants Industry

4.9. Patent Landscape and IP Analysis

4.10. Pricing Analysis by Propellant Type and Region

5. Low-GWP Propellants Market, by Product Category

5.1. Introduction

5.2. Aerosol Propellants

5.2.1. Hydrofluoroolefins (HFO)

5.2.2. Hydrocarbon Propellants

5.2.3. Dimethyl Ether (DME)

5.2.4. Compressed Gas Propellants

5.3. Pharmaceutical Propellants (MDI Propellants)

5.3.1. HFO-1234ze(E)

5.3.2. HFA-152a

5.3.3. Next-Generation Ultra-Low GWP MDI Propellants

6. Low-GWP Propellants Market, by Propellant Type

6.1. Introduction

6.2. Hydrofluoroolefins (HFO)

6.2.1. HFO-1234ze

6.2.2. HFO-1234yf

6.2.3. HFO Blends

6.3. Hydrocarbon Propellants

6.3.1. Propane

6.3.2. n-Butane

6.3.3. Isobutane

6.4. Dimethyl Ether (DME)

6.5. Compressed Gas Propellants

6.5.1. Nitrogen

6.5.2. Carbon Dioxide

6.5.3. Nitrous Oxide

6.6. Other Low-GWP Propellants

7. Low-GWP Propellants Market, by Application

7.1. Introduction

7.2. Personal Care Aerosols

7.2.1. Deodorants & Body Sprays

7.2.2. Hair Sprays

7.2.3. Shaving Foams & Gels

7.3. Household Aerosols

7.3.1. Air Fresheners

7.3.2. Insecticides

7.3.3. Cleaning Products

7.4. Industrial Aerosols

7.4.1. Lubricants

7.4.2. Spray Paints & Coatings

7.4.3. Electronics Cleaning Sprays

7.5. Medical Aerosols

7.5.1. Metered Dose Inhalers (MDIs)

7.5.2. Topical Pharmaceutical Sprays

7.6. Food & Specialty Aerosols

7.6.1. Whipped Cream Dispensers

7.6.2. Cooking Sprays

7.6.3. Other Specialty Aerosol Products

8. Low-GWP Propellants Market, by Geography

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.3.6. Netherlands

8.3.7. Belgium

8.3.8. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. Japan

8.4.3. India

8.4.4. South Korea

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Thailand

8.4.8. Vietnam

8.4.9. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Argentina

8.5.4. Chile

8.5.5. Colombia

8.5.6. Rest of Latin America

8.6. Middle East & Africa

8.6.1. Saudi Arabia

8.6.2. UAE

8.6.3. South Africa

8.6.4. Turkey

8.6.5. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Ranking/Positioning Analysis of Key Players, 2025

10. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Honeywell International Inc.

10.2. The Chemours Company

10.3. Arkema S.A.

10.4. Nouryon

10.5. Linde plc

10.6. Daikin Industries Ltd.

10.7. AGC Inc.

10.8. SRF Limited

10.9. Orbia (Koura Global)

10.10. Tazzetti S.p.A.

10.11. Harp International Ltd.

10.12. Gas Servei S.A.

10.13. Sinochem Lantian Co., Ltd.

10.14. Zhejiang Juhua Co., Ltd.

10.15. Shandong Yuean Chemical Industry Co., Ltd.

11. Appendix

11.1. Additional Customization

11.2. Related Reports

Published Date: May-2025

Published Date: May-2024

Subscribe to get the latest industry updates