Resources

About Us

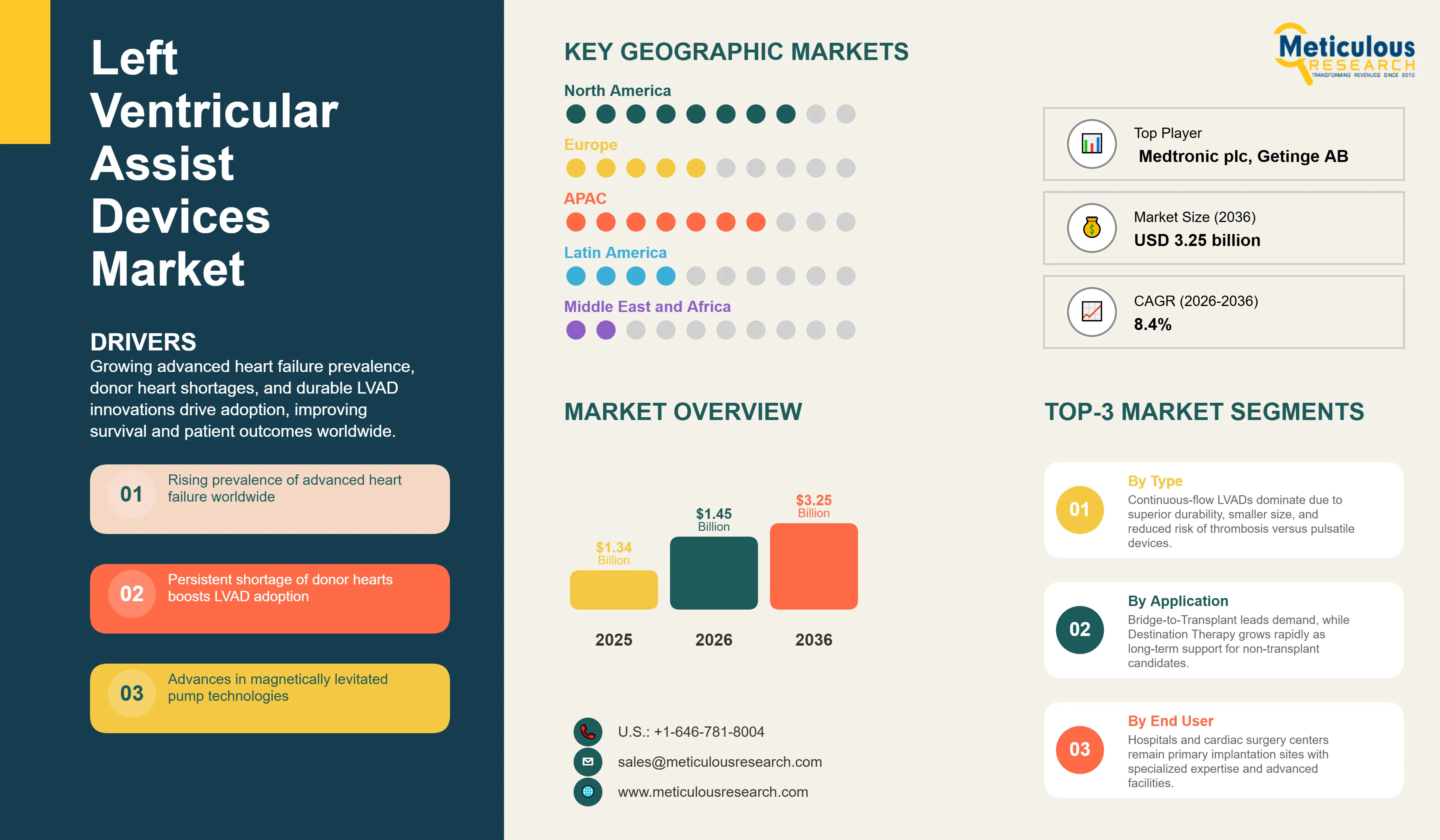

The global left ventricular assist devices market is estimated to be USD 1.45 billion in 2026. This market is expected to reach USD 3.25 billion by 2036, growing at a CAGR of 8.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global left ventricular assist devices (LVAD) market represents one of the most advanced segments of mechanical circulatory support, providing a life-sustaining therapy for patients with end-stage (Stage D) heart failure. Cardiovascular diseases remain the leading cause of mortality worldwide, accounting for approximately 19.8 million deaths in 2022, or 32% of all global deaths, according to the World Health Organization (WHO). Population aging and the growing prevalence of chronic cardiovascular disorders are increasing the number of patients progressing to advanced heart failure, thereby expanding the need for durable circulatory support therapies.

Mechanical circulatory support has evolved from an experimental treatment into an established therapy for carefully selected patients with refractory heart failure. Durable LVADs are used both as a bridge-to-transplant for patients awaiting donor organs and as destination therapy for patients who are not candidates for transplantation. According to the International Society for Heart and Lung Transplantation (ISHLT), durable LVAD implantation has become an integral component of advanced heart failure management, helping improve survival, functional capacity, and quality of life in patients with severe left ventricular dysfunction.

Technological advancements have transformed the market from first-generation pulsatile pumps to predominantly continuous-flow devices, particularly magnetically levitated centrifugal pumps that offer improved durability and enhanced hemocompatibility. These innovations have contributed to lower rates of pump thrombosis and mechanical failure, thereby improving long-term clinical outcomes. The HeartMate 3 system, employing fully magnetically levitated centrifugal-flow technology, has become the dominant platform in the global durable LVAD market.

Demand for LVADs is also supported by the persistent imbalance between the number of patients requiring heart transplantation and the limited availability of donor hearts. Bridge-to-transplant, destination therapy, bridge-to-recovery, and bridge-to-candidacy applications have expanded the clinical utility of LVADs, enabling physicians to tailor treatment strategies to individual patient profiles. Furthermore, increasing healthcare expenditure, improved heart failure management programs, and ongoing innovations in miniaturized pump designs and wireless energy transfer technologies are expected to broaden patient eligibility and support continued market growth over the next decade.

Drivers: Bridging the Gap in Heart Transplantation and Enhancing Long-Term Survival for Non-Transplant Candidates

The growth of the global LVAD market is primarily driven by the critical shortage of donor hearts and the significant clinical improvements in device durability that allow for long-term permanent support.

Persistent Scarcity of Donor Hearts and Growing Transplant Waitlists

The global demand for heart transplantation far exceeds the supply of available donor organs. Thousands of patients remain on transplant waitlists for extended periods, during which their clinical condition often deteriorates. LVADs serve as a critical life-sustaining 'bridge' that allows these patients to survive until a suitable organ becomes available. This persistent gap in transplantation remains a primary driver for the market, as clinical guidelines from major cardiovascular societies like the AHA and ESC emphasize the use of mechanical support to maintain end-organ perfusion and improve transplant candidacy in eligible patients.

Technological Advancements in Hemocompatibility and Device Durability

The transition to third-generation centrifugal pumps with Full MagLev technology has revolutionized the LVAD market. These advancements have significantly reduced pump-related complications such as thrombosis, hemolysis, and stroke, which were major barriers to long-term use. The improved safety profile and durability of modern devices have made them a viable permanent therapy (destination therapy) for patients who are not eligible for transplantation. This technological maturity is driving confidence among clinicians and patients alike, leading to earlier intervention and broader adoption of mechanical circulatory support.

Restraints: Navigating Post-Operative Complications and the High Economic Burden of LVAD Therapy

Despite their life-saving potential, the adoption of LVADs is restrained by the risk of long-term adverse events and the substantial costs associated with the device, the surgical procedure, and chronic patient management.

Risk of Device-Related Adverse Events and Quality of Life Challenges

Patients living with LVADs remain at risk for significant complications, including driveline infections, gastrointestinal bleeding, and neurological events. Furthermore, the requirement for an external power source and a percutaneous driveline can impose significant lifestyle restrictions and psychological burdens on patients. These potential complications and the impact on daily living can lead to clinical hesitancy, particularly in patients who are relatively stable on medical management, thereby restraining the overall market penetration.

Substantial Cost of Devices and Intensive Resource Requirements

LVAD therapy is one of the most expensive interventions in cardiovascular medicine. The high cost of the durable pump, combined with the resource-intensive surgical procedure and the need for lifelong specialized follow-up, creates a significant economic burden. In many healthcare systems, particularly in emerging economies, the lack of comprehensive reimbursement or high out-of-pocket costs limits access to this therapy. Budgetary constraints in hospitals also restrict the number of centers capable of offering LVAD implantation, further limiting market growth.

Opportunities: Pioneering Fully Implantable Systems and Expanding into Emerging Markets with Specialized Cardiac Care

The future of the LVAD market lies in the development of 'fully implantable' systems that eliminate the need for a percutaneous driveline and the expansion of mechanical support into underserved global regions.

Development of Wireless Power Transfer and Fully Implantable LVAD Systems

The development of Transcutaneous Energy Transfer (TET) systems represents a major opportunity for the market. By eliminating the driveline, which is the primary source of infection and a major lifestyle constraint, fully implantable LVADs could drastically improve patient quality of life and reduce hospital readmissions. This technological breakthrough would likely expand the eligible patient population for destination therapy and could make LVAD support a more attractive alternative to transplantation for a broader range of patients.

Expansion of Specialized Heart Failure Centers in Emerging Economies

There is a significant opportunity for market expansion in the Asia-Pacific and Latin American regions. As countries like China, India, and Brazil invest in specialized cardiac surgery centers and heart failure clinics, the infrastructure to support LVAD implantation is growing. Developing more cost-effective devices or regional manufacturing hubs could further accelerate adoption in these high-potential markets. Furthermore, increasing awareness among regional cardiologists about the benefits of mechanical support for advanced heart failure offers a pathway for significant long-term growth.

Accelerated Adoption of Destination Therapy as a Primary Treatment Modality

A major trend in 2026 is the growing use of destination therapy (DT) as the dominant indication for durable LVAD implantation. According to the Society of Thoracic Surgeons (STS) and INTERMACS registry reports, destination therapy has accounted for the majority of durable LVAD implants in recent years, reflecting the limited availability of donor hearts and expanding eligibility criteria for long-term mechanical support. In 2024, only about 4,500 heart transplants were performed worldwide according to the International Society for Heart and Lung Transplantation (ISHLT), while millions of patients live with advanced heart failure. In parallel, five-year outcomes from the MOMENTUM 3 trial demonstrated survival rates approaching 58% with Abbott's HeartMate 3 device, supporting updated guidelines from the American Heart Association (AHA), American College of Cardiology (ACC), and ISHLT that recognize durable LVADs as an established therapy for patients ineligible for transplantation. These developments are accelerating the acceptance of mechanical circulatory support as a permanent treatment strategy rather than solely a bridge-to-transplant.

Integration of AI-Driven Remote Monitoring and Predictive Diagnostics

The integration of digital health technologies and artificial intelligence into LVAD management is emerging as a key trend. Data from the STS-INTERMACS registry indicate that more than 40,000 mechanical circulatory support devices have been enrolled since the registry's inception, generating large volumes of pump performance and patient data that are increasingly being utilized for predictive analytics. Modern centrifugal-flow systems equipped with advanced sensors enable continuous monitoring of pump speed, flow, and power consumption, allowing clinicians to identify complications such as suction events, right-heart failure, and thrombosis at earlier stages. In addition, the U.S. Centers for Medicare & Medicaid Services (CMS) has expanded reimbursement pathways for remote patient monitoring services, encouraging broader adoption of telehealth-based follow-up programs. AI-assisted analysis and remote monitoring platforms are helping reduce avoidable hospital readmissions, which remain a major burden in heart failure management, where the U.S. Centers for Disease Control and Prevention (CDC) estimates nearly one million heart failure-related hospitalizations annually. Consequently, predictive diagnostics and connected care ecosystems are becoming increasingly important components of long-term LVAD management.

Analysis by Type of Flow

Based on the type of flow, the continuous-flow LVADs segment is expected to hold the largest share of the global left ventricular assist devices market in 2026. This dominant position is due to the complete technological shift from pulsatile to continuous-flow pumps, which offer superior durability, smaller size, and significantly lower complication rates. Within this segment, centrifugal continuous-flow LVADs are projected to register the highest CAGR during the forecast period. The adoption of Fully Magnetically Levitated (Full MagLev) centrifugal technology has set a new clinical standard for hemocompatibility, driving rapid growth as clinicians prioritize devices that minimize the risk of thrombosis and stroke.

Analysis by Application

By application, the bridge-to-transplant (BTT) segment is expected to hold the largest share in 2026. The severe and persistent shortage of donor hearts globally ensures that BTT remains the primary application for LVADs, as they provide a critical life-sustaining therapy for the large population of patients awaiting transplantation. However, the destination therapy (DT) segment is projected to grow at the fastest CAGR during the forecast period. The increasing durability of modern pumps and the reduction in long-term adverse events have made LVAD support a highly effective permanent therapy for patients ineligible for transplant, driving its rapid expansion as a definitive treatment for end-stage heart failure.

Analysis by End User

By end user, the hospitals & cardiac surgery centers segment is expected to hold the largest share in 2026. The complexity of LVAD implantation requires the specialized infrastructure, advanced imaging, and expert surgical teams only found in high-volume cardiac centers. However, specialized heart failure clinics are projected to register the highest CAGR during the forecast period. As the population of patients living long-term with destination therapy devices grows, there is an increasing demand for specialized outpatient clinics that focus on chronic LVAD management, remote monitoring, and patient support, driving the rapid growth of this segment.

Largest Share: North America

North America is expected to dominate the global left ventricular assist devices market in 2026, accounting for around 45–50% of total revenue. This leadership is supported by the high burden of advanced heart failure, affecting approximately 6.7 million adults in the United States according to the Centers for Disease Control and Prevention (CDC), along with a well-established network of transplant and advanced heart failure centers. Despite a record number of approximately 4,700 heart transplants performed in the United States in 2025, the shortage of donor organs continues to drive demand for durable mechanical circulatory support. Favorable reimbursement policies under the Centers for Medicare & Medicaid Services (CMS) for both bridge-to-transplant (BTT) and destination therapy (DT), combined with strong clinical research activity and early adoption of advanced technologies, further reinforce the region's leadership. Key companies operating in the North American market include Abbott Laboratories, Jarvik Heart, Inc., Evaheart, Inc., and Berlin Heart GmbH, while Abbott's HeartMate 3 system remains the dominant durable LVAD platform.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global left ventricular assist devices market, with a CAGR of 11.2% during the forecast period. This rapid expansion is fueled by significant investments in specialized cardiac healthcare infrastructure, a rapidly aging population, and the rising burden of cardiovascular diseases in China and India. Increasing awareness of mechanical circulatory support options and the expansion of regional distribution networks are accelerating market growth. Key companies operating in the Asia Pacific market are Terumo Corporation, Sun Medical Technology, and various regional partners for global heart failure therapy leaders.

The global left ventricular assist devices market is highly consolidated, with a few major players dominating the landscape through advanced technological portfolios and extensive clinical data. Competition is focused on improving hemocompatibility to reduce adverse events and miniaturizing devices to allow for less invasive implantation techniques. Key players are investing heavily in 'next-generation' pump designs, including Full MagLev technology and wireless power transfer systems. Strategic partnerships with heart failure clinics and investments in remote monitoring platforms are also major areas of focus as companies seek to provide comprehensive patient management solutions. The market is also seeing the emergence of innovative startups focusing on specialized niche applications, such as pediatric support and temporary circulatory assistance, which are increasingly being acquired by larger medical device leaders.

Abbott Laboratories, Berlin Heart GmbH, Jarvik Heart, Inc., Evaheart, Inc., Asahi Kasei Corporation, Calon Cardio-Technology Ltd., BiVACOR, Inc., CorWave SA, FineHeart SA, Procyrion, Inc., CoreMedic GmbH, Leviticus Cardio Ltd., Windmill Cardiovascular Systems, Inc., CH-Biotech Co., Ltd., Sun Medical Technology Research Corp., ReliantHeart, Inc., Getinge AB, Medtronic plc, CARMAT SA, SynCardia Systems, LLC.

The global market is estimated at USD 1.45 billion in 2026, with a projected growth to USD 3.25 million by 2036, at a CAGR of 8.4%.

Primary drivers include the severe shortage of donor hearts and technological advancements in device durability and hemocompatibility.

Major restraints include the risk of post-operative complications (e.g., infections, bleeding) and the high economic burden of the therapy.

Opportunities lie in the development of fully implantable systems and the expansion of cardiac centers in emerging economies.

Continuous-flow LVADs are expected to hold the largest share, having completely superseded pulsatile technology with superior reliability.

Destination therapy (DT) is projected to grow at the fastest CAGR as LVAD support becomes a viable permanent alternative to transplant.

Hospitals & cardiac surgery centers are expected to hold the largest share as the primary setting for complex LVAD implantation.

North America is expected to dominate the market due to its high prevalence of heart failure and robust transplant center network.

Asia Pacific is projected to witness the fastest growth, fueled by aging populations and investments in specialized cardiac care.

Key trends include the rise of destination therapy and the integration of AI-driven remote monitoring and predictive diagnostics.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Persistent Scarcity of Donor Hearts and Growing Transplant Waitlists

4.2.1.2. Technological Advancements in Hemocompatibility and Device Durability

4.2.2. Restraints

4.2.2.1. Risk of Device-Related Adverse Events and Quality of Life Challenges

4.2.2.2. Substantial Cost of Devices and Intensive Resource Requirements

4.2.3. Opportunities

4.2.3.1. Development of Wireless Power Transfer and Fully Implantable LVAD Systems

4.2.3.2. Expansion of Specialized Heart Failure Centers in Emerging Economies

4.2.4. Trends

4.2.4.1. Accelerated Adoption of Destination Therapy as a Primary Treatment Modality

4.2.4.2. Integration of AI-Driven Remote Monitoring and Predictive Diagnostics

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Left Ventricular Assist Devices Market, by Type of Flow

5.1. Continuous-Flow LVADs

5.1.1. Centrifugal Flow

5.1.2. Axial Flow

5.2. Pulsatile-Flow LVADs

6. Global Left Ventricular Assist Devices Market, by Application

6.1. Bridge-to-Transplant (BTT)

6.2. Destination Therapy (DT)

6.3. Bridge-to-Recovery (BTR)

6.4. Bridge-to-Candidacy (BTC)

7. Global Left Ventricular Assist Devices Market, by End User

7.1. Hospitals & Cardiac Surgery Centers

7.2. Specialized Heart Failure Clinics

8. Global Left Ventricular Assist Devices Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Key Players Strategies

9.2. Market Share Analysis

9.3. Strategic Developments

9.4. Competitive Benchmarking

10. Company Profiles

10.1. Abbott Laboratories

10.2. Berlin Heart GmbH

10.3. Jarvik Heart, Inc.

10.4. Evaheart, Inc.

10.5. Asahi Kasei Corporation

10.6. Calon Cardio-Technology Ltd.

10.7. BiVACOR, Inc.

10.8. CorWave SA

10.9. FineHeart SA

10.10. Procyrion, Inc.

10.11. CoreMedic GmbH

10.12. Leviticus Cardio Ltd.

10.13. Windmill Cardiovascular Systems, Inc.

10.14. CH-Biotech Co., Ltd.

10.15. Sun Medical Technology Research Corp.

10.16. ReliantHeart, Inc.

10.17. Getinge AB

10.18. Medtronic plc

10.19. CARMAT SA

10.20. SynCardia Systems, LLC

11. Appendix

11.1. Abbreviations

11.2. Disclaimer

12. Key Questions Answered

Published Date: Aug-2026

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Jan-2025

Subscribe to get the latest industry updates