Resources

About Us

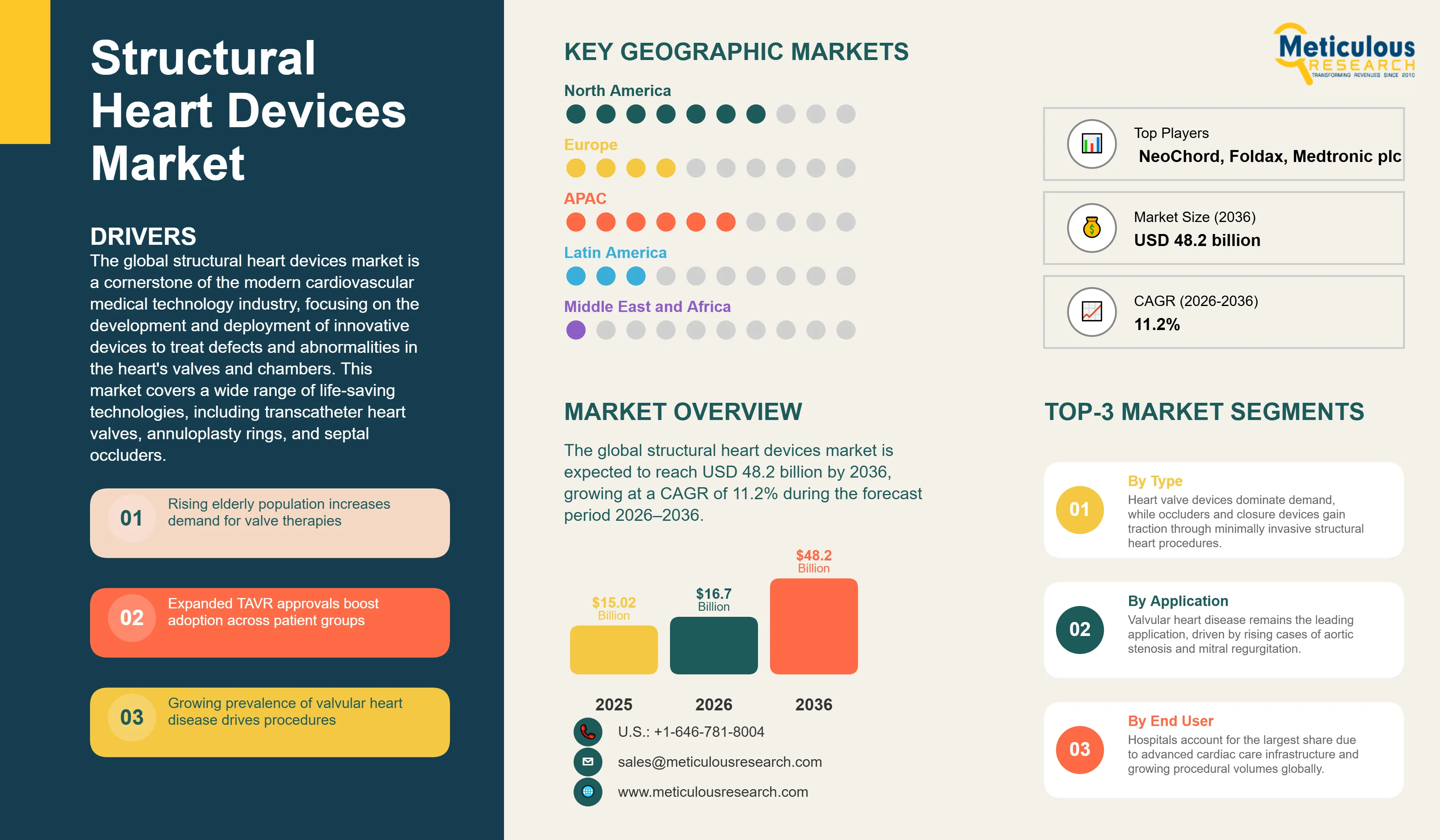

Structural Heart Devices Market Size, Share & Trends Analysis by Product (Heart Valve Devices [TAVI, TMVR, TTVR], Annuloplasty Rings, Occluders and Closure Devices, Others), Indication (Valvular Heart Disease, Cardiomyopathy, Congenital Heart Defects, Others), End User, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

Report ID: MRHC - 1042009 Pages: 246 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global structural heart devices market was valued at USD 16.7 billion in 2026. This market is expected to reach USD 48.2 billion by 2036, growing at a CAGR of 11.2% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global structural heart devices market is a cornerstone of the modern cardiovascular medical technology industry, focusing on the development and deployment of innovative devices to treat defects and abnormalities in the heart's valves and chambers. This market covers a wide range of life-saving technologies, including transcatheter heart valves, annuloplasty rings, and septal occluders. The primary focus is on addressing conditions such as aortic stenosis, mitral regurgitation, and congenital heart defects through minimally invasive or percutaneous approaches. The growth of this market is mainly driven by the global aging population, the increasing prevalence of valvular heart disease, and the clinical shift from high-risk open-heart surgery toward safer, transcatheter-based therapies.

Transcatheter Aortic Valve Replacement (TAVR) remains the dominant segment within the market, having revolutionized the treatment of severe aortic stenosis. As of 2025, TAVR has become the dominant form of aortic valve replacement in the United States, with estimates suggesting over two-thirds of procedures performed via transcatheter routes. This trend is expected to continue as FDA-approved indications expand from high-risk to low-risk patient populations (FDA approved low-risk TAVR in 2019. Furthermore, the market is witnessing a surge in innovation for mitral and tricuspid valve therapies (TMVR and TTVR), which represent the next major frontier in structural heart intervention. The prevalence of valvular heart disease increases significantly with age, affecting around 10-13% of individuals aged 75-79 and 14-15% of those aged 80-85 with moderate or greater disease (12.5% overall for 75+), creating a strong demand for durable and effective structural heart solutions.

Despite the rapid technological advancements, the structural heart devices market faces restraints, including the high cost of transcatheter procedures and the stringent regulatory pathways required for new device clearances. The financial burden on healthcare systems for these high-value devices can be a barrier to adoption in price-sensitive regions. Additionally, while minimally invasive, these procedures still carry risks of conduction disturbances and paravalvular leaks, necessitating continuous refinement in device design and delivery systems. However, the emergence of Left Atrial Appendage (LAA) closure devices as an alternative to long-term anticoagulation for stroke prevention in atrial fibrillation patients presents a substantial growth opportunity, with this segment projected to witness some of the highest growth rates in the industry.

The major driver for the structural heart devices market is the aging global population and the subsequent increase in the prevalence of age-related heart conditions. Aortic stenosis and mitral regurgitation are significantly more common in older adults, necessitating the use of structural heart devices for repair or replacement. The American Heart Association (AHA) has highlighted that as the global population continues to age, the burden of valvular heart disease will grow, creating a sustained demand for innovative interventional therapies.

Another key driver is the expansion of clinical indications for transcatheter aortic valve replacement (TAVR). Initially reserved for high-risk surgical patients, TAVR is now increasingly being used for intermediate and low-risk patients based on robust clinical trial data demonstrating its safety and efficacy. This expansion has significantly increased the target patient population for structural heart devices. Furthermore, the continuous improvement in device delivery systems, which are becoming smaller and more flexible, is allowing for safer procedures and broader clinical adoption.

A major restraint is the high cost of structural heart procedures and the associated devices. Transcatheter valves and closure devices are among the most expensive medical technologies, and the total cost of the procedure, including hospitalization and specialized imaging, can be a significant burden on healthcare budgets. In many emerging markets, the lack of adequate reimbursement and the high out-of-pocket costs for patients can limit the adoption of these life-saving technologies. Furthermore, the risk of complications such as stroke or conduction disturbances requiring permanent pacemaker implantation remains a concern for both clinicians and patients.

The development of transcatheter therapies for the mitral and tricuspid valves (TMVR and TTVR) presents a massive growth opportunity. While TAVR is a mature segment, the mitral and tricuspid markets are in the early stages of development and offer significant untapped potential. Additionally, the growth of Left Atrial Appendage (LAA) closure devices as an alternative to long-term oral anticoagulation for stroke prevention in AFib patients is a key opportunity. As more patients seek alternatives to blood thinners, the demand for LAA closure devices is expected to rise sharply.

Navigating the stringent regulatory pathways for new structural heart technologies remains a critical challenge. Manufacturers must provide extensive clinical data to demonstrate long-term safety and durability, which can be a costly and time-consuming process. Furthermore, the shortage of highly trained interventional cardiologists and specialized heart teams in certain regions can limit the availability of structural heart procedures. Ensuring the long-term durability of bio-prosthetic valves compared to mechanical valves also remains a long-term clinical challenge for the industry.

There is a dominant trend toward replacing open-heart surgeries with minimally invasive transcatheter procedures. This shift is driven by the desire for shorter hospital stays, faster recovery times, and reduced procedural complications. The clinical community is increasingly moving toward a 'transcatheter-first' approach for many structural heart conditions, particularly for patients who are at high or intermediate surgical risk. This trend is fueling the rapid adoption of TAVR, TMVR, and percutaneous closure devices.

The integration of advanced 3D imaging, such as transesophageal echocardiography (TEE) and multi-detector computed tomography (MDCT), into the procedural workflow is an emerging trend. These imaging modalities provide detailed anatomical information that is essential for precise device sizing and placement. Furthermore, the use of digital guidance and augmented reality for real-time procedural assistance is gaining traction, improving the accuracy and safety of complex structural heart interventions.

Based on product, the overall structural heart devices market is segmented into Heart Valve Devices, Annuloplasty Rings, Occluders and Closure Devices, and others. In 2026, the heart valve devices segment is expected to hold the largest share of the market. This dominance is due to the established clinical success of TAVR and the high unit cost of transcatheter valves. Heart valve devices are the primary revenue generator for major players in the structural heart market, driven by the high volume of aortic valve replacement procedures.

The occluders and closure devices market is projected to register a significant CAGR during the forecast period. This growth is driven by the rapid expansion of the LAA closure market and the increasing use of septal occluders for treating congenital heart defects like patent foramen ovale (PFO) and atrial septal defect (ASD). The shift away from long-term blood thinners is a major driver for this segment.

North America is expected to dominate the global structural heart devices market in 2026, primarily due to its advanced healthcare infrastructure, high clinical adoption of new technologies, and favorable reimbursement policies. The U.S. is the leading market for structural heart innovation, with a robust ecosystem of technology providers and research institutions. The presence of major industry players like Edwards Lifesciences and Abbott is a key driver. The key companies operating in the North American market are Edwards Lifesciences, Medtronic, Abbott, and Boston Scientific.

The Asia-Pacific structural heart devices market is projected to witness the fastest growth during the forecast period. This is driven by rapid digitalization in healthcare, increasing investments in medical technology in China and India, and a rising geriatric population. The region's large population and the increasing adoption of advanced medical technologies are driving the demand for scalable structural heart solutions. The key companies operating in the Asia-Pacific market are Terumo, Lepu Medical, Microport, and various emerging medical technology specialists in the region.

The global structural heart devices market is characterized by intense competition and a high degree of innovation. The competitive landscape is dominated by a few major medical device giants who have secured early regulatory approvals and are leveraging their extensive distribution networks to drive adoption. Edwards Lifesciences, Medtronic, and Abbott currently lead the market, having pioneered the TAVR and transcatheter mitral repair segments. These companies are actively investing in clinical trials to expand the indications for their devices and are acquiring specialized startups to bolster their technology portfolios.

In addition to the large incumbents, the market features several specialized companies focused on next-generation structural heart technologies, particularly for the mitral and tricuspid valves. The competitive landscape is also shaped by strategic partnerships between device manufacturers and imaging system providers. As the market evolves, the focus is shifting toward providing complete procedural solutions, including pre-procedural planning software and post-procedural monitoring. Key players in the global structural heart devices market include Edwards Lifesciences Corporation, Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Johnson & Johnson, and Terumo Corporation.

The market is projected to reach USD 48.2 billion by 2036, growing at a CAGR of 11.2% from 2026 to 2036.

The heart valve devices segment is expected to hold the largest share in 2026 due to the success of TAVR.

The aging global population and the rising prevalence of valvular heart disease are the primary drivers.

Asia-Pacific is projected to witness the highest CAGR due to rapid healthcare expansion and a rising geriatric population.

TAVR offers a minimally invasive alternative with shorter recovery times and reduced procedural risks for many patients.

Challenges include the high cost of transcatheter procedures and stringent regulatory approval processes.

LAA closure is a high-growth segment as it offers a safe alternative to long-term anticoagulation for AFib patients.

Yes, TMVR and TTVR are emerging as the next major growth areas for structural heart intervention.

Advanced imaging is essential for precise device sizing, procedural planning, and real-time guidance.

Leading companies include Edwards Lifesciences, Medtronic, Abbott, Boston Scientific, and Terumo.

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Dec-2017

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates