Resources

About Us

Left Atrial Appendage Closure (LAAC) Devices Market Size, Share & Trends Analysis by Product Type (Endocardial (Transcatheter), Epicardial (Surgical)), End User, Application, and Geography – Global Opportunity Analysis and Industry Forecast (2026–2036)

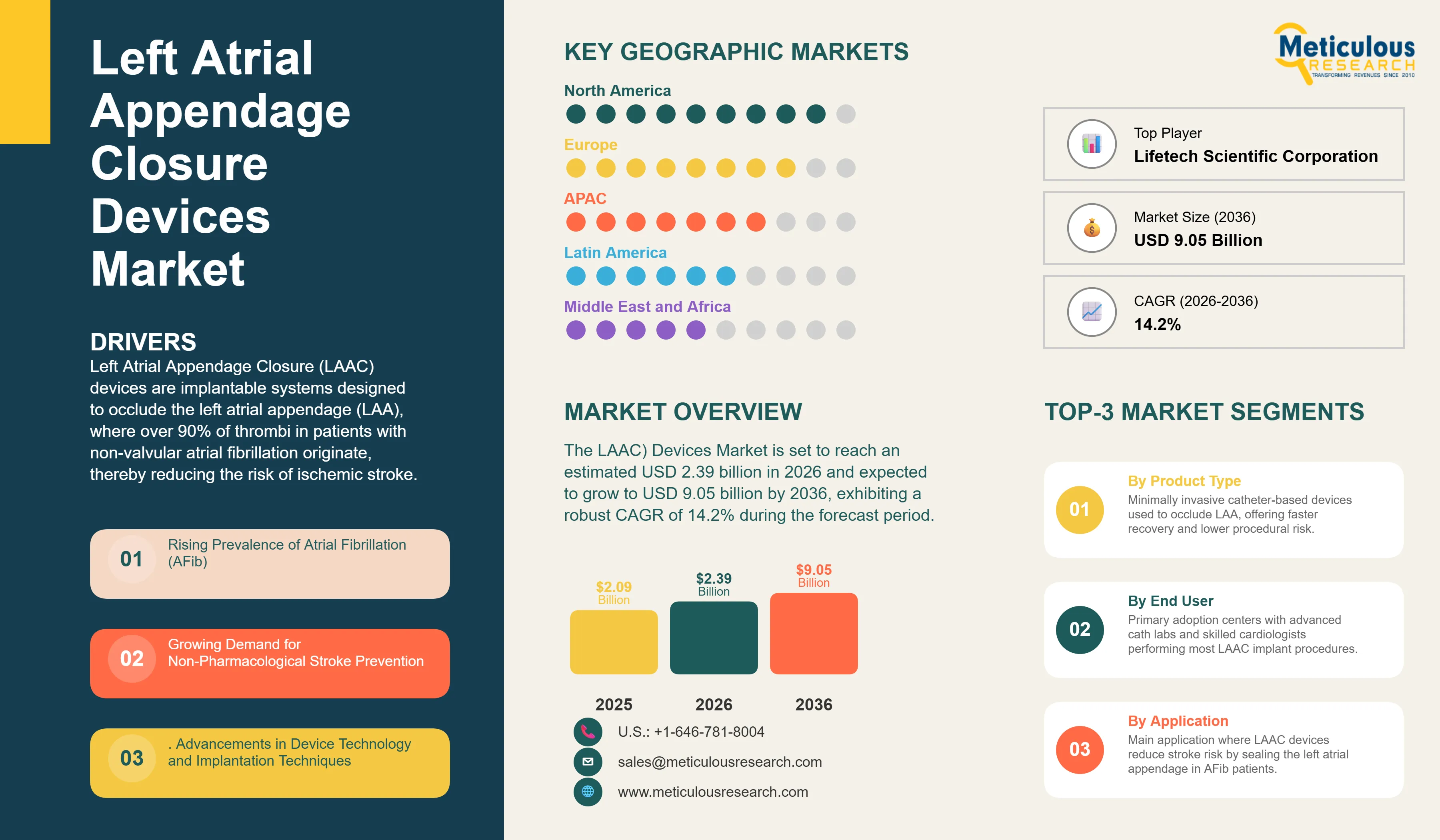

Report ID: MRHC - 1042094 Pages: 297 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global Left Atrial Appendage Closure (LAAC) Devices Market is projected to reach an estimated USD 2.39 billion in 2026 and is expected to grow significantly to USD 9.05 billion by 2036, exhibiting a robust Compound Annual Growth Rate (CAGR) of 14.2% during the forecast period.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Left Atrial Appendage Closure (LAAC) devices are implantable systems designed to occlude the left atrial appendage (LAA), where over 90% of thrombi in patients with non-valvular atrial fibrillation originate, thereby reducing the risk of ischemic stroke. With more than 60 million people worldwide living with atrial fibrillation and AF contributing to approximately one in seven strokes in the U.S., LAAC has become an important treatment option for patients who are unsuitable for long-term oral anticoagulation because of bleeding risks or other contraindications.

The market comprises endocardial (transcatheter) and epicardial (surgical) LAAC devices. Growing recognition of the LAA as the primary source of cardioembolic stroke, coupled with advances in device design, minimally invasive implantation techniques, and expanding clinical evidence supporting safety and efficacy, continues to accelerate adoption. As guideline recommendations and reimbursement improve, LAAC devices are increasingly becoming a standard non-pharmacological strategy for stroke prevention in eligible atrial fibrillation patients.

Drivers: Catalysts for LAAC Devices Market Growth

Rising Prevalence of Atrial Fibrillation (AFib): The increasing global incidence and prevalence of atrial fibrillation, particularly in the aging population, is a primary driver for the LAAC devices market, as AFib is a major risk factor for stroke.

Growing Demand for Non-Pharmacological Stroke Prevention: For AFib patients unsuitable for long-term oral anticoagulation due to high bleeding risk or other contraindications, LAAC devices offer a vital non-pharmacological alternative for stroke prevention.

Advancements in Device Technology and Implantation Techniques: Continuous innovations in LAAC device design, including improved conformability, deliverability, and reduced profile, along with refined transcatheter implantation techniques, are enhancing procedural safety and efficacy.

Increasing Clinical Evidence and Favorable Reimbursement Policies: A growing body of clinical data demonstrating the long-term safety and effectiveness of LAAC devices, coupled with expanding reimbursement coverage in key regions, is accelerating market adoption.

Restraints: Navigating the Hurdles to LAAC Devices Adoption

High Cost of LAAC Procedures: The significant cost associated with LAAC devices and the implantation procedure can be a barrier to widespread adoption, particularly in healthcare systems with budget constraints or for patients without adequate insurance coverage.

Risk of Procedure-Related Complications: While improving, LAAC procedures carry inherent risks of complications such as pericardial effusion, device embolization, and stroke, which can limit their broader acceptance.

Requirement for Specialized Expertise and Infrastructure: The successful implantation of LAAC devices demands highly specialized interventional cardiologists and dedicated cardiac catheterization lab infrastructure, limiting access in some regions.

Competition from Oral Anticoagulants: Despite their limitations, oral anticoagulants remain the first-line therapy for stroke prevention in many AFib patients, posing a competitive challenge to the LAAC devices market.

Opportunities: Unlocking New Avenues for LAAC Devices Growth

Expansion of Indications for LAAC Devices: Opportunities exist for expanding the indications for LAAC devices to a broader patient population, including those with lower bleeding risk or specific anatomical considerations, following further clinical research.

Development of Next-Generation Devices: The development of novel LAAC devices with enhanced safety profiles, easier deliverability, improved conformability to diverse LAA anatomies, and reduced procedural complexity presents significant market opportunities.

Increasing Awareness and Physician Education: Greater awareness among cardiologists and primary care physicians about the benefits and appropriate patient selection for LAAC procedures can drive increased referrals and market growth.

Geographic Expansion into Emerging Markets: As healthcare infrastructure improves and the prevalence of AFib rises in developing economies, these regions present significant untapped market potential for LAAC device manufacturers.

Challenges: Overcoming Obstacles in the LAAC Devices Market

Patient Selection and Referral Pathways: Identifying the optimal patient population for LAAC procedures and establishing clear, efficient referral pathways remain challenges, requiring multidisciplinary collaboration.

Long-Term Data on Device Durability and Efficacy: While short-to-medium term data is robust, continuous collection of long-term data on device durability, efficacy in stroke prevention, and potential late complications is crucial for sustained market growth.

Training and Skill Development for Interventionalists: Ensuring adequate training and skill development for a growing number of interventional cardiologists to perform LAAC procedures safely and effectively is a continuous challenge.

Regulatory Hurdles for New Device Approvals: The rigorous regulatory approval process for novel medical devices, particularly those implanted in the heart, can be lengthy and costly, posing a challenge for new market entrants.

The global LAAC devices market is being shaped by the rapid adoption of transcatheter LAAC devices, supported by expanding clinical evidence and updated guideline recommendations. According to the 2023 American College of Cardiology (ACC), American Heart Association (AHA), American College of Chest Physicians (ACCP), and Heart Rhythm Society (HRS) Atrial Fibrillation Guideline, percutaneous LAAC received an upgraded recommendation (Class IIa) for patients with non-valvular atrial fibrillation who have contraindications to long-term oral anticoagulation, accelerating physician confidence and procedural adoption. Device manufacturers are also focusing on miniaturized delivery systems, enhanced conformability, and improved sealing mechanisms to improve procedural success and minimize peri-device leaks and device-related thrombus.

Another key trend is the increasing use of advanced cardiac imaging, including transesophageal echocardiography (TEE) and cardiac CT, to enable patient-specific LAA anatomical assessment and optimize device sizing and placement. Simultaneously, ongoing trials such as CHAMPION-AF and CATALYST are evaluating LAAC as a first-line alternative to direct oral anticoagulants in broader patient populations, potentially expanding future indications. Coupled with the fact that more than 90% of thrombi in patients with non-valvular atrial fibrillation originate in the left atrial appendage (European Society of Cardiology), these developments continue to strengthen the clinical adoption of LAAC devices worldwide.

Analysis by Product Type: Endocardial Devices Leading the Way

Based on product type, the endocardial (transcatheter) LAAC devices segment is expected to hold the largest share of the global LAAC devices market. This dominance is attributed to their minimally invasive nature, which offers significant advantages over surgical approaches, including reduced patient recovery time and lower procedural risks. The epicardial (surgical) LAAC devices segment is anticipated to witness a steady CAGR, particularly in conjunction with other cardiac surgeries, offering a complementary approach for LAA management.

Analysis by End User: Hospitals as Primary Adoption Centers

Based on end user, hospitals are expected to command the largest share of the global LAAC devices market. This is due to hospitals being the primary facilities equipped with the necessary infrastructure, specialized cardiac catheterization labs, and interventional cardiology expertise required for performing LAAC procedures. The ambulatory surgical centers (ASCs) segment is anticipated to exhibit the fastest CAGR, driven by the increasing shift towards outpatient procedures and the potential for cost-effectiveness in suitable patient populations.

Analysis by Application: Stroke Prevention in Atrial Fibrillation Dominating

Based on application, the stroke prevention in atrial fibrillation segment is projected to account for the largest share of the LAAC devices market. This is the primary and most established indication for LAAC devices, addressing the critical need to reduce stroke risk in AFib patients who cannot tolerate oral anticoagulants. The other applications segment (e.g., for patients with contraindications to long-term anticoagulation due to other medical conditions) is expected to grow at a significant CAGR as research expands the utility of LAAC devices.

North America: A Leader in Advanced Cardiovascular Interventions

North America is expected to hold the largest share of the global LAAC Devices market. This dominance is attributed to a high prevalence of atrial fibrillation, well-established healthcare infrastructure, significant investments in cardiovascular research and technology, the presence of numerous key market players, and favorable reimbursement policies for LAAC procedures. The United States, in particular, is a major contributor due to its large patient population and strong adoption of advanced interventional cardiology techniques.

Europe: Advancing Stroke Prevention Strategies with Robust Healthcare Systems

Europe is expected to hold a significant share of the global LAAC Devices market, driven by a growing aging population susceptible to AFib, well-established healthcare systems, increasing awareness about stroke prevention alternatives, and supportive regulatory frameworks. Countries like Germany, the U.K., and France are key contributors due to their advanced medical facilities and the presence of leading medical device manufacturers. The key companies operating in the European market are Boston Scientific Corporation, Abbott Laboratories, and Medtronic plc.

Asia-Pacific: Rapid Growth Fueled by Rising AFib Prevalence and Healthcare Modernization

Asia-Pacific is projected to witness the fastest CAGR during the forecast period. This rapid growth is driven by a large and aging population, increasing prevalence of atrial fibrillation, improving healthcare infrastructure, and growing awareness about advanced cardiovascular interventions in countries like China, Japan, and India. Government initiatives to combat cardiovascular diseases, coupled with the expanding presence of international medical device companies, also contribute to the region's market expansion. The key companies operating in the Asia-Pacific market are Boston Scientific Corporation (with regional presence), Abbott Laboratories (with regional presence), and Lifetech Scientific Corporation.

Latin America: Emerging Opportunities in Cardiovascular Device Adoption

Latin America is anticipated to witness steady growth in the LAAC Devices market, primarily due to increasing investments in healthcare infrastructure, a rising focus on improving cardiovascular care outcomes, and growing awareness about AFib and stroke prevention in countries like Brazil and Mexico. The modernization of medical facilities and the adoption of international guidelines for cardiovascular interventions also contribute to the demand for LAAC devices. The key companies operating in the Latin American market are Boston Scientific Corporation (with regional presence) and Abbott Laboratories (with regional presence).

Middle East & Africa: Gradual Expansion with Developing Healthcare Sectors

The Middle East & Africa region is expected to experience gradual growth in the LAAC Devices market, driven by increasing healthcare investments, government initiatives to develop local medical capabilities, and a growing focus on adopting advanced cardiovascular technologies. Countries like UAE and Saudi Arabia are investing in cardiovascular research and treatment, leading to a gradual increase in demand for LAAC devices. The key companies operating in the Middle East & Africa market are Boston Scientific Corporation (with regional presence) and Abbott Laboratories (with regional presence).

The global Left Atrial Appendage Closure (LAAC) Devices market is characterized by a dynamic and highly competitive landscape. It features a mix of large, diversified medical device companies and specialized cardiovascular technology firms. Key players are focusing on expanding their product portfolios, investing in R&D for next-generation devices with improved safety and efficacy, offering comprehensive physician training programs, and forming strategic collaborations or acquisitions to strengthen their market positions. The competitive strategy often revolves around demonstrating clinical superiority, ensuring regulatory approvals, providing robust post-market surveillance, and offering integrated solutions for stroke prevention in AFib patients. Companies are also investing heavily in expanding their geographic reach and increasing patient and physician awareness about the benefits of LAAC procedures.

The global LAAC Devices market is estimated at USD 2.39 billion in 2026 and is projected to reach USD 9.05 billion by 2036, growing at a CAGR of 14.2%.

The market is driven by the rising prevalence of atrial fibrillation, growing demand for non-pharmacological stroke prevention, advancements in device technology, and increasing clinical evidence and favorable reimbursement policies.

Key restraints include the high cost of LAAC procedures, risk of procedure-related complications, requirement for specialized expertise and infrastructure, and competition from oral anticoagulants.

Opportunities include expansion of indications, development of next-generation devices, increasing awareness and physician education, and geographic expansion into emerging markets.

Challenges include patient selection and referral pathways, long-term data on device durability and efficacy, training and skill development for interventionalists, and regulatory hurdles for new device approvals.

Endocardial (transcatheter) LAAC devices hold the largest share, while epicardial (surgical) LAAC devices are anticipated to witness a steady CAGR.

Which end-user segment accounts for the largest share, and which is anticipated to grow the fastest?

Hospitals hold the largest share, and ambulatory surgical centers (ASCs) are anticipated to exhibit the fastest CAGR.

Stroke prevention in atrial fibrillation accounts for the largest share, and other applications are expected to grow at a significant CAGR.

North America leads the market, and Asia-Pacific is projected to witness the fastest CAGR.

Key players include Boston Scientific Corporation, Abbott Laboratories, Medtronic plc, Johnson & Johnson, AtriCure, Inc., Lifetech Scientific Corporation, Occlutech AG, and Cardia, Inc.

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates